Behavioral economists have found that people are more willing to save if saving is the

default option, as in the case in which they have to opt out of an automatic payroll

deduction savings plan. Economists call this:

A. a rule of thumb.

B. the ultimatum game.

C. the status quo bias.

D. bounded rationality.

Answer:

An economist who looks at the data that suggest that people are making decisions that

are based on rules of thumb and concludes that people tend to make decisions that are

based on habit and not on the economic decision rule is most likely to be a(n):

A. traditional economist.

B. behavioral economist.

C. irrational economist.

D. engineering economist.

Answer:

The law of demand states that the quantity demanded of a good is inversely related to

the price of that good. Therefore, as the price of a good goes:

A. up, the quantity demanded also goes up.

B. up, the quantity demanded goes down.

C. down, the quantity demanded goes down.

D. down, the quantity demanded stays the same.

Answer:

Maintaining objectivity is easiest in:

A. positive economics.

B. the art of economics.

C. normative economics.

D. subjective economics.

Answer:

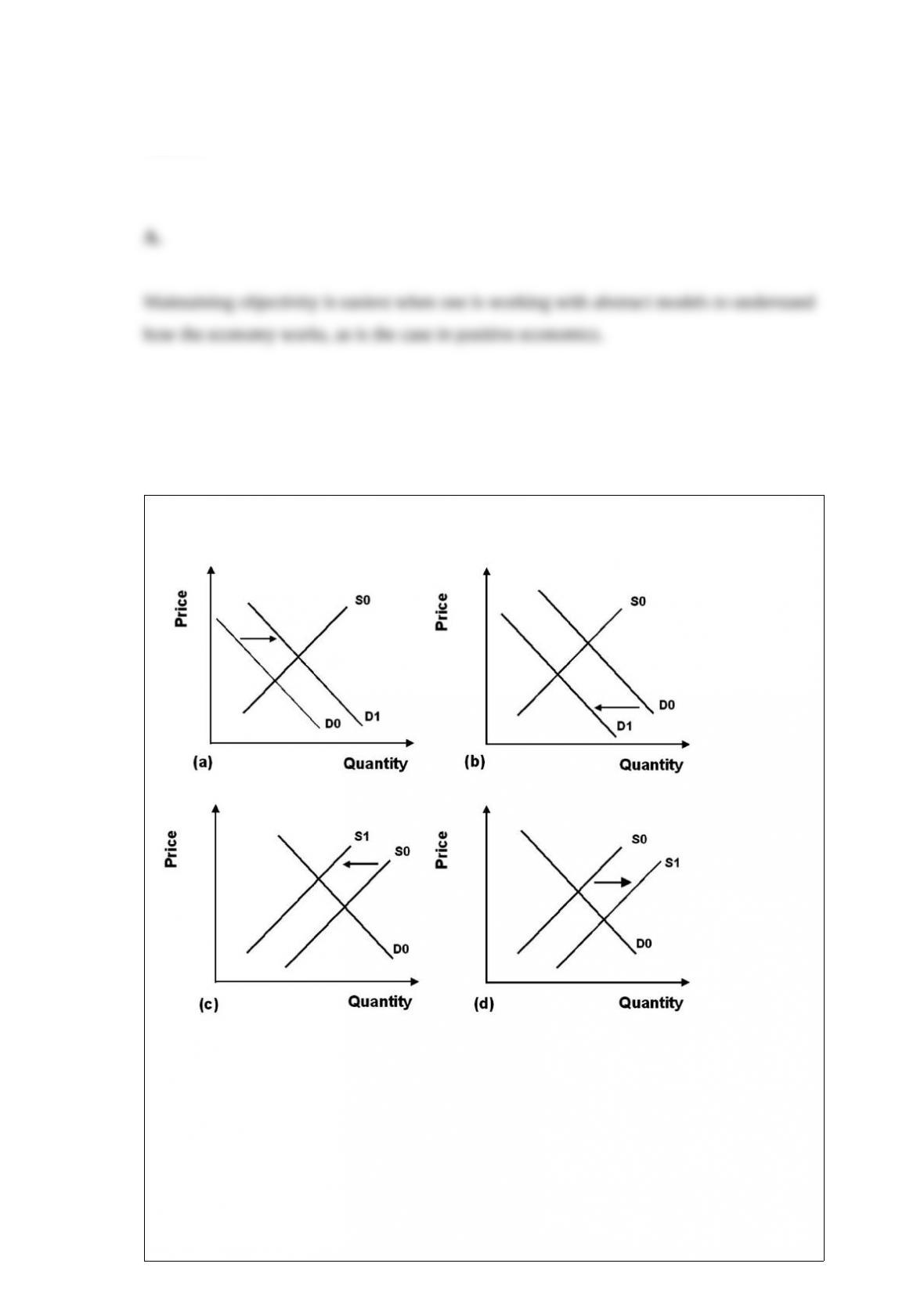

Refer to the graphs shown. The relevant market is corn. The impact of a poor corn

harvest on the market for corn would most likely be demonstrated by which graph?

A. a

B. b

C. c

D. d

Answer:

Being able to find stable patterns in data means that empirical models can be labeled as:

A. butterfly effect models.

B. heuristic models.

C. pattern-finding models.

D. traditional models.

Answer:

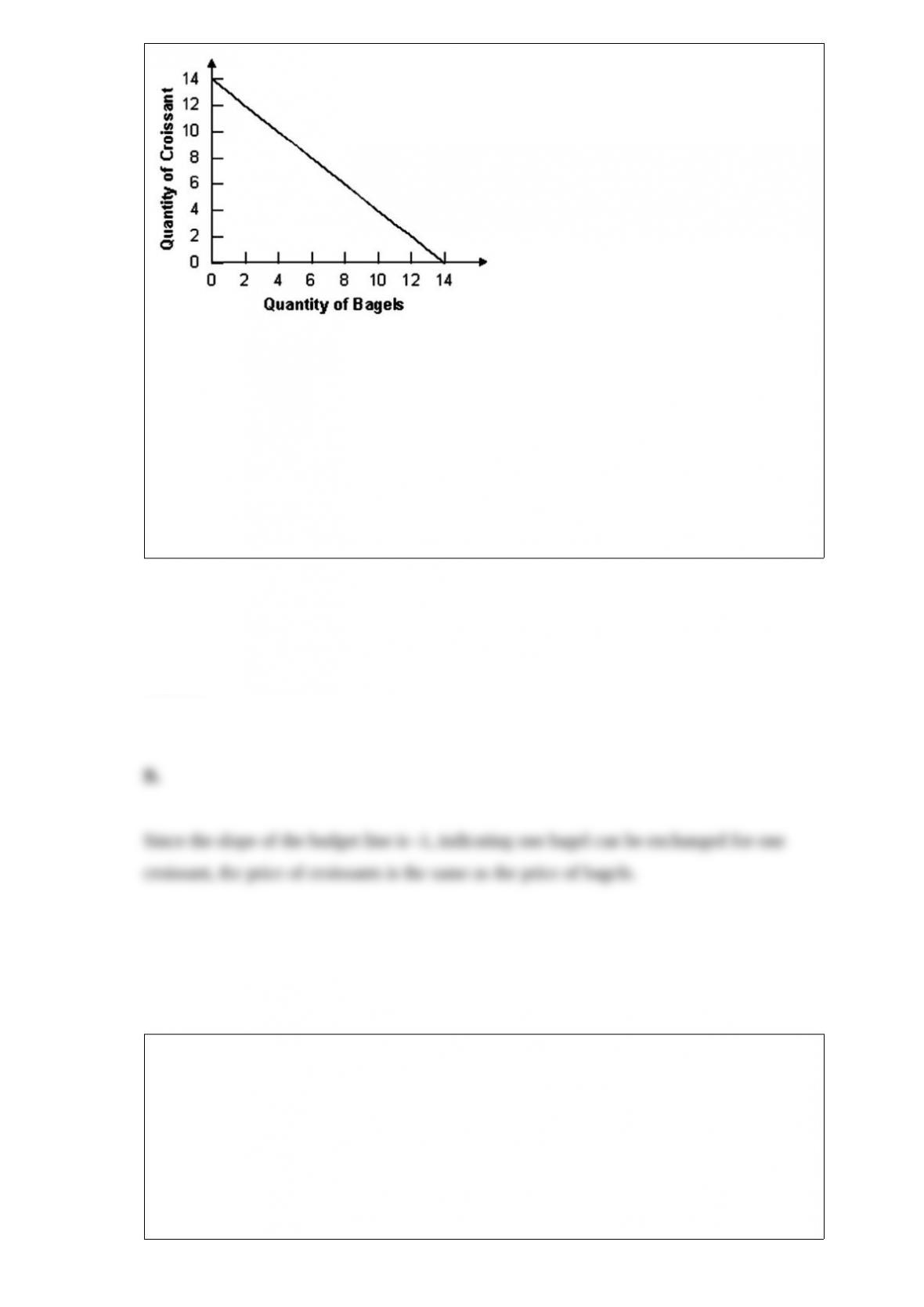

Refer to the graph shown. Given this budget constraint, if bagels cost $1.80 each,

croissants must cost:

A. $0.90 each.

B. $1.80 each.

C. $3.60 each.

D. It is impossible to know from the information given.

Answer:

Susan Athey is the chief economist at Microsoft. She is most likely:

A. an economic scientist.

B. an economic engineer.

C. a heuristic economist.

D. a traditional economist.

Answer:

A higher marginal income tax rate reduces incentives to work because:

A. leisure and other nonmarket activities aren’t taxed, and so their relative price goes

down.

B. leisure and other nonmarket activities aren’t taxed, and so their relative price goes up.

C. the opportunity cost of leisure remains constant while after-tax wages fall.

D. the opportunity cost of leisure increases with the marginal income tax rate.

Answer:

Economic forces:

A. are a reaction to scarcity.

B. give rise to scarcity.

C. are not related to scarcity.

D. are not related to rationing.

Answer:

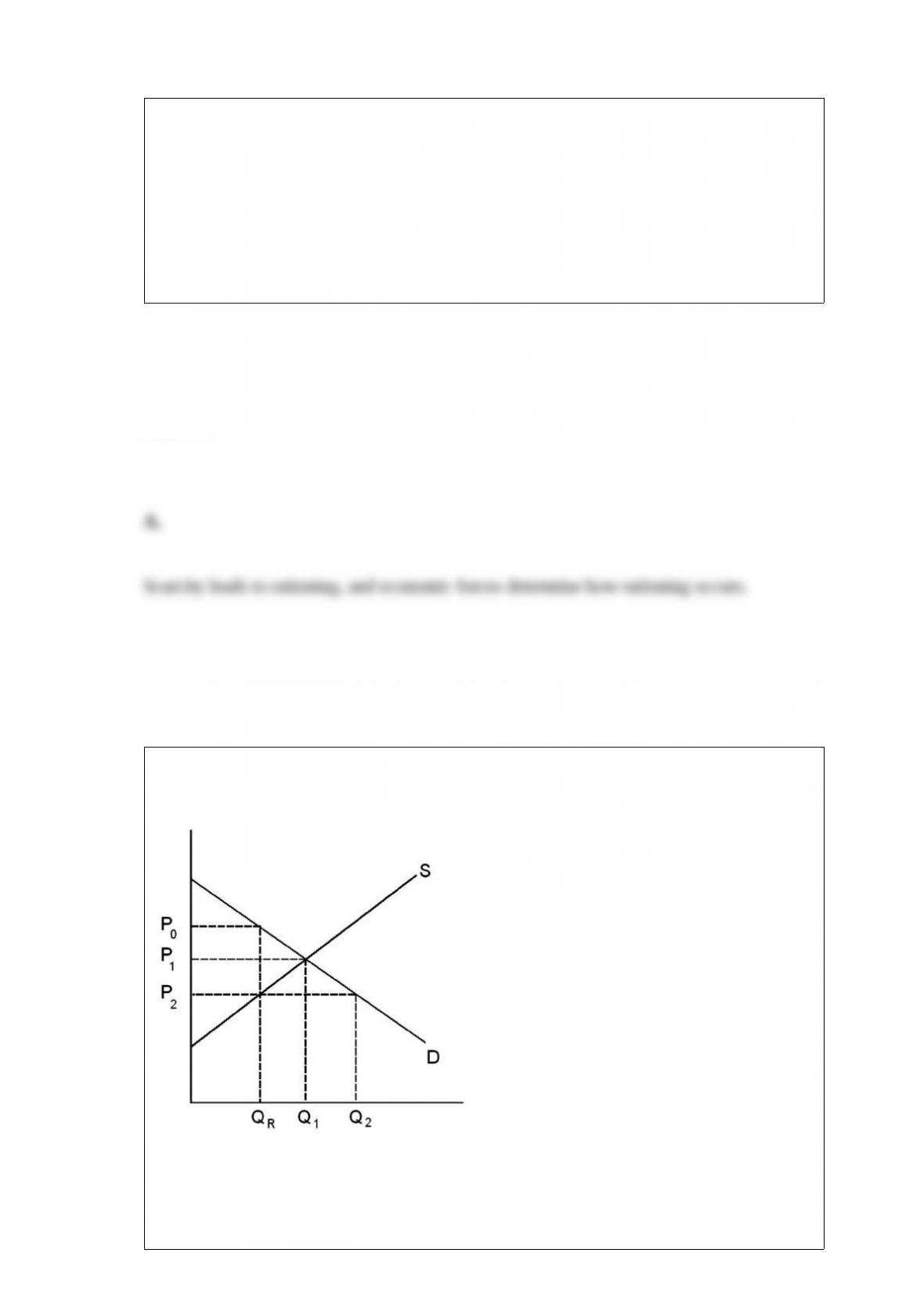

Refer to the graph shown. A quantity restriction of QR will:

A. raise market price to P0.

B. maintain a market price of P1.

C. lower market price to P2.

D. have no effect in the market depicted.

Answer:

Grocery stores in affluent communities tend to sell more premade salads than do

similar-size stores in less affluent communities. To economists, this suggests that

premade salads are:

A. in excess demand.

B. overpriced.

C. inferior goods.

D. normal goods.

Answer:

All of the following are arguments in support of protectionist legislation except:

A. supporting infant industries.

B. preserving domestic employment.

C. increasing global trade.

D. promoting national security.

Answer:

In a perfectly competitive decreasing-cost industry:

A. factor prices do not change as industry output increases.

B. factor prices rise as industry output increases.

C. factor prices fall as industry output increases.

D. there is no way to predict what will happen to factor prices as industry output

increases.

Answer:

Behavioral economists want to:

A. eliminate the supply and demand model.

B. eliminate heuristic models.

C. eliminate traditional economic building blocks.

D. maintain supply and demand models.

Answer:

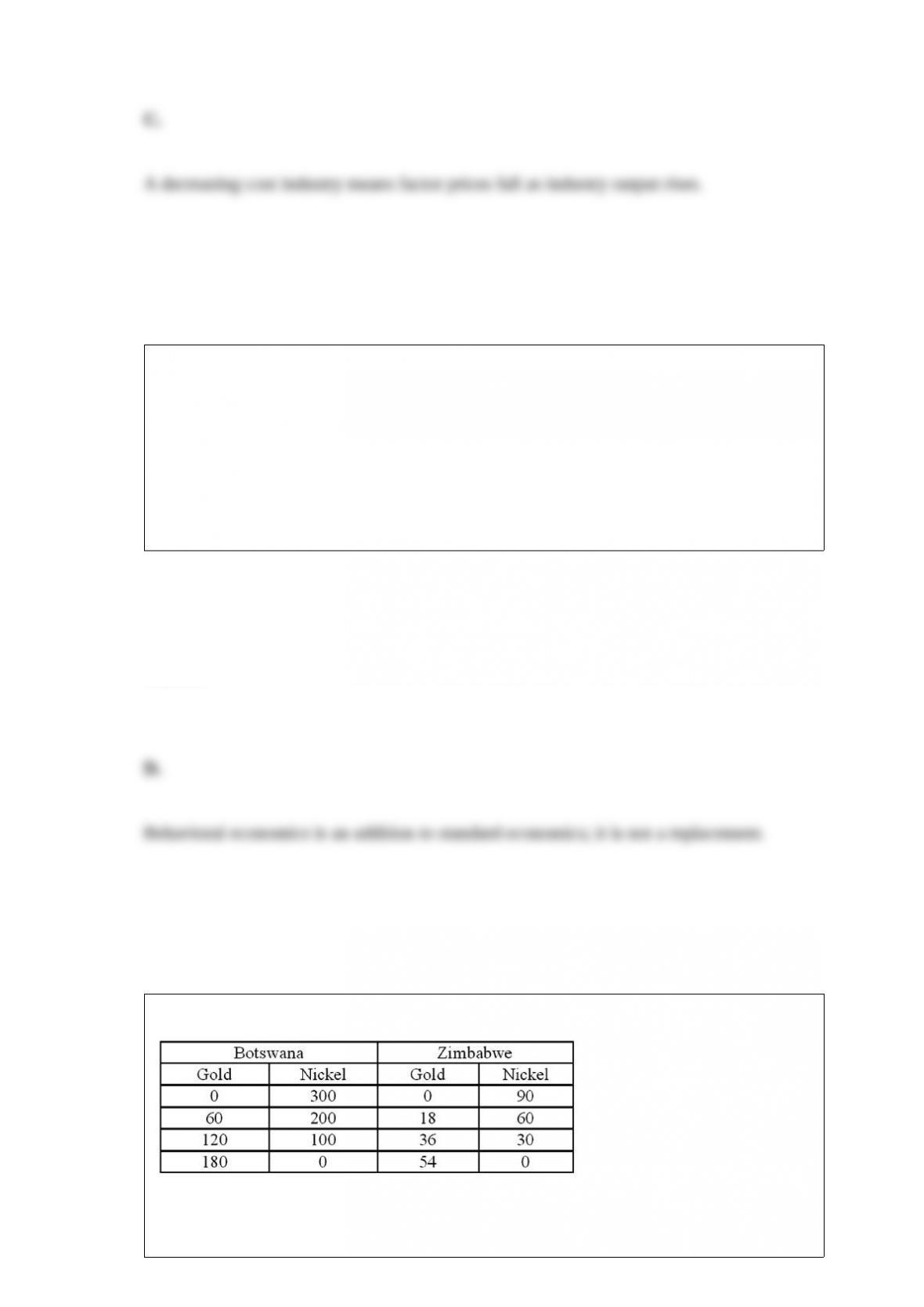

Refer to the table shown. In this example:

A. there are gains from trade for Botswana.

B. there are gains from trade for Zimbabwe.

C. there are gains from trade for both countries.

D. there are no possible gains from trade.

Answer:

State and local governments do not receive income directly from which source?

A. Property taxes

B. Sales taxes

C. Social security taxes

D. Local income taxes

Answer:

The theory of bounded rationality based on rules of thumb such as “the value of a

product is indicated by its price” may result in:

A. diminishing marginal utility.

B. constant marginal utility.

C. an upward-sloping demand curve.

D. an upward-sloping supply curve.

Answer:

When a monopolistically competitive industry is in long-run equilibrium:

A. firms earn economic profits.

B. firms earn zero economic profits.

C. price equals minimum average total cost.

D. price equals marginal cost.

Answer:

Relative to corporations, sole proprietorships are:

A. more numerous and smaller in size.

B. less numerous and smaller in size.

C. more numerous and larger in size.

D. less numerous and larger in size.

Answer:

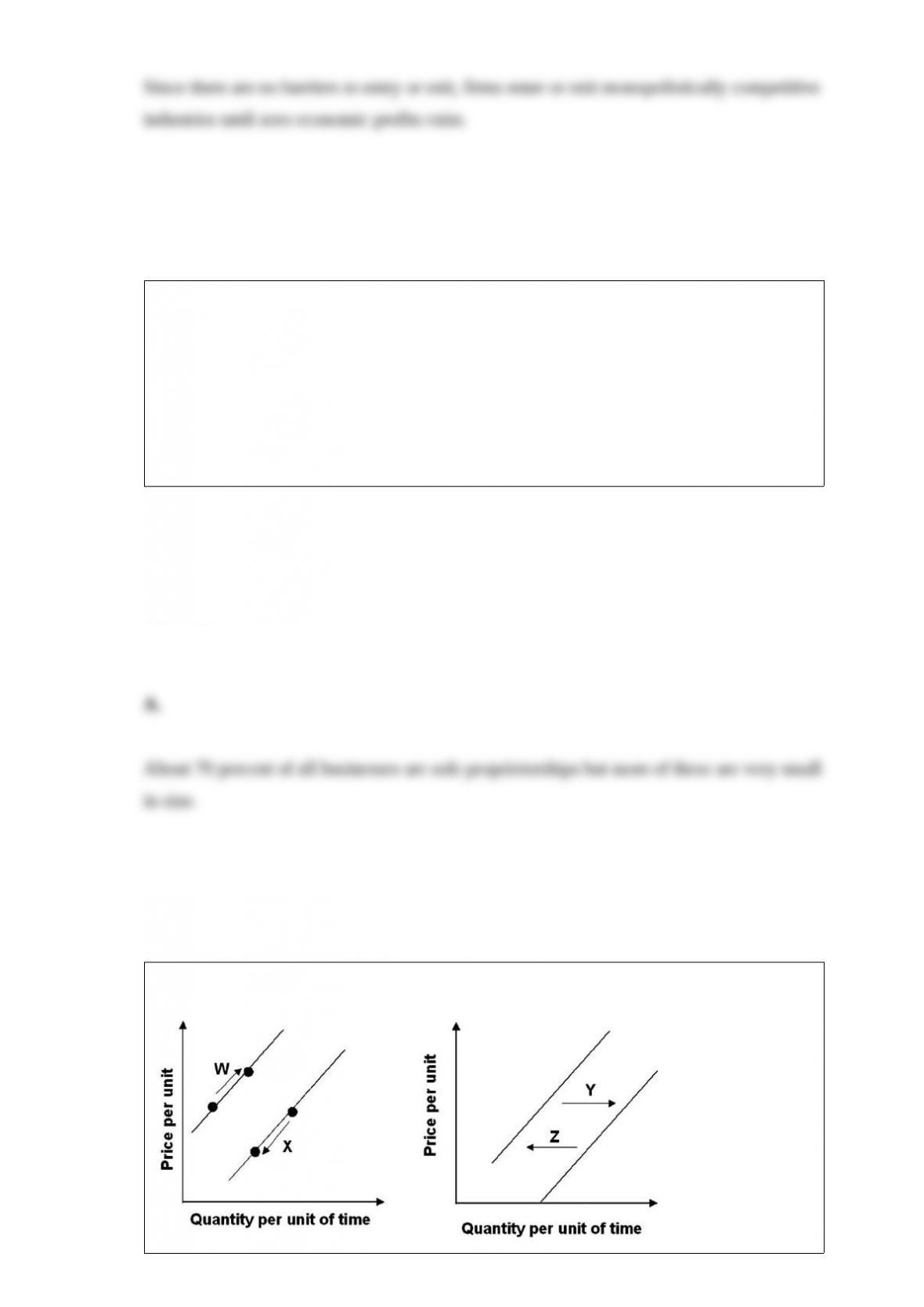

Refer to the graphs shown. The arrow that best shows an increase in supply is:

A. W

B. X

C. Y

D. Z

Answer:

If macaroni and cheese is an inferior good, falling incomes will tend to:

A. put upward pressure on its price and quantity.

B. put downward pressure on its price and quantity.

C. raise its price but lower its quantity.

D. lower its price but raise its quantity.

Answer:

Antitrust laws are an example of:

A. social forces.

B. political forces.

C. economic forces.

D. the invisible hand.

Answer:

The text attributes the growth of economies over the last 200 years largely to:

A. the development of markets.

B. the discovery of additional resources.

C. a decrease in the size of the world population.

D. laissez-faire policies.

Answer:

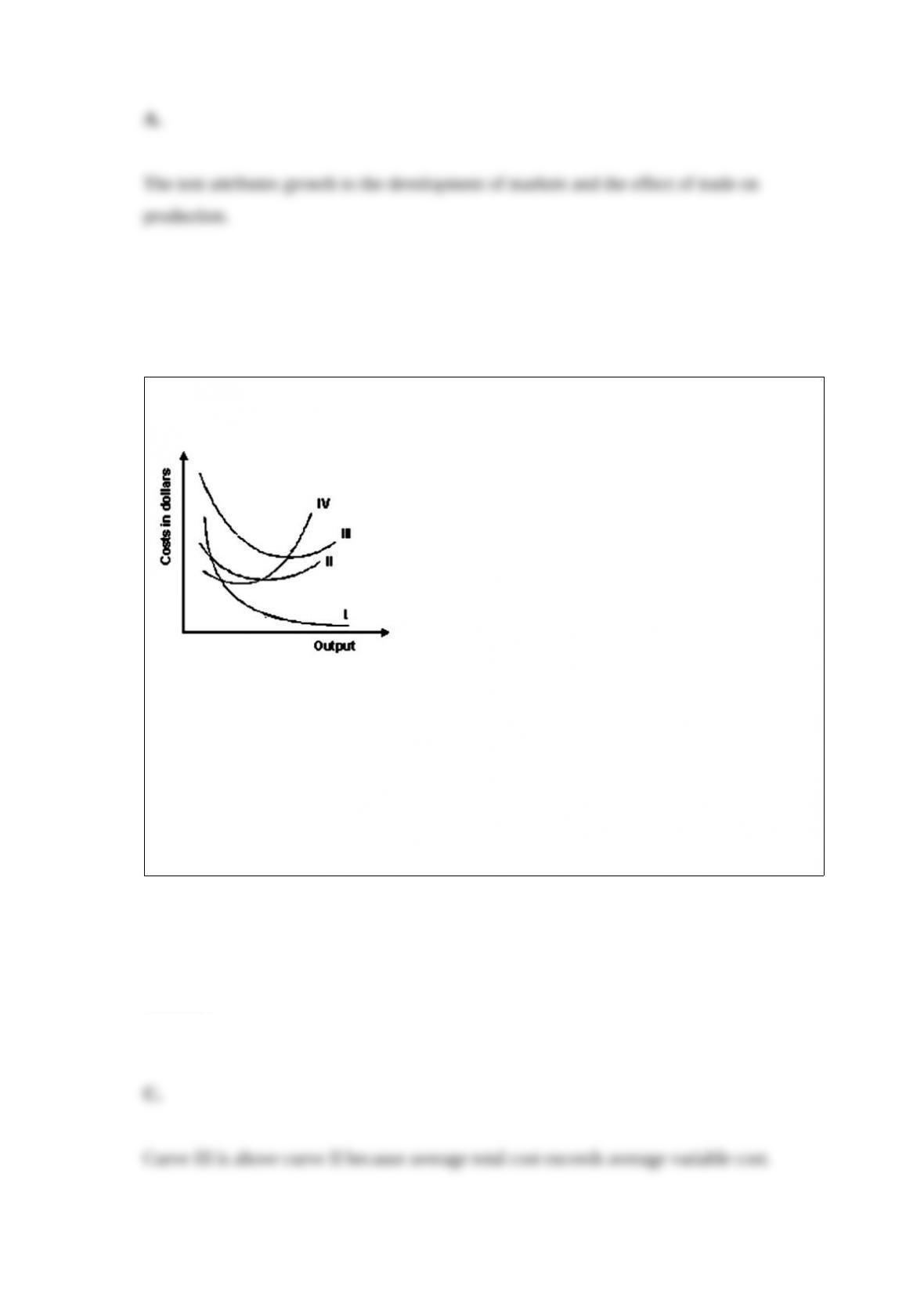

The following graph shows average fixed costs, average variable costs, average total

costs, and marginal costs of production.

Refer to the graph shown. The average total cost curve is represented by which curve?

A. I

B. II

C. III

D. IV

Answer:

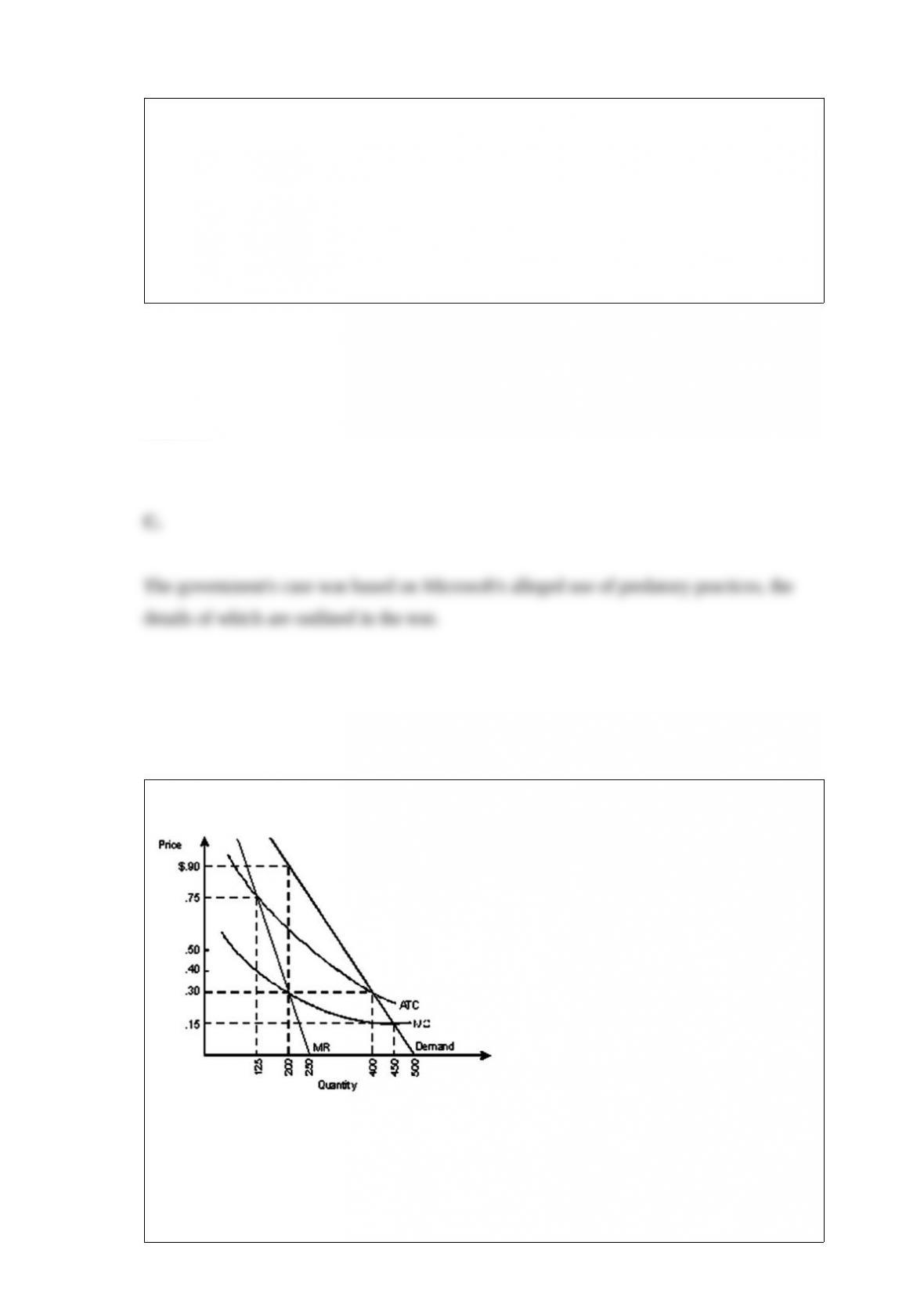

The government’s antitrust suit against Microsoft charged Microsoft with:

A. using price discrimination to earn higher profits.

B. being a monopoly, although there was no evidence of unfair business practices.

C. being a monopoly and using that monopoly power in a predatory way.

D. bribing government officials to drop the antitrust lawsuit.

Answer:

Refer to the graph shown. If this monopolist were forced to set price equal to marginal

cost, in the long run it probably would produce:

A. 0 units of output.

B. 200 units of output.

C. 400 units of output.

D. 450 units of output.

Answer:

The idea that people should be free to make their own decisions belongs to the ___

philosophy.

A. communist

B. libertarian

C. fascist

D. traditional

Answer:

The cost of dispensing fluoxetine (the generic for Prozac) is about $5 to $10 per

prescription, but the consumer’s price at most pharmacies is about $85. This suggests

that the market for prescription drugs is:

A. perfectly competitive.

B. a pure monopoly.

C. something that cannot be explained by economic theory.

D. not very competitive.

Answer:

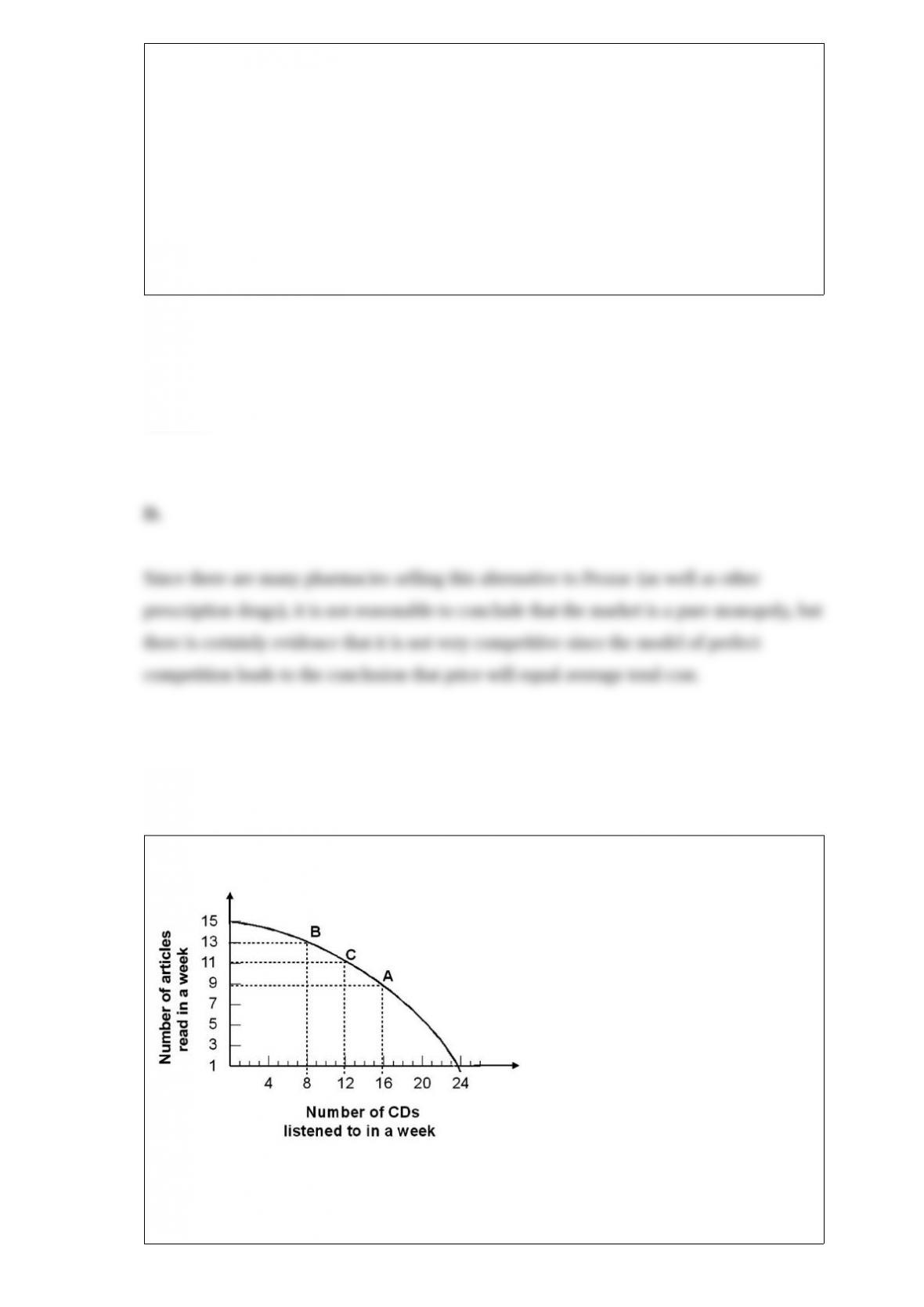

Given the production possibility curve shown, the opportunity cost of listening to each

additional CD when moving from point B to point A is on average:

A. ½ article.

B. 1 article.

C. 2 articles.

D. 3 articles.

Answer:

The antitrust case against AT&T was settled when:

A. AT&T was broken up into “Baby Bells” and the parent company.

B. AT&T filed for bankruptcy.

C. AT&T agreed to subject itself to more regulation.

D. the Department of Justice dropped the case.

Answer: