1) Marginal resource cost is:

A.The increase in a firm’s total cost caused by hiring one additional unit of an input

B.A firm’s cost of hiring one group of inputs, such as capital or labor

C.The firm’s demand curve for a productive resource

D.Determined by the marginal physical product schedule for an input

2) In an oligopoly, producers’ agreements to restrict output tend to be unstable because

each firm has an incentive to:

A.Produce more than its output quota

B.Lower both its price and its output

C.Raise its price above the cooperative price

D.Establish competitive price and output levels

3) Which of the following increases in labor demand is due to a change in the price of a

related resource?

A.Software sales rise, thus increasing the demand for software developers

B.Snowboarding increases in popularity, thus increasing the demand for the workers

who make snowboards

C.A decrease in the price of wood decreases the cost of furniture, thus increasing the

demand for furniture workers

D.A technological change increases output per worker in the computer industry, thus

increasing the demand for computer workers

4) An increase in the demand for loanable funds may be caused by a(n):

A.Increase in the availability of loanable funds

B.Increase in consumers’ willingness to save

C.Increase in business borrowing

D.Decrease in the interest rate

5) The three types of farm subsidies under the Food, Conservation, and Energy Act of

2008 are:

A.Equipment coupons, land leases, and income contributions

B.Marketing agreements, transition payments, and interest loans

C.Direct payments, countercyclical payments, and marketing loans

D.Public land sales, fertilizer discounts, and farm bank loans

6) The law of diminishing marginal utility explains why:

A.supply curves slope upward.

B.demand curves slope downward.

C.addicts can never get enough.

D.people will only consume their favorite goods and not try new things.

7) Concentration ratios:

A.may overstate the degree of competition because they ignore imported products.

B.may overstate the degree of competition because interindustry competition is ignored.

C.may understate the degree of competition because they ignore imported products.

D.provide detailed insights as to the price and output behavior of firms that comprise

the various industries.

8) Trade adjustment assistance:

A.provides financial assistance to all unemployed workers in the United States.

B.guarantees jobs for all workers displaced by imports or plant relocations abroad.

C.provides assistance to about 20 percent of unemployed U.S. workers each year.

D.provides cash assistance for workers displaced by imports or plant relocations

abroad.

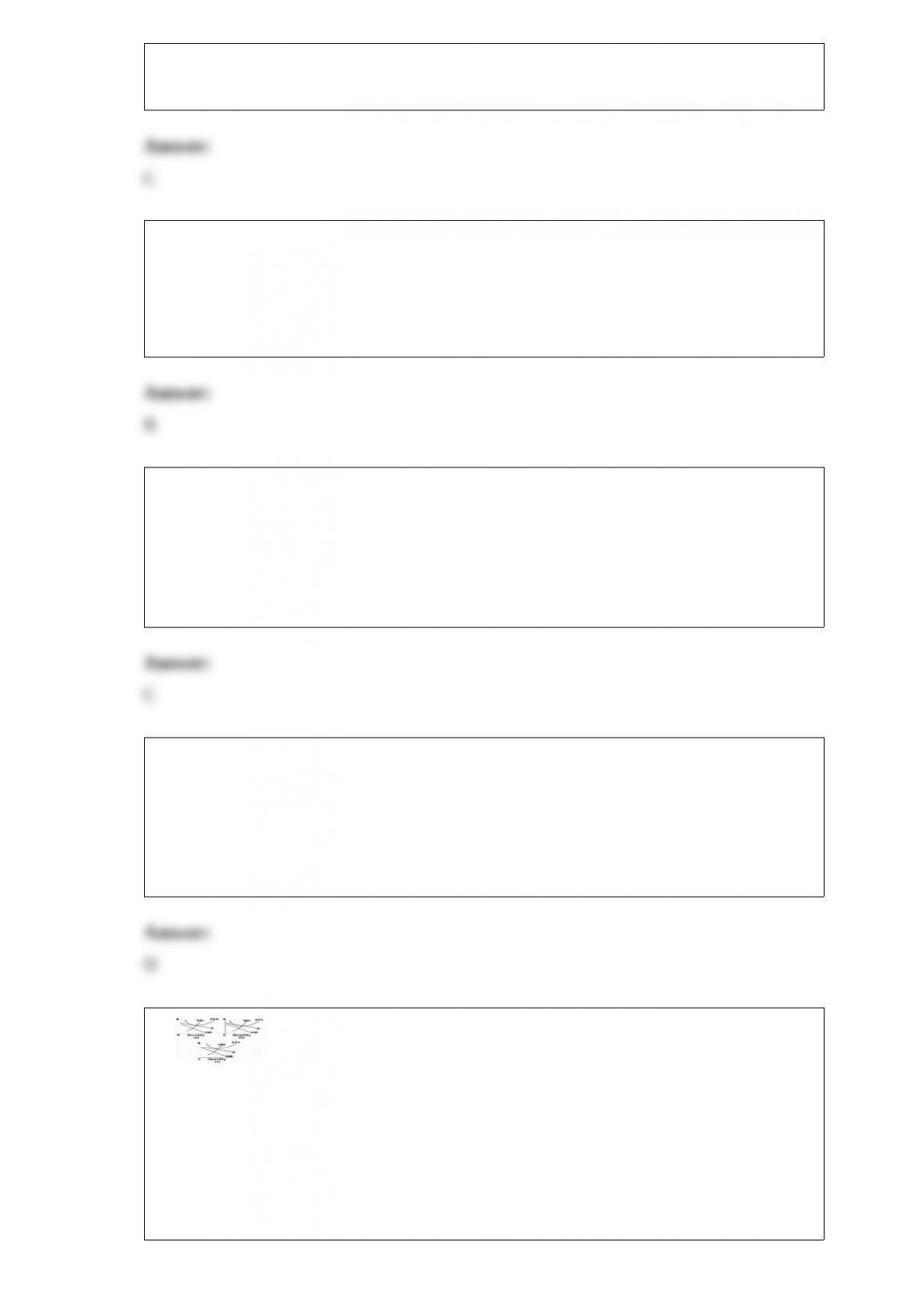

9)

Refer to the diagrams, which pertain to monopolistically competitive firms. Long-run

equilibrium is shown by:

A.diagram a only.

B.diagram b only.

C.diagram c only.

D.both diagrams b and c.

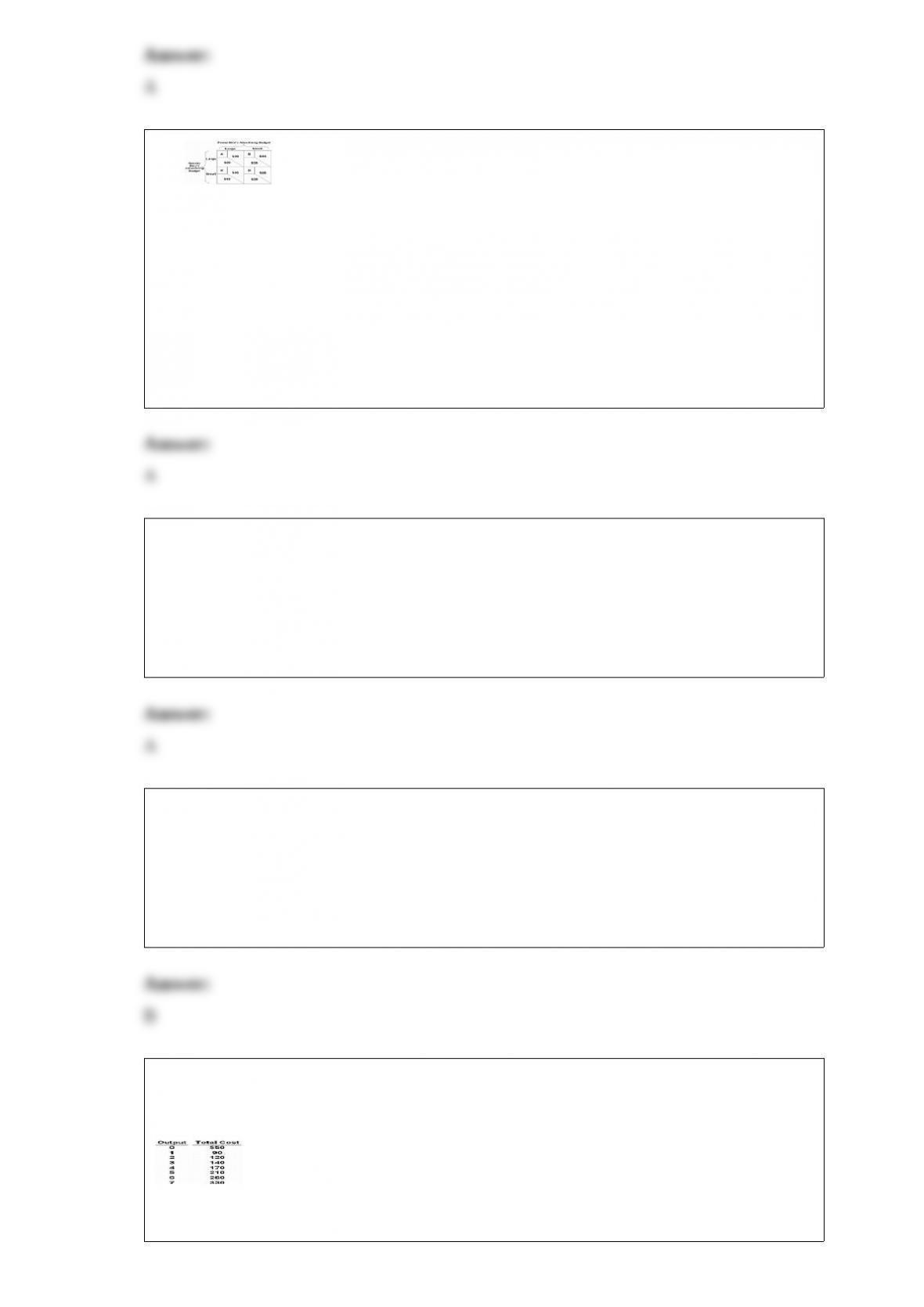

10)

Refer to the payoff matrix. Suppose that Speedy Bike and Power Bike are the only two

bicycle manufacturing firms serving the market. Both can choose large or small

advertising budgets. If this is a one-time, simultaneous game, which cell represents the

final outcome we would expect to occur?

A.A

B.B

C.C

D.D

11) In percentage terms, which of the following occupations is expected to be the fastest

growing from 2010 to 2020?

A.Personal care aides

B.Athletic trainers

C.Carpentry helpers

D.Convention and event planners

12) If the firms in an oligopolistic industry can establish an effective cartel, the

resulting output and price will approximate those of:

A.a purely competitive producer.

B.a pure monopoly.

C.a monopolistically competitive producer.

D.an industry with a low four-firm concentration ratio.

13) Answer the question on the basis of the following cost data for a purely competitive

seller:

Refer to the data. If product price is $60, the firm will:

A.shut down.

B.produce 4 units and realize a $120 economic profit.

C.produce 6 units and realize a $100 economic profit.

D.produce 3 units and incur a $40 loss.