Subjective Short Answer

1. A group of buyers and sellers of a particular good or service is called a

market.

2. Since individual buyers and individual sellers in a competitive market have no influence on the market price, what do

we call the buyers and sellers in a competitive market?

Table 4-14

The table below shows the quantities demanded of milk per month by four families at various prices.

Price of Gallon of

Milk

The Berman

Family

The Johnson

Family

The Harris

Family

The Patel Family

$3.00

9

15

12

14

$4.00

8

12

10

10

$5.00

7

9

8

6

$6.00

6

6

6

2

3. Refer to Table 4-14. If the four families listed are the only demanders in this market and the price of a gallon of milk is

$4.00, what is the market quantity demanded?

40 gallons

4. Refer to Table 4-14. If the four families listed are the only demanders in this market and the price of a gallon of milk

increases from $4.00 to $5.00, what is the change in the market quantity demanded?

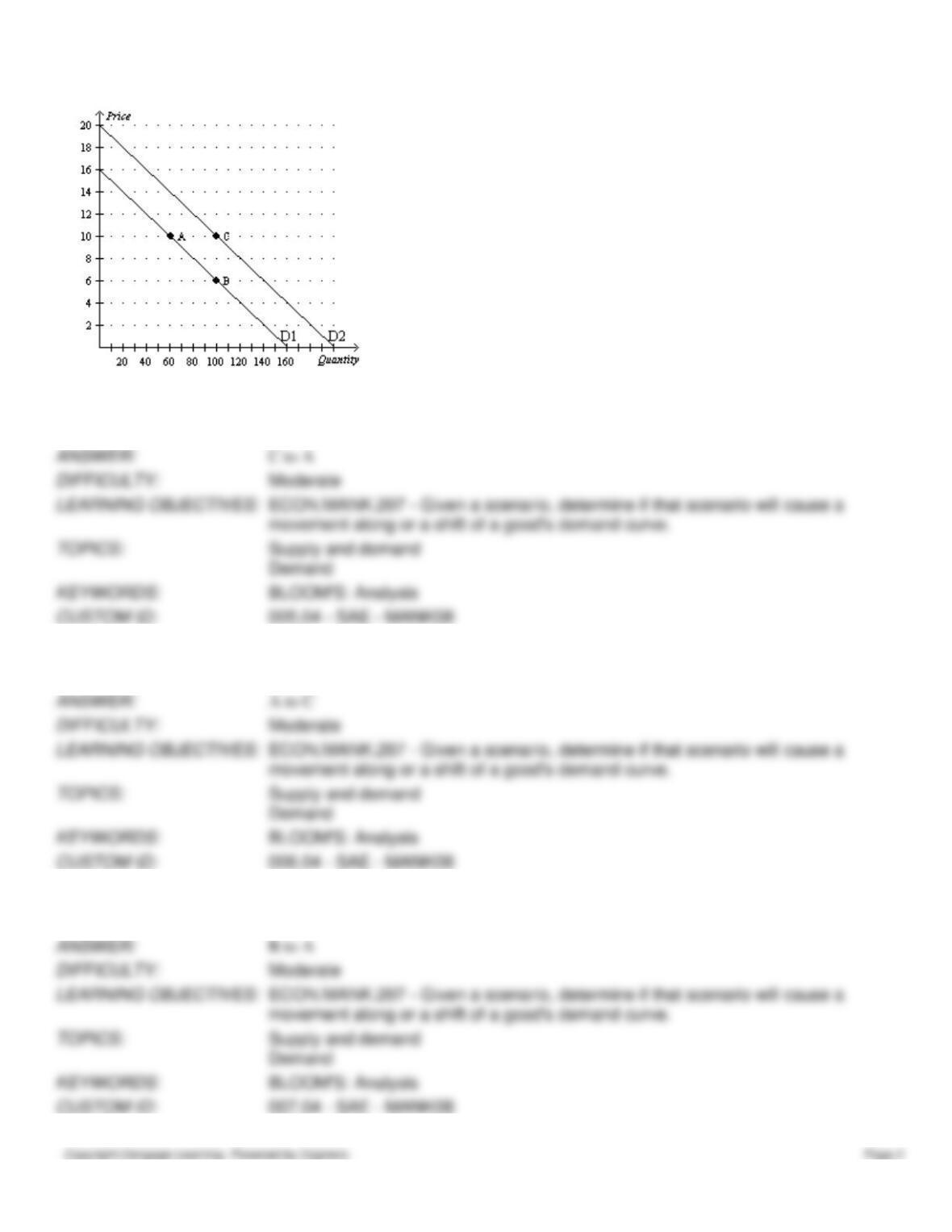

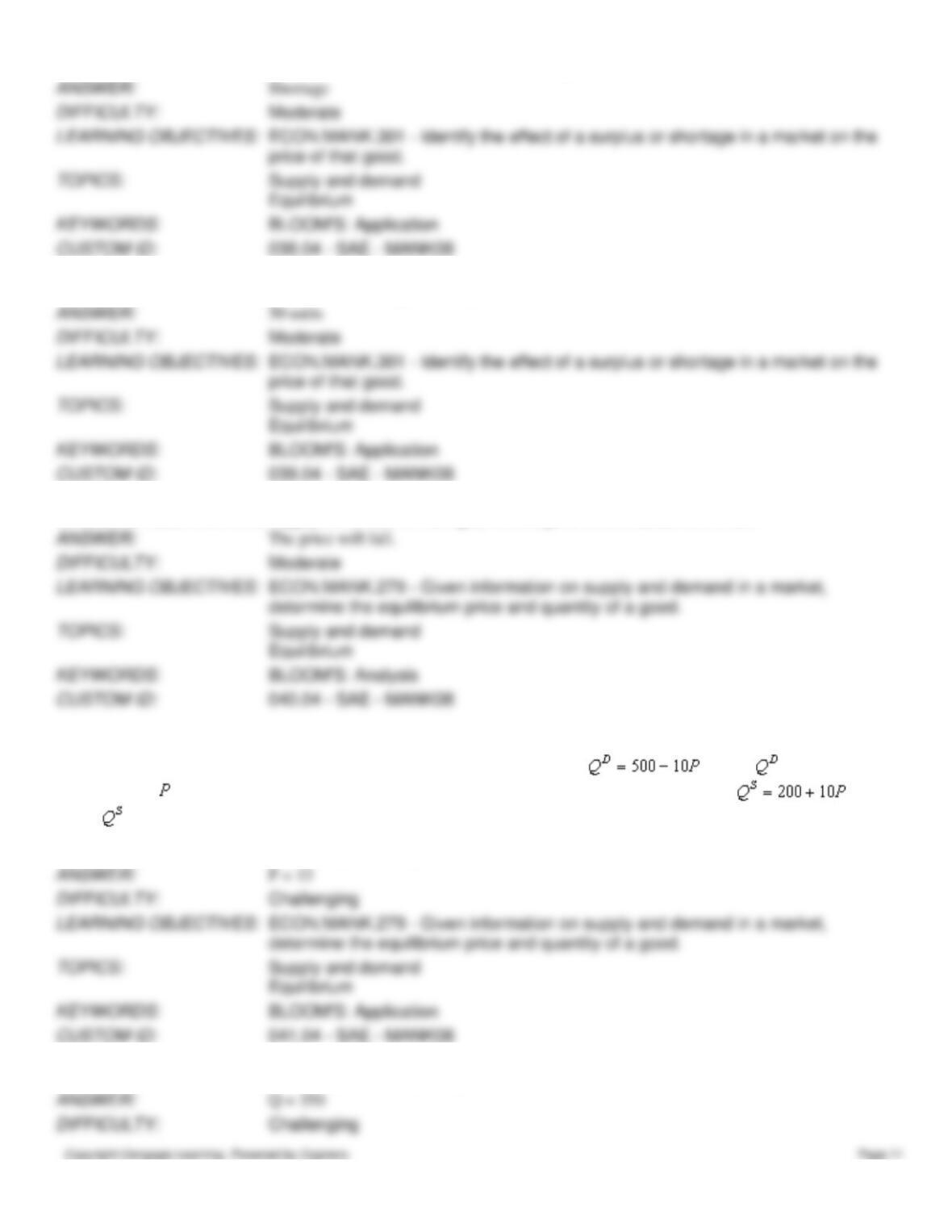

Figure 4-28

5. Refer to Figure 4-28. Using the points on the figure, describe the change that would occur if consumer incomes

increase and this is an inferior good.

6. Refer to Figure 4-28. Using the points on the figure, describe the change that would occur if the price of a substitute

for this good becomes more expensive.

7. Refer to Figure 4-28. Using the points on the figure, describe the change that would occur if the price of this good

increases.

8. Refer to Figure 4-28. Using the points on the figure, describe the change that would occur if a news report stated that

the price of this good was expected to increase next week.

9. Studies show that lower cigarette prices are associated with greater use of marijuana; therefore, tobacco and marijuana

are

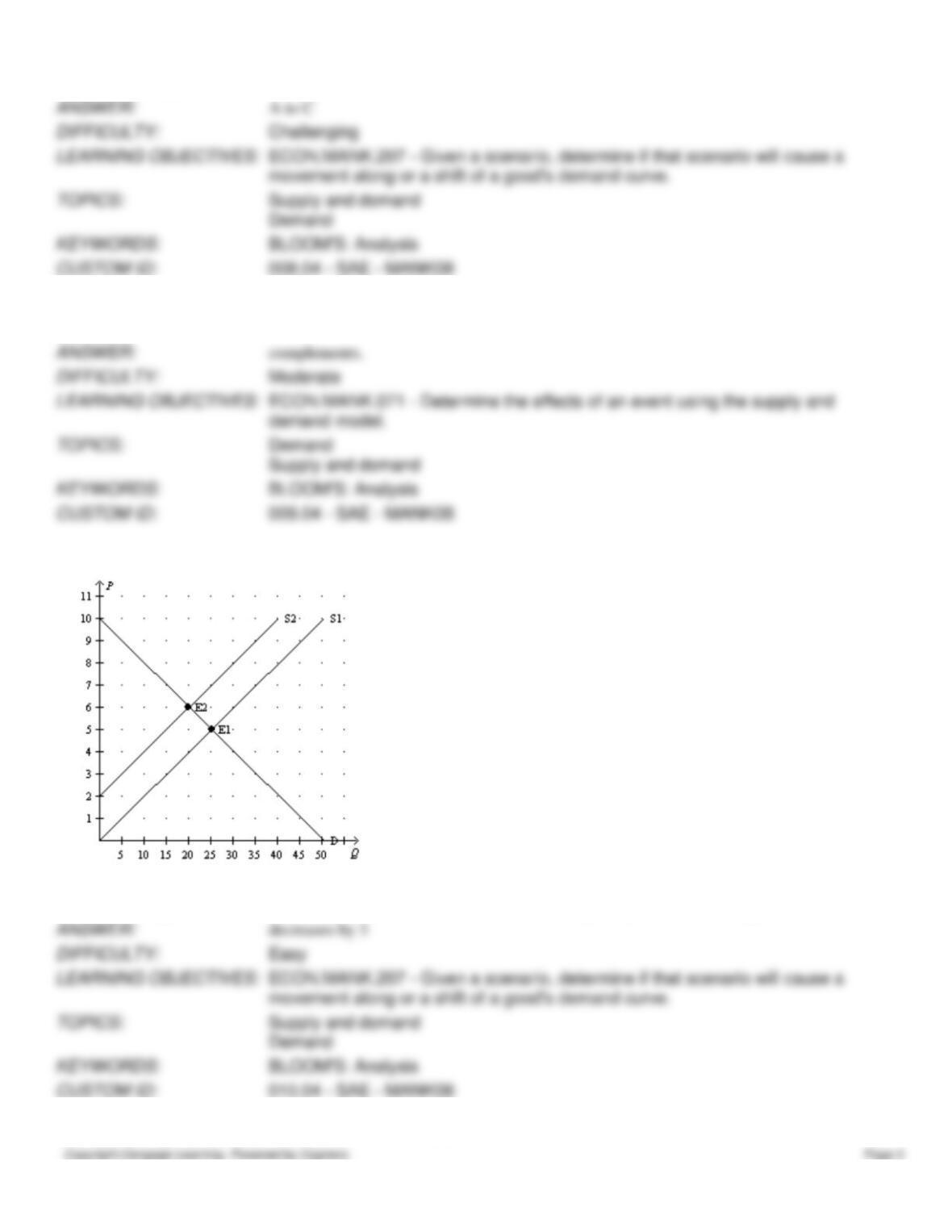

Figure 4-29

10. Refer to Figure 4-29. If the price increases from $5 to $6, how does the quantity demanded change?

11. Refer to Figure 4-29. The movement from S1 to S2 is a

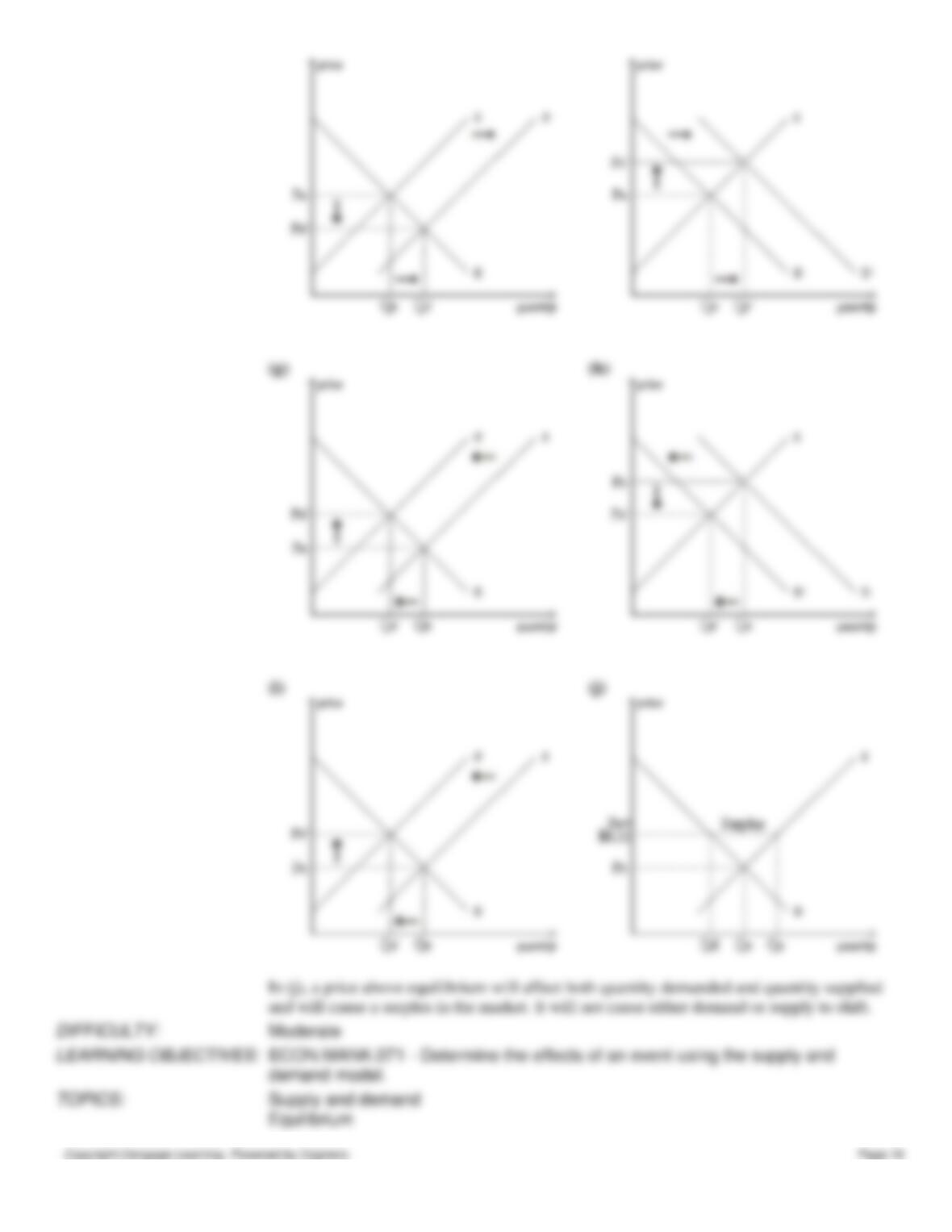

12. According to the law of demand, when price increases the quantity demanded of a good

13. Does a change in the price in a market result in a shift of the demand curve or in a movement along the demand curve?

14. If income rises in the market for an inferior good, will the demand curve for the inferior good shift to the right or to

the left?

15. If income rises in the market for a normal good, will the demand curve for the normal good shift to the right or to the

left?

16. Suppose goods A and B are substitutes. If the price of good A increases, will the demand for good B increase or

decrease?

The demand for good B will increase.

17. Suppose goods A and B are complements. If the price of good A increases, will the demand for good B increase or

decrease?

The demand for good B will decrease.

18. Suppose consumers expect the price of a good to be higher in the future than it is today. Would the current demand for

the good increase or decrease?

The current demand will increase.

19. Suppose the number of buyers in a market decreases. As a result, would the demand curve in this market shift to the

right or to the left?

The demand curve will shift to the left.

Table 4-15

The following table shows the number of cases of water each seller is willing to sell at the prices listed.

Price per case

Alpine Springs

Brook Mountain

Cascade Waters

Dew Good

$0.00

0 cases

0 cases

0 cases

0 cases

$3.00

100 cases

40 cases

60 cases

100 cases

$6.00

200 cases

80 cases

120 cases

200 cases

$9.00

300 cases

120 cases

180 cases

300 cases

20. Refer to Table 4-15. If all four suppliers operate in this market, what is the market quantity supplied when the price is

$6.00 per case?

600 cases

21. Refer to Table 4-15. If only Brook Mountain and Cascade Waters operate in this market, what is the market quantity

supplied when the price is $3.00 per case?

100 cases

22. Refer to Table 4-15. Assuming these are the only four suppliers in this market, the function for market supply can be

written as QS=

100P

23. Refer to Table 4-15. Assuming these are the only four suppliers in this market and the function for market demand is

QD=1000-100P, where QD is the quantity demanded and P is the price, what is the equilibrium price?

$5.00 per case

24. Refer to Table 4-15. Assuming these are the only four suppliers in this market and the function for market demand is

QD=1000-100P, where QD is the quantity demanded and P is the price, what is the equilibrium quantity?

25. Refer to Table 4-15. Assume these are the only four suppliers in this market and the function for market demand is

QD=1000-100P, where QD is the quantity demanded and P is the price. If the price is $6 per case, is there a shortage or

surplus, and how large is the shortage or surplus?

Figure 4-30

26. Refer to Figure 4-30. In this market for iPhones, the technology improves while all other factors remain constant.

Which curve(s) shift(s) and in which direction?

27. Refer to Figure 4-30. In this market for iPhones, the technology improves while all other factors remain constant.

Explain the change(s) in the equilibrium price and quantity.

28. Refer to Figure 4-30. In this market for tablet computers, more suppliers enter the market and the price of laptops, a

substitute good, increases, while all other factors remain constant. Which curve(s) shift(s) and in which direction?

29. Refer to Figure 4-30. In this market for tablet computers, more suppliers enter the market and the price of laptops, a

substitute good, increases, while all other factors remain constant. Explain the change(s) in the equilibrium price and

quantity.

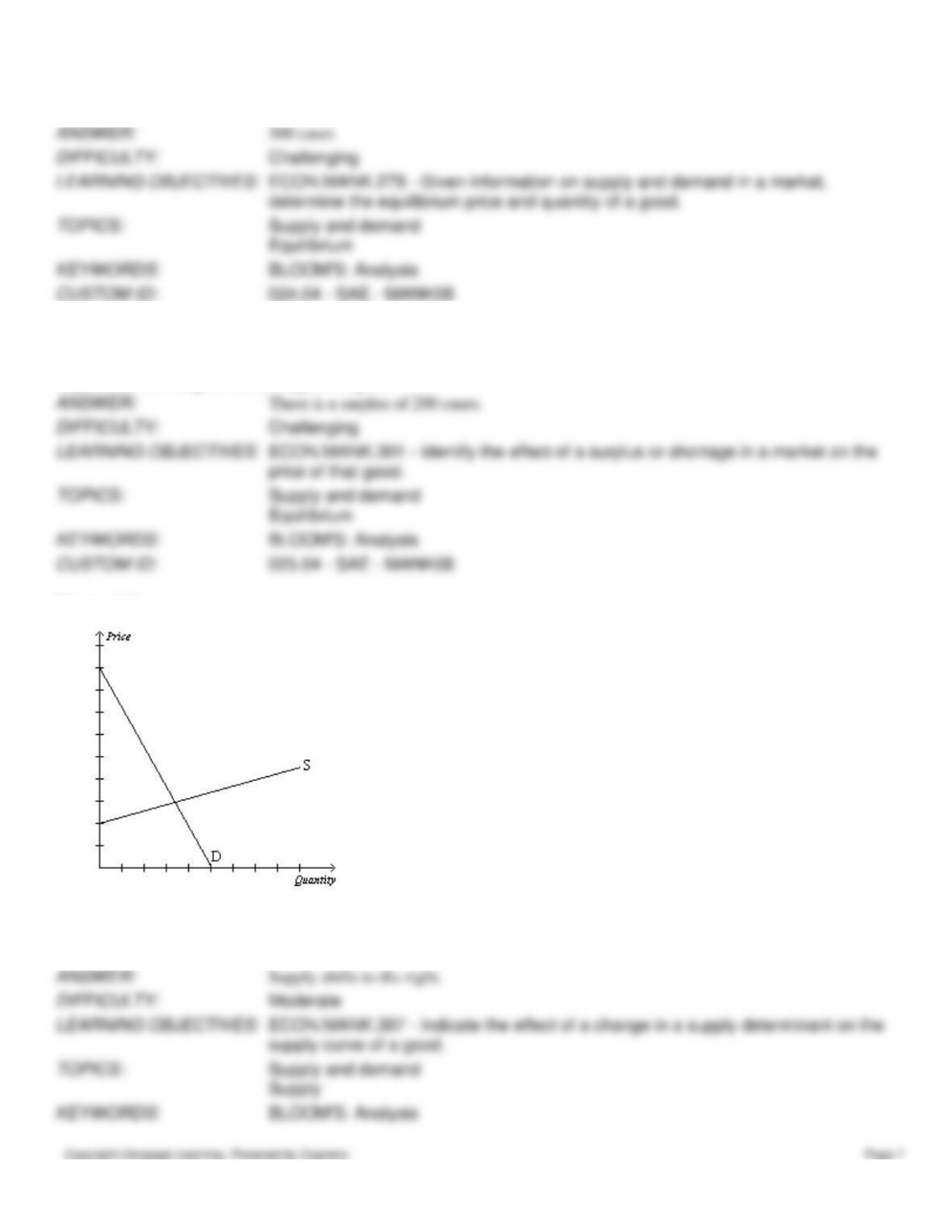

30. If corn is an input into the production of ethanol, will a decrease in the price of corn increase the supply of ethanol or

decrease the supply of ethanol?

31. Suppose researchers discover a new, lower cost method of producing calculators. As a result, will the supply of

calculators increase or decrease?

Figure 4-31

Consider the market for 2-packs of light bulbs below.

32. Refer to Figure 4-31. What are the values of the equilibrium price and quantity?

33. Refer to Figure 4-31. At a price of $3, is there a shortage or surplus, and how large is the shortage/surplus?

34. Refer to Figure 4-31. At a price of $6, is there a shortage or surplus, and how large is the shortage/surplus?

35. Refer to Figure 4-31. Suppose there is an improvement in technology in this market and the price of lamps, a

complementary good, increases. What changes do you predict in the equilibrium price and quantity?

Table 4-16

The following table shows the supply and demand schedules in a market.

Price ($)

Quantity

Demanded

(units)

Quantity

Supplied

(units)

0

50

0

2

40

15

4

30

30

6

20

45

8

10

60

10

0

75

36. Refer to Table 4-16. What is the equilibrium price in this market?

$4

37. Refer to Table 4-16. What is the equilibrium quantity in this market?

30 units

38. Refer to Table 4-16. At a price of $2, will there be a surplus or shortage of units in this market?

39. Refer to Table 4-16. At a price of $8, how large of a surplus will there be in this market?

40. Refer to Table 4-16. If the supply curve shifts to the right, will the price in this market rise or fall?

Scenario 4-1

Suppose the demand schedule in a market can be represented by the equation , where is the quantity

demanded and is the price. Also, suppose the supply schedule can be represented by the equation ,

where is the quantity supplied.

41. Refer to Scenario 4-1. What is the equilibrium price in this market?

42. Refer to Scenario 4-1. What is the equilibrium quantity in this market?

43. Refer to Scenario 4-1. Suppose the price is currently equal to 10 in this market. Is there a shortage or surplus in this

market, and how large is the shortage/surplus?

44. Refer to Scenario 4-1. Suppose the price is currently equal to 18 in this market. Is there a shortage or surplus in this

market, and how large is the shortage/surplus?

45. Refer to Scenario 4-1. Suppose the supply curve shifts to . What is the new equilibrium price and

quantity in this market?

46. Suppose the supply and demand of corn both increase. As a result, what will happen to the equilibrium price and

equilibrium quantity in the market?

47. If the supply of tennis balls, a complement to tennis racquets, decreases, what will happen to the equilibrium price of

tennis balls and to the equilibrium price of tennis racquets?

48. If the supply of pencils, a substitute for pens, increases, what will happen to the equilibrium price of pencils and to the

equilibrium price of pens?

49. If the price of steel, an input into the production of automobiles, rises, and at the same time the price of gasoline rises,

what will happen to the equilibrium price and quantity of automobiles?

50. If the demand for a good increases at the same time as the supply of the same good decreases, what will happen to the

equilibrium price and quantity of the good?

51.

a.

What is the difference between a “change in demand” and a “change in quantity

demanded?” Graph your answer.

b.

For each of the following changes, determine whether there will be a change in quantity

demanded or a change in demand.

i.

a change in the price of a related good

ii.

a change in tastes

iii.

a change in the number of buyers

iv.

a change in price

v.

a change in consumer expectations

vi.

a change in income

a.

A change in demand refers to a shift of the demand curve. A change in quantity

demanded refers to a movement along a fixed demand curve.

b.

listed shift the demand curve.

52.

a.

What is the difference between a “change in supply” and a “change in quantity

supplied?” Graph your answer.

b.

For each of the following changes, determine whether there will be a change in quantity

supplied or a change in supply.

i.

a change in input costs

ii

a change in producer expectations

iii.

a change in price

iv.

a change in technology

v.

a change in the number of sellers

a.

A change in supply refers to a shift of the supply curve. A change in quantity supplied

refers to a movement along a fixed supply curve.

b.

shift the supply curve.

53.

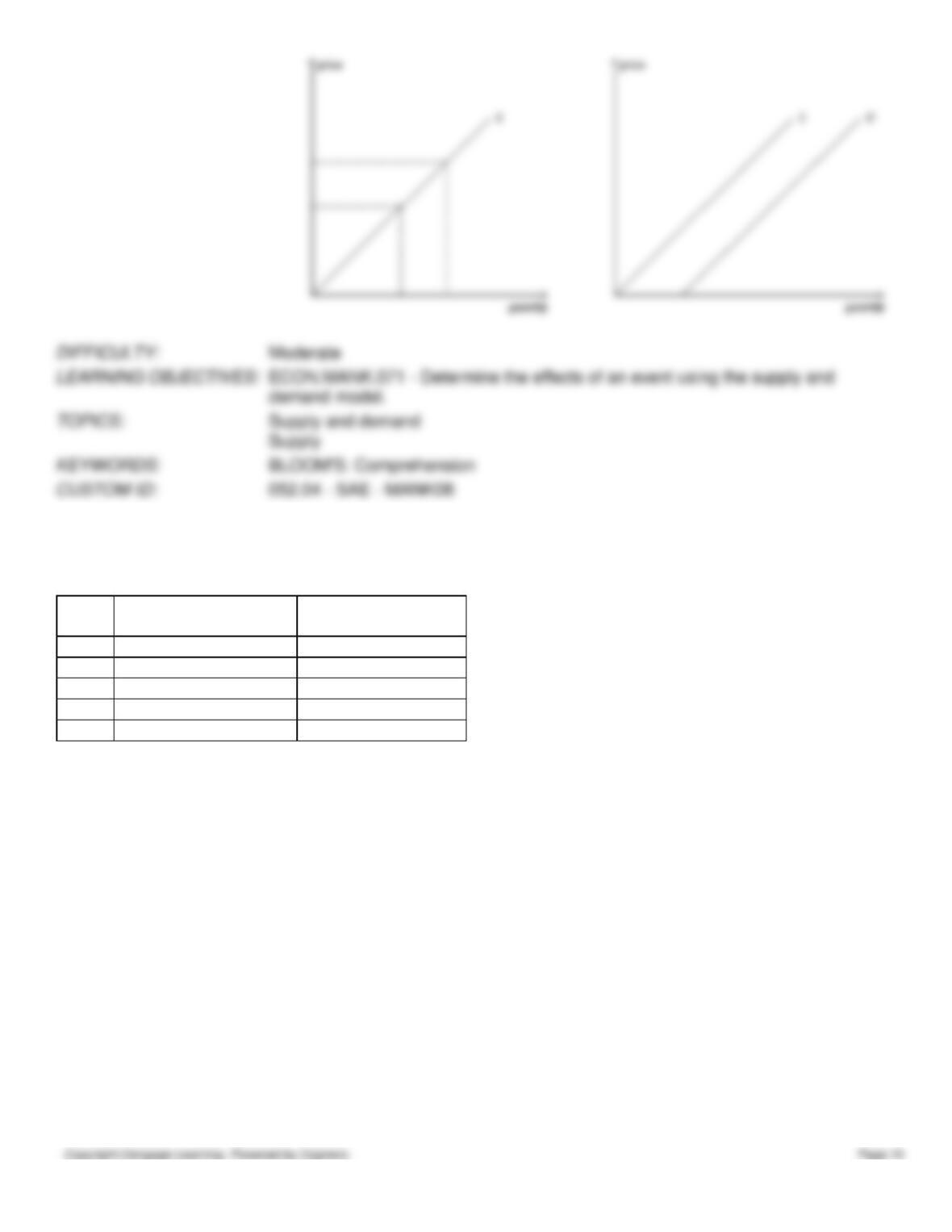

a.

Given the table below, graph the demand and supply curves for flashlights. Make certain

to label the equilibrium price and equilibrium quantity.

Price

Quantity Demanded

Per Month

Quantity Supplied

Per Month

$5

6,000

10,000

$4

8,000

8,000

$3

10,000

6,000

$2

12,000

4,000

$1

14,000

2,000

b.

What is the equilibrium price and the equilibrium quantity?

c.

Suppose the price is currently $5. What problem would exist in the market? What would

you expect to happen to price? Show this on your graph.

d.

Suppose the price is currently $2. What problem would exist in the market? What would

you expect to happen to price? Show this on your graph.

The equilibrium price (Pe) is $4 and the equilibrium quantity (Qe) is 8,000.

A surplus of 4,000 flashlights would be the problem in the market, and we would

expect the price to fall.

A shortage of 8,000 flashlights would be the problem in the market, and we would

expect the price to rise.

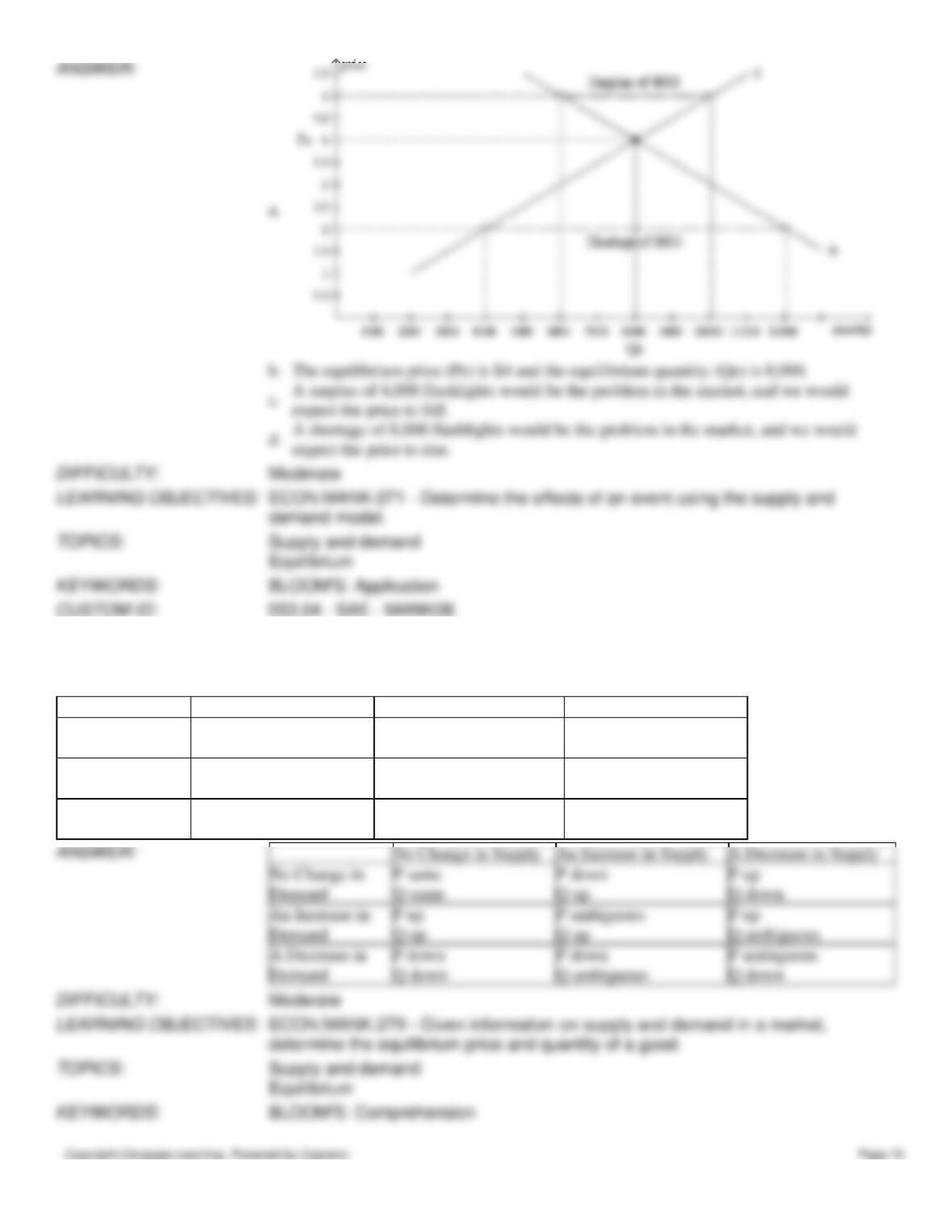

54. Fill in the table below, showing whether equilibrium price and equilibrium quantity go up, go down, stay the same, or

change ambiguously.

No Change in Supply

An Increase in Supply

A Decrease in Supply

No Change in

Demand

An Increase in

Demand

A Decrease in

Demand

No Change in Supply

An Increase in Supply

A Decrease in Supply

No Change in

Demand

P same

Q same

P down

Q up

P up

Q down

An Increase in

Demand

P up

Q up

P ambiguous

Q up

P up

Q ambiguous

A Decrease in

Demand

P down

Q down

P down

Q ambiguous

P ambiguous

Q down

55. Suppose we are analyzing the market for hot chocolate. Graphically illustrate the impact each of the following would

have on demand or supply. Also show how equilibrium price and equilibrium quantity would change.

a.

Winter starts, and the weather turns sharply colder.

b.

The price of tea, a substitute for hot chocolate, falls.

c.

The price of cocoa beans decreases.

d.

The price of whipped cream falls.

e.

A better method of harvesting cocoa beans is introduced.

f.

The Surgeon General of the U.S. announces that hot chocolate cures acne.

g.

Protesting farmers dump millions of gallons of milk, causing the price of milk to rise.

h.

Consumer income falls because of a recession, and hot chocolate is considered a normal

good.

i.

Producers expect the price of hot chocolate to increase next month.

j.

Currently, the price of hot chocolate is $0.50 per cup above equilibrium.