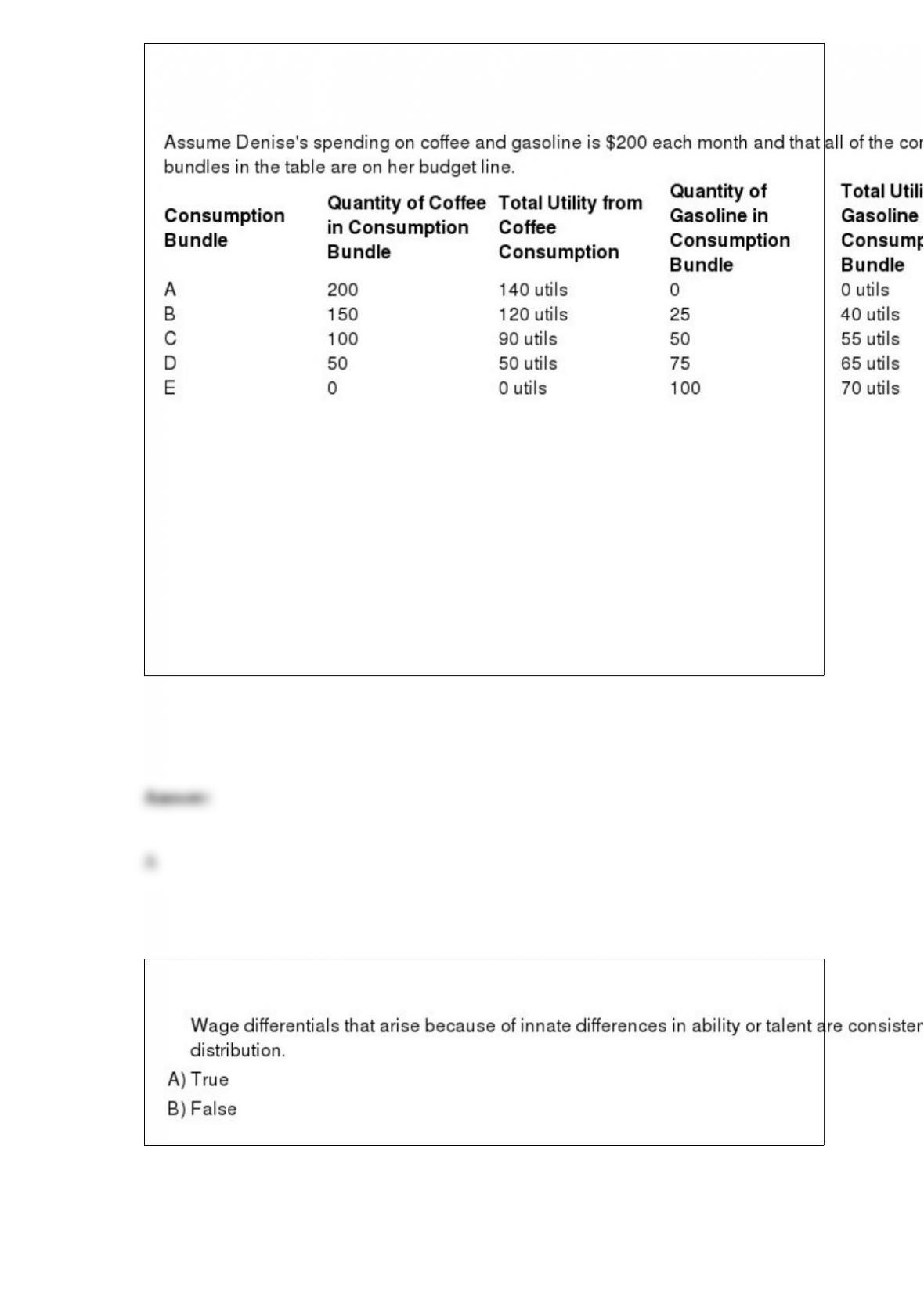

Table: Denise’s Consumption of Coffee and Gasoline

(Table: Denise’s Consumption of Coffee and Gasoline) Look at the table Denise’s

Consumption of Coffee and Gasoline. Suppose Denise initially chooses consumption

bundle A. She can increase her total utility by:

A) consuming more gasoline and less coffee.

B) consuming more coffee and less gasoline.

C) not consuming more coffee or gasoline.

D) consuming more coffee and more gasoline.

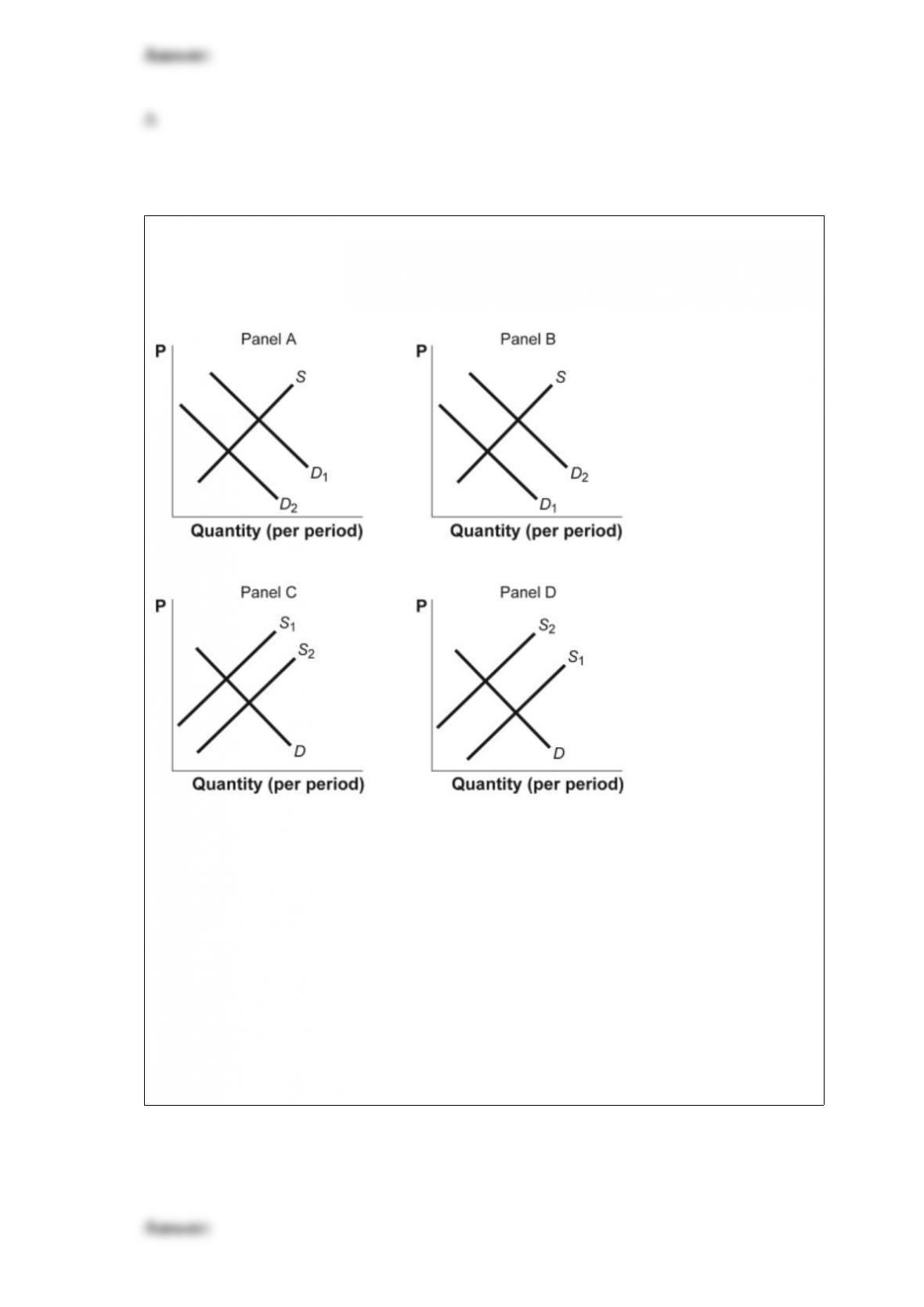

Figure: Shifts in Demand and Supply IV

(Figure: Shifts in Demand and Supply IV) Look at the figure Shifts in Demand and

Supply IV. The figure shows how supply and demand might shift in response to specific

events. Suppose oil becomes more expensive. Which panel BEST describes how this

will affect the market for gasoline, which is made from oil?

A) panel A

B) panel B

C) panel C

D) panel D

Figure: Shifts in Demand and Supply IV

(Figure: Shifts in Demand and Supply IV) Look at the figure Shifts in Demand and

Supply IV. The figure shows how supply and demand might shift in response to specific

events. Suppose half of the people in San Diego pack up and move to Colorado Springs.

Which panel BEST describes how this will affect the supply of houses in San Diego?

A) panel A

B) panel B

C) panel C

D) panel D

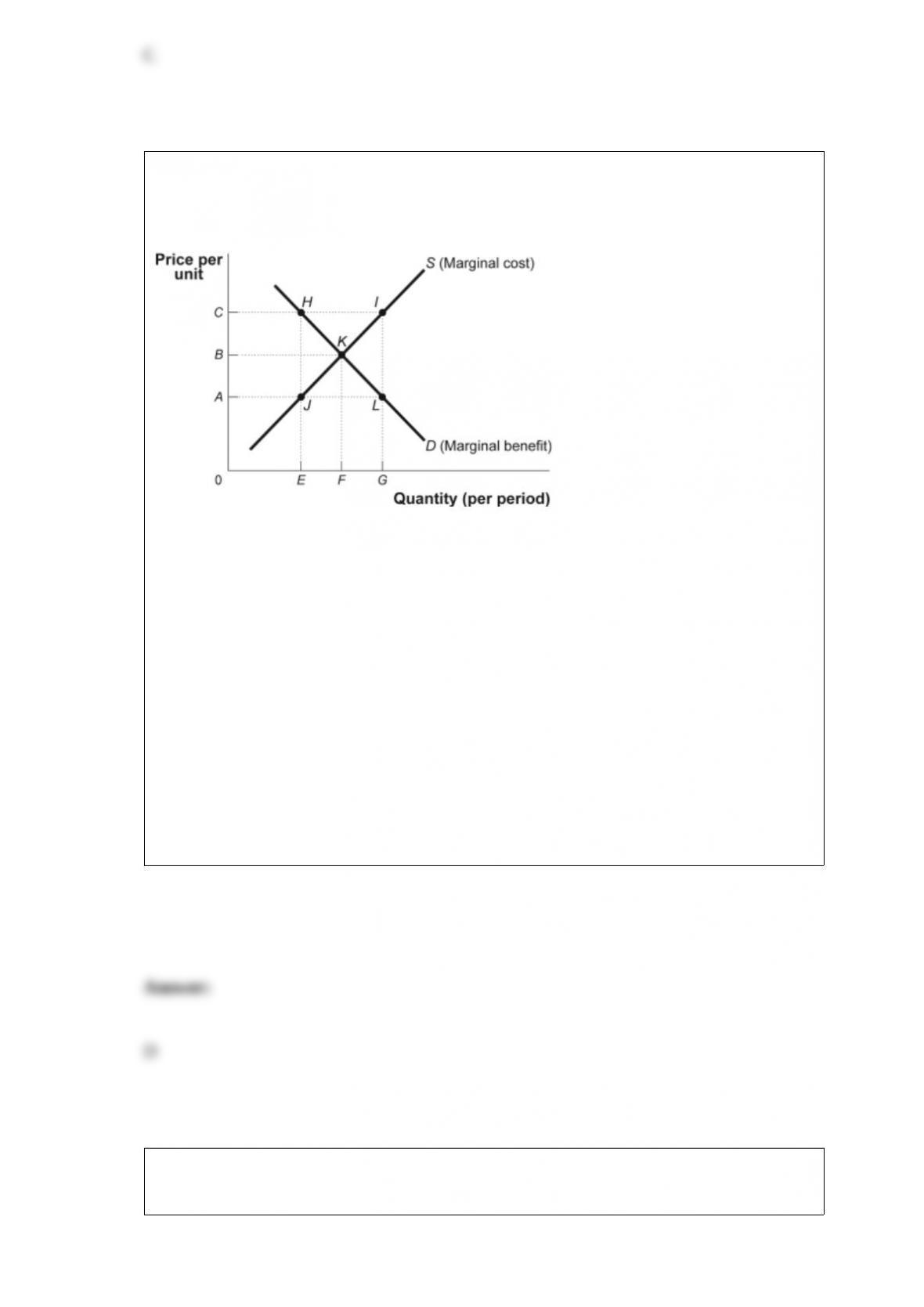

Figure: Market Failure

(Figure: Market Failure) Look at the figure Market Failure. Suppose the supply curve

represents the marginal cost of providing streetlights in a neighborhood that is

composed of two people, Ann and Joe. The demand curve represents the marginal

benefit that Ann receives from the streetlights. Suppose that Joe’s marginal benefit from

the streetlights is a constant amount equal to AC. The marginal social benefit of F

streetlights is:

A) 0.

B) B.

C) less than B.

D) greater than B.

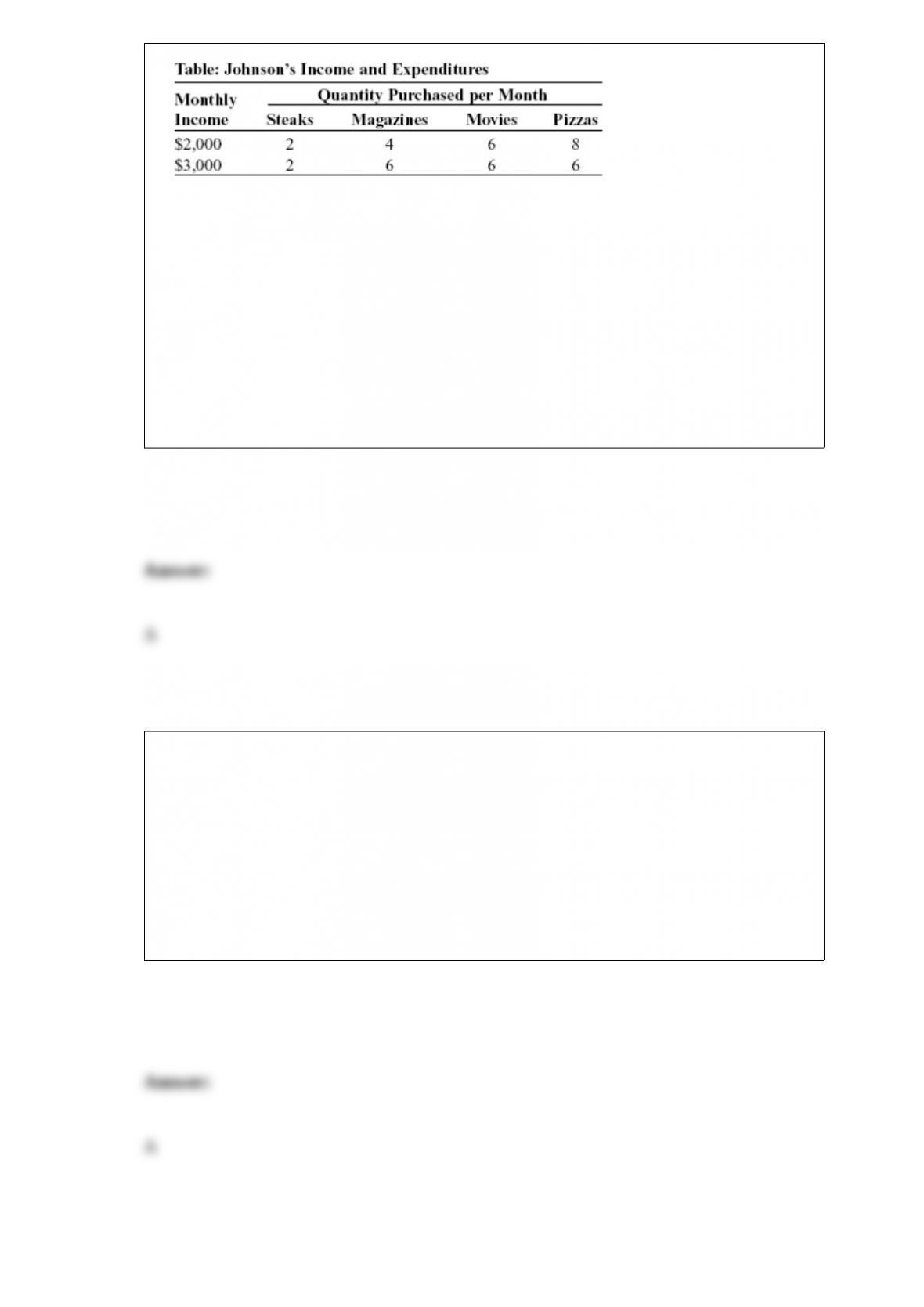

(Table: Johnson’s Income and Expenditures) Look at the table Johnson’s Income and

Expenditures. For Johnson, pizzas are a(n) _____ good.

A) inferior

B) positive

C) neutral

D) normal

Which of the following is an excise tax?

A) a tax of $0.41 per gallon of gas

B) a tax of 12.4% of your wages

C) a tax on the value of your property

D) a one-time local per capita tax of $50

Which of the following U.S. welfare programs is a monetary benefit that is NOT

means-tested?

A) Earned Income Tax Credit

B) Social Security

C) food stamps

D) Medicaid

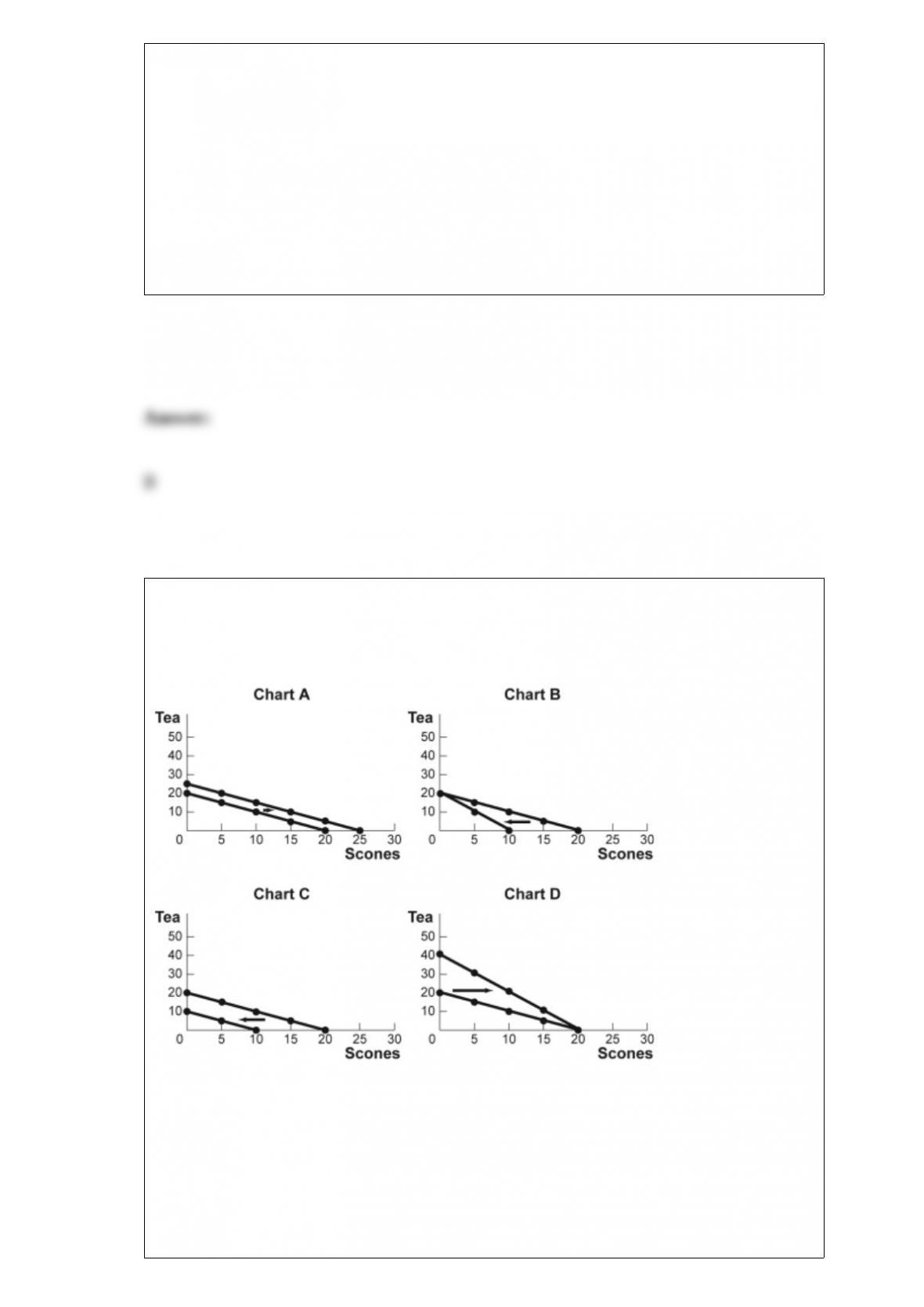

Figure: Budget Lines for Tea and Scones

(Figure: Budget Lines for Tea and Scones) Look at the figure Budget Lines for Tea and

Scones. For months now, Agnes has had $20 per month to spend on tea and scones. The

price of each cup of tea and each scone has been $1. Which of the charts shows what

will happen to her budget line if her income decreases to $10?

A) A

B) B

C) C

D) D

I know when I shop at the local grocery store, I am helping my community. This

statement best represents this economic concept:

A) People usually exploit opportunities to make themselves better off.

B) There are gains from trade.

C) One person’s spending is another person’s income.

D) Overall spending sometimes gets out of line with the economy’s productive capacity.

The labor demand curve in a perfectly competitive factor market is the horizontal sum

of all firms’ _____ product of labor curves.

A) marginal

B) value of the marginal

C) marginal physical

D) average physical

Until recently Rosemarie worked as an accountant, earning $30,000 annually. Then she

inherited a piece of commercial real estate that had been renting for $12,000 annually.

Rosemarie decided to leave her job and operate a Peruvian restaurant in the space she

inherited. At the end of the first year, her books showed total revenues of $260,000 and

total costs of $230,000 for food, utilities, cooks, and other supplies. Her economic

profit at the end of one year is:

A) $230,000.

B) $30,000.

C) $0.

D) “$12,000.

Figure: The Market for Gas Stations

(Figure: The Market for Gas Stations) The figure The Market for Gas Stations shows

curves facing a typical gas station in a large town. The market is characterized by many

firms, differentiated products, easy entry, and easy exit. If the gas station here is typical,

prices charged by firms in the market are likely to:

A) fall in the long run.

B) rise in the long run.

C) remain unchanged.

D) rise dramatically in the long run.

Economic growth that is not industry-specific is most likely to:

A) have no effect on most businesses.

B) result in many businesses doing well.

C) result in many businesses not doing well.

D) affect only a few select businesses.

Price leadership occurs if:

A) smaller firms in an industry silently agree to charge the same price as the largest

firm.

B) two or more firms in an industry agree to fix the price at a given level.

C) competition among a large number of small firms generates a stable market price.

D) competition among a large number of small firms generates similar but slightly

different prices.

Suppose that the market for candy canes operates under conditions of perfect

competition, that it is initially in long-run equilibrium, that the price of each candy cane

is $0.10, and that the market demand curve is downward-sloping. The price of sugar

rises, increasing the marginal and average total costs of producing candy canes by

$0.05. In the short run a typical producer of candy canes will be making:

A) an economic profit.

B) zero economic profit.

C) negative economic profit.

D) The answer is impossible to determine from the information given.

José, a corn farmer operating in a perfectly competitive market, pays his workers $8 an

hour. At his current level of labor use, the marginal product of an additional hour of

labor is three bushels of corn. The market price of corn is $2.75. To maximize his

profits, Jose should:

A) hire more labor.

B) hire less labor.

C) not change the amount of labor.

D) This question cannot be answered without knowing the average product of labor.

The ability of a monopolist to raise the price of a product above the competitive level

by reducing the output is known as:

A) product differentiation.

B) barrier to entry.

C) market power.

D) patents and copyrights.

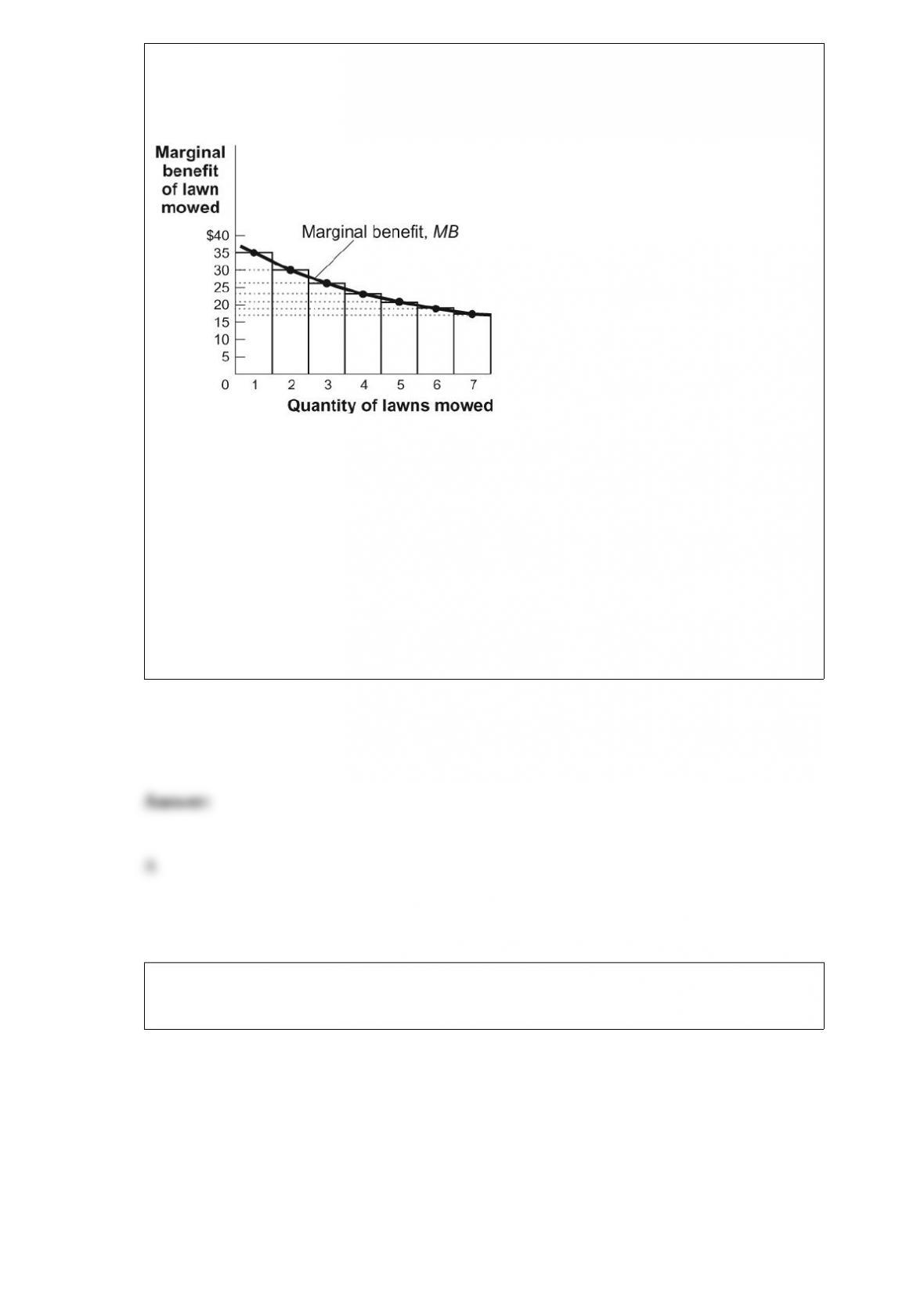

Figure: The Marginal Benefit Curve

(Figure: The Marginal Benefit Curve) Look at the figure The Marginal Benefit Curve.

The total benefit of mowing seven lawns is approximately:

A) $172.

B) $140.

C) $60.

D) $18.

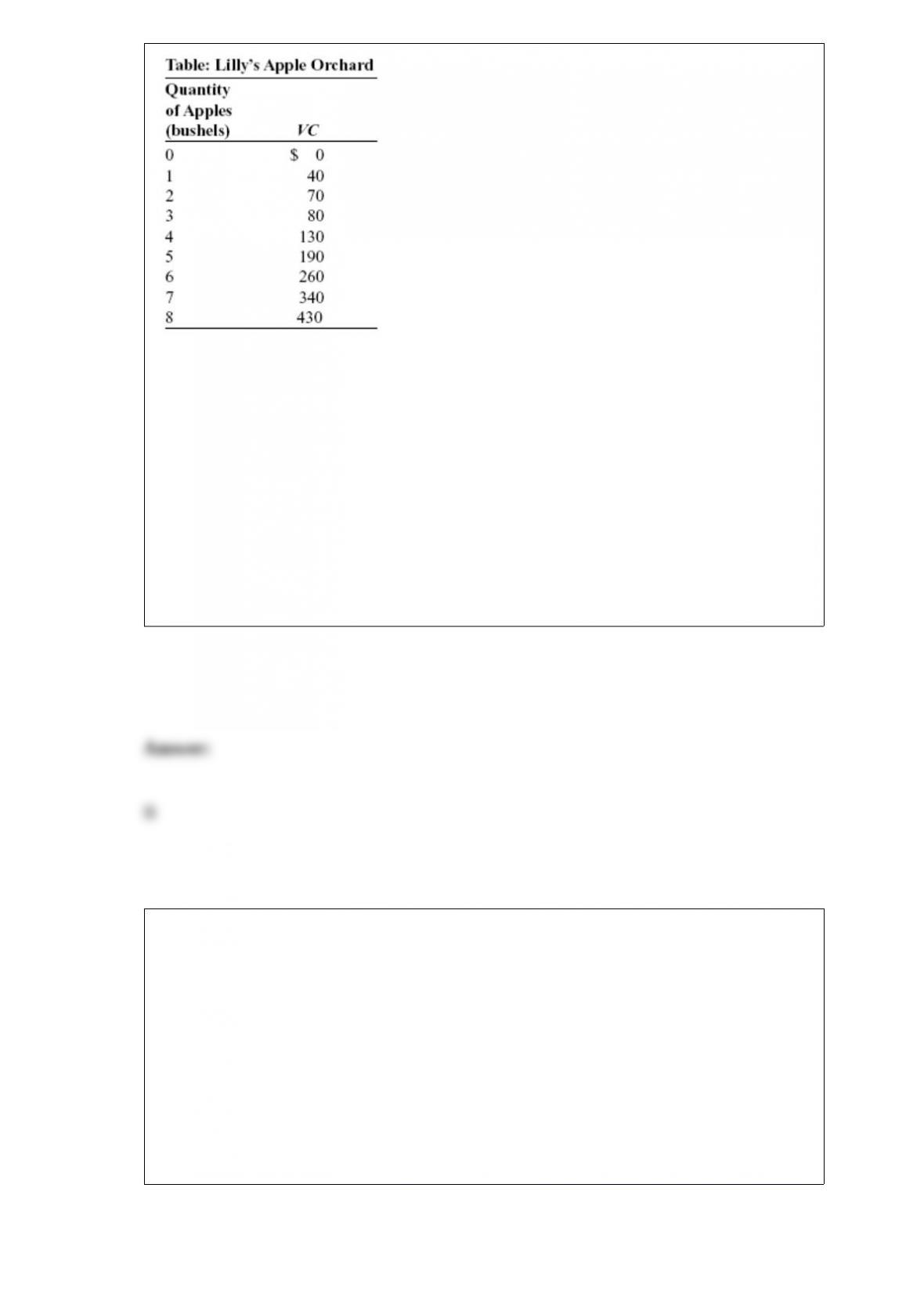

(Table: Lilly’s Apple Orchard) Look at the table Lilly’s Apple Orchard. Lilly is the

price-taking owner of an apple orchard. Her orchard has fixed costs of $30. If the price

of a bushel of apples is $35, her economic profit will be:

A) “$30

B) “$5

C) $0

D) $5

If the price is greater than the average variable cost and less than the average total cost

at the profit-maximizing quantity of output in the short run, a perfectly competitive firm

will:

A) continue to produce at an economic loss.

B) earn an economic profit.

C) encourage other firms to enter the industry.

D) produce more than the profit-maximizing quantity.

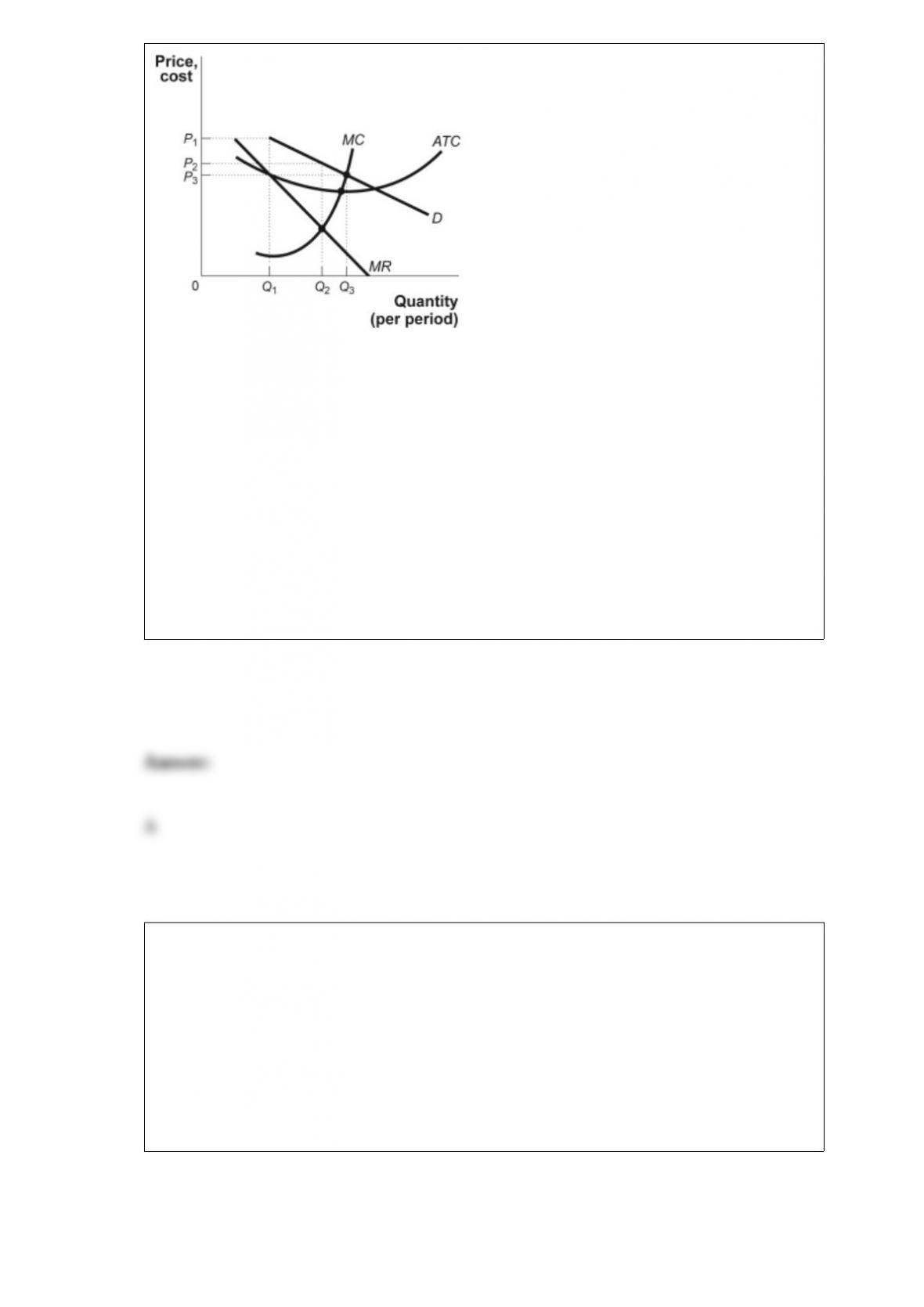

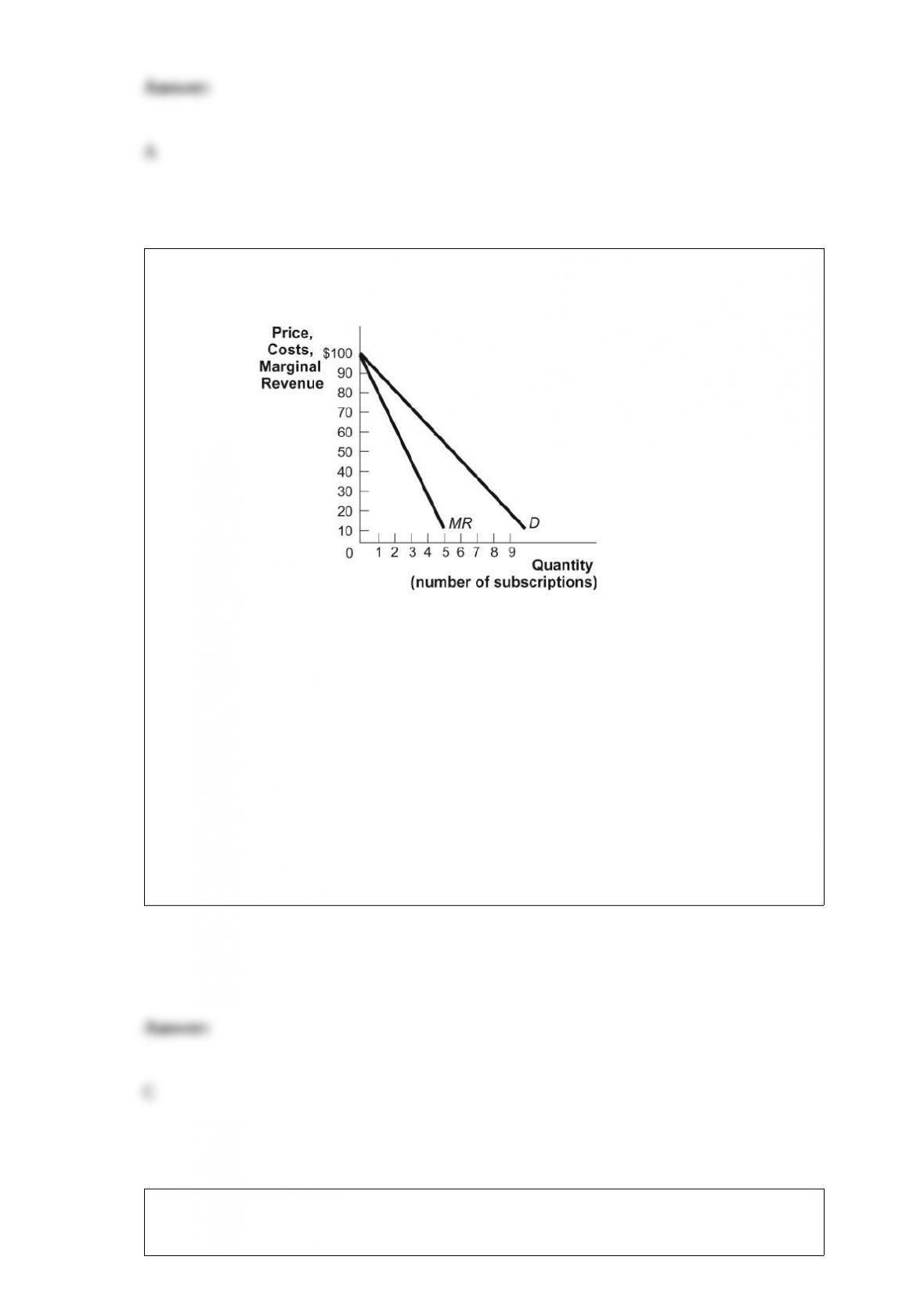

Figure: PPV

(Figure: PPV) Look at the figure PPV, which shows the demand and marginal revenue

for a pay-per-view football game on cable TV. Assume that the marginal cost and

average cost are a constant $20. If the cable company is a monopoly, how much is

deadweight loss when the monopolist maximizes profit?

A) $0

B) $20

C) $80

D) $160

An excise tax is levied on:

A) each unit of a good or service that is sold.

B) earnings.

C) the ownership of real estate.

D) the inheritance of assets.

As a result of frequent flooding, the insurance market has noted a positive correlation

between flooding and the amount of insurance monies paid out for such floods. Holding

demand for insurance constant, if flooding is expected to continue to be a problem,

flood insurance premiums will most likely:

A) rise.

B) fall.

C) stay the same.

D) rise, fall, or stay the same.

Suppose the wealth of buyers in the insurance market falls. We would expect insurance

premiums to _____ as the _____ curve shifts _____.

A) rise; supply; left

B) fall; supply; right

C) fall; demand; left

D) rise; demand; right

Faruq spends all of his income on tacos and milkshakes. His income is $100, the price

of tacos is $10, and the price of milkshakes is $2. Put tacos on the horizontal axis and

milkshakes on the vertical axis. If Faruq spends all of his income, the opportunity cost

of one taco equals _____ milkshakes.

A) 2

B) 10

C) 5

D) 1/5

An economy is efficient if it is:

A) possible to produce more of all goods and services.

B) possible to produce more of one good without producing less of another.

C) not possible to produce more of one good without producing less of another good.

D) producing a combination of goods.

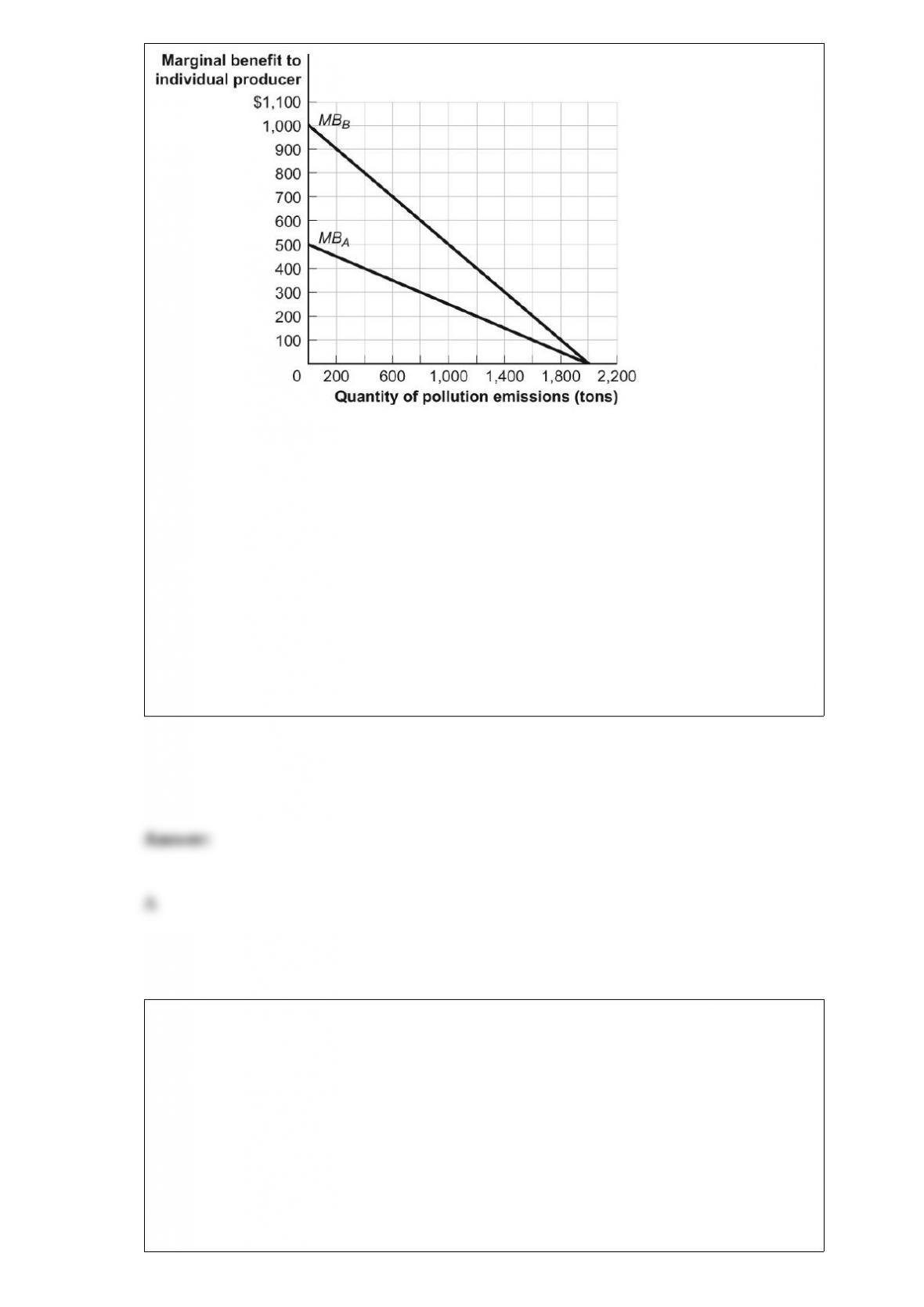

Figure: City with Two Polluters

(Figure: City with Two Polluters) Look at the figure City with Two Polluters. If the

government does not intervene in the pollution market, equilibrium will occur where

firm A produces _____ tons and firm B produces _____ tons of pollution, for a total of

_____ tons.

A) 2,000; 2,000; 4,000

B) 0; 1,000; 1,000

C) 1,000; 0; 1,000

D) 800; 1,400; 2,200

The typical supply curve illustrates that:

A) other things equal, the quantity supplied for a good is inversely related to the price

of a good.

B) other things equal, the supply of the good creates its own demand for the good.

C) other things equal, the quantity supplied for a good is positively related to the price

of a good.

D) price and quantity supplied are unrelated.