16

3. Why might the RJR Nabisco board have accepted the KKR bid over the Johnson bid?

4. How might bondholders and preferred stockholders have been hurt in the RJR Nabisco leveraged buyout?

5. Describe the potential benefits and costs of LBOs to shareholders, employers, lenders, customers, and

communities in which the firm undergoing the buyout may have operations. Do you believe that on average

LBOs provide a net benefit or cost to society? Explain your answer.

Private Equity Firms Acquire Yellow Pages Business

Qwest Communications agreed to sell its yellow pages business, QwestDex, to a consortium led by the Carlyle Group

and Welsh, Carson, Anderson and Stowe for $7.1 billion. In a two stage transaction, Qwest sold the eastern half of the

yellow pages business for $2.75 billion in late 2002. This portion of the business included directories in Colorado,

Iowa, Minnesota, Nebraska, New Mexico, South Dakota, and North Dakota. The remainder of the business, Arizona,

Idaho, Montana, Oregon, Utah, Washington, and Wyoming, was sold for $4.35 billion in late 2003. Caryle and Welsh

Carson each put in $775 million in equity (about 21 percent of the total purchase price).

Qwest was in a precarious financial position at the time of the negotiation. The telecom was trying to avoid

bankruptcy and needed the first stage financing to meet impending debt repayments due in late 2002. Qwest is a local

phone company in 14 western states and one of the nation’s largest long-distance carriers. It had amassed $26.5 billion

in debt following a series of acquisitions during the 1990s.

The Carlyle Group has invested globally, mainly in defense and aerospace businesses, but it has also invested in

companies in real estate, health care, bottling, and information technology. Welsh Carson focuses primarily on the

communications and health care industries. While the yellow pages business is quite different from their normal areas

of investment, both firms were attracted by its steady cash flow. Such cash flow could be used to trim debt over time

and generate a solid return. The business’ existing management team will continue to run the operation under the new

ownership. Financing for the deal will come from J.P. Morgan Chase, Bank of America, Lehman Brothers, Wachovia

Securities, and Deutsche Bank. The investment groups agreed to a two stage transaction to facilitate borrowing the

large amounts required and to reduce the amount of equity each buyout firm had to invest. By staging the purchase, the

lenders could see how well the operations acquired during the first stage could manage their debt load.

The new company will be the exclusive directory publisher for Qwest yellow page needs at the local level and will

provide all of Qwest’s publishing requirements under a fifty year contract. Under the arrangement, Qwest will continue

to provide certain services to its former yellow pages unit, such as billing and information technology, under a variety

of commercial services and transitional services agreements (Qwest: 2002).

Discussion Questions:

1. Why was QwestDex considered an attractive LBO candidate? Do you think it has significant growth potential?

Explain the following statement: “A business with high growth potential may not be a good candidate for an LBO.

2. Why did the buyout firms want a 50-year contract to be the exclusive provider of publishing services to Qwest

Communications?

3. Why would the buyout firms want Qwest to continue to provide such services as billing and information

technology support? How might such services be priced?

4. Why would it take five very large financial institutions to finance the transactions?

5. Why was the equity contribution of the buyout firms as a percentage of the total capital requirements so much

higher than amounts contributed during the 1980s?

18

Cox Enterprises Offers to Take Cox Communications Private

In an effort to take the firm private, Cox Enterprises announced on August 3, 2004 a proposal to buy the remaining

38% of Cox Communications’ shares that they did not currently own for $32 per share. The deal is valued at $7.9

billion and represented a 16% premium to Cox Communication’s share price at that time. Cox Communications would

become a subsidiary of Cox Enterprises and would continue to operate as an autonomous business. In response to the

proposal, the Cox Communications Board of Directors formed a special committee of independent directors to consider

the proposal. Citigroup Global Markets and Lehman Brothers Inc. have committed $10 billion to the deal. Cox

Enterprises would use $7.9 billion for the tender offer, with the remaining $2.1 billion used for refinancing existing

debt and to satisfy working capital requirements.

Cable service firms have faced intensified competitive pressures from satellite service providers DirecTV Group and

EchoStar communications. Moreover, telephone companies continue to attack cable’s high-speed Internet service by

cutting prices on high-speed Internet service over phone lines. Cable firms have responded by offering a broader range

of advanced services like video-on-demand and phone service. Since 2000, the cable industry has invested more than

$80 billion to upgrade their systems to provide such services, causing profitability to deteriorate and frustrating

investors. In response, cable company stock prices have fallen. Cox Enterprises stated that the increasingly competitive

cable industry environment makes investment in the cable industry best done through a private company structure.

Discussion Questions::

1. Why did the board feel that it was appropriate to set up special committee of independent board directors?

2. Why does Cox Enterprises believe that the investment needed for growing its cable business is best done

through a private company structure?

Financing Challenges in the Home Depot Supply Transaction

Buyout firms Bain Capital, Carlyle Group, and Clayton, Dubilier & Rice (CD&R) bid $10.3 billion in June 2007 to buy

Home Depot Inc.’s HD Supply business. HD Supply represented a collection of small suppliers of construction

products. Home Depot had announced earlier in the year that it planned to use the proceeds of the sale to pay for a

portion of a $22.5 billion stock buyback.

Three banks, Lehman Brothers, JPMorgan Chase, and Merrill Lynch agreed to provide the firms with a $4 billion

loan. The repayment of the loans was predicated on the ability of the buyout firms to improve significantly HD

Supply’s current cash flow. Such loans are normally made with the presumption that the they can be sold to investors,

with the banks collecting fees from both the borrower and investor groups. However, by July, concern about the credit

quality of subprime mortgages spread to the broader debt market and raised questions about the potential for default of

loans made to finance highly leveraged transactions. The concern was particularly great for so–called “covenant–lite”

loans for which the repayment terms were very lenient.

Fearing they would not be able to resell such loans to investors, the three banks involved in financing the HD

Supply transaction wanted more financial protection. Additional protection, they reasoned, would make such loans

more marketable to investors. They used the upheaval in the credit markets as a pretext for reopening negotiations on

19

their previous financing commitments. Home Depot was willing to lower the selling price thereby reducing the amount

of financing required by the buyout firms and was willing to guarantee payment in the event of default by the buyout

firms. While Bain, Carlyle, and CD&R were willing to increase their cash investment and pay higher fees to the banks,

they were unwilling to alter the original terms of the loans. Eventually the banks agreed to provide financing consisting

of a $1 billion “covenant–lite” loan and a $1.3 billion “payment–in–kind” loan. Home Depot agreed to assume the loan

payments on the $1 billion loan if the investor firms were to default and to lower the selling price to $8.5 billion for

87.5 percent of HD Supply, with Home Depot retaining the remaining 12.5 percent.

By the end of August, Home Depot had succeeded in raising the cash needed to help pay for its share repurchase,

and the banks had reduced their original commitment of $4 billion in loans to $2.3 billion. While they had agreed to put

more money into the transaction, the buyout firms had been successful in limiting the number of new restrictive

covenants.

Case Study Discussion Questions:

1. Based on the information given it the case, determine the amount of the price reduction Home Depot accepted

for HD Supply and the amount of cash the three buyout firms put into the transaction?

2. Why did banks lower their lending standards in financing LBOs in 2006 and early 2007? How did the lax

standards contribute to their inability to sell the loans to investors? How did the inability to sell the loans once

made curtail their future lending?

Cerberus Capital Management Acquires Chrysler Corporation

According to the terms of the transaction, Cerberus would own 80.1 percent of Chrysler’s auto manufacturing and

financial services businesses in exchange for $7.4 billion in cash. Daimler would continue to own 19.9 percent of the

new business, Chrysler Holdings LLC. Of the $7.4 billion, Daimler would receive $1.35 billion while the remaining

$6.05 billion would be invested in Chrysler (i.e., $5.0 billion is to be invested in the auto manufacturing operation and

$1.05 billion in the finance unit). Daimler also agreed to pay to Cerberus $1.6 billion to cover Chrysler’s long-term debt

and cumulative operating losses during the four months between the signing of the merger agreement and the actual

closing. In acquiring Chrysler, Cerberus assumed responsibility for an estimated $18 billion in unfunded retiree pension

and medical benefits. Daimler also agreed to loan Chrysler Holdings LLC $405 million.

The transaction is atypical of those involving private equity investors, which usually take public firms private,

expecting to later sell them for a profit. The private equity firm pays for the acquisition by borrowing against the firm’s

assets or cash flow. However, the estimated size of Chrysler’s retiree health–care liabilities and the uncertainty of future

cash flows make borrowing impractical. Therefore, Cerberus agreed to invest its own funds in the business to keep it

running while it restructured the business.

By going private, Cerberus would be able to focus on the long–term without the disruption of meeting quarterly

earnings reports. Cerberus was counting on paring retiree health-care liabilities through aggressive negotiations with

the United Auto Workers (UAW). Cerberus sought a deal similar to what the UAW accepted from Goodyear Tire and

Rubber Company in late 2006. Under this agreement, the management of $1.2 billion in health-care liabilities was

transferred to a fund managed by the UAW, with Goodyear contributing $1 billion in cash and Goodyear stock. By

transferring responsibility for these liabilities to the UAW, Chrysler believed that it would be able to cut in half the $30

dollar per hour labor cost advantage enjoyed by Toyota. Cerberus also expected to benefit from melding Chrysler’s

financial unit with Cerberus’s 51 percent ownership stake in GMAC, GM‘s former auto financing business. By

20

consolidating the two businesses, Cerberus hoped to slash cost by eliminating duplicate jobs, combining overlapping

operations such as data centers and field offices, and increasing the number of loans generated by combining back–

office operations.

However, the 2008 credit market meltdown, severe recession, and subsequent free fall in auto sales threatened the

financial viability of Chrysler, despite an infusion of U.S. government capital, and its leasing operations as well as

GMAC. GMAC applied for commercial banking status to be able to borrow directly from the U.S. Federal Reserve. In

late 2008, the U.S. Treasury purchased $6 billion in GMAC preferred stock to provide additional capital to the

financially ailing firm. To avoid being classified as a bank holding company under direct government supervision,

Cerberus reduced its ownership in 2009 to 14.9 percent of voting stock and 33 percent of total equity by distributing

equity stakes to its coinvestors in GMAC. By surrendering its controlling interest in GMAC, it is less likely that

Cerberus would be able to realize anticipated cost savings by combining the GMAC and Chrysler Financial operations.

In early 2009, Chrysler entered into negotiations with Italian auto maker Fiat to gain access to the firm’s technology in

exchange for a 20 percent stake in Chrysler.

Discussion Questions and Answers:

1. What were the motivations for this deal from Cerberus’ perspective? From Daimler’s perspective?

2. What are the risks to this deal’s eventual success? Be specific.

3. Cite examples of economies of scale and scope?

4. Cerberus and Daimler will own 80.1% and 19.9% of Chrysler Holdings LLC, respectively. Why do you think

the two parties agreed to this distribution of ownership?

5. Which of the leading explanations of why deals sometimes fail to meet expectations best explains why the

combination of Daimler and Chrysler failed? Explain your answer.

21

6. The new company, Chrysler Holdings, is a limited liability company. Why do you think CCM chose this legal

structure over a more conventional corporate structure?

Pacific Investors Acquires California Kool in a Leveraged Buyout

Pacific Investors (PI) is a small private equity limited partnership with $3 billion under management. The objective of

the fund is to give investors at least a 30–percent annual average return on their investment by judiciously investing

these funds in highly leveraged transactions. PI has been able to realize such returns over the last decade because of its

focus on investing in industries that have slow but predictable growth in cash flow, modest capital investment

requirements, and relatively low levels of research and development spending. In the past, PI made several lucrative

investments in the contract packaging industry, which provides packaging for beverage companies that produce various

types of noncarbonated and carbonated beverages. Because of its commitments to its investors, PI likes to liquidate its

investments within four to six years of the initial investment through a secondary public offering or sale to a strategic

investor.

Following its past success in the industry, PI currently is negotiating with California Kool (CK), a privately owned

contract beverage packaging company with the technology required to package many types of noncarbonated drinks.

CK’s 2003 revenue and net income are $190.4 million and $5.9 million, respectively. With a reputation for effective

management, CK is a medium-sized contract packaging company that owns its own plant and equipment and has a

history of continually increasing cash flow. The company also has significant unused excess capacity, suggesting that

production levels can be increased without substantial new capital spending.

The owners of CK are demanding a purchase price of $70 million. This is denoted on the balance sheet (see Table

13-15 at the end of the case) as a negative entry in additional paid-in capital. This price represents a multiple of 11.8

times 2003’s net income, almost twice the multiple for comparable publicly traded companies. Despite the “rich”

multiple, PI believes that it can finance the transaction through an equity investment of $25 million and $47 million in

debt. The equity investment consists of $3 million in common stock, with PI’s investors and CK’s management each

contributing $1.5 million. Debt consists of a $12 million revolving loan to meet immediate working capital

requirements, $20 million in senior bank debt secured by CK’s fixed assets, and $15 million in a subordinated loan

from a pension fund. The total cost of acquiring CK is $72 million, $70 million paid to the owners of CK and $2

million in legal and accounting fees.

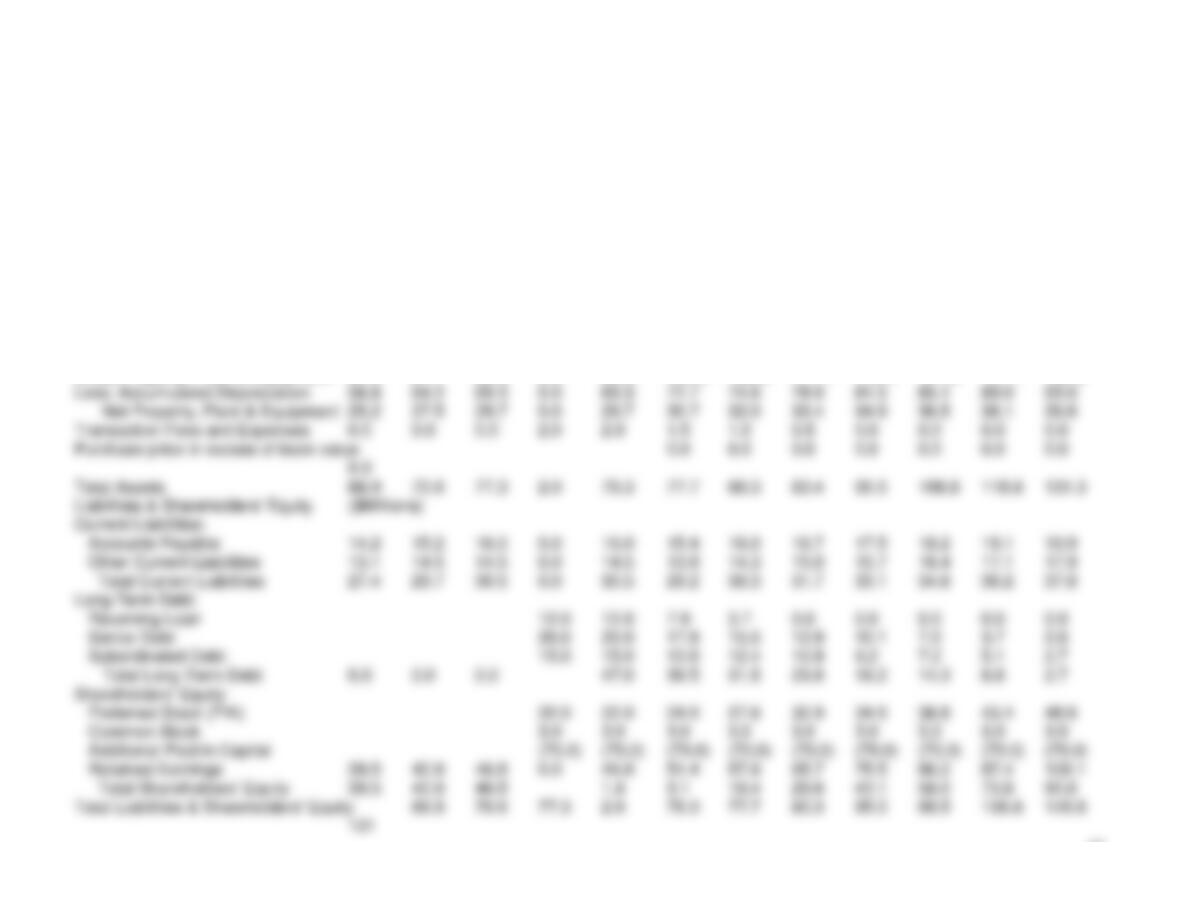

As indicated on Table 13-15, the change in total liabilities plus shareholders’ equity (i.e., total sources of funds or

cash inflows) must equal the change in total assets (i.e., total uses of funds or cash outflows). Therefore, as shown in

the adjustments column, total liabilities increase by $47 million in total borrowings and shareholders’ equity declines by

$45 million (i.e., $25 million in preferred and common equity provided by investors less $70 million paid to CK

owners). The excess of sources over uses of $2 million is used to finance legal and accounting fees incurred in closing

the transaction. Consequently, total assets increase by $2 million and total liabilities plus shareholders’ equity increase

by $2 million between the pre- and postclosing balance sheets as shown in the adjustments column.hasi1 ΔTotal

assets = ΔTotal liabilities + ΔShareholders’ equity: $2 million = $47 million –$45 million = $2 million.

Revenue for CK is projected to grow at 4.5 percent annually through the foreseeable future. Operating expenses and

sales, general, and administrative expenses as a percent of sales are expected to decline during the first three years of

operation due to aggressive cost cutting and the introduction of new management and engineering processes. Similarly,

improved working capital management results in significant declines in working capital as a percent of sales during the

first year of operation. Gross fixed assets as percent of sales is held constant at its 2003 level during the forecast period,

reflecting reinvestment requirements to support the projected increase in net revenue. Equity cash flow adjusted to

include cash generated in excess of normal operating requirements (i.e., denoted by the change in investments available

for sale) is expected to reach $8.5 million annually by 2010. Using the cost of capital method, the cost of equity

declines in line with the reduction in the firm’s beta as the debt is repaid from 26 percent in 2004 to 16.5 percent in

2010. In contrast, the adjusted present value method employs a constant unlevered COE of 17 percent.

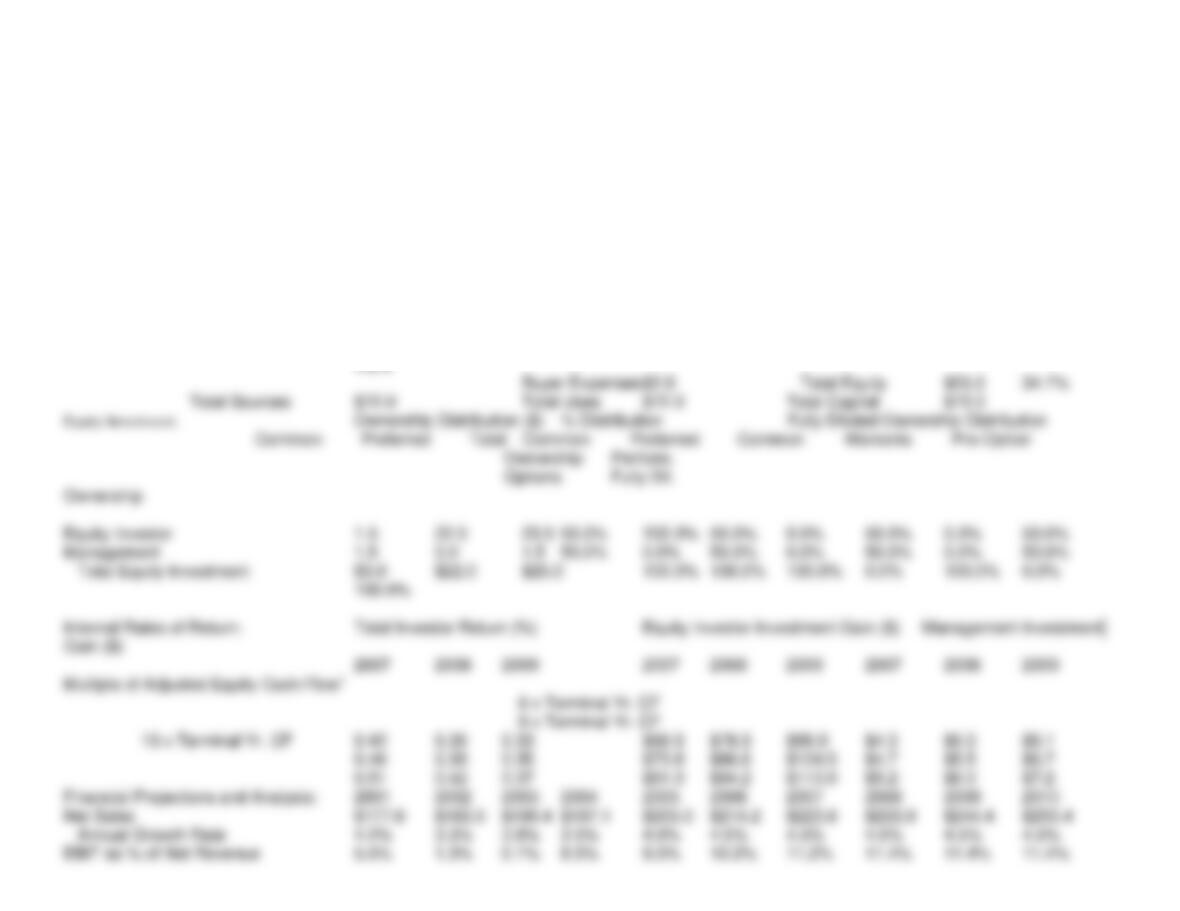

The deal would appear to make sense from the standpoint of PI, since the projected average annual internal rates of

return (IRRs) for investors exceed PI’s minimum desired 30 percent rate of return in all scenarios considered between

2007 and 2009 (see Table 13-13). This is the period during which investors would like to “cash out.” The rates of return

scenarios are calculated assuming the business can be sold at different multiples of adjusted equity cash flow in the

year in which the business is assumed to be sold. Consequently, IRRs are calculated using the cash outflow (initial

equity investment in the business) in the first year offset by any positive equity cash flow from operations generated in

the first year, equity cash flows for each subsequent year, and the sum of equity cash flow in the year in which the

business is sold or taken public plus the estimated sale value (e.g., eight times equity cash flow) in that year. Adjusted

equity cash flow includes free cash flow generated from operations and the increase in “investments available for sale.”

Such investments represent cash generated in excess of normal operating requirements; and as such, this cash is

available to LBO investors.

The actual point at which CK would either be taken public, sold to a strategic investor, or sold to another LBO fund

depends on stock market conditions, CK’s leverage relative to similar firms in the industry, and cash flow performance

as compared to the plan. Discounted cash flow analysis also suggests that PI should do the deal, since the total present

value of adjusted equity cash flow of $57.2 million using the CC method is more than twice the magnitude of the initial

equity investment. At $56 million, the APV method results in a slightly lower estimate of total present value. See

Tables 13-14,13-15, and 13-16 for the income, balance-sheet, and cash-flow statements, respectively, associated with

this transaction. Exhibits 13-1 and 13-2 illustrate the calculation of present value of the transaction based on the cost of

capital and the adjusted present value methods, respectively. Note the actual Excel spreadsheets and formulas used to

create these financial tables are available on the CD-ROM accompanying this book in a worksheet, Excel-Based

Leveraged Buyout Valuation and Structuring Model.

Discussion Questions

1. What criteria did Pacific Investors (PI) use to select California Kool (CK) as a target for an LBO? Why

were these criteria employed?

2. Describe how PI financed the purchase price. Speculate as why each source of financing was selected?

How did CK pay for feels incurred in closing the transaction?

3. What are the advantages and disadvantages of using enterprise cash flow in valuing CK? In what might

EBITDA been a superior (inferior) measure of cash flow for valuing CK?

4. Compare and contrast the Cost of Capital Method and the Adjusted Present Value Method of valuation.

Table 13-11: California Kool Model Output Summary

Sources (Cash Inflows) and Uses (Cash Outflows) of Funds: Pro Forma Capital Structure

Amount($) Interest

Rate (%) Uses of Funds Amount ($) Form of Debt and Equity Market

Value % of Total

Capital

Sources of Funds:

Cash From Balance Sheet $0.0 0.0% Cash to Owners $70.0 Revolving Loan $12.0 16.7%

New Revolving Loan $12.0 9.0% Seller’s Equity $0.0 Senior Debt $20.0 27.8%

New Senior Debt $20.0 9.0% Seller’s Note $0.0 Subordinated Debt $15.0 20.8%

New Subordinated Debt $15.0 12.0% Excess Cash $0.0 Total Debt $47.0 65.3%

New Preferred Stock (PIK) $22.0 12.0% Paid to Owners $70.0 Preferred Equity

$22.0 30.6%

New Common Stock $3.0 0.0% Debt Repayment $0.0 Common Equity $3.0

25

Adjusted Enterprise Cash Flow2 $4.2 $0.2 $0.1 $9.5 $9.6 $10.8 $13.0 $13.4 $14.2 $14.9

Adjusted Equity Cash Flow $4.2 $0.2 $0.1 $0.3 $0.2 $1.8 $7.4 $7.7 $8.1 $8.5

Total Debt Outstanding 0 0 $47.0 $39.5 $31.5 $23.8 $19.2 $14.3 $8.8 $2.7

Total Debt/Adjusted Enterprise Cash Flow 0.0 0.0 NA 4.1 3.3 2.2 1.5 1.1 0.6 0.2

EBIT/Interest Expense 0 0 0 3.6 4.9 6.6 10.1 13.3 18.6 30.9

PV of Adjusted Equity Cash Flow @ 26% $57.2

Table 13-12. California Kool Income Statement and Forecast Assumptions

Historical Period Projections: Twelve Months Ending December 31,

Income Statement Assumptions: 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Net Sales Growth (%) 0.042 0.033 0.038 0.035 0.040 0.045 0.045 0.045 0.045 0.045

Cost of Sales as % of Sales 0.805 0.814 0.780 0.765 0.758 0.755 0.750 0.750 0.750 0.750

SG&A as % of Sales 0.133 0.144 0.142 0.135 0.130 0.125 0.120 0.120 0.120 0.120

Effective Tax Rate (%) 0.400 0.400 0.400 0.400 0.400 0.400 0.400 0.400 0.400 0.400

Income Statement:

Net Sales $177.6 $183.5 $190.4 $197.1 $205.0 $214.2 $223.8 $233.9 $244.4 $255.4

Cost of Sales 143.0 149.3 148.5 150.8 155.4 161.7 167.9 175.4 183.3 191.6

Gross Profit 34.6 34.1 41.9 46.3 49.6 52.5 56.0 58.5 61.1 63.9

Depreciation 1.3 5.4 5.1 2.4 2.9 3.4 3.5 3.7 3.8 4.0

27

Table 13-13. California Kool Balance Sheet and Forecast Assumptions

Historical Period Adjust. Closing Projections: Twelve Months Ended December,

2001 2002 2003 2003 2004 2005 2006 2007 2008 2009 2010

Balance Sheet Assumptions:

Cash & Marketable Securities (%Sales) 0.02 0.02 0.02 0.0 0.02 0.02 0.02 0.02 0.02 0.02 0.02

0.02

Accounts Receivable (%Sales) 0.161 0.158 0.167 0.0 0.167 0.155 0.155 0.155 0.155 0.155 0.155 0.155

Other Current Assets (%Sales) 0.054 0.057 0.063 0.0 0.063 0.055 0.055 0.055 0.055 0.055 0.055 0.055

Gross Prop., Plant & Equip. (%Sales) 0.473 0.5 0.52 0.0 0.52 0.52 0.52 0.52 0.52 0.52 0.52 0.52

Accumulated Depreciation (%GP&E) 0.7 0.7 0.7 0.0 0.7 0.7 0.7 0.7 0.7 0.7 0.7 0.7

Accounts Payable (%Sales) 0.08 0.083 0.084 0.0 0.084 0.078 0.078 0.078 0.078 0.078 0.078 0.078

Other Current Liabilities (%Sales) 0.074 0.079 0.076 0.0 0.076 0.07 0.07 0.07 0.07 0.07 0.07 0.07

Assets: ($Millions)

Current Assets

Cash and Marketable Securities 3.6 3.7 3.8 0.0 3.8 4.1 4.3 4.5 4.7 4.9 5.1 5.1

Accounts Receivable 28.6 29.0 31.8 0.0 31.8 30.6 31.8 33.2 34.7 36.3 37.9 39.6

Other Current Assets 9.6 10.5 12.0 0.0 12.0 10.8 11.3 11.8 12.3 12.9 13.4 14.0

Total Current Assets 41.7 43.1 47.6 0.0 47.6 45.5 47.3 49.5 51.7 54.0 56.4 58.8

Investments Available for Sale 0.0 0.0 0.0 0.0 0.0 8.9 16.3 24.2 32.7

Gross Property, Plant & Equipment 84.0 91.7 99.0 0.0 99.0 102.5 106.6 111.4 116.4 121.6 127.1 132.8

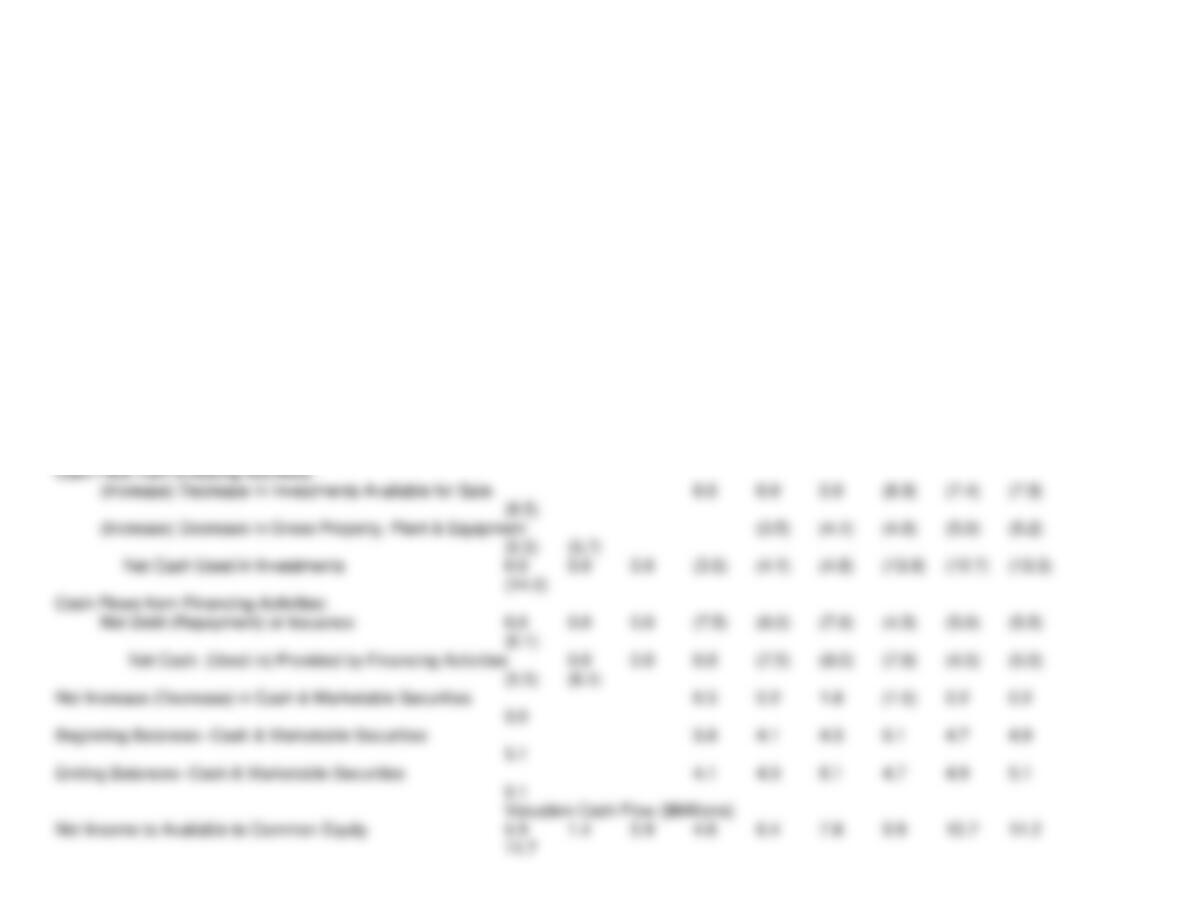

Table 13-14: California Kool Cash Flow Statement and Analysis

Historical Data Projections: Twelve Months Ended

December 31,

2001 2002 2003 2004 2005 2006 2007 2008 2009

2010

GAAP Cash Flow ($Millions)

Cash Flow from Operating Activities:

Net Income Available to Common Equity 5.9 1.4 5.9 4.6 6.4 7.8 9.9 10.7 11.2

11.7

Adjustments to Reconcile Net Income to Net Cash Flow

Depreciation 1.3 5.4 5.1 2.4 2.9 3.4 3.5 3.7 3.8

4.0

Amortization of Financing Fees 0.0 0.0 0.0 0.5 0.5 0.5 0.5 0.0 0.0

0.0

PIK Preferred Dividends 0.0 0.0 0.0 2.6 3.0 3.3 3.7 4.2 4.7

5.2

Net Change in Working Capital 0.0 1.1 (3.6) 1.1 (0.5) (0.6) (0.6) (0.6) (0.7)

(0.7)

Net Cash Flow from Operations 7.2 5.7 14.6 11.3 12.2 14.4 17.0 17.9 19.0

20.3

After-Tax Net Interest Expense (Income) 0 0 0 1.7 1.4 1.2 1.0 0.8 0.6

0.4

Depreciation 1.3 5.4 5.1 2.4 2.9 3.4 3.5 3.7 3.8

4.0

Amortization of Financing Fees 0 0 0 0.5 0.5 0.5 0.5 0 0

0

PIK Preferred Dividend 0 0 0 2.6 3.0 3.3 3.7 4.2 4.7

5.2

Net Cash Flow Before Working Capital 7.2 6.8 11.0 11.9 14.2 16.1 18.6 19.3 20.3

21.3

Net Change in Working Capital 0.0 1.1 (3.6) 1.1 (0.5) (0.6) (0.6) (0.6) (0.7)

(0.7)

Net Cash Flow Before Gross Property, Plant & Equip. Spending 7.2 7.9 7.4 13.0 13.7 15.6 18.0 18.7

19.6 20.7

(Increase) Decrease in Invest Available for Sale 0.0 0.0 0.0 (8.9) (7.4) (7.9)

(8.5)

(Increase) Decrease in Gross Property, Plant & Equipment (3.0) (7.7) (7.3) (3.5) (4.1) (4.8) (5.0) (5.2) (5.5)

(5.7)

Enterprise Cash Flow 4.2 0.2 0.1 9.5 9.6 10.8 4.1 6.0 6.3