The infant industry argument is valid if the present value of the stream of national

benefits is less than the present value of the stream of national costs.

Answer:

Banks open branches in countries where profits are taxed less and their books of

accounts are less scrutinized.

Answer:

A foreign resident increasing her holdings of a U.S. financial asset will be recorded as a

debit item in the financial account of the U.S. balance of payments.

Answer:

A tax imposed on the exports of a small country usually drives down the domestic price

of the exportable good.

Answer:

Greece was among the 11 EU countries deemed to meet the five criteria in early 1998.

Answer:

A large enough production subsidy can turn an imported-product into an exportable

product.

Answer:

A tariff always lowers the well-being of each nation, including the nation imposing the

tariff.

Answer:

The greater the degree of international capital mobility:

a. the further to the right is the FE curve.

b. the further to the left is the FE curve.

c. the steeper is the FE curve.

d. the flatter is the FE curve.

Answer:

Harry used work in a launderette and earned $30 a day. After work, he normally had a

chicken burger worth $5 at McDonalds. However, his pay was lowered to $20 some

days later. Then after work he used to have a vegetable burger worth $3. Here the

vegetable burger is an example of a(n):

a. inferior good.

b. normal good.

c. complement good.

d. luxury good.

Answer:

Which of the following refers to trade diversion?

a. The volume of trade that is redirected from low-cost exporters to higher cost

domestic firms when the domestic government imposes import restrictions

b. The volume of trade that is redirected from low-cost exporters to higher-cost trade

bloc member countries

c. The amount of the imported goods that is substituted with domestically produced

goods

d. The change in the trade pattern such that the good which was formerly imported is

now exported as the government subsidizes its production

Answer:

As the value of the yen falls relative to the U.S. dollar in the foreign exchange market:

a. Japanese goods become more expensive to the U.S. consumers.

b. the supply of dollars will fall.

c. the demand for Japanese goods will increase in the U.S. market

d. U.S. goods become less expensive to Japanese consumers.

Answer:

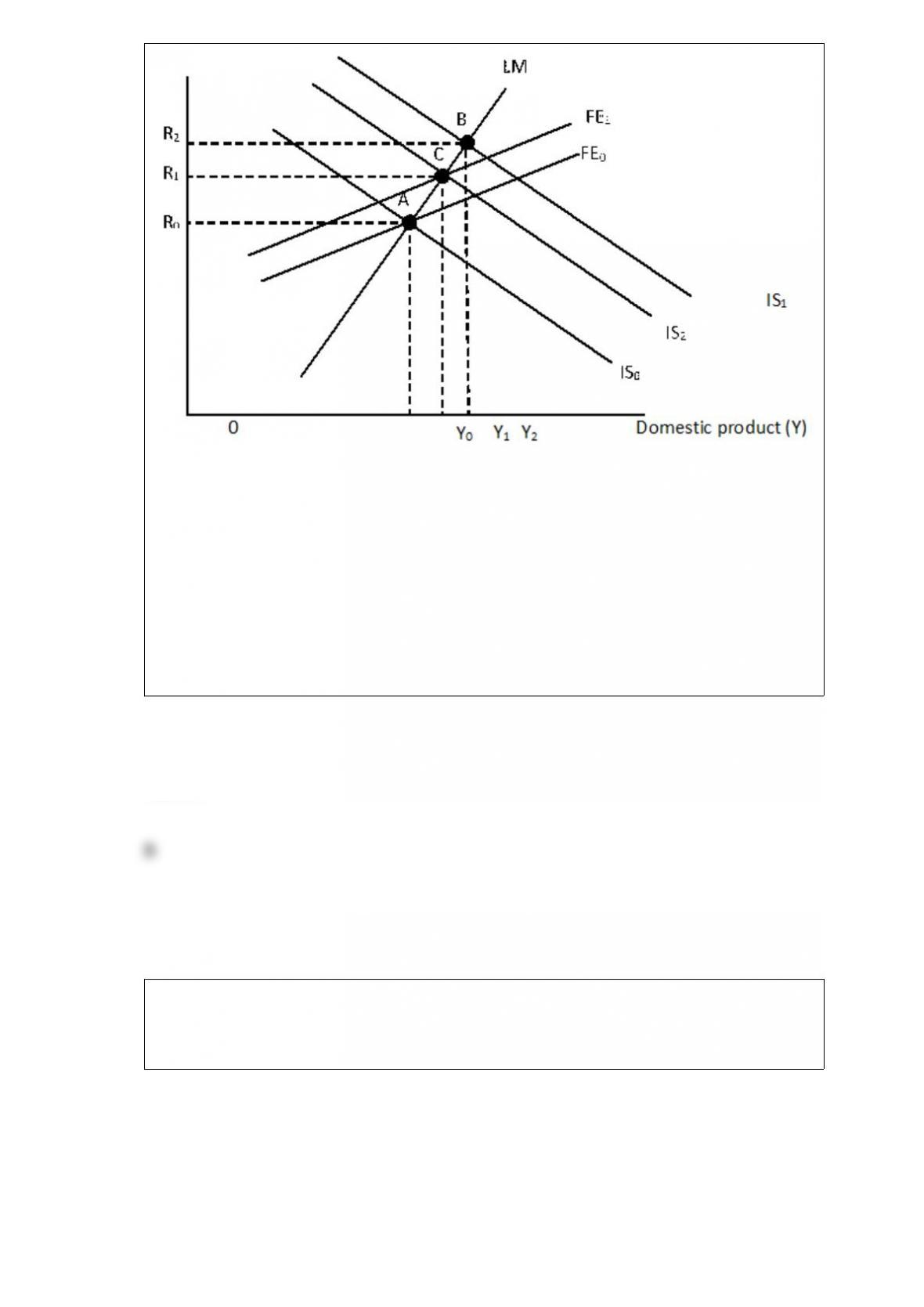

The figure given below depicts the IS-LM-FE model with floating exchange rates.

The move from point A to point B is caused by:

a. expansionary monetary policy.

b. expansionary fiscal policy.

c. contractionary monetary policy.

d. contractionary fiscal policy.

Answer:

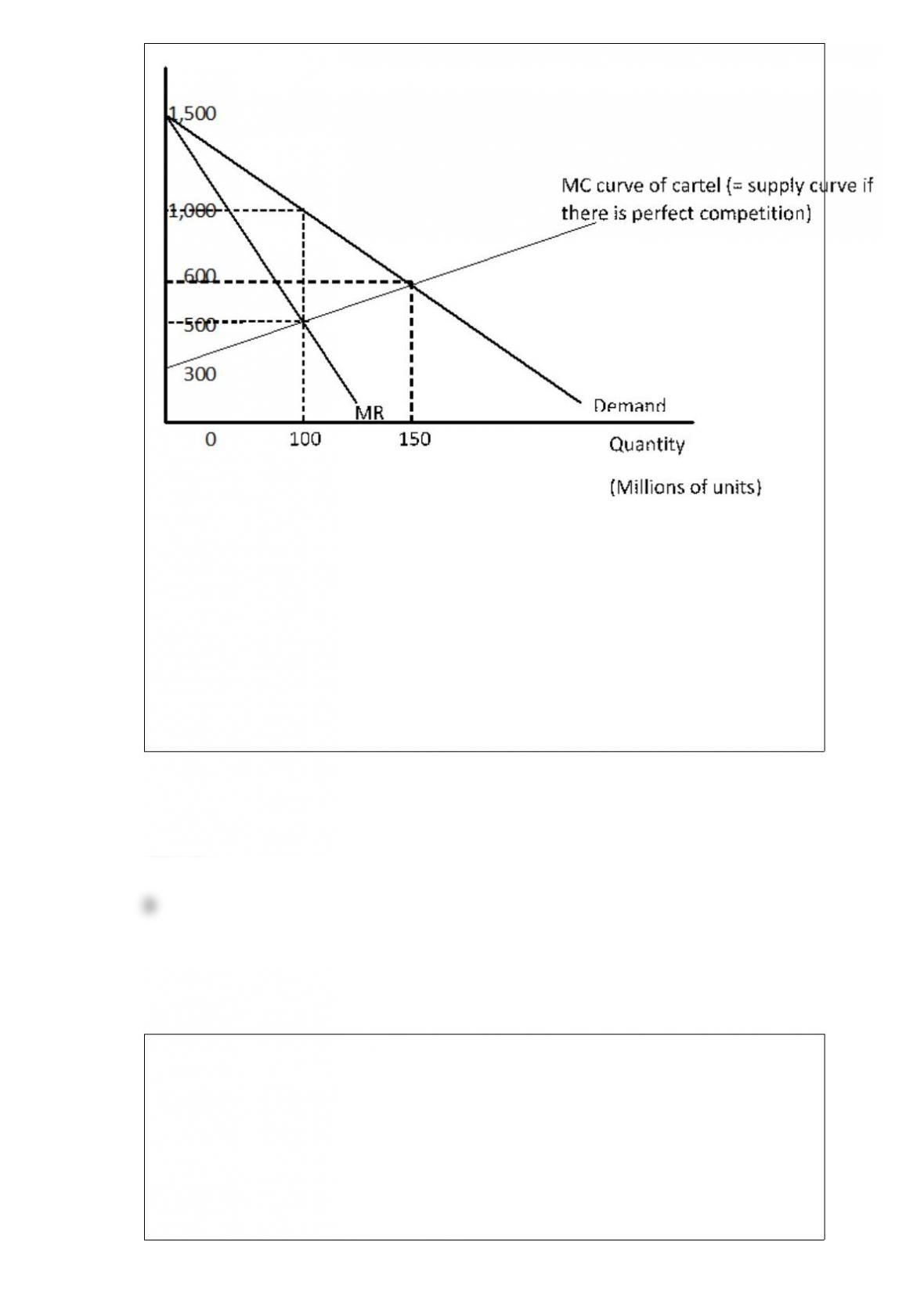

The figure given below shows a situation where the producers of good X are forming an

international cartel. Here, MR = Marginal Revenue, MC = Marginal Cost, and P =

Price. The cartel use monopoly pricing for its output.

How much well-being would world lose as a result of the formation of the cartel?

a. $5.0 billion

b. $12.5 billion

c. $15.0 billion

d. $50.0 billion

Answer:

What is the proper characterization of the European Union (EU), and what is its

primary accomplishment?

a. The EU is a regional trade bloc which controls the money supply in each member

country.

b. The EU is a regional trade agreement that has eliminated most trade barriers between

member countries.

c. The EU is a trade treaty that provides a forum where member countries can resolve

their trade disputes.

d. The EU is a trading cooperative that protects member countries from unfair trade

tactics by non-member countries.

Answer:

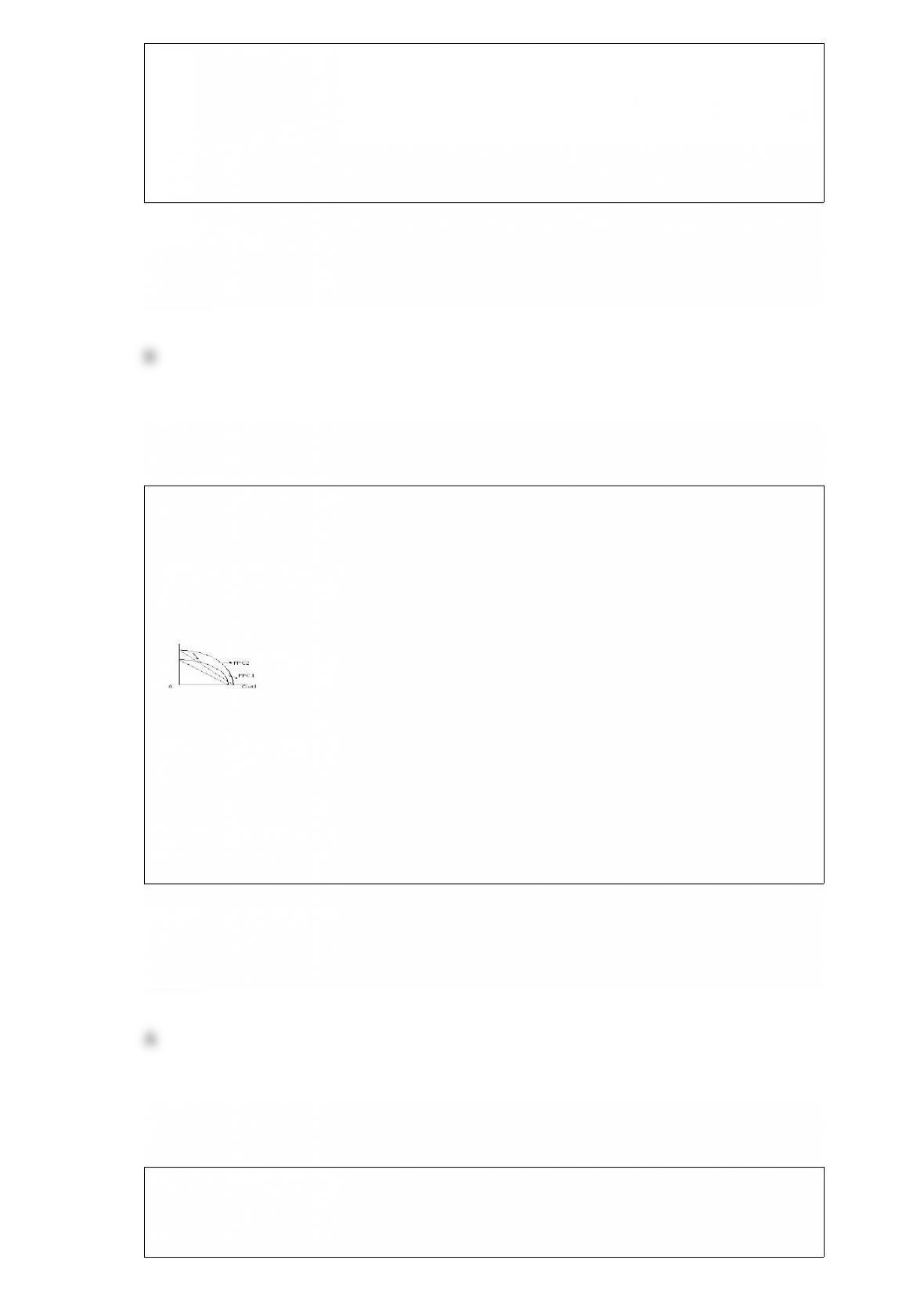

In the figure given below, we see an expansion of the production-possibility curve

(from PPC1 to PPC2). The two goods produced are wheat and cloth, which are

land-intensive and labor-intensive respectively. The outward shift of the

production-possibility curve shows:

Wheat

a. biased growth.

b. balanced growth.

c. a move from a no-trade situation to free trade.

d. a fall in production costs of both the goods.

Answer:

The existence of economies of scale suggests that:

a. FDI is a complement to exporting.

b. exporting can be preferable to FDI.

c. licensing local firms in the foreign market is preferable to exporting.

d. inherent disadvantages cannot be fully overcome.

Answer:

In November 2011, the interest rate on 10 year Spanish and Italian bonds were 4 to 5

percentage points higher than the interest rate on comparable German bonds. What did

that difference indicate?

a. German bonds were considered to be safer investments than Spanish or Italian bonds.

b. There was a higher demand for Spanish and Italian bonds than for German bonds.

c. The integration of the markets in EU countries promised by the introduction of the

euro worked.

d. The German economy was reducing the value of Spanish and Italian bonds.

Answer:

Which of following is most likely to happen when the dollar appreciates against the

euro?

a. There will be a huge inflow of ‘hot money’ to the European nations.

b. The prices of American goods in the European countries will decline.

c. The prices of European goods in the U.S. markets will decline.

d. The rate of inflation in the United States will increase.

Answer:

The _____ states that it is usually more efficient to use the government policy tool that

acts as directly as possible on the source of the distortion separating private and social

benefits or costs.

a. Pigou effect

b. spillover effect

c. sudden-damage effect

d. specificity rule

Answer:

How can one profit through arbitrage if the dollar per euro exchange rate in London is

$2 per pound while in New York is $1.95 per pound?

a. Buy dollars in New York and sell them in London

b. Buy pounds in London and sell them in New York

c. Buy pounds in New York and sell them in London

d. Buy dollars in London and sell pounds in New York

Answer:

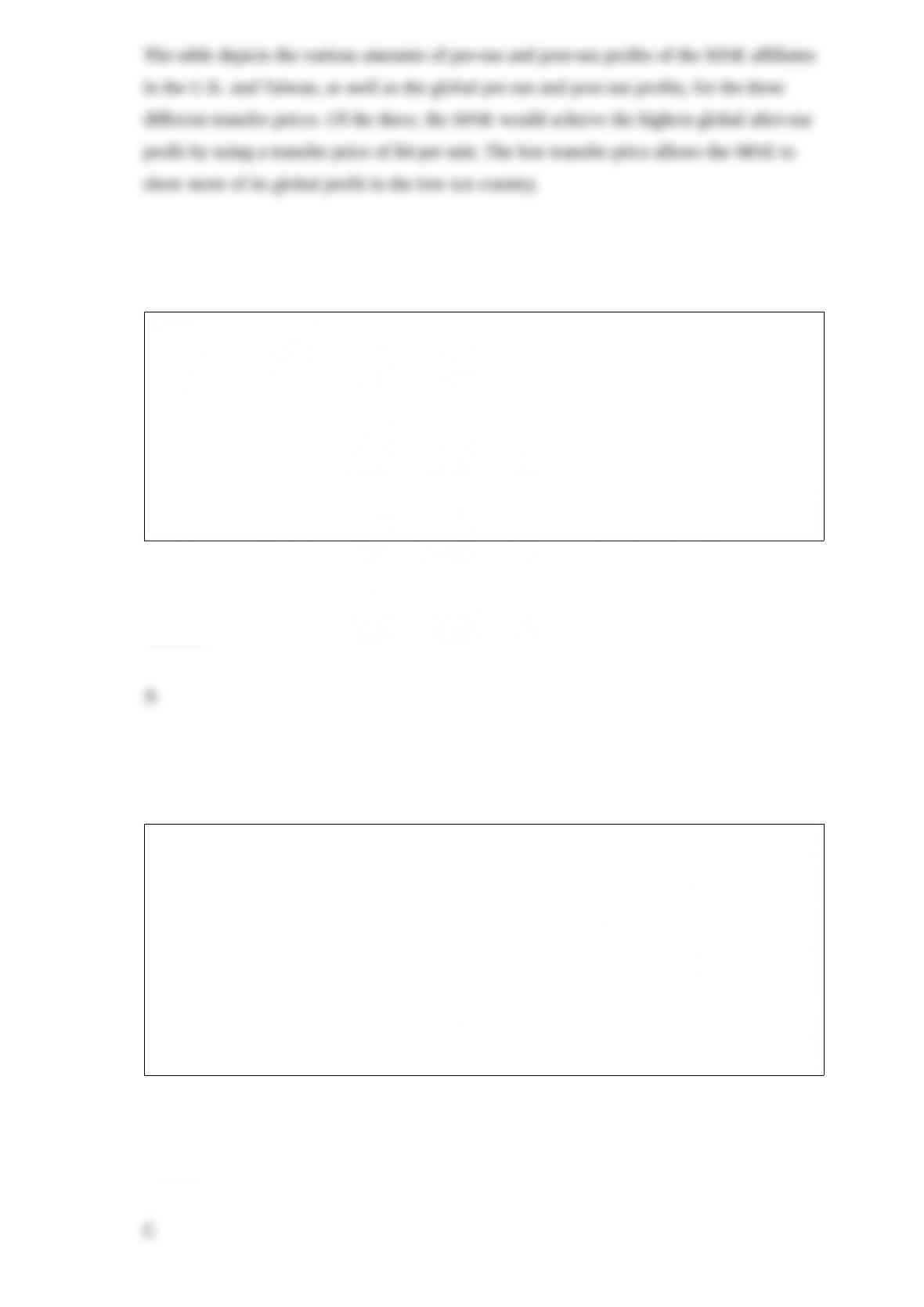

A multinational enterprise produces a component in the United Kingdom, where the

corporate income tax rate is 60 percent. It produces its final product in Taiwan, where

the corporate income tax rate is 25 percent. The cost of the component produced in the

United Kingdom is $4 per unit. The components can be shipped to Taiwan at almost no

cost, and there is no tariff on the component when it is imported into Taiwan. Each unit

of the final product requires one unit of the component. Other production costs in

Taiwan to complete the final product are $14 per unit. The final product price, when it

is sold by the Taiwan affiliate to outside buyers, is $20 per unit. If the goal of the

multinational enterprise is to maximize its global after tax profit, which of the following

three choices should the controller of the multinational enterprise favor? Why?

a. Charge a transfer price of $4 per unit

b. Charge a transfer price of $5 per unit

c. Charge a transfer price of $6 per unit

Answer:

A(n) _____ in a country’s money supply causes international capital _____.

a. expansion; outflows

b. expansion; inflows

c. contraction; outflows

d. contraction; stock to stabilize

Answer:

If trade is consistent with the H-O theory, then growth in a country’s scarce factor of

production will lead to:

a. an increased willingness to trade.

b. balanced growth.

c. a decreased willingness to trade.

d. a deterioration in the country’s terms of trade.

Answer:

Suppose manufacturing of paper results in substantial ground-water pollution. One

possible policy that can be used to fix this externality is:

a. to subsidize the production of paper by the domestic firms.

b. to impose tax on the production of paper.

c. to raise tariff barriers on paper imports.

d. to provide tax benefits to the firms exporting paper.

Answer:

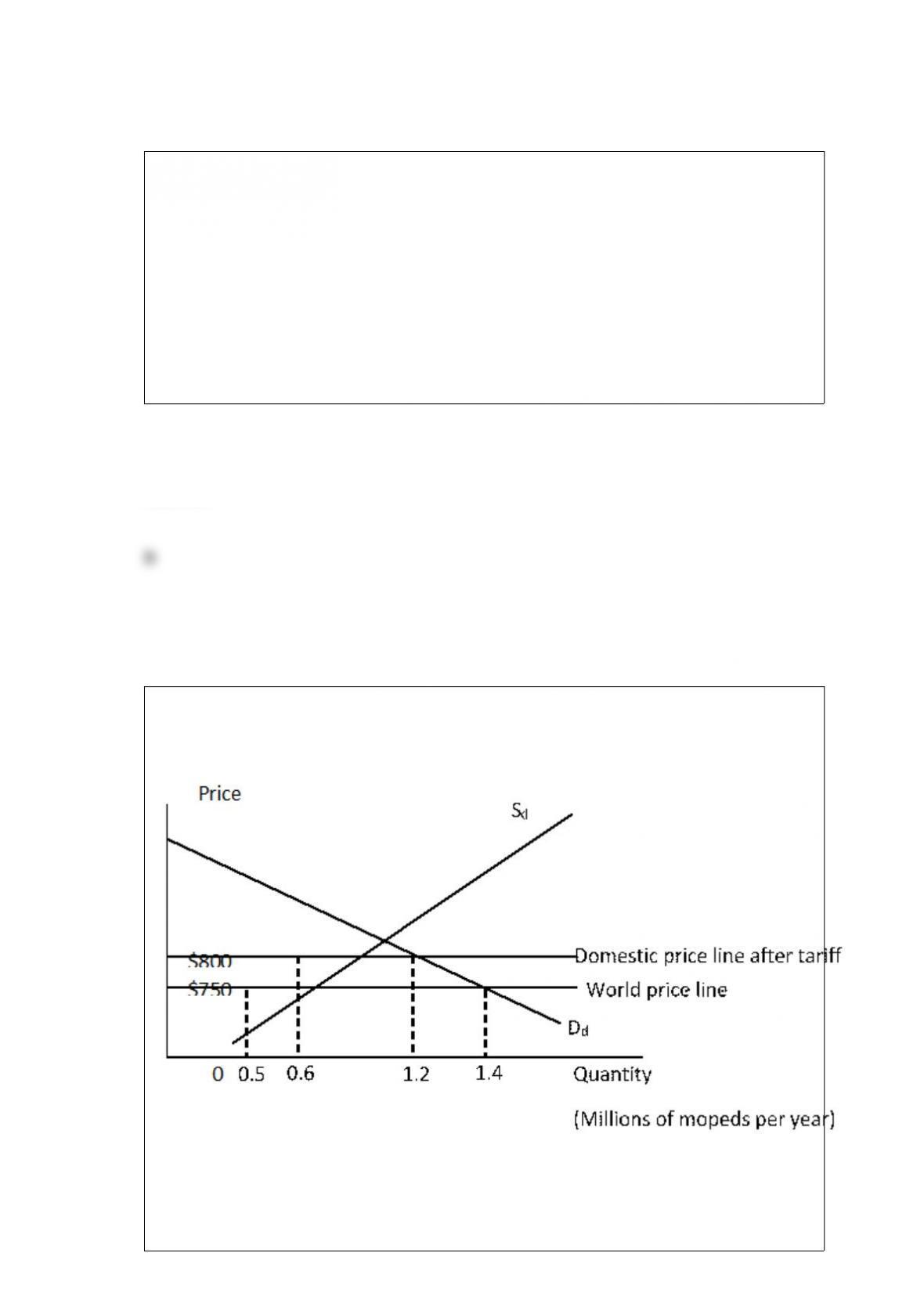

The figure given below shows the national market for mopeds in a country. Dd and Sd

are the domestic demand and supply curves of mopeds respectively.

Calculate the welfare loss arising from the production effect of the tariff.

a. $14 million

b. $2.5 million

c. $5 million

d. $7.5 million

Answer:

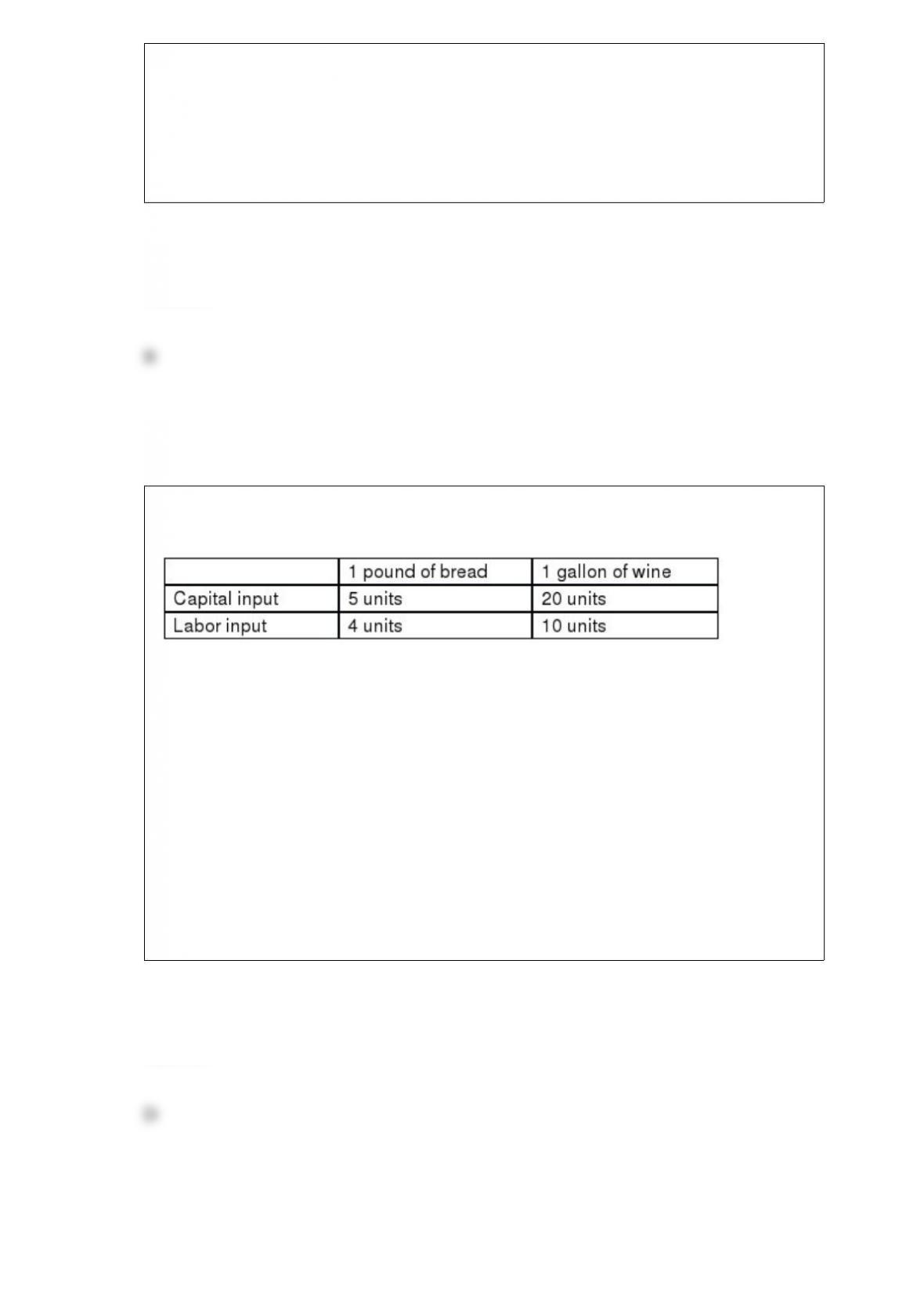

The following input-requirements data are for country A, a capital-abundant country

where they produce nothing but bread and wine using only capital and labor as inputs.

Which of the following can most reasonably be inferred for the short run after this

country opens to free trade?

a. The wage rates in all the sectors of the country will increase.

b. The rental rates of capital in all the sectors of the economy will decline.

c. The wage rates and the rental rates of capital will rise in the bread industry but will

fall in the wine industry.

d. The wage rates and the rental rates of capital will rise in the wine industry but will

fall in the bread industry.

Answer:

Which of the following refers to foreign exchange?

a. The act of trading different nations’ moneys

b. The holdings of foreign assets

c. The act of exchanging goods and services internationally.

d. The adoption of foreign trade policies

Answer:

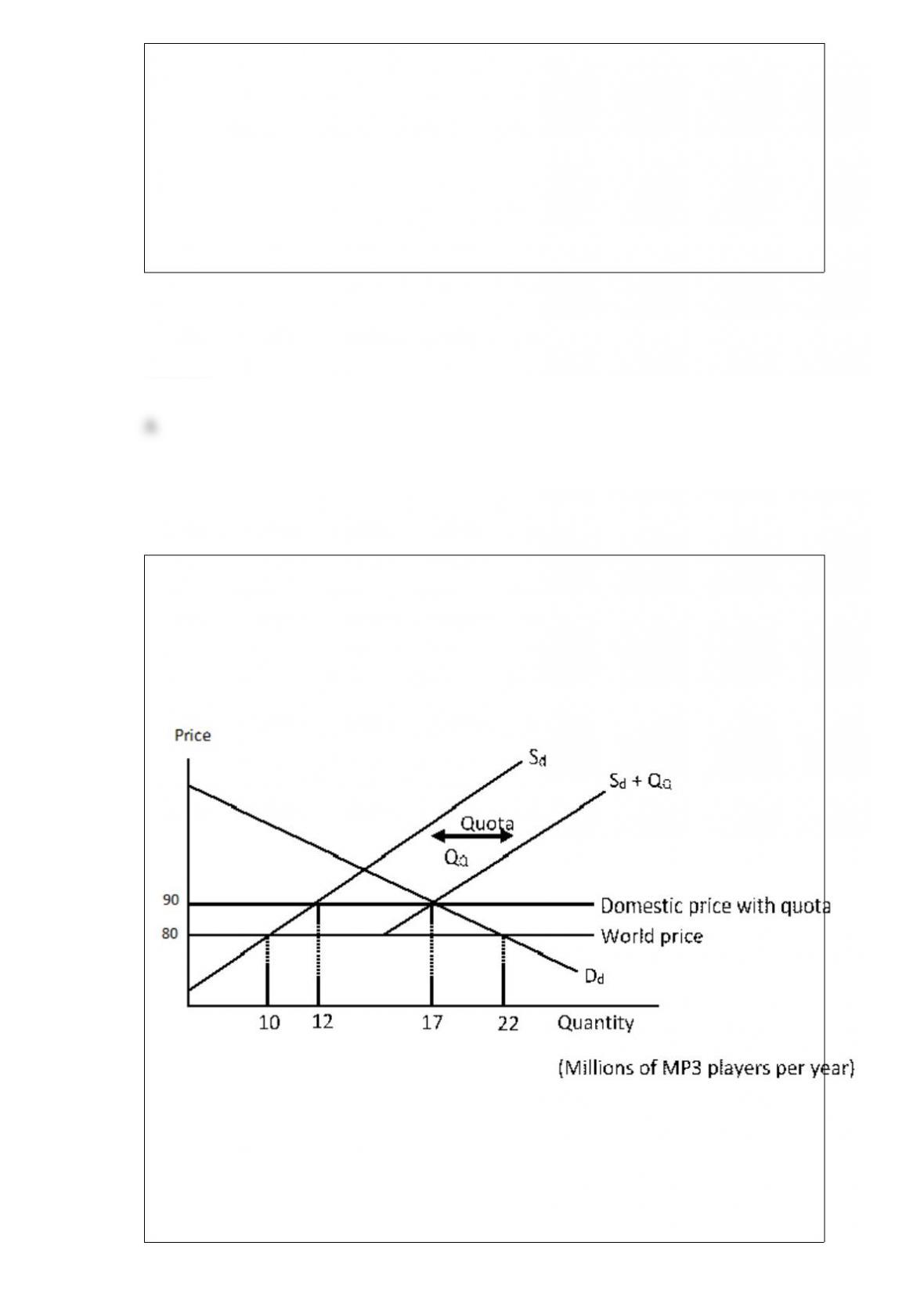

The figure given below shows the market for MP3 players in a small country. Dd and Sd

are the domestic demand and domestic supply curves of the MP3 players before the

imposition of the quota. (Sd + QQ) is the total available domestic supply curve after the

quota has been imposed. How many MP3 players can be imported from abroad after the

quota is imposed?

a. 2 million.

b. 5 million

c. 12 million

d. 17 million

Answer:

The figure given below shows the market for shoes in the U.S. The domestic price line

with tariff lies above the international price line. Dd and Sd are the domestic demand

and supply curves of shoes respectively.

Following the imposition of tariff, the domestic consumer surplus _____ by the area

_____.

a. increases; c + d

b. decreases; d

c. decreases; (a + b + c +d)

d. increases; (b + d)

Answer: