1) Economists generally agree that the most important tax in the U.S. economy is the

a.investment tax.

b.sales tax.

c.property tax.

d.labor tax.

2) Suppose a profit-maximizing firm in a competitive market produces rubber bands.

When the market price for rubber bands falls below the minimum of its average total

cost, but still lies above the minimum of average variable cost, in the short run the firm

will

a.experience losses but will continue to produce rubber bands.

b.shut down.

c.earn both economic and accounting profits.

d.raise the price of its product.

3) The federal government sets the poverty line at roughly

a.five times the cost of providing an adequate diet.

b.four times the cost of providing an adequate diet.

c.three times the cost of providing an adequate diet.

d.two times the cost of providing an adequate diet.

4) After initial success, the OPEC cartel saw the price of oil and the revenues of its

members decline due, in part, to

a.the low elasticity of demand for oil in the short run.

b.the large number of buyers from each member nation.

c.surging demand for oil in the early 1980s.

d.OPEC members failing to produce their agreed-upon production levels.

5) If you are assigned the role of Player A in the Ultimatum game and you propose that

player B gets $1 and you get $99

a.you are behaving as a rational wealth-maximizer and player B is likely to accept your

offer.

b.you are behaving as a rational wealth-maximizer and player B is likely to reject your

offer.

c.you are not behaving as a rational wealth-maximizer and player B is likely to accept

your offer.

d.you are not behaving as a rational wealth-maximizer and player B is likely to reject

your offer.

6) Scenario 12-3

Suppose Roger and Regina receive great satisfaction from their consumption of

cheesecake. Regina would be willing to purchase only one slice and would pay up to $8

for it. Roger would be willing to pay $11 for his first slice,$9 for his second slice, and

$5 for his third slice. The current market price is $5 per slice. Assume that the

government places a $4 tax on each slice of cheesecake and that the new equilibrium

price is $9. What is the deadweight loss of the tax?

a.$3

b.$6

c.$8

d.$9

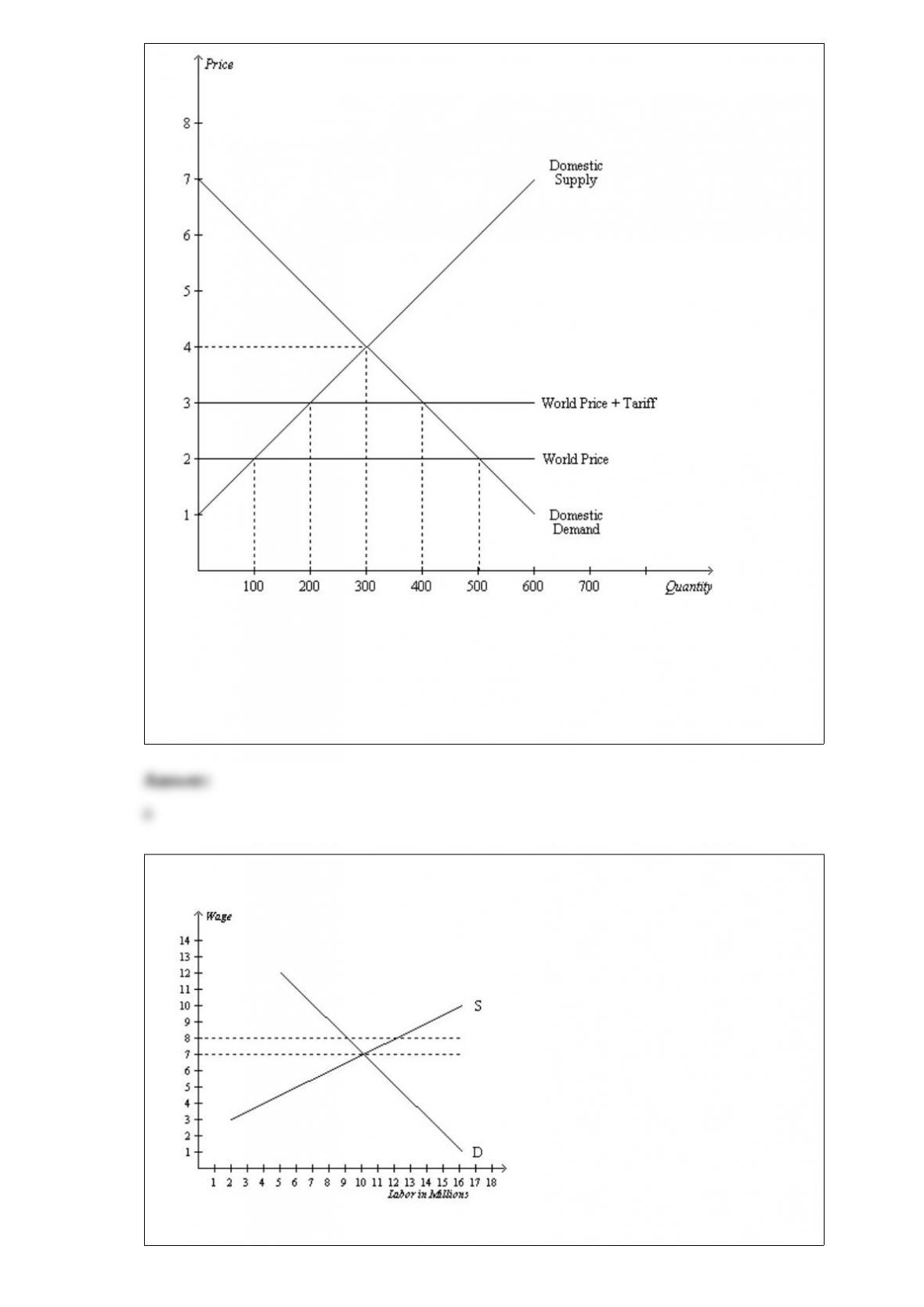

7) Figure 9-6

The figure illustrates the market for roses in a country.

With trade

and without a tariff,

a.the domestic price is equal to the world price.

b.roses are sold at $4 in this market.

c.there is a shortage of 400 roses in this market.

d.this country imports 200 roses.

8) Figure 19-1

Refer to Figure 19-1. Suppose the local labor market was in equilibrium to begin with

but then the largest local employer decided to change its compensation scheme to $8 as

shown. Which of the following compensation schemes could the graph be illustrating?

a.An efficiency wage.

b.Discrimination.

c.A compensating differential.

d.The superstar phenomenon.

9) Suppose that a large rogue wave destroys the (thankfully unoccupied) fleet of

swordfish fishing boats docked in the Gloucester, Massachusetts harbor. What happens

to the earnings of fishermen and women in Gloucester?

a.The reduction in the supply of fishing boats increases the marginal productivities of

Gloucester fishermen and women, which causes the equilibrium wage to fall.

b.The reduction in the supply of fishing boats reduces the marginal productivities of

Gloucester fishermen and women, which causes the equilibrium wage to fall.

c.The reduction in the supply of fishing boats increases the marginal productivities of

Gloucester fishermen and women, which causes the equilibrium wage to rise.

d.The reduction in the supply of fishing boats reduces the marginal productivities of

Gloucester fishermen and women, which causes the equilibrium wage to rise.

10) The tradeoff between inflation and unemployment

a.implies that policies designed to reduce unemployment also reduce inflation.

b.was eliminated by improved economic policies in the 1900s.

c.is a long-run tradeoff, persisting for decades, according to most economists.

d.None of the above are correct.