Consider Company A with a zero earnings retention ratio and a real growth rate in

earnings of

%. In an inflationary environment, the company can only pass inflation through its

earnings

at a flow-through rate of %. So if I is the inflation rate, its earnings will grow at a

rate of

g = + . The real rate of return required for this company is , so the nominal rate

of return required is = + I.

Use a simple dividend discount model (DDM) assuming that dividends will grow

indefinitely at a constant compounded annual growth rate (CAGR), g = + .

a. Derive formulas equivalent of Equations (6.7) and (6.8), which assumed no real

growth in earnings. Discuss the results.

b. Use these formulas to calculate P/E ratio on prospective earnings with the following

data on Company A: = 2%, I = 4%, = 4%, = 100%.

c. Same question for a Company B, whose inflation pass-through rate is only 80%.

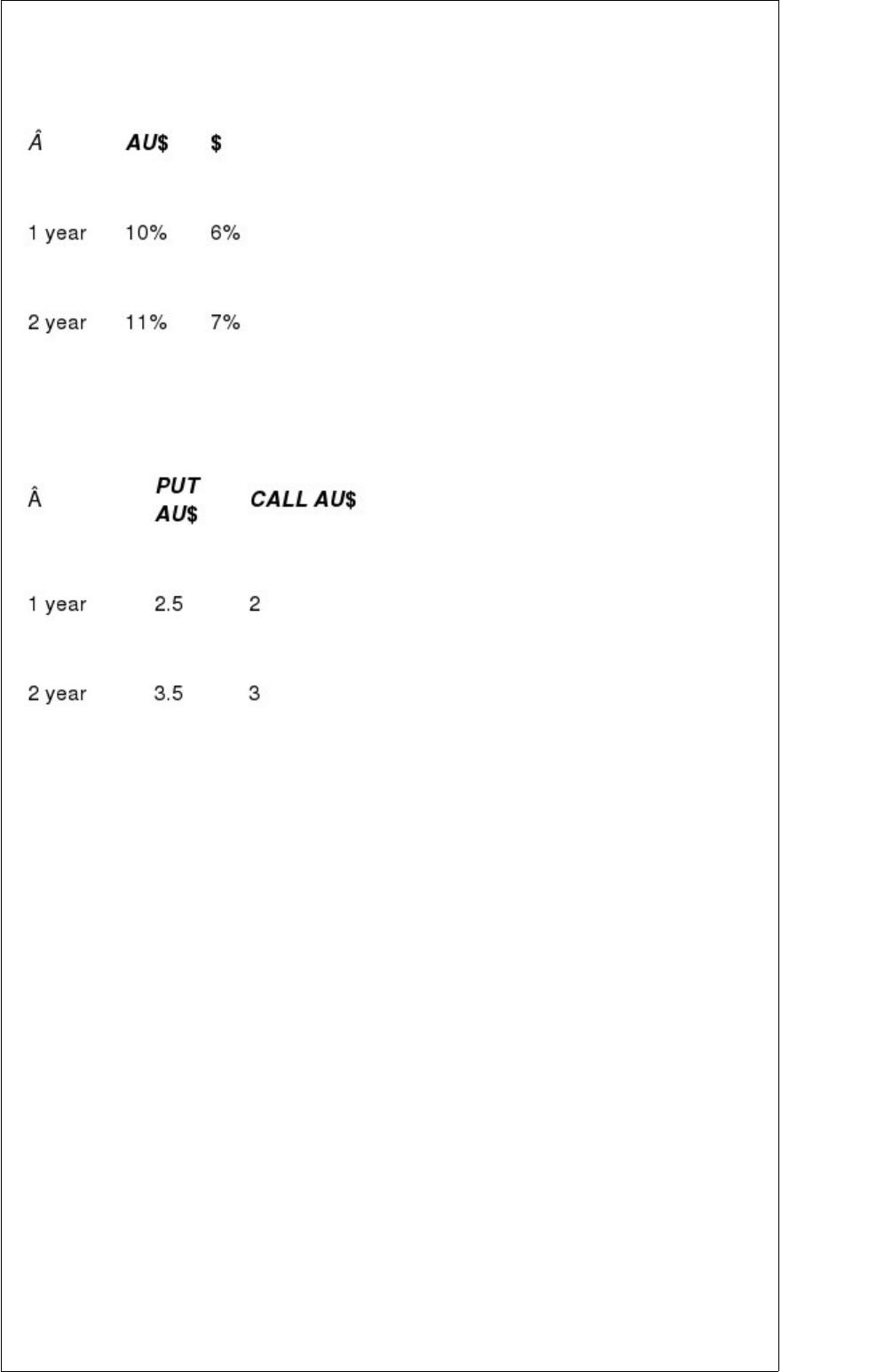

A young investment banker meets one of its clients, SOSO Inc. that is based in Sydney,

Australia.

Current market conditions are the following:

FX Spot rate: AU$/$ = 2.

Interest rate (zero-coupon):

Quote in U.S.$ cents for options (strike price: 50 cents per AU$).

For example a PUT AU$, traded in Chicago, gives the right to sell 1 Australian dollar

(AU$) at

50 cents in a year. Its current price is 2.5 cents per AU$.

SOSO would like to issue a bond paying a fixed annual coupon of 6 AU$ and to be

reimbursed in a year 100 AU$ or 50$ at the bearer’s choice.

a. Assuming that the bond is actually issued at 105 AU$, what is the implicit price of

the option linked to that bond? Would you recommend that bond to an investor?

b. If the market was efficient, what is the normal issue price for such a bond?

After many thoughts, SOSO agrees to issue instead a dual-currency bond with an

annual coupon in AU$ and a nominal to be reimbursed in US$ with the following

characteristics:

– Issue Price: 100 AU$.

– Reimbursement Price: 50$

– Maturity: 2 years.

– Annual Coupon: C AU$.

c. Under current market conditions, at what level should Coupon C on the

dual-currency

bond be set?

Consider two companies based in a country with an inflation rate of 2%. There is no

real growth in earnings. The real rate of return required by global investors for this type

of stock investment is 5%.

a. Assume that the Company A can only pass 60% of inflation through its earnings.

What should be its P/E using prospective earnings?

b. Assume that the Company B can pass the full inflation through its earnings. What

should be its P/E using prospective earnings?

Paf is a small country. Its currency is the pif and the exchange rate with the U.S. dollar

was 2 pifs

per dollar in 1980. The inflation indexes in 1980 were equal to 100 in the United States

and in Paf. Twenty years later, the inflation indexes were equal to 400 in the United

States and 200 in Paf. The current exchange rate is 0.9 pifs per dollar.

a. What should the current exchange rate be if PPP prevailed?

b. Is the Pif over/undervalued according to PPP?

Back in 1990, East Germany was in the process of merging into West Germany. Its

national currency was to be replaced by the Deutsche mark (DM). A U.S. dollar-based

investor has a portfolio worth DM 100 million in German bonds. The current spot

exchange rate is 2 DM/$. The current one-year market interest rates are 6% in DM and

10% in dollars. One-year currency options are quoted in Chicago with a strike price of

50 U.S. cents per DM; a call DM is quoted at 1 U.S. cent and a put

DM is quoted at 1.2 U.S. cents; these option prices are for one DM.

You are worried that the integration of East and West Germany will cause inflation in

Germany and a drop in the DM. So, you consider using forward contracts or options to

hedge the currency risk.

a. What is the one-year forward exchange rate DM/$?

b. Simulate the dollar value of your portfolio assuming that its DM value stays at DM

100 million; use DM/$ spot exchange rates equal in one year to: 1.6, 1.8, 2, 2.2, and

2.4. First consider a currency forward hedge, then a currency-option insurance.

c. What could make your forward hedge imperfect?

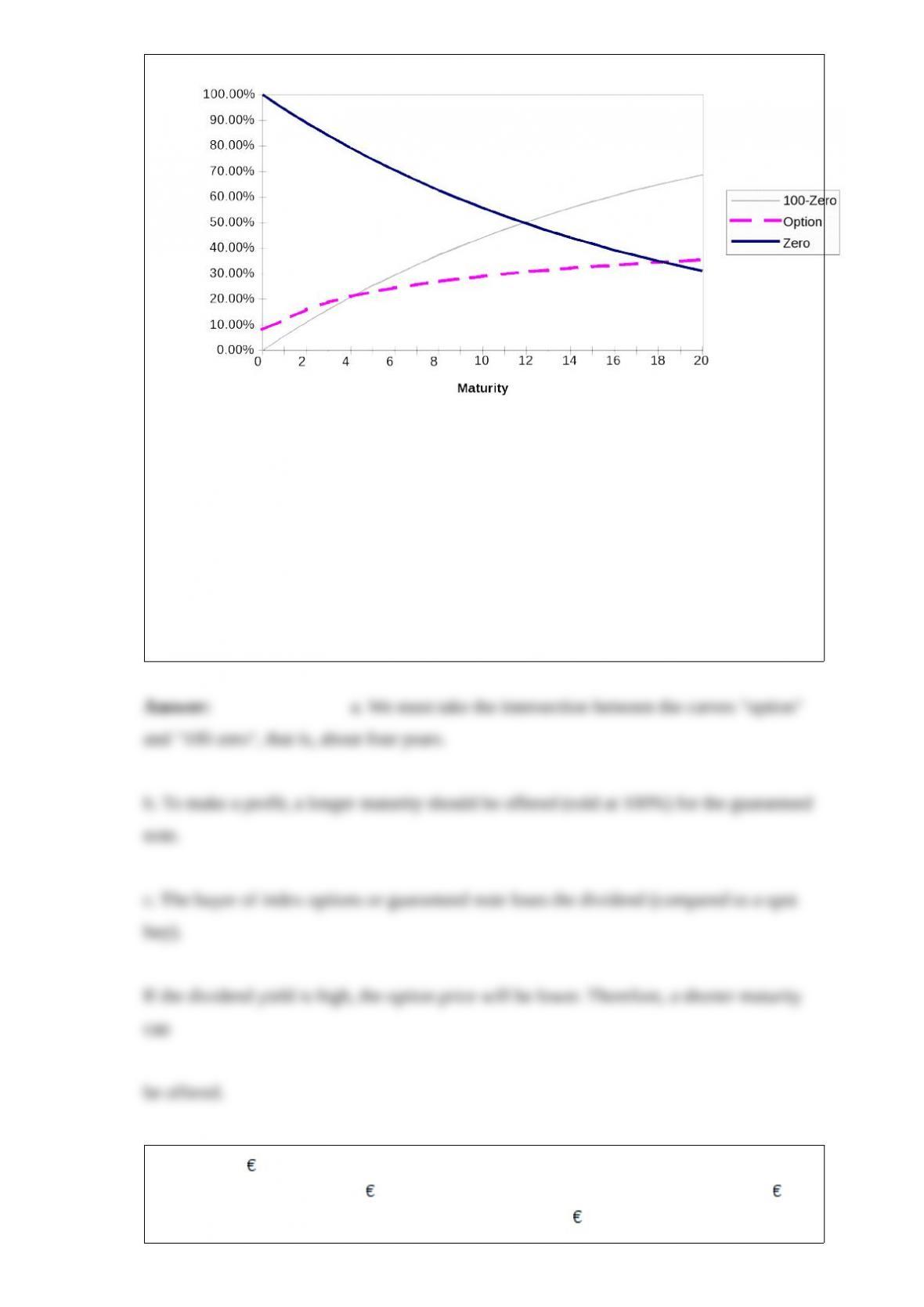

You’re a banker. A client wishes to buy a guaranteed note with a 100% indexation to the

stock index’s growth. In other words, he doesn’t want any coupon but requires 100% of

the index growth. You wonder about the maturity of such a note. You check the prices

of various index calls traded on the market for different maturities. Their strike is the

current index level and their price is expressed as a percentage of this level. (For

instance if the CAC is worth 3,000, the strike is 3,000 and the one-year maturity call

trades at 11% of 3,000. You also check the price of a zero-coupon in percentage for

various maturities. The following graph shows, for each maturity, the price of the

option, that of the zero-coupon, and 100%-zero.

a. What is the maturity of the guaranteed note (coupon =0%, indexation =100%)?

Justify.

b. If as a banker, you want to make a profit, should you lengthen or shorten the maturity

of that note? Explain why.

c. Everything remaining constant (that is, same volatility and interest rate), should the

maturity of the guaranteed note be shorter or longer if the index pays a low dividend

rather than a high one? Why?

A client has 1 million invested in European equity at the start of the quarter. After one

month the portfolio value is 1.1 million and the client who needs cash withdraws

200,000. At the end of the quarter the portfolio is worth 900,000. Over the quarter, the

European equity index, used as a benchmark, gained 15%.

a. What are the rates of returns using the various methods outlined in the text?

b. Which rate should you use to evaluate the performance of the manager relative to its

benchmark?

You noticed that the exchange rate between the Korean won and the U.S. dollar has

changed considerably. The won/dollar exchange rate has moved from 800 won per

dollar to 1000 won per dollar.

a. Has the Korean won appreciated or depreciated with respect to the dollar? By what

percentage?

b. By what percentage has the value of the dollar changed with respect to the won?

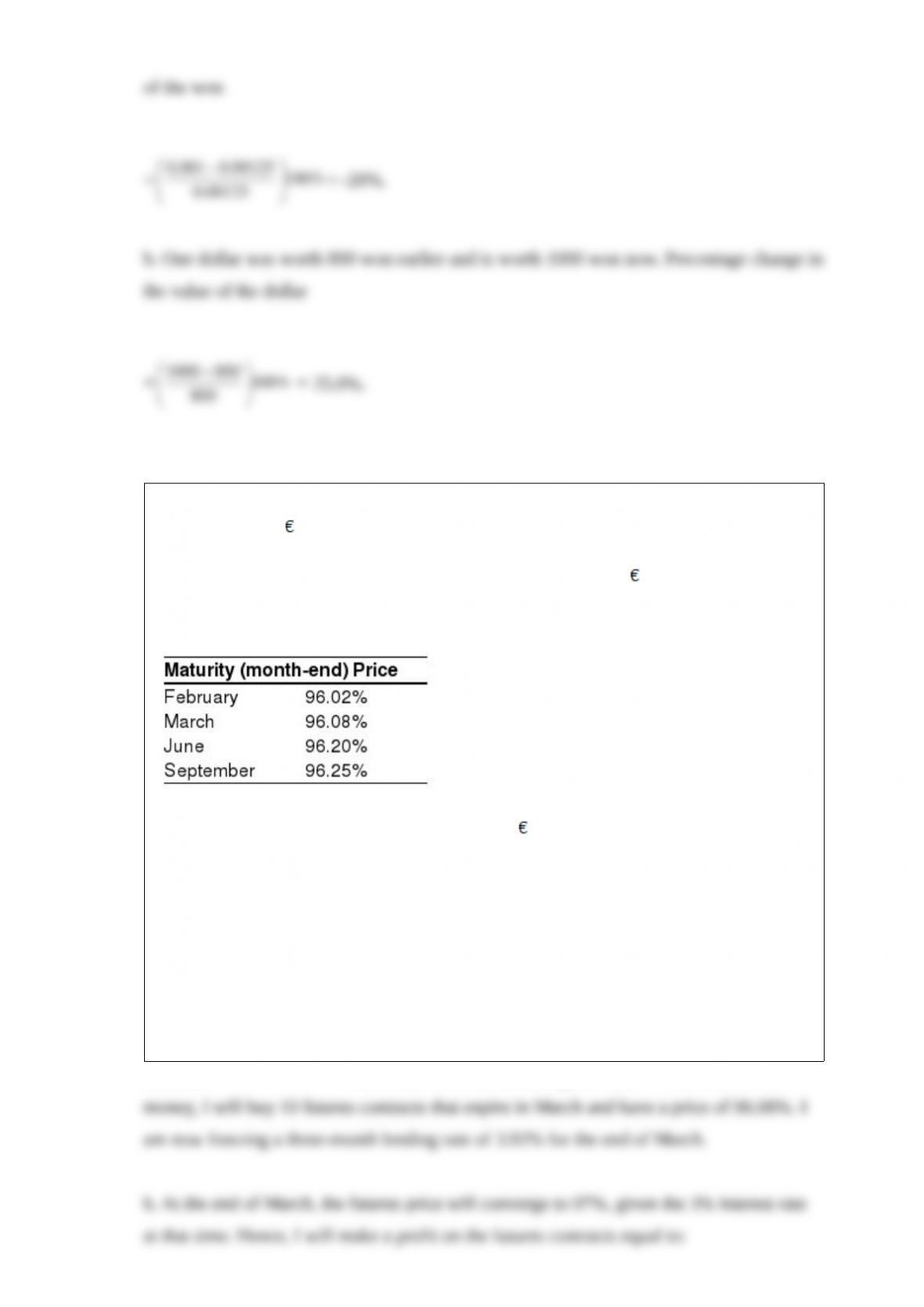

You are the treasurer of a major Japanese construction company. Today is January You

expect to receive 10 million at the end of March, as payment from a client on some

construction work in France. You know that you will need this sum somewhere else in

Europe at the end of June. Meanwhile, you wish to invest these 10 million for three

months. The current three-month interest rate in euros is 4%, but you are worried that it

will quickly drop. Listed below are Euribor futures quotations on EUREX:

a. Knowing that Euribor contracts have a size of 1 million, what should you do to

freeze a lending rate when you will receive the money?

b. At the end of March, when you receive the money, the three-month Euribor is equal

to 3%.

How much money (number of euros) have you gained by engaging in the above

transaction

(as opposed to doing nothing on January 15)?

An American investor believes that the dollar will depreciate and buys one call option

on the euro at an exercise price of 110 cents per euro. The option premium is 1 cent per

euro, or $625 per contract of 62,500 euros (Philadelphia):

a. For what range of exchange rates should the investor exercise the call option at

expiration?

b. For what range of exchange rates will the investor realize a net profit, taking the

original cost

into account?

c. If the investor had purchased a put with the same exercise price and premium, instead

of a call, how would you answer the previous two questions?