1) The use of the coordinate system allows

a.for the display of the flows of dollars, goods and services, and factors of production in

an economic system.

b.for the display of how labor and other resources are organized in the production

process.

c.for the display of two variables on a single graph.

d.for the creation of pie charts and bar graphs.

2) Alan Greenspan, former Chairman of the Federal Reserve, discussed the advantages

of which kind of tax system, “particularly if one were designing a tax system from

scratch”?

a.a progressive tax system

b.a regressive tax system

c.a consumption tax

d.a lump-sum tax

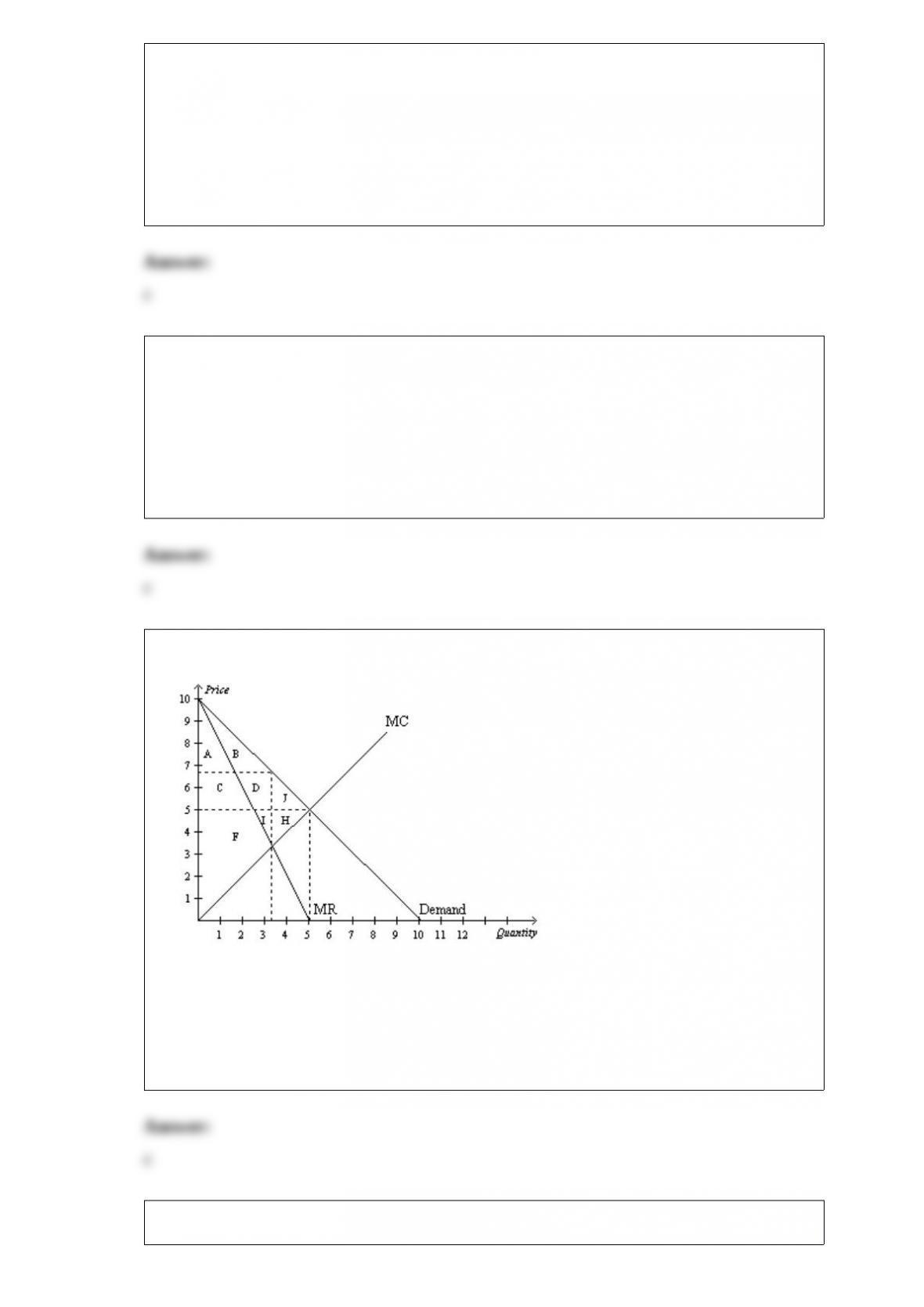

3) Figure 15-11

Which area represents the deadweight loss from monopoly?

a.A+B

b.C+F

c.G

d.A+B+C+F

4) If orange juice and apple juice are substitutes, an increase in the price of orange juice

will shift the demand curve for apple juice to the right.

a.True

b.False

5) If the selling price of a bushel of cranberries rises, we would expect the demand for

labor in the cranberry industry to

a.increase.

b.decrease.

c.be unchanged.

d.increase by less than the corresponding decrease in supply.

6) In 1913, the Ford Motor Company decided to pay its employees $5 a day. This wage

was significantly higher than what any other organization offered. Henry Ford believed

that this wage would make his employees happier, increase their productivity, and lower

employee turnover. Economists would say that Mr. Ford offered his employees

a.a union.

b.an efficiency wage.

c.a diminishing rate of marginal return.

d.a leisure wage.

7) The U.S. president who referred to inflation as public enemy number one was

a.Richard Nixon.

b.Gerald Ford.

c.Jimmy Carter.

d.Ronald Reagan.

8) Arturo’s Production Possibilities FrontierDina’s Production Possibilities

Frontier

15) If goods A and B are perfect substitutes, then the marginal rate of substitution of

good A for good B is constant.

a.True

b.False

16) Roger owns a small health store that sells vitamins in a perfectly competitive

market. If vitamins sell for $12 per bottle and the average total cost per bottle is $11.50

at the profit-maximizing output level, then in the long run

a.more firms will enter the market.

b.some firms will exit from the market.

c.the equilibrium price per bottle will rise

d.average total costs will rise.

17) When supply and demand both increase, equilibrium

a.price will increase.

b.price will decrease.

c.quantity may increase, decrease, or remain unchanged.

d.price may increase, decrease, or remain unchanged.