CUSTOM ID:

087.33.5 – MC – MANK08

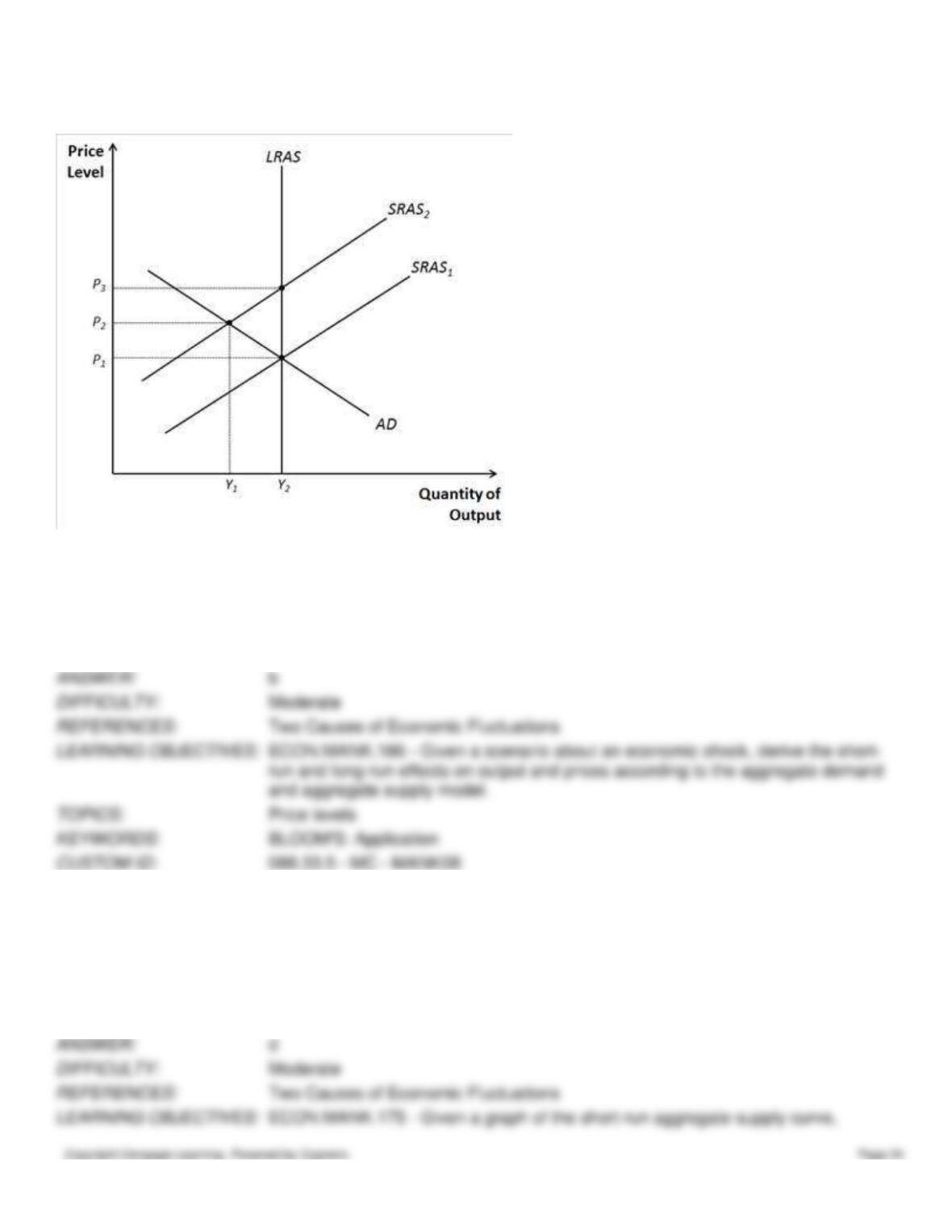

Figure 33-11.

88. Refer to Figure 33–11. A movement from P1 and Y2, to P2 and Y1 would be consistent with

a.

a decrease in consumption expenditures.

b.

stagflation.

c.

sticky-wages.

d.

an increase in net exports.

CUSTOM ID:

088.33.5 – MC – MANK08

89. Suppose that there is an increase in the costs of production that shifts the short-run aggregate supply curve left. If there

is no policy response, then eventually

a.

because unemployment is low, wages will be bid up and short-run aggregate supply will shift right.

b.

because unemployment is low, wages will be bid down and short-run aggregate supply will shift right.

c.

because unemployment is high, wages will be bid up and short-run aggregate supply will shift right.

d.

because unemployment is high, wages will be bid down and short-run aggregate supply will shift right.

90. Other things the same, an increase in the expected price level shifts

a.

short-run aggregate supply right.

b.

short-run aggregate supply left.

c.

aggregate-demand right.

d.

aggregated-demand left.

91. The short-run effects of an increase in the expected price level include

a.

a lower level of output and a lower price level.

b.

a lower level of output and a higher price level.

c.

a higher level of output and a lower price level.

d.

a higher level of output and a higher price level.

92. Which of the following would raise the price level in both the short and long run?

a.

an increase in taxes

b.

an increase in government expenditures

c.

a decrease in the minimum wage

d.

an increase in the capital stock

93. Which of the following would cause prices to rise and real GDP to fall in the short run?

a.

an increase in the expected price level.

b.

an increase in the capital stock.

c.

an increase in the money supply.

d.

an increase in taxes.

94. Which of the following will reduce the price level and real output in the short run?

a.

an increase in government purchases.

b.

an decrease in oil prices

c.

a decrease in the money supply

d.

technical progress

95. Imagine the U.S. economy is in long-run equilibrium. Then suppose the value of the U.S. dollar decreases. At the

same time, people in the U.S. revise their expectations so that the expected price level rises. We would expect that in the

short-run

a.

real GDP will rise and the price level might rise, fall, or stay the same.

b.

real GDP will fall and the price level might rise, fall, or stay the same.

c.

the price level will rise, and real GDP might rise, fall, or stay the same.

d.

the price level will fall, and real GDP might rise, fall, or stay the same.

96. Suppose the economy is in long-run equilibrium. If there is an increase in the supply of labor as well as an increase in

the money supply, then we would expect that in the short-run,

a.

real GDP will rise and the price level might rise, fall, or stay the same.

b.

real GDP will fall and the price level might rise, fall, or stay the same.

c.

the price level will rise, and real GDP might rise, fall, or stay the same.

d.

the price level will fall, and real GDP might rise, fall, or stay the same.

97. Suppose that the economy is at long-run equilibrium. If there is a sharp rise in the stock market combined with a

significant increase in the minimum wage, then in the short run

a.

real GDP will rise and the price level might rise, fall, or stay the same.

b.

real GDP will fall and the price level might rise, fall, or stay the same.

c.

the price level will rise, and real GDP might rise, fall, or stay the same.

d.

the price level will fall, and real GDP might rise, fall, or stay the same.

98. Suppose the economy is in long-run equilibrium. If there is an increase in government purchases at the same time

there is a large increase in the price of oil, then in the short-run

a.

real GDP will rise and the price level might rise, fall, or stay the same.

b.

real GDP will fall and the price level might rise, fall, or stay the same.

c.

the price level will rise, and real GDP might rise, fall, or stay the same.

d.

the price level will fall, and real GDP might rise, fall, or stay the same.

99. Suppose the economy is in long-run equilibrium. Concerns about pollution cause the government to significantly

restrict the production of electricity. At the same time, taxes fall. In the short-run

a.

real GDP will rise, and the price level might rise, fall, or stay the same.

b.

real GDP will fall, and the price level might rise, fall, or stay the same.

c.

the price level will rise, and real GDP might rise, fall, or stay the same.

d.

the price level will fall, and real GDP might rise, fall, or stay the same.

100. Suppose the economy is in long-run equilibrium. Senator A succeeds in getting taxes raised. At the same time,

Senator B succeeds in getting major restrictions on logging removed. In the short run

a.

real GDP will rise and the price level might rise, fall, or stay the same.

b.

real GDP will fall and the price level might rise, fall, or stay the same.

c.

the price level will rise, and real GDP might rise, fall, or stay the same.

d.

the price level will fall, and real GDP might rise, fall, or stay the same.

101. Suppose the economy is in long-run equilibrium. In a short span of time, there is a sharp rise in the stock market, an

increase in government purchases, an increase in the money supply and a decline in the value of the dollar. In the short

run

a.

the price level and real GDP will both rise.

b.

the price level and real GDP will both fall.

c.

neither the price leave nor real GDP will change.

d.

All of the above are possible.

102. Suppose the economy is in long-run equilibrium. In a short span of time, there is a sharp increase in the supply of

labor, a major new discovery of oil, and new environmental regulations that raise the cost of electricity production. In the

short run

a.

the price level will rise and real GDP will fall.

b.

the price level will fall and real GDP will rise.

c.

the price level and real GDP will both stay the same.

d.

All of the above are possible.

103. Suppose the economy is in long-run equilibrium. In a short span of time, there is a large influx of skilled immigrants,

a major new discovery of oil, and a major new technological advance in electricity production. In the short run, we would

expect

a.

the price level to rise and real GDP to fall.

b.

the price level to fall and real GDP to rise.

c.

the price level and real GDP both to stay the same.

d.

All of the above are possible.

104. Suppose the economy is in long-run equilibrium. If there is a sharp increase in the minimum wage as well as an

increase in taxes, then in the short run, real GDP will

a.

rise and the price level might rise, fall, or stay the same. In the long run, the price level might rise, fall, or stay

the same but real GDP will be unaffected.

b.

fall and the price level might rise, fall, or stay the same. In the long run, the price level might rise, fall, or stay

the same but real GDP will be unaffected.

c.

rise and the price level might rise, fall, or stay the same. In the long run, the price level might rise, fall, or stay

the same but real GDP will be lower.

d.

fall and the price level might rise, fall, or stay the same. In the long run, the price level might rise, fall, or stay

the same but real GDP will be lower.

105. Suppose the economy is in long-run equilibrium. If there is a sharp decline in government purchases combined with a

significant increase in immigration of skilled workers, then in the short run,

a.

real GDP will rise and the price level might rise, fall, or stay the same. In the long-run, real GDP will rise and

the price level might rise, fall, or stay the same.

b.

the price level will fall, and real GDP might rise, fall, or stay the same. In the long-run, real GDP and the price

level will be unaffected.

c.

the price level will rise, and real GDP might rise, fall, or stay the same. In the long run, real GDP will rise and

the price level will fall.

d.

the price level will fall, and real GDP might rise, fall, or stay the same. In the long run, real GDP will rise and

the price level will fall.

106. In 1986, OPEC countries increased their production of oil. This caused

a.

the price level to rise.

b.

aggregate supply to shift right.

c.

unemployment to rise.

d.

None of the above is correct.

107. In the mid-1970s the price of oil rose dramatically. This

a.

shifted aggregate supply left, the price level rose, and real GDP fell.

b.

caused U.S. prices to fall, and real GDP rose.

c.

caused an increase in U.S. prices and real GDP.

d.

caused a decrease in U.S. prices and real GDP.

108. The recessions of the 1970s are often attributed to

a.

declining inflation expectations.

b.

an increase in oil prices.

c.

declines in the price of stock.

d.

decreases in the money supply.

109. Changes in the price of oil

a.

can only lead to recessions.

b.

have not contributed much to output fluctuations in the United States.

c.

change the economy principally by changing aggregate demand.

d.

created both inflation and recession in the United States in the 1970s.

110. The recession of 2008-2009 was preceded by

a.

a sharp decline in housing prices.

b.

large losses among financial institutions that owned mortgage-backed securities.

c.

rises in mortgage defaults and home foreclosures.

d.

all of the above

111. During the 2008-2009 recession real GDP fell by about

a.

2%

b.

4%

c.

6%

d.

8%

112. During the 2008-2009 unemployment rose from about 4.4% to about

a.

6%

b.

8%

c.

10%

d.

12%

113. Which of the following affected aggregate demand during the recession of 2008-2009?

a.

a decline in residential construction and a decrease in lending

b.

a decline in residential construction but not a decrease in lending

c.

a decrease in lending but not a decline in residential construction

d.

neither a decrease in residential construction nor a decrease in lending

114. Which of the following did the Fed do during the recession of 2008-2009?

a.

lowered the federal funds rate and sold securities and loans

b.

lowered the federal funds rate and purchased securities and loans

c.

raised the federal funds rate and sold securities and loans

d.

raised the federal funds rate and purchased securities and loans

115. Which of the following correctly describes actions of the U.S. government during the recession of 2008-2009?

a.

It refused to provide banks funding and made no significant changes in government spending.

b.

It refused to provide banks funding but made a large increase in government spending.

c.

It became part owner of some banks but made no significant change in government spending

d.

It became part owner of some banks and made a large increase in government spending.

116. If a central bank is independent,

a.

it has the ability to alter taxes.

b.

it allocates savings to firms.

c.

it restricts trade to increase domestic employment.

d.

it operations are not controlled by the political process.

117. In 1936, John Maynard Keynes published a book, The General Theory, which attempted to explain

a.

stagflation.

b.

the classical dichotomy.

c.

short-run economic fluctuations.

d.

how changes in the money supply had created the Great Depression.

118. Keynes explained that recessions and depressions occur because of

a.

excess aggregate demand.

b.

inadequate aggregate demand.

c.

excess aggregate supply.

d.

inadequate aggregate supply.

119. Keynes believed that economies experiencing high unemployment should adopt policies to

a.

reduce the money supply.

b.

reduce government expenditures.

c.

increase aggregate demand.

d.

increase aggregate supply.

120. Imagine the U.S. economy is in long-run equilibrium. Then suppose the aggregate demand increases. We would

expect that in the long-run the price level would

a.

increase.

b.

decrease.

c.

stay the same.

d.

decrease by the same amount as the increase in aggregate demand.