CUSTOM ID:

130.06 – TF – MANK08

131. Buyers and sellers always share the burden of a tax equally.

a.

True

b.

False

CUSTOM ID:

131.06 – TF – MANK08

132. Buyers and sellers rarely share the burden of a tax equally.

a.

True

b.

False

CUSTOM ID:

132.06 – TF – MANK08

133. Who bears the majority of a tax burden depends on whether the tax is placed on the buyers or the sellers.

a.

True

b.

False

CUSTOM ID:

133.06 – TF – MANK08

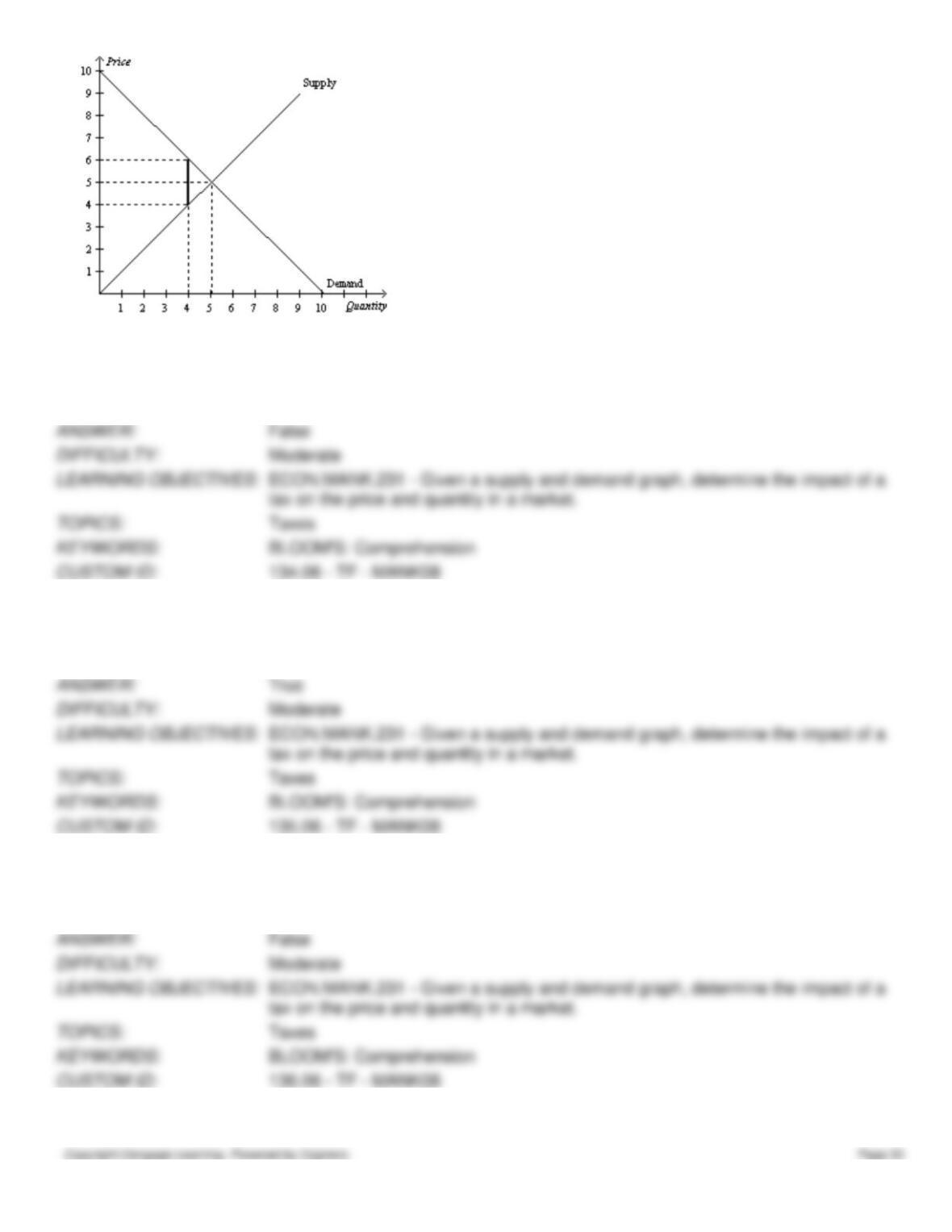

134. Refer to Figure 6-36. If the government places a $2 tax in the market, the buyer pays $4.

a.

True

b.

False

135. Refer to Figure 6-36. If the government places a $2 tax in the market, the buyer pays $6.

a.

True

b.

False

136. Refer to Figure 6-36. If the government places a $2 tax in the market, the seller receives $6.

a.

True

b.

False

137. Refer to Figure 6-36. If the government places a $2 tax in the market, the seller receives $4.

a.

True

b.

False

138. Refer to Figure 6-36. If the government places a $2 tax in the market, the buyer bears $2 of the tax burden.

a.

True

b.

False

139. Refer to Figure 6-36. If the government places a $2 tax in the market, the buyer bears $1 of the tax burden.

a.

True

b.

False

140. Refer to Figure 6-36. If the government places a $2 tax in the market, the seller bears $2 of the tax burden.

a.

True

b.

False

141. Refer to Figure 6-36. If the government places a $2 tax in the market, the seller bears $1 of the tax burden.

a.

True

b.

False

142. Most labor economists believe that the supply of labor is much more elastic than the demand.

a.

True

b.

False

143. FICA is an example of a payroll tax, which is a tax on the wages that firms pay their workers.

a.

True

b.

False

144. Since half of the FICA tax is paid by firms and the other half is paid by workers, the burden of the tax must fall

equally on firms and workers.

a.

True

b.

False

145. Workers, rather than firms, bear most of the burden of the payroll tax.

a.

True

b.

False

146. Who bears the majority of a tax burden depends on the relative elasticity of supply and demand.

a.

True

b.

False

147. If the demand curve is very elastic and the supply curve is very inelastic in a market, then the sellers will bear a

greater burden of a tax imposed on the market, even if the tax is imposed on the buyers.

a.

True

b.

False

148. If the demand curve is very inelastic and the supply curve is very elastic in a market, then the sellers will bear a

greater burden of a tax imposed on the market, even if the tax is imposed on the buyers.

a.

True

b.

False

149. A tax burden falls more heavily on the side of the market that is less elastic.

a.

True

b.

False

150. The tax burden falls more heavily on the side of the market that is more inelastic.

a.

True

b.

False

151. A tax on a market with elastic demand and elastic supply will shrink the market more than a tax on a market with

inelastic demand and inelastic supply will shrink the market.

a.

True

b.

False

152. The true burden of a payroll tax has nothing to do with the percentage of the tax that employers are required to pay.

a.

True

b.

False

153. Even though federal law mandates that workers and firms each pay half of the total FICA tax, the tax burden may not

fall equally on workers and firms.

a.

True

b.

False

154. Most of the burden of a luxury tax falls on the middle class workers who produce luxury goods rather than on the

rich who buy them.

a.

True

b.

False

155. The burden that results from a tax on yachts falls more heavily on the buyers of yachts than on the sellers of yachts.

a.

True

b.

False

156. The burden of a luxury tax most likely falls more heavily on sellers because demand is more elastic and supply is

more inelastic.

a.

True

b.

False

157. Price ceilings are never binding when set above the equilibrium price.

a.

True

b.

False

158. Rent controls only affect the demand side of the rental market.

a.

True

b.

False

159. Since one effect of rent controls is to reduce the supply of available rental properties,rent controls can contribute to

the problems of homelessness in cities with rent controls.

a.

True

b.

False

160. Long lines and gasoline shortages during the 1970’s can be attributed completely to the decision by OPEC to raise

crude oil prices.

a.

True

b.

False

161. Whether the minimum wage is a binding price floor always depends upon whether the economy is in a recession.

a.

True

b.

False

162. The distribution of the burden of a tax depends strictly on the elasticity of demand.

a.

True

b.

False

163. The distribution of the burden of a tax depends strictly on the elasticity of supply.

a.

True

b.

False

164. To determine the incidence of a tax, it is necessary to have information on both the elasticity of demand and the

elasticity of supply.

a.

True

b.

False

165. Since a tax imposed on buyers of a product only affects demand, such a tax has no impact on sellers in that market.

a.

True

b.

False

166. Since the FICA tax is split equally between employers and employees, we can conclude that the incidence of this tax

is also equally shared.

a.

True

b.

False