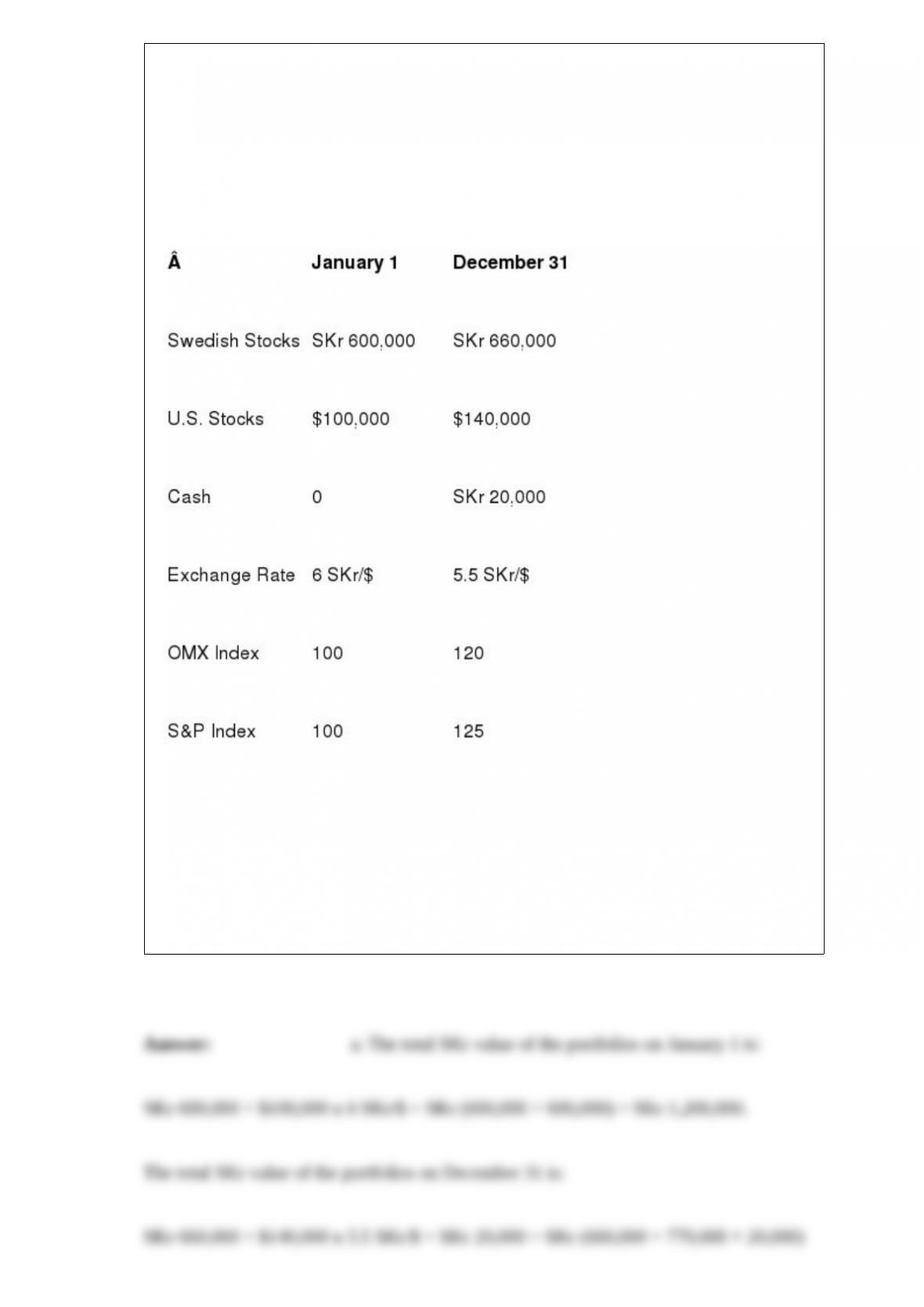

You are a Swedish investor owning a portfolio of Swedish and American stocks. Their

respective benchmarks are the OMX index and the S&P index. There have been no

movements during the year (cash flows, sales, or purchase). Dividends of SKr 20,000

have been paid on Swedish stocks. Valuation and performance analysis is done in

Swedish krona (SKr). Here are the valuations at the start and the end of the year:

a. What is the total value of the portfolio in SKr on January 1 and on December 31?

b. What is the total return on the portfolio?

c. Decompose this return into capital gain, yield, and currency contribution.

d. What is the contribution of security selection?

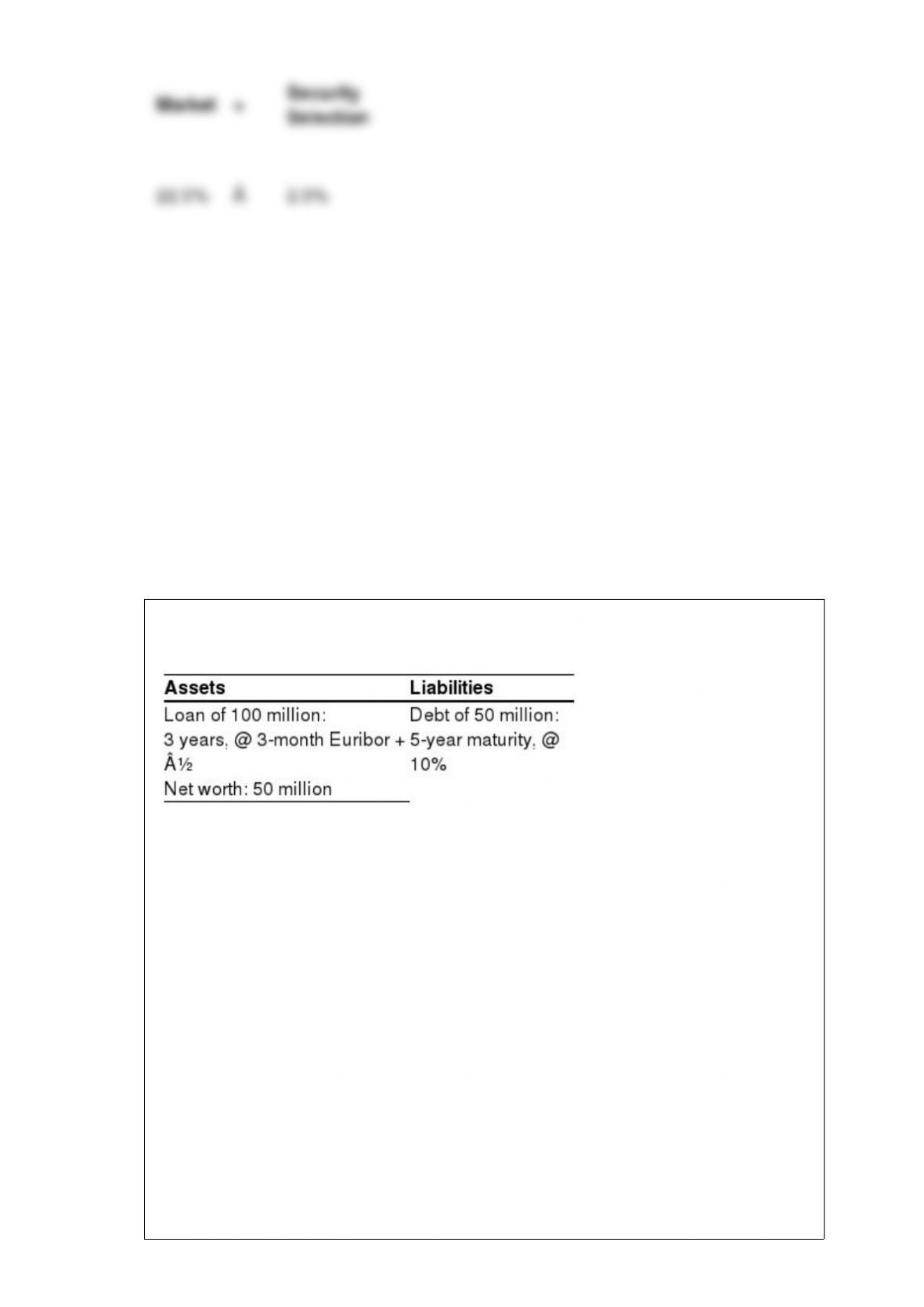

A small French bank has the following balance sheet, based on historical (nominal)

values.

All assets and liabilities are denominated in euros. The net worth is calculated as the

difference between the value of assets and liabilities. The current interest rate term

structure in euro is flat at 8%. The risk premium over Euribor required on the loan to a

client remains at 50 basis points.

a. Value the balance sheet based on market value.

b. The bank anticipates a sharp drop in French interest rates. Would this drop be good

for the bank?

The current market conditions for interest rate swaps with a maturity of three or five

years are 8% against Euribor.

c. Assume that the bank simply wishes to immunize its market value against any

movements in interest rates (drop or rise). What swap would you make to hedge this

interest rate risk?

d. Assume that the bank is quite confident in its interest rate prediction (a drop). What

would you suggest?

The next day, all interest rates drop to 7%.

e. Value the balance sheet again, assuming that the floating rate debt remains at 100%

and that the bank has undertaken the swap that you recommended. How much did the

bank save by undertaking this swap?

A zero-coupon bond with a five-year maturity is worth 68.06% of its final

reimbursement value.

a. Verify that its actuarial yield-to-maturity is equal to 8% by compounding 8% over

five years.

b. What is the simple yield of this bond, and why is it so different from the actuarial

yield?

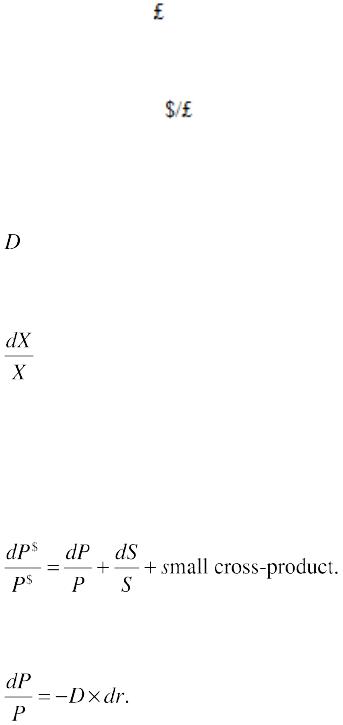

An American investor holds a British bond portfolio worth 100 million. The portfolio

has a duration of 7. She fears a temporary depreciation of the pound but wishes to retain

the bonds. To cover this risk, she decides to sell pounds forward. She has observed that

the British government tends to adopt a “leaning-against-the-wind” policy. When the

pound depreciates, British interest rates tend to rise to defend the currency. A regression

of “variations in long-term British yields” on “percentage exchange rate

movements” has a slope coefficient of -0.1. In other words, British yields tend to

go up by 10 basis points (0.1%) when the pound depreciates by 1% relative to the

dollar.

a. What should be the optimal hedge ratio used by the investor if she wishes to reduce

the uncertainty caused by exchange risk? (The investor uses only forward currency

contracts to hedge this risk, not bond futures contracts.)

b. Detail the factors that could make this hedge imperfect if the depreciation of the

pound materializes.

Fundamental Value Based on Absolute PPP. Ideally, one would like to compare

directly the price

of goods in two countries to see if an exchange rate conforms to absolute PPP, or

whether it is overvalued or undervalued in real terms. As mentioned in Chapter 2, this

can only be done for some individual goods that are clearly comparable (“law of one

price”), and the estimation for different goods can lead to opposing conclusions. In

Chapter 2, we provide an analysis based on the well-known Big Mac report of The

Economist. Of course, the Big Mac is a very particular product and a fundamental PPP

value can be computed on a wide range of products. The results are often conflicting.

For example, one can look at production prices rather than consumption prices. Some

studies are conducted by looking at labor costs. Rather than looking at unit labor costs

for unskilled workers, as is often done, the exhibit below reports the average annual

remuneration of the chief executive officer (CEO) of industrial companies with annual

revenues of 250 million to 500 million in ten selected areas of the world. The

figures are also from April 199 They include all forms of compensation, such as

bonuses, perks, and stock options, but are not adjusted for different taxes or costs of

living.

The first column gives the total CEO compensation measured in U.S. dollars using the

actual exchange rate, which is indicated in the second column. The third column gives

the fundamental PPP value of each currency, implied by the national CEO

compensations. It is the exchange rate with the dollar that would make CEO

compensation identical in all countries. The fourth column gives the actual

overvaluation (if positive) or undervaluation (if negative) of the local currency relative

to its fundamental value in terms of CEO compensation.

EXHIBIT: Determining a Fundamental PPP Value Based on CEOs€ Remuneration

Source:Total compensation data comes from Towers Perrin, 1998.

What conclusions can you draw from this exhibit?

A hedge fund currently has assets of $500 million. The annual fee structure of this fund

consists of a fixed fee of 1% of portfolio assets plus a 20% incentive fee. The fund

applies the incentive fee to the gross return each year in excess of the portfolio’s

previous high watermark, which is the maximum fund value in the past two years. The

fund is closed to new investors and the maximum value that the fund has achieved in

the past two years was $520 million. Compute the fee that the manager will earn, in

dollars, if the return on the fund in the coming year turns out to be:

a. 30%

b. 2%

c. -2%

A young investment banker considers issuing a DM/$ currency option bond for a AAA

client and wonders about its pricing. He knows that currency options are available on

the market and that they could help set the conditions on the bond issue. As a first step,

he decides to study a simple case: a one-year bond. The current market conditions are as

follows:

·One-year dollar interest rate: 10%.

·One-year Deutsche mark interest rate: 7%.

·Spot DM/$ exchange rate: $1 = DM 2.

The banker could issue a bond in dollars at 10%, a bond in DM at 7%, or a currency

option bond at an interest rate to be determined. One-year currency options are

negotiated on the over-the-counter market. A one-year currency option to exchange one

dollar for two Deutsche marks is quoted at 4%, that is, four cents per dollar. This is a

European option, which can be exercised only at maturity. The one-year forward

exchange rate is:

a. Given these data, what should the interest rate be on a one-year DM/$ bond?

b. How would you determine how to set the interest rate on an -year currency bond?

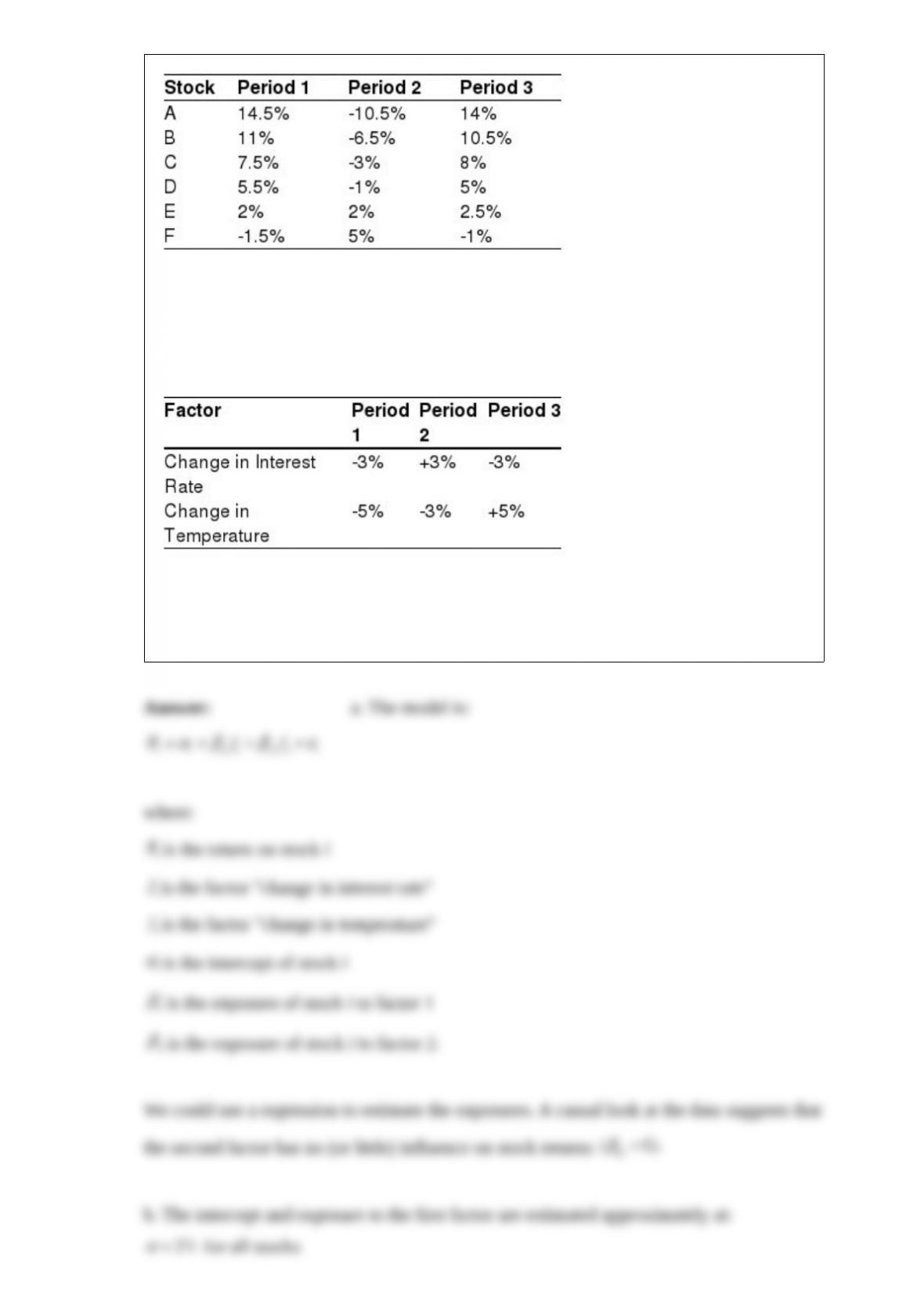

You invest in a country named Papaf. You observe the stock returns on a list of stocks

during

three periods.

You consider explaining differences in returns by common factors, with a linear model

as represented in Equation (6.9). You have two candidates for factors: movements in

interest rates and changes in the local temperature measured at noon-time from the

previous day. The various values of these factors are given below:

a. Try to assess whether each factor has an influence on stock returns.

b. Try to estimate the intercept and the factor exposures of each asset.

Strumpf Ltd. decides to issue a convertible bond with a maturity of two years. Each

bond is issued with a nominal value of 100 and an annual coupon C; of course, C has to

be determined. Each bond can be redeemed for 100 or converted into one share of

Strumpf at the option of the bondholder.

The current stock price of Strumpf is 90. The yield curve for an issuer like Strumpf is

flat at 6%. Barings is ready to issue long-term options on Strumpf shares. The

premiums on calls with one-year and two-year expirations are given below:

a. American-type calls are more expensive than European-type calls. Is it reasonable?

b. Assume that the bond can only be converted at maturity, after payment of the second

coupon. What should be the fair coupon rate C, consistent with the above market

conditions?

c. Assume that the bond is issued with the coupon rate determined above. The yield

curve suddenly moves from 6% to 6.1% and the option premiums stay the same. What

should be the new market price of the convertible bond?

d. Assume now that the bond can be converted on two dates (rather than one as above).

These dates are the first year (right after the first coupon payment) and the second year

as above. It is not possible to convert the two-year bond at any other date. Is it possible

to construct an arbitrage portfolio allowing to price the fair coupon C with the above

data? Be precise in your explanation and state what type of options you would need to

price the bond.

A company without default risk can issue a perpetual FRN at LIBOR. The coupon is

paid and reset semiannually. It is certain that the issuer will never have default risk and

will always be able to borrow at LIBOR. The FRN is issued on November 1, 2005,

when the six-month LIBOR is at 4.5%. On May 1, 2006, the six-month LIBOR is at

5%.

a. What is the coupon paid on May 1, 2006, per $1,000 bond?

b. What is the new value of the coupon set on the bond?

c. On May 2, 2006, the six-month LIBOR has dropped to 4.9%. What is the new value

of the FRN?

Bank PAPOUF decides to issue two bonds and wonders what the fair interest rate on

these bonds should be:

A. A one-year currency option bond. The bond is issued in dollars with a face value of

$100. The bondholder can choose to have the coupon and principal paid in dollars or in

SFr, at a specified exchange rate of SFr/$ = 2, that is, receive either $100 or SFr 200 as

principal repayment, and receive either $C or SFr 2C as interest if C is the coupon set in

dollars. The coupon rate is

c = C/100.

B. A two-year currency option bond. The bond is issued in dollars, with a face value of

$100 and pays an annual coupon C¢. The bondholder can choose to have the coupons

and principal paid in dollars or in SFr, at a specified exchange rate of SFr/$ = 2, that is,

receive either $100 or SFr 200 as principal repayment, and receive either $C’ or SFr

2C’ as interest, if C’ is the coupon set in dollars. The coupon rate is c’ = C’/100.

Current market conditions are given below:

· Interest Rates 1-Year 2-Year

Zero-coupon rates

US$ 8% 8%

SFr 4% 4%

· Spot exchange rate: SFr/$ = 2

· Currency options:

SFr call, strike price 50 U.S. cents, expiration one year: 2 U.S. cents.

SFr call, strike price 50 U.S. cents, expiration two years: 5 U.S. cents.

a. Compute the coupon C on Bond A that would be consistent with market conditions at

time of issue.

b. Compute the coupon C‘ on Bond B that would be consistent with market conditions

at time of issue.

Survivorship bias is a serious potential problem in drawing conclusions from historical

track records. Show why the following statements can be misleading:

a. “There are today 100 Type-A hedge funds in operation. Their average return over the

past two years is 20%. Hence, they have outperformed the stock market (return of

15%)” [actually, some 50 funds disappeared during these two years].

b. “The Poupou commodity index has been back-calculated from 1970 to 1990 using

the leading commodity futures contracts; by leading we mean those that have been most

active. The Poupou commodity index had a remarkable performance from 1970 to

1995″ [actually, several commodity futures contracts have been removed from the

commodity exchange or have experienced a drop in trading activity].

Titi, a Japanese company, issued a six-year Eurobond in dollars convertible to shares of

the Japanese company. At time of issue, the long-term bond yield on straight dollar

bonds was 10% for such an issuer. Instead, Titi issued bonds at 8%. Each $1,000 par

bond is convertible into 100 shares of Titi. At time of issue, the stock price of Titi is

1,600 yen and the exchange rate is 100 yen = 0.5 dollar

($/Y = 0.005).

a. Why can the bond be issued with a yield of only 8%?

b. What would happen if:

·The stock price of Titi increases?

·The yen appreciates?

·The market interest rate of dollar bonds drops?

c. A year later, the new market conditions are as follows:

·The yield on straight dollar bonds of similar quality has risen from 10% to 11%.

·Titi stock price has moved up to Y 2000.

·The exchange rate is $/Y = 0.006.

·What would be a minimum price for the Titi convertible bond?

d. Could you try to assess the theoretical value of this convertible bond as a package of

other securities such as a straight bond issued by Titi, options or warrants on the yen

value of Titi stock, an futures and options on the dollar/yen exchange rate?

The investment fund of Lemon County of California is investing $1 billion in a

leveraged-bond hedge fund. This hedge fund has the following structure:

· $4 billion invested in a reverse-floater (also called bull FRN). This is a five-year bond

with a coupon set at: 9% minus three-month LIBOR.

· $3 billion borrowed at: three-month LIBOR.

The current yield curve is flat at 4.5%. The reverse floater is currently priced at 100%.

a. Estimate the yield-enhancement over LIBOR that the hedge fund would provide if

the yield curve drops uniformly by 10 basis points (0.1%).

Actually, the whole yield curved moved up to 7% within a few days.

b. What would be the new income (coupon rate) on this $1 billion investment made by

Lemon County?

c. Can you provide some rough estimate of the new market value of this $1 billion

investment?

Assume that the domestic volatility (standard deviation in yen) of the Japanese stock

market is 18%. The volatility of the yen against the U.S. dollar is 6%.

a. What would the dollar volatility of the Japanese stock market be for a U.S. investor if

the correlation between the Japanese stock market returns and exchange rate

movements were zero?

b. Suppose the dollar volatility of the Japanese stock market is 18.4%, what can you

conclude about the correlation between the Japanese stock market movements and

exchange rate movements?

Your pension fund decides to invest in many national stock markets in a passive way.

The objective is to try to match the performance of the local market

capitalization-weighted index in each country. You do not buy national index funds but

invest directly in companies listed on each market. Because of the limited size of your

portfolios, you can buy only a few issues in each market. In which national markets are

you likely to track the index well or poorly?

The euro was introduced in 1999 as the common currency of eleven European countries

(Euroland). What should happen to the inflation rates of France, Germany, and Italy

after the introduction of the common currency?

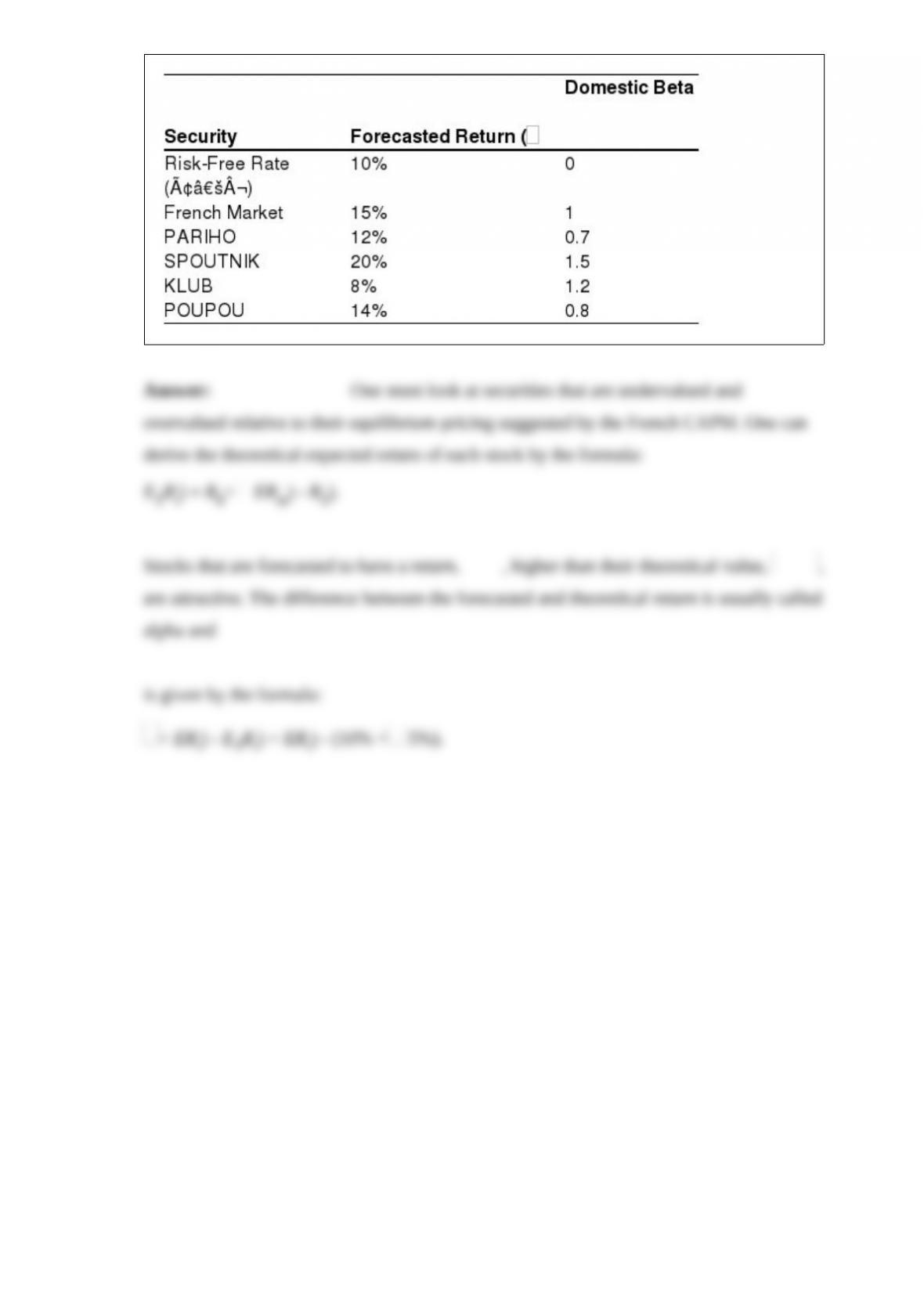

You are a money manager of French stocks. Your research department prepared the

table below. According to the domestic CAPM for French securities, which stocks

would you recommend for purchase and sale?

An Italian importer will be paid $1 million in three months (March). He must decide

whether to sell $1 million forward or to buy currency options for that amount.

The current market prices are as follows:

Exchange rates: Spot = 1.10

Three-month forward: = 1.11

Call euro March 110 U.S. cents: 1.5 U.S. cents per .

Put euro March 110 U.S. cents: 1.0 U.S. cents per .

What are the differences between the strategies of selling currency forward and buying

currency options?

The bid-ask rates are as follows:

Spot exchange rate:

CHF/USD: 1.5500-1.5540

Interest rates:

One-month CHF 31/2 – 5/8

One-year CHF 41/4 – 1/2

One-month USD 61/8 – 1/4

One-year USD 61/2 – 3/4

What are the quotations for the one-month and one-year CHF/USD forward exchange

rates?