Figure 10.1 Reverse Merger Process

Coinciding with the closing date, CCAC completed a private placement of 3.1 million common shares at a

purchase price of $5 to investors consisting of some CCAC’s existing shareholders realizing proceeds of $15.5

million. In connection with the private placement, CCAC agreed to register the shares with the Securities and

Exchange Commission within 120 days of closing. This activity is sometimes called private investment in public

equity or PIPE financing.

Companies that become public through a reverse merger with a shell company are not permitted to list on a

major public securities exchange until certain conditions have been satisfied. The new firm must complete a one–

year “seasoning period” in the U.S. by trading over the counter market or another regulated U.S. or foreign stock

exchange following a reverse merger and be registered with the SEC. The shares must maintain a minimum share

price required by the exchange for a sustained period for at least 30 to 60 trading days.

Concluding Comments

One Group had the choice of remaining private or taking STK public. Each ownership structure has its pros and

cons. For example, after twenty years as a publicly traded company, Dell Inc. converted from to a private

corporation. While gaining access to additional capital, STK will face new challenges as a public company. To go

public, One Group chose a reverse merger from a range of options. While sometimes effective, reverse mergers

often create more problems than alternative strategies.

Discussion Questions

1. What are common reasons for a private firm to go public? What are the advantages and disadvantages or

doing so? Be specific.

2. What are corporate shells, and how can they create value? Be specific.

CCAC Acquisition Sub

(Merger Sub)

Cash &

CCAC

Common

Shares

Merger Sub

Shares

Cash & CCAC

Common Shares

Common Shares

One Group Becomes

Wholly-Owned CCAC Sub

Membership Interests

3. What were the options available to One Group LLC to raise capital to finance their expansion plans? Discuss

the pros and cons of each. Be specific.

4. Discuss the pros and cons of a reverse merger versus an IPO.

5. Why is it likely that shares trade at a discount from their value when issued if investors attempted to sell

such shares within one year following closing of the reverse merger?

23

6. What is the purpose of ultimately listing of a major stock exchange such as NASDAQ?

Shell Game: Going Public through Reverse Mergers

___________________________________________________________________________________________

Key Points

Reverse mergers represent an alternative to an initial public offering (IPO) for a private company wanting to “go

public.”

The challenge with reverse mergers often is gaining access to accurate financial statements and quantifying current

or potential liabilities.

Performing adequate due diligence may be difficult, but it is the key to reducing risk.

______________________________________________________________________________

The highly liquid U.S. equity markets have proven to be an attractive way of gaining access to capital for both

privately owned domestic and foreign firms. Common ways of doing so have involved IPOs and reverse mergers.

While both methods allow the private firm’s shares to be publicly traded, only the IPO necessarily results in raising

capital, which affects the length of time and complexity of the process of “going–public.”

To undertake a reverse merger, a firm finds a shell corporation with relatively few shareholders who are

interested in selling their stock. The shell corporation’s shareholders often are interested in either selling their shares

for cash, owning even a relatively small portion of a financially viable company to recover their initial investments,

or transferring the shell’s liabilities to new investors. Alternatively, the private firm may merge with an existing

special-purpose acquisition company (SPAC) already registered for public stock trading. SPACs are shell, or

“blank–check,” companies that have no operations but go public with the intention of merging with or acquiring a

company with the proceeds of the SPAC’s IPO.

In a merger, it is common for the surviving firm to be viewed as the acquirer, since its shareholders usually end

up with a majority ownership stake in the merged firms; the other party to the merger is viewed as the target firm

because its former shareholders often hold only a minority interest in the combined companies. In a reverse merger,

the opposite happens. Even though the publicly traded shell company survives the merger, with the private firm

becoming its wholly owned subsidiary, the former shareholders of the private firm end up with a majority ownership

stake in the combined firms. While conventional IPOs can take months to complete, reverse mergers can take only a

few weeks. Moreover, as the reverse merger is solely a mechanism to convert a private company into a public entity,

the process is less dependent on financial market conditions because the company often is not proposing to raise

capital.

The speed with which a firm can “go public” as compared to an IPO often is attractive to foreign firms desirous

of entering U.S. capital markets quickly. In recent years, private equity investors have found the comparative ease of

the reverse merger process convenient, because it has enabled them to take public their investments in both domestic

24

and foreign firms. In recent years the story of the rapid growth of Chinese firms has held considerable allure for

investors, prompting a flurry of reverse mergers involving Chinese-based firms. With speed comes additional risk.

Shell company shareholders may simply be looking for investors to take over their liabilities, such as pending

litigation, safety hazards, environmental problems, and unpaid tax liabilities. To prevent the public shell’s

shareholders from dumping their shares immediately following the merger, investors are required to hold their

shares for a specific period of time. The recent entry of Chinese firms into the U.S. public equity markets illustrates

the potential for fraud. Of the 159 Chinese–based firms that have been listed since 2006 via a reverse merger, 36

have been suspended or have halted trading in the United States after auditors found significant accounting issues.

Eleven more firms have been delisted from major U.S. stock exchanges.

Huiheng Medical (Huiheng) is one such firm that came under SEC scrutiny, having first listed its shares on the

over-the-counter (OTC) market in early 2008. The firm claimed it was China’s leading provider of gamma-ray

technology, a cancer-fighting technology, and boasted of having a strong order backlog and access to Western

management expertise through a joint venture. What follows is a discussion of how the firm went public and the

participants in that process. The firms involved in the reverse merger process included Mill Basin Technologies

(Mill), a Nevada incorporated and publicly listed shell corporation, and Allied Moral Holdings (Allied), a privately

owned Virgin Islands company with subsidiaries, including Huiheng Medical, primarily in China. Mill was the

successor firm to Pinewood Imports (Pinewood), a Nevada-based corporation, formed in November 2002 to import

pine molding. Ceasing operations in September 2006 to become a shell corporation, Pinewood changed its name to

Mill Basin Technologies. The firm began to search for a merger partner and registered shares for public trading in

2006 in anticipation of raising funds.

The reverse merger process employed by Allied, the privately owned operating company and owner of Huiheng,

to merge with Mill, the public shell corporation, early in 2008 to become a publicly listed firm is described in the

following steps. Allied is the target firm, and Mill is the acquiring firm.

Step 1. Negotiate terms and conditions: Premerger, Mill and Allied had 10,150,000 and 13,000,000 common

shares outstanding, respectively. Mill also had 266,666 preferred shares outstanding. Mill and Allied agreed to a

merger in which each Allied shareholder would receive one share of Mill stock for each Allied share they held. With

Mill as the surviving entity, former Allied shareholders would own 96.65% of Mill’s shares, and Mill’s former

shareholders would own the rest.

Step 2. Recapitalize the acquiring firm: Prior to the share exchange, shareholders in Mill, the shell corporation,

recapitalized the firm by contributing 9,700,000 of the shares they owned prior to the merger to Treasury stock,

effectively reducing the number of Mill common shares outstanding to 450,000 (10,150,000 – 9,700,000). The

objective of the recapitalization was to limit the total number of common shares outstanding postmerger in order to

support the price of the new firm’s shares. Such recapitalizations often are undertaken to reduce the number of

shares outstanding following closing in order to support the combined firms’ share price once it begins to trade on a

public exchange.4 The firm’s earnings per share are increased for a given level of earnings by reducing the number

of common shares outstanding.

Step 3. Close the deal: The terms of the merger called for Mill (the acquirer) to purchase 100% of the outstanding

Allied (the target) common and preferred shares, which required Mill to issue 13,000,000 new common shares and

266,666 new preferred shares. All premerger Allied shares were cancelled. Mill Basin Technologies was renamed

Huiheng Medical, reflecting potential investor interest at that time in both Chinese firms and in the healthcare

industry. See Exhibit 10.4 for an illustration of the premerger recapitalization of Mill, the postmerger equity

structure of the combined firms, and the resulting ownership distribution.

While Huiheng traded as high as $13 in late 2008, it plummeted to $1.60 in early 2012, reflecting the failure of

the firm to achieve any significant revenue and income in the cancer market, an inability to get an auditing firm to

approve their financial statements, and the absence of any significant order backlog. Having reported net income as

high as $9 million in 2007, just prior to completing the reverse merger, the firm was losing money and burning

4 Without the reduction in Mill’s premerger shares outstanding, total shares outstanding postmerger would have

been 23,150,000 [10,150,000 (Mill shares premerger) + 13,000,000 (Allied shares premerger)] rather than the

13,450,000 after the recapitalization.

25

through its remaining cash. The firm was left looking at alternative applications for its technology, such as

preserving food with radiation.

Huiheng’s SEC filings state that the firm designs, develops, and markets radiation therapy systems used to treat

cancer and acknowledge that the firm had experienced delays selling its technology in China and had no

international sales in 2009 or 2010. The filings also show the reverse merger was directed by Richard Propper, a

venture capitalist and CEO of Chardan Capital, a San Diego merchant bank with expertise in helping Chinese firms

enter the U.S. equity markets. Chardan Capital invested $10 million in Huiheng in exchange for more than 52,000

shares of the firm’s preferred stock. Chardan and Roth Capital Partners, a California investment bank, were co–

underwriters for a planned 2008 Huiheng stock offering that was later withdrawn. Chardan had been fined $40,000

for three violations of short–selling rules from 2005 to 2009. Roth is a defendant in alleged securities’ fraud lawsuits

involving other Chinese reverse merger firms.5

Exhibit 10.4 Mill Basin Technologies (Mill)

Pre-Merger Equity Structure:

Common 10,150,000

Series A Preferred 266,666

Recapitalized Equity Structure

Common 450,000a

Series A Preferred 266,666

New Mill Shares Issued to Acquire 100% of Allied shares

Common 13,000,000

Series A Preferred 266,666

Post-Merger Equity Structure:

Common 13,450,000b

Series A Preferred 266,666

Post-Merger Ownership Distribution of Common Shares:

Former Allied Shareholders: 96.65% c

Former Mill Shareholders: 3.35%

aMill shareholders contributed 9,700,000 shares of their pre-merger holdings to treasury stock cutting the

number of Mill shares outstanding to 450,000 in order to reduce the total number of shares outstanding

postmerger, which would equal Mill’s premerger shares outstanding plus the newly issued shares. This also

could have been achieved by the Mill shareholders agreeing to a reverse stock split. The 10,150,000 pre–

merger Mill shares outstanding could be reduced to 450,000 through a reverse split in which Mill

shareholders receive 1 new Mill share for each 22.555 outstanding prior to the merger.

bPost-Merger Mill Basin Technologies’ capital structure equals the 450,000 premerger Mill common shares

resulting from the recapitalization plus the 13,000,000 newly issued common shares plus 266,666 Series A

preferred shares.

c(13,000,000/13,450,000)

Huiheng ran into legal problems soon after its reverse merger. Harborview Master Fund, Diverse Trading Ltd.,

and Monarch Capital Fund, institutional investors having a controlling interest in Huiheng, approved the reverse

merger and invested $1.25 million in exchange for stock. However, they sued Huiheng and Chardan Capital in 2009

as Huiheng’s promise of orders failed to materialize. The lawsuit charged that Huiheng bribed Chinese hospital

officials to win purchasing deals. The firm’s initial investors forced the firm to buy back their shares as a result of a

legal settlement of their lawsuit in which they argued that the firm had committed fraud when it “went public.” The

lawsuit alleged that the firm’s public statements about the efficacy of its technology and order backlog were highly

inflated. Huiheng and its codefendants settled out of court in 2010 with no admission of liability by buying back

some of its stock. In 2011, the firm had difficulty in collecting receivables and generating cash. That same year,

Huiheng’s operations in China were struggling and were on the verge of ceasing production.

Discussion Questions

5 McCoy and Chu, December 26, 2011

1. What are common reasons for a private firm to go public?

2. What is a corporate shell and how can they create value?

3. Who are the key participants in the case study and what are their roles in the reverse merger?

4. Discuss the pros and cons of a reverse merger versus an initial public offering for taking a company public.

27

5. What are the auditing challenges associated with reverse mergers? How can investors protect themselves

from the liabilities that may be contained in corporate shells?

6. Mill was recapitalized just prior to completing its merger with Allied. What was the purpose of the

recapitalization? Did it affect the ability of the combined firm’s to generate future earnings? Explain your

answers.

Determining Liquidity Discounts: The Taylor Devices and Tayco Development Merger

____________________________________________________________________________________________

Key Points

Privately held shares or shares for which there is not a readily available resale market often can only be sold at a

discount from what is believed to be their intrinsic value.

However, estimating the magnitude of the discount often is highly problematic.

____________________________________________________________________________________________

This discussion6 is a highly summarized version of how a business valuation firm evaluated the liquidity risk

associated with Taylor Devices’ unregistered common stock, registered common shares, and a minority investment

in a business that it was planning to sell following its merger with Tayco Development. The estimated liquidity

discounts were used in a joint proxy statement submitted to the SEC by the two firms to justify the value of the offer

the boards of Taylor Devices and Tayco Development had negotiated.

Taylor Devices and Tayco Development agreed to merge in early 2008. Tayco would be merged into Taylor,

with Taylor as the surviving entity. The merger would enable Tayco’s patents and intellectual property to be fully

integrated into Taylor’s manufacturing operations, since intellectual property rights transfer with the Tayco stock.

Each share of Tayco common stock would be converted into one share of Taylor common stock, according to the

terms of the deal. Taylor’s common stock is traded on the NASDAQ Small Cap Market under the symbol TAYD,

and on January 8, 2009 (the last trading day before the date of the filing of the joint proxy statement with the SEC),

the stock closed at $6.29 per share. Tayco common stock is traded over the counter on “Pink Sheets” (i.e., an

informal trading network) under the trading symbol TYCO.PK, and it closed on January 8, 2009, at $5.11 per share.

6 Source: SEC Form S4 filing of a proxy statement for Taylor Devices and Tayco Development dated 1/15/08.

An appraisal firm was hired to value Taylor’s unregistered shares, which were treated as if they were restricted

shares because there was no established market for trading in these shares. The appraiser believed that the risk of

Taylor’s unregistered shares is greater than for letter stocks, which have a stipulated period during which the shares

cannot be sold, because the Taylor shares lacked a date indicating when they could be sold. Using this line of

reasoning, the appraisal firm estimated a liquidity discount of 20%, which it believed approximated the potential

loss that holders of these shares might incur in attempting to sell their shares. The block of registered Taylor stock

differs from the unregistered shares, in that they are not subject to Rule 144. Based on the trading volume of Taylor

common stock over the preceding 12 months, the appraiser believed that it would likely take less than one year to

convert the block of registered stock into cash and estimated the discount at 13%, consistent with the Aschwald

(2000) studies.

The appraisal firm also was asked to estimate the liquidity discount for the sale of Taylor’s minority investment

in a real estate development business. Due to the increase in liquidity of restricted stocks since 1990, the business

appraiser argued that restricted-stock studies conducted before that date may provide a better proxy for liquidity

discounts for this type of investment. Interests in closely held firms are more like letter-stock transactions occurring

before the changes in SEC Rule 144 beginning in 1990, when the holding period was reduced from three years to

two and later (after 1997) to one. Such firms have little ability to raise capital in public markets due to their small

size, and they face high transaction costs. Based on the SEC and other prior 1990 studies, the liquidity discount for

this investment was expected to be between 30% and 35%. Pre-IPO studies could push it higher to a range of 40–

45%. The appraisal firm argued that the discount for most minority-interest investments tended to fall in the range of

25–45%. Because of the small size of the real estate development business, the liquidity discount is believed by the

appraisal firm to be at the higher end of the range.

Discussion Questions

1. Explain how the appraiser estimated the liquidity discount for Taylor’s unregistered shares.

2. What other factors could the appraiser have used to estimate the liquidity discount on the unregistered

stock?

3. In view of your answer to question 2, how might these factors have changed the appraiser’s conclusions?

Be specific.

4. Based on the estimated liquidity discount of 13 percent estimated by the business appraiser, what was the

actual purchase price premium paid to Tayco shareholders?

29

Taking Advantage of a “Cupcake Bubble”

__________________________________________________________________________________________

Key Points

Financing growth represents a common challenge for most small businesses.

Selling a portion of the business either to private investors or in a public offering represents a common way for

small businesses to finance major expansion plans.

____________________________________________________________________________

When Crumbs first opened in 2003 on the upper west side of Manhattan, the bakery offered three varieties of

cupcakes among 150 other items. When the cupcakes became increasingly popular, the bakery began introducing

cupcakes with different toppings and decorations. The firm’s founders, Jason and Mia Bauer, followed a

straightforward business model: Hold costs down, and minimize investment in equipment. Although all of Crumbs’

cupcake recipes are Mia Bauer’s, there are no kitchens or ovens on the premises. Instead, Crumbs outsources all of

the baking activities to commercial facilities. The firm avoids advertising, preferring to give away free cupcakes

when it opens a new store and to rely on “word of mouth.” By keeping costs low, the firm has expanded without

adding debt. The firm targets locations with high daytime “foot traffic,” such as urban markets. In 2010, the firm

sold 13 million cupcakes through 34 locations, accounting for $31 million in revenue and $2.5 million in earnings

before interest, taxes, and depreciation. Crumbs’ success spawned a desire to accelerate growth by opening up as

many as 200 new locations by 2014. The challenge was how to finance such a rapid expansion.

The Bauers were no strangers to raising capital to finance the ongoing growth of their business, having sold one–

half of the firm to Edwin Lewis, former CEO of Tommy Hilfiger, for $10 million in 2008. This enabled them to

reinvest a portion in the business to sustain growth as well as to draw cash out of the business for their personal use.

However, this time the magnitude of their financing requirements proved daunting. The couple was reluctant to

burden the business with excessive debt, well aware that this had contributed to the demise of so many other rapidly

growing businesses. Equity could be sold directly in the private placement market or to the public. Private

placements could be expensive and may not provide the amount of financing needed; tapping the public markets

directly through an IPO required dealing with underwriters and a level of financial expertise they lacked. Selling to

another firm seemed to satisfy best their primary objectives: Get access to capital, retain their top management

positions, and utilize the financial expertise of others to tap the public capital markets and to share in any future

value creation.

The 57th Street General Acquisition Corporation (57th Street), a special-purpose acquisition company, or SPAC,

appeared to meet their needs. In May 2010, 57th Street raised $54.5 million through an IPO, with the proceeds

placed in a trust pending the completion of planned acquisitions.7 One year later, 57th Street announced it had

acquired Crumbs for $27 million in cash and $39 million in 57th Street stock. On June 30, 2011, 57th announced

that NASDAQ had approved the listing of its common stock, giving Crumbs a market value of nearly $60 million.

Panda Ethanol Goes Public in a Shell Corporation

In early 2007, Panda Ethanol, owner of ethanol plants in west Texas, decided to explore the possibility of taking its

ethanol production business public to take advantage of the high valuations placed on ethanol-related companies in

the public market at that time. The firm was confronted with the choice of taking the company public through an

initial public offering or by combining with a publicly traded shell corporation through a reverse merger.

After enlisting the services of a local investment banker, Grove Street Investors, Panda chose to “go public”

through a reverse merger. This process entailed finding a shell corporation with relatively few shareholders who

were interested in selling their stock. The investment banker identified Cirracor Inc. as a potential merger partner.

Cirracor was formed on October 12, 2001, to provide website development services and was traded on the over-the-

counter bulletin board market (i.e., a market for very low-priced stocks). The website business was not profitable,

and the company had only ten shareholders. As of June 30, 2006, Cirracor listed $4,856 in assets and a negative

7 SPACs are shell, or blank-check, companies that have no operations but go public with the intention of merging

with or acquiring a company with the proceeds of the SPAC’s initial public offering.

shareholders’ equity of $(259,976). Given the poor financial condition of Cirracor, the firm’s shareholders were

interested in either selling their shares for cash or owning even a relatively small portion of a financially viable

company to recover their initial investments in Cirracor. Acting on behalf of Panda, Grove Street formed a limited

liability company, called Grove Panda, and purchased 2.73 million Cirracor common shares, or 78 percent of the

company, for about $475,000.

The merger proposal provided for one share of Cirracor common stock to be exchanged for each share of Panda

Ethanol common outstanding stock and for Cirracor shareholders to own 4 percent of the newly issued and

outstanding common stock of the surviving company. Panda Ethanol shareholders would own the remaining 96

percent. At the end of 2005, Panda had 13.8 million shares outstanding. On June 7, 2007, the merger agreement was

amended to permit Panda Ethanol to issue 15 million new shares through a private placement to raise $90 million.

This brought the total Panda shares outstanding to 28.8 million. Cirracor common shares outstanding at that time

totaled 3.5 million. However, to achieve the agreed-on ownership distribution, the number of Cirracor shares

outstanding had to be reduced. This would be accomplished by an approximate three-for-one reverse stock split

immediately prior to the completion of the reverse merger (i.e., each Cirracor common share would be converted

into 0.340885 shares of Cirracor common stock). As a consequence of the merger, the previous shareholders of

Panda Ethanol were issued 28.8 million new shares of Cirracor common stock. The combined firm now has 30

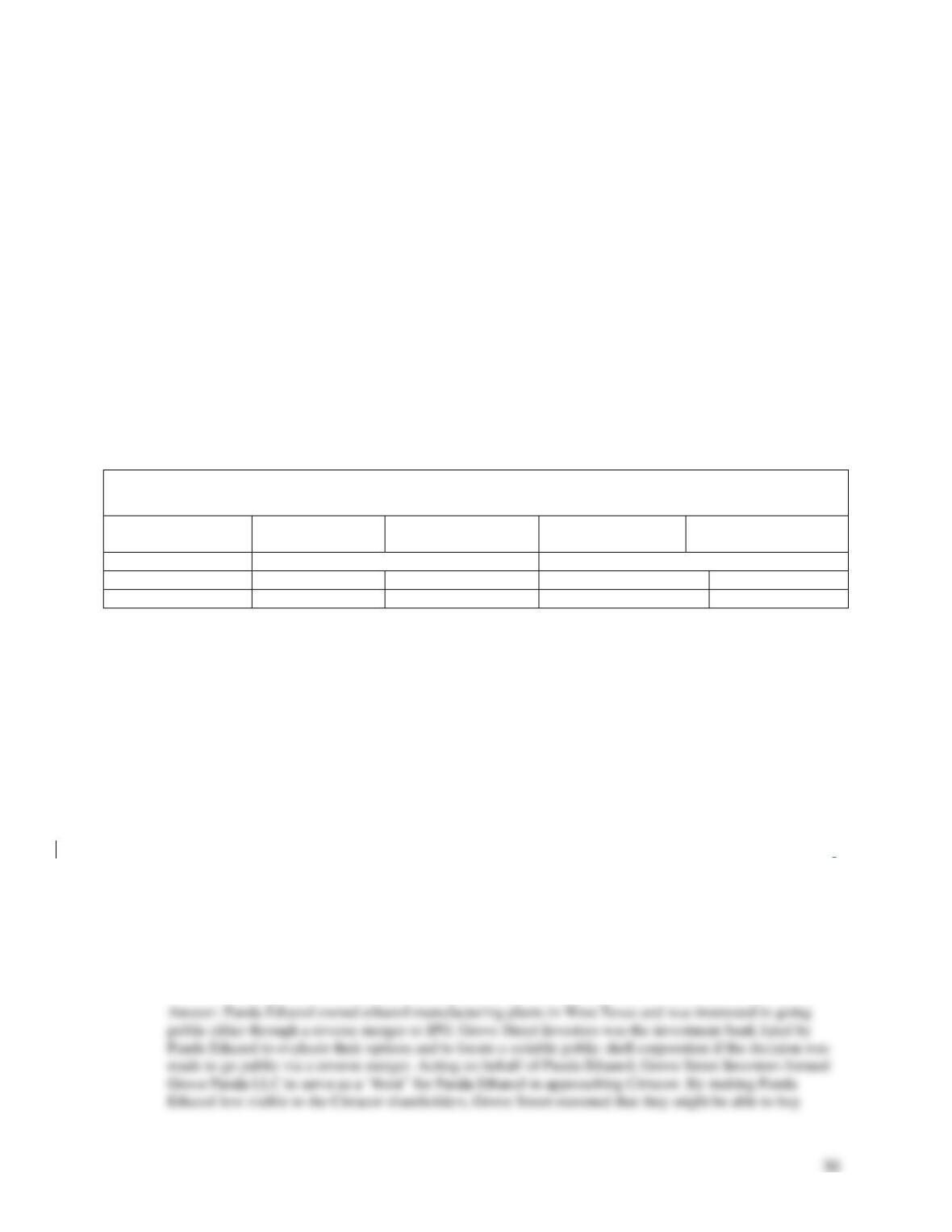

million shares outstanding, with the Cirracor shareholders owning 1.2 million shares. The following table illustrates

the effect of the reverse stock split.

Effects of Reverse Stock Split

Shares

Outstanding*

Ownership

Distribution (%)

Shares

Outstanding*)

Ownership

Distribution (%)

Before Reverse Split

After Reverse Split

Panda Ethanol

28.8

89.2

28.8

96

Cirracor Inc.

3.5

10.8

1.2

4

* In millions of dollars.

A special Cirracor shareholders’ meeting was required by Nevada law (i.e., the state in which Cirracor was

incorporated) in view of the substantial number of new shares that were to be issued as a result of the merger. The

proxy statement filed with the Securities and Exchange Commission and distributed to Cirracor shareholders

indicated that Grove Panda, a 78 percent owner of Cirracor common stock, had already indicated that it would vote

its shares for the merger and the reverse stock split. Since Cirracor’s articles of incorporation required only a simple

majority to approve such matters, it was evident to all that approval was imminent.

On November 7, 2007, Panda completed its merger with Cirracor Inc. As a result of the merger, all shares of

Panda Ethanol common stock (other than Panda Ethanol shareholders who had executed their dissenters’ rights

under Delaware law) would cease to have any rights as a shareholder except the right to receive one share of

Cirracor common stock per share of Panda Ethanol common. Panda Ethanol shareholders choosing to exercise their

right to dissent would receive a cash payment for the fair value of their stock on the day immediately before closing.

Cirracor shareholders had similar dissenting rights under Nevada law. While Cirracor is the surviving corporation,

Panda is viewed for accounting purposes as the acquirer. Accordingly, the financial statements shown for the

surviving corporation are those of Panda Ethanol.

Discussion Questions:

1. Who were Panda Ethanol, Grove Street Investors, Grove Panda, and Cirracor? What were their roles in the

case study? Be specific.

2. Discuss the pros and cons of a reverse merger versus an initial public offering for taking a

company public.

3. Why did Panda Ethanol undertake a private equity placement totaling $90 million shortly before

implementing the reverse merger?

4. Why do you believe Panda did not directly approach Cirraco ? How were the Panda Grove investment

holdings used to influence the outcome of the proposed merger?

Cantel Medical Acquires Crosstex International

On August 3, 2005, Cantel Medical Corporation (Cantel), as part of its strategic plan to expand its infection

prevention and control business, announced that it had completed the acquisition of Crosstex International

Incorporated (Crosstex). Cantel is a leading provider of infection prevention and control products. Crosstex is a

privately owned manufacturer and reseller of single-use infection control products used primarily in the dental

market.

As a consequence of the transaction, Crosstex became a wholly owned subsidiary of Cantel, a publicly traded

firm. For the fiscal year ended April 30, 2005, Crosstex reported revenues of approximately $47.4 million and pretax

income of $6.3 million. The purchase price, which is subject to adjustment for the net asset value at July 31, 2005,

was $74.2 million, comprising $67.4 million in cash and 384,821 shares of Cantel stock (valued at $6.8 million).

Furthermore, Crosstex shareholders could earn another $12 million payable over three years based on future

operating income. Each of the three principal executives of Crosstex entered into a three-year employment

agreement.

James P. Reilly, president and CEO of Cantel, stated, “We continue to pursue our strategy of acquiring branded

niche leaders and expanding in the burgeoning area of infection prevention and control. Crosstex has a reputation for

quality branded products and seasoned management.” Richard Allen Orofino, Crosstex’s president, noted, “We have

built Crosstex over the past 50 years as a family business and we continue growing with our proven formula for

success. However, with so many opportunities in our sights, we believe Cantel is the perfect partner to aid us in

accelerating our growth plans.”

Discussion Questions and Answers:

1. What were the primary reasons Cantel wants to acquire Crosstex? Be specific.

33

2. What do you believe could have been the primary factors causing Crosstex to accept Cantel’s offer?

3. What factors might cause Crosstex’s net asset value to change between signing and closing of the

agreement of purchase and sale?

4. Speculate why Cantel may have chosen to operate Crosstex as a wholly-owned subsidiary following

closing. Be specific

5. The purchase price consisted of cash, stock, and an earnout. What are some of the factors that might

have determined the purchase price from the seller’s perspective? From the buyer’s perspective?

.

Deb Ltd. Seeks an Exit Strategy

In late 2004, Barclay’s Private Equity acquired slightly more than one half the equity in Deb Ltd. (Deb), valued at

about $250 million. The private equity arm of Britain’s Barclay’s bank outbid other suitors in an auction to acquire a

controlling interest in the firm. PriceWaterhouseCooper had been hired by the Williamson family, the primary

stockholder in the firm, to find a buyer.

The sale solved a dilemma for Nick Williamson, the firm’s CEO and son of the founder, who had invented the

firm’s flagship product, Swarfega. The company had been founded some 60 years earlier based on a single product,

a car cleaning agent. Since then, the Swarfega brand name had grown into a widely known brand associated with a

broad array of cleaning products.

In 1990, the elder Williamson wanted to retire and his son Nick, along with business partner Roy Tillead, bought

the business from his father. Since then, the business has continued to grow, and product development has

accelerated. The company developed special Swarfega-dispensing cartridges that have applications in hospitals,

clinics, and other medical faculties.

After 13 years of sustained growth, Williamson realized that some difficult decisions had to be made. He knew

he did not have a natural successor to take over the company. He no longer believed the firm could be managed

successfully by the same management team. It was now time to think seriously about succession planning. So in

early 2004, he began to seek a buyer for the business. He preferably wanted somebody who could bring in new

talents, ideas, and up-to-date management techniques to continue the firm’s growth.

The terms of the agreement called for Williamson to work with a new senior management team until Barclays

decided to take the firm public. This was expected some time during the five–to-seven year period following the

sale. At that point, Williamson would sell the remainder of his family’s stock in the business (Goodman, 2005).

Discussion Questions

1. Succession planning issues are often a reason for family-owned businesses to sell. Why do you believe it may

have been easier for Nick than his father to sell the business to a non-family member?

2. What other alternatives could Nick have pursued? Discuss the advantages and disadvantages of each.

3. What do you believe might be some of the unique challenges in valuing a family-owned business? Be specific.

GHS Helps Itself by Avoiding an IPO

In 1999, GHS, Inc., a little known supplier of medical devices, engineered a reverse merger to avoid the time–

consuming, disclosure-intensive, and costly process of an initial public offering to launch its new internet-based self-

help website. GHS spun off its medical operations as a separate company to its shareholders. The remaining shell is

being used to launch a ‘‘self–help’’ Website, with self-help guru Anthony Robbins as its CEO. The shell corporation

will be financed by $3 million it had on hand as GHS and will receive another $15 million from a private placement.

With the inclusion of Anthony Robbins as the first among many brand names in the self-help industry that it hopes

to feature on its site, its stock soared from $.75 per share to more than $12 between May and August 1999. Robbins,

who did not invest anything in the venture, has stock in the new company valued at $276 million. His contribution to

the company is the exclusive online rights to his name, which it will use to develop Internet self-help seminars, chat

rooms, and e-commerce sites.

Discussion Questions:

1. What are the advantages of employing a reverse merger strategy in this instance?

2. Why was the shell corporation financed through a private placement?

35

Valuing a Privately Held Company

Background

BigCo is interested in acquiring PrivCo, whose owner desires to retire. The firm is 100% owned by the current

owner. PrivCo has revenues of $10 million and an EBIT of $2 million in the preceding year. The market value of the

firm’s debt is $5 million; the book value of equity is $4 million. For publicly traded firms in the same industry, the

average debt-to-equity ratio is .4 (based on the market value of debt and equity), and the marginal tax rate is 40%.

Typically, the ratio of the market value of equity to book value for these firms is 2. The average of publicly traded

firms that are in the same business is 2.00. Capital expenditures and depreciation amounted to $0.3 million and $0.2

million in the prior year. Both items are expected to grow at the same rate as revenues for the next 5 years. Capital

expenditures and depreciation are expected to be equal beyond 5 years (i.e., capital spending will be internally

funded). As a result of excellent working capital management practices, the change in working capital is expected to

be essentially zero throughout the forecast period and beyond. The revenues of this firm are expected to grow 15%

annually for the next 5 years and 5% per year thereafter. Net income is expected to increase 15% a year for the next

5 years and 5% thereafter. The 10-year U.S. Treasury bond rate is 6%. The pretax cost of debt for a nonrated firm is

10%. No adjustment is made in the calculation of the cost of equity for a marketability discount. Estimate the

shareholder value of the firm.

Note: To estimate the WACC for a leveraged private firm, it is necessary to calculate the firm’s leveraged . This

requires an estimate of the firm’s unleveraged which can be obtained by estimating the unleveraged for similar

firms in the same industry. In addition, the value of debt and equity in calculating the cost of capital should be

expressed as market rather than book values.

Calculating COE and WACC:

36

Pacific Wardrobe Acquires Surferdude Apparel

by a Skillful Structuring of the Acquisition Plan

Pacific Wardrobe (Pacific) is a privately owned California corporation that has annual sales of $20 million and

pretax profits of $2 million. Its target market is the surfwear/sportswear segment of the apparel industry. The

surfwear/sportswear market consists of two segments: cutting-edge and casual brands. The first segment includes

high-margin apparel sold at higher-end retail establishments. The second segment consists of brands that sell for

lower prices at retail stores such as Sears, Target, and J.C. Penney. Pacific operates primarily as a U.S.

importer/distributor of mainly casual sportswear for young men and boys between 10–21 years of age. Pacific’s

strategic business objectives are to triple sales and pretax profits during the next 5 years. Pacific intends to achieve

these objectives by moving away from the casual sportswear market segment and more into the high-growth, high–

profit cutting-edge surfer segment. Because of the rapid rate at which trends change in the apparel industry, Pacific’s

management believes that it can take advantage of current trends only through a well-conceived acquisition strategy.

Pacific’s Operations and Competitive Environment

Pacific imports all of its apparel from factories in Hong Kong, Taiwan, Nepal, and Indonesia. Its customers consist

of major chains and specialty stores. Most customers are lower-end retail stores. Customers include J.C. Penney,

Sears, Stein Mart, Kids “R” Us, and Target. No one customer accounts for more than 20% of Pacific’s total revenue.

The customers in the lower-end market are extremely cost sensitive. Customers consist of those in the 10–21 years

of age range who want to wear cutting–edge surf and sport styles but who are not willing or able to pay high prices.

Pacific offers an alternative to the expensive cutting-edge styles.

Pacific has found a niche in the young men’s and teenage boy’s sportswear market. The firm offers similar styles

as the top brand names in the surf and sport industry, such as Mossimo, Red Sand, Stussy, Quick Silver, and Gotcha,

but at a lower price point. Pacific indirectly competes with these top brand names by attempting to appeal to the

same customer base. There are few companies that compete with Pacific at their level—low-cost production of

‘‘almost’’ cutting-edge styles.

Pacific’s Strengths and Weaknesses

Pacific’s core strengths lie in their strong vendor support in terms of quantity, quality, service, delivery, and

price/cost. Pacific’s production is also scaleable and has the potential to produce at high volumes to meet peak

demand periods. Additionally, Pacific also has strong financial support from local banks and a strong management

team, with an excellent track record in successfully acquiring and integrating small acquisitions. Pacific also has a

good reputation for high-quality products and customer service and on-time delivery. Finally, Pacific has a low cost

of goods sold when compared with the competition. Pacific’s major weakness is that it does not possess any cutting-

edge/trendy labels. Furthermore, their management team lacks the ability to develop trendy brands.

Acquisition Plan

37

Pacific’s management objectives are to grow sales, improve profit margins, and increase its brand life cycle by

acquiring a cutting-edge surfwear retailer with a trendy brand image. Pacific intends to improve its operating

margins by increasing its sales of trendy clothes under the newly acquired brand name, while obtaining these clothes

from its own low-cost production sources.

Pacific would prefer to use its stock to complete an acquisition, because it is currently short of cash and wishes to

use its borrowing capacity to fund future working capital requirements. Pacific’s target debt–to-equity ratio is 3 to 1.

The firm desires a friendly takeover of an existing surfwear company to facilitate integration and avoid a potential

‘‘bidding war.’’ The target will be evaluated on the basis of profitability, target markets, distribution channels,

geographic markets, existing inventory, market brand recognition, price range, and overall ‘‘fit’’ with Pacific.

Pacific will locate this surfwear company by analyzing the surfwear industry; reviewing industry literature; and

making discrete inquiries relative to the availability of various firms to board members, law firms, and accounting

firms. Pacific would prefer an asset purchase because of the potentially favorable impact on cash flow and because it

is concerned about unknown liabilities that might be assumed if it acquired the stock.

Pacific’s screening criteria for identifying potential acquisition candidates include the following:

1. Industry: Garment industry targeting young men, teens, and boys

2. Product: Cutting-edge, trendy surfwear product line

3. Size: Revenue ranging from $5 million to $10 million

4. Profit: Minimum of break-even on operating earnings for fiscal year 1999

5. Management: Company with management expertise in brand and image building

6. Leverage: Maximum debt–to-equity ratio of 3 to 1

After a review of 14 companies, Pacific’s management determined that SurferDude best satisfied their criteria.

SurferDude is a widely recognized brand in the surfer sports apparel line; it is marginally profitable, with sales of $7

million and a debt-to–equity ratio of 3 to 1. SurferDude’s current lackluster profitability reflects a significant

advertising campaign undertaken during the last several years. Based on financial information provided by

SurferDude, industry averages, and comparable companies, the estimated purchase price ranges from $1.5 million to

$15 million. The maximum price reflects the full impact of anticipated synergy. The price range was estimated using

several valuation methods.

Valuation

On a standalone basis, sales for both Pacific and SurferDude are projected to increase at a compound annual average

rate of 20% during the next 5 years. SurferDude’s sales growth assumes that its advertising expenditures in 1998 and

1999 have created a significant brand image, thus increasing future sales and gross profit margins. Pacific’s sales

growth rate reflects the recent licensing of several new apparel product lines. Consolidated sales of the combined

companies are expected to grow at an annual growth rate of 25% as a result of the sales and distribution synergies

created between the two companies.

The discount factor was derived using different methods, such as the buildup method or the CAPM. Because this

was a private company, the buildup method was utilized and then supported by the CAPM. At 12%, the specific

business risk premium is assumed to be somewhat higher than the 9% historical average difference between the

return on small stocks and the risk-free return as a result of the capricious nature of the highly style-conscious

surfware industry. The marketability discount is assumed to be a relatively modest, 20% because Pacific is acquiring

a controlling interest in SurferDude. After growing at a compound annual average growth rate of 25% during the

next 5 years, the sustainable long-term growth rate in SurferDude’s standalone revenue is assumed to be 8%.

The buildup calculation included the following factors:

Risk-Free Rate: 6.00%

Market Risk Premium to Invest in Stocks: 5.50%

Specific Business Risk Premium: 12.00%

Marketability Risk Premium: 20.00%

Discount Rate 43.50%

Less: Long-Term Growth Rate 8.00%

Capitalization Rate 35.50%

The CAPM method supported the buildup method. One comparable company, Apparel Tech, had a ß estimated

by Yahoo.Marketguide.com to be 4.74, which results in a ke of 32.07 for this comparable company. The weighted

average cost of capital using a target debt–to-equity ratio of 3 to 1 for the combined companies is estimated to be

26%.

The standalone values of SurferDude and Pacific assume that fixed expenses will decrease as a percentage of

sales as a result of economies of scale. Pacific will outsource production through its parent’s overseas facilities, thus

significantly reducing the cost of goods sold. SurferDude’s administrative expenses are expected to decrease from

25% of sales to 18% because only senior managers and the design staff will be retained. The sustainable growth rate

for the terminal period for both the standalone and the consolidated models is a relatively modest 6%. Pacific

believes this growth rate is reasonable considering the growth potential throughout the world. Although Pacific and

SurferDude’s current market concentration resides largely in the United States, it is forecasted that the combined

companies will develop a global presence, with a particular emphasis in developing markets. The value of the

combined companies including synergies equals $15 million.

Developing an Initial Offer Price

Using price-to-cash flow multiples to develop an initial offer price, the target was valued on a standalone

basis and a multiple of 4.51 for a comparable publicly held company called Stage II Apparel Corp. The standalone

valuation, excluding synergies, of SurferDude ranges from $621,000 to $2,263,000.

Negotiating Strategy

Pacific expects to initially offer $2.25 million and close at $3.0 million. Pacific’s management believes that

SurferDude can be purchased at a modest price when compared with anticipated synergy, because an all-stock

transaction would give SurferDude’s management ownership of between 25% and 30% of the combined companies.

Integration

A transition team consisting of two Pacific and two SurferDude managers will be given full responsibility for

consolidating the businesses following closing. A senior Pacific manager will direct the integration team. Once an

agreement of purchase and sale has been signed, the team’s initial responsibilities will be to first contact and inform

employees and customers of SurferDude that operations will continue as normal until the close of the transaction. As

an inducement to remain through closing, Pacific intends to offer severance packages for those SurferDude

employees who will be terminated following the consolidation of the two businesses.

Source: Adapted from Contino, Maria, Domenic Costa, Larui Deyhimy, and Jenny Hu, Loyola, Marymount

University, MBAF 624, Los Angeles, CA, Fall 1999.

Discussion Questions:

1. What were the key assumptions implicit in Pacific Wardrobe’s acquisitions plan, with respect to the

market, valuation, and integration? Comment on the realism of these assumptions.

39

2. Discuss some of the challenges that Pacific Wardrobe is likely to experience during due diligence.

3. Identify alternative deal structures Pacific Wardrobe might have employed in order to complete the

transaction. Discuss why these alternatives might have been superior or inferior to the one actually chosen.

Cashing Out of a Privately Held Enterprise

When he had reached his early sixties, Anthony Carnevale starting reducing the amount of time he spent managing

Sentinel Benefits Group Inc., a firm he had founded. He planned to retire from the benefits and money management

consulting firm in which he was a 26 percent owner. Mr. Carnevale, his two sons, and two nonfamily partners had

built the firm to a company of more than 160 employees with $2.5 billion under management.

Selling the family business was not what the family expected to happen when Mr. Carnevale retired. He believed

that his sons and partners were quite capable of continuing to manage the firm after he left. However, like many

small businesses, Sentinel found itself with a succession planning challenges. If the sons and the company’s two

other nonfamily partners bought out Mr. Carnevale, the firm would have little cash left over for future growth. The

firm was unable to get a loan, given the lack of assets for collateral and the somewhat unpredictable cash flow of the

business. Even if a loan could have been obtained, the firm would have been burdened with interest and principal

repayment for years to come.

Over the years, Mr. Carnevale had rejected buyout proposals from competitors as inadequate. However, he

contacted a former suitor, Focus Financial Partners LLC (a partnership that buys small money management firms

and lets them operate largely independently). After several months of negotiation, Focus acquired 100 percent of

Sentinel. Each of the five partners—Mr. Carnevale, his two sons, and two nonfamily partners—received an

undisclosed amount of cash and Focus stock. A four-person Sentinel management team is now paid based on the

company’s revenue and growth.

The major challenges prior to the sale dealt with the many meetings held to resolve issues such as compensation,

treatment of employees, how the firm would be managed subsequent to the sale, how client pricing would be

determined, and who would make decisions about staff changes. Once the deal was complete, the Carnivales found

it difficult to tell employees, particularly those who had been with the firm for years. Since most employees were

not directly affected, only one left as a direct result of the sale.8

8Adapted from Simona Covel, “Firm Sells Itself to Let Patriarch Cash Out,” Wall Street Journal, November 1, 2007,

p. B8