Chapter 12: Structuring the Deal:

Tax and Accounting Considerations

Examination Questions and Answers

1. Taxes are an important consideration in almost any transaction, and they are often the primary motivation for an acquisition.

True or False

2. From the viewpoint of the seller or target company shareholder, transactions may be tax-free or entirely or partially taxable.

True or False

3. The sale of stock, rather than assets, is generally preferable to the target firm shareholders to avoid double taxation, if the target

firm is structured as a limited liability company.

True or False

4. A transaction generally will be considered non-taxable to the seller or target firm’s shareholder if it involves the purchase of the

target’s stock or assets for substantially all cash, notes, or some other nonequity consideration. True or False

5. In a triangular cash merger, the target firm may either be merged into an acquirer’s operating or shell acquisition subsidiary with

the subsidiary surviving or the acquirer’s subsidiary is merged into the target firm with the target surviving.

True or False

6. A transaction is usually taxable to the target firm’s shareholders, if the acquirer’s stock is used to purchase at least 30% of the

target firm’s stock or assets. True or False

7. The major advantages of using a triangular structure are limitations of the voting rights of acquiring shareholders and that the

acquirer gains control of the target through a subsidiary without being directly responsible for the target’s known and unknown

liabilities. True or False

8. It is seldom important that the buyer and seller agree on the allocation of the sales price among the assets being sold, since the

allocation will determine the potential tax liability that would be incurred by the seller but that could by passed on to the buyer

through to terms of the sales contract. True or False

9. The form of payment does not affect whether a transaction is taxable to the seller’s shareholders. True or False

10. If a transaction involves a cash purchase of target stock, the target company’s tax cost or basis in the acquired stock or assets is

increased or “stepped up” automatically to their fair market value (FMV), which is equal to the purchase price paid by the

acquirer.

True or False

11. In a cash purchase of assets. the target’s shareholders could be taxed twice, once when the firm pays taxes on any gains and a

second time when the proceeds from the sale are paid to the shareholders either as a dividend or distribution following

liquidation of the corporation.

True or False

12. Empirical studies generally show that the tax shelter resulting from the ability of the acquiring firm to increase the value of

acquired assets to their FMV is a highly important motivating factor for a takeover. True or False

13. Taxable transactions usually involve the purchase of the target’s voting stock, because the purchase of assets automatically will

trigger a taxable gain for the target if the fair market value of the acquired assets exceeds the target firm’s tax basis in the assets.

True or False

14. In a taxable purchase of target stock with cash, the target firm does not restate (i.e., revalue) its assets and liabilities for tax

purposes to reflect the amount that the acquirer paid for the shares of common stock. Rather, the tax basis (i.e., their value on the

target’s financial statements) of assets and liabilities of the target before the acquisition carries over to the acquirer after the

acquisition.

True or False

15. According to Section 338 of the U.S. tax code, a purchaser of 80% or more of the assets of the target may elect to treat the

acquisition as if it were an acquisition of the target’s assets for tax purposes.

True or False

16. The IRS generally views forward triangular cash mergers as a purchase of target stock followed by a liquidation of the target for

which target shareholders will recognize a taxable gain or loss as if they had sold their shares.

True or False

17. Under purchase accounting, the difference between the combined firm’s shareholders’ equity immediately following closing and

the acquiring firm’s shareholders’ equity equals the purchase price paid for the target firm.

True or False

18. Under purchase price accounting, the excess of the purchase price paid over the book value of equity of the target firm is

assigned only to the tangible assets up to their fair market value or to goodwill. True or False

19. Purchase accounting affects only the cash flow of the combined firms but not the reported net income. True or False

20. As a general rule, a transaction is taxable to the target company shareholders if they receive the acquiring firm’s stock and non–

taxable if they receive cash. True or False

21. Tax free reorganizations generally require that all or substantially all of the target company’s assets or shares be acquired in

order to ensure that the acquiring firm has a continuing ownership interest in the combined firms. True or False

22. Tax benefits that result from an acquisition should always be considered as among the most important justification for paying a

very high premium for the target firm. True or False

23. In a forward triangular merger, the target firm’s tax attributes in the form of any tax loss carry forwards or carrybacks or

investment tax credits carry over to the acquirer because the target ceases to exist. True or False

24. The IRS treats the reverse triangular cash merger as a purchase of target shares, with the target firm, including its assets,

liabilities, and tax attributes, ceasing to exist. True or False

25. If the acquirer invokes a 338 election no taxes will have to be paid on any gains on assets written up to their fair market value.

True or False

26. With the purchase of target stock, the acquirer retains the target’s tax attributes, but there is no step up in the basis of the

acquired assets unless the acquirer adopts a 338 election. True or False

27. As a result of a 338 election, the IRS treats the purchase of target shares as a taxable purchase of assets which can be stepped up

to fair market value. Only the buyer has to agree to the 338 election. True or False

28. In a purchase of assets, the buyer retains the target’s tax attributes. True or False

29. In a statutory merger, the buyer retains the target’s tax attributes. True or False

30. In a reverse triangular merger, the acquirer retains the target’s tax attributes. True or False

31. In a tax-free reorganization, the buyer is never required to get shareholder approval. True or False

32. Transactions may be partially taxable if the target shareholders receive some nonequity consideration, such as cash or debt, in

addition to the acquirer’s stock. True or False

33. Acquirers and targets planning to enter into a tax-free transaction seldom seek to get an advance ruling from the IRS to

determine its tax-free status. True or False

34. If the transaction is tax-free, the acquiring company is able to transfer or carry over the target’s tax basis to its own financial

statements. True or False

35. The tax-free structure is generally not suitable for the acquisition of a division within a corporation. True or False.

36. To demonstrate continuity of interests (COI), target shareholders must continue to own a substantial part of the value of the

combined target and acquiring firms. True or False

37. Nontaxable transactions also are called tax-free reorganizations. True or False

38. Tax-free reorganizations generally require that all or substantially all of the target company’s assets or shares be acquired. True

or False

39. A buyer may divest a significant portion of the acquired company immediately following closing without jeopardizing the tax–

free status of the transaction. True or False

40. Tax-free reorganizations require that substantially all of the consideration received by the target’s shareholders be paid in cash.

True or False

41. Tax-free reorganizations require that substantially all of the consideration received by the target’s shareholders be paid in

common or preferred stock. True or False

42. Since the IRS requires that target shareholders continue to hold a substantial equity interest in the acquiring company, the tax

code defines what constitutes a substantial equity interest. True or False

43. Triangular mergers are rarely used for tax-free transactions. True or False

44. To qualify for a Type A reorganization, the transaction must be either a merger or a consolidation. True or False

45. Type A reorganizations are generally viewed as the least flexible of the various types of tax-free reorganizations. True or False

46. The acquirer must be careful that not too large a proportion of the purchase price be composed of cash, because this might not

meet the IRS’s requirement for continuity of interests of the target shareholders and disqualify the transaction as a Type A

reorganization. True or False

47. In a type B stock-for-stock reorganization, the acquirer must purchase an amount of voting stock that comprises at least 50% of

the voting power of all of the target’s voting stock outstanding. True or False

48. A type C reorganization is a stock-for-assets reorganization with the requirement that at least 50% of the FMV of the target’s

assets, as well as the assumption of certain specified liabilities, are acquired solely in exchange for voting stock. True or False

49. The Type C reorganization is used when it is essential for the acquirer not to assume any undisclosed liabilities. True or False

50. A forward triangular merger is the most commonly used form of reorganization for tax-free stock acquisitions in which the form

of payment is acquirer stock. It involves three parties: the acquiring firm, the target firm, and a shell subsidiary of the target

firm. True or False

51. Asset sales by the target firm just prior to the transaction may threaten the tax-free status of the deal. Moreover, tax-free deals are

disallowed within ten-years of a spin-off. True or False

52. The disadvantages of the forward triangular merger may include the requirement of the buyer to get shareholder approval. True

or False

53. A section of the U.S. tax code known as 1031 forbids investors to make a “like kind” exchange of investment properties. True or

False

54. To qualify for a 1031 exchange, the property must be an investment property or one that is used in a trade or business (e.g., a

warehouse, store, or commercial office building). True or False

55. Although NOLs represent a potential source of value, their use must be monitored carefully to realize the full value resulting

from the potential for deferring income taxes. True or False

56. Subchapter S Corporation shareholders, and LLC members, are taxed at their personal tax rates. True or False

57. So-called Morris Trust transactions tax code rules restrict how certain types of corporate deals can be structured to avoid taxes.

True or False

58. Goodwill no longer has to be amortized over its projected life, but it must be written off if it is deemed to have been impaired.

Impairment reviews are to be taken annually or whenever the firm has experienced an event which materially affects the value of

its assets. True or False

59. For tax purposes, goodwill created after July 1993 may be amortized up to 15 years and is tax deductible. Goodwill booked

before July 1993 is also tax deductible. True or False

Multiple Choice (Circle only one)

1. Which of the following is not true about mergers and acquisitions and taxes?

a. Tax considerations and strategies are likely to have an important impact on how a deal is structured by affecting the

amount, timing, and composition of the price offered to a target firm.

b. Tax factors are likely to affect how the combined firms are organized following closing, as the tax ramifications of a

corporate structure are quite different from those of a limited liability company or partnership.

c. Potential tax savings are often the primary motivation for an acquisition or merger.

d. Transactions may be either partly or entirely taxable to the target firm’s shareholders or tax-free.

b. None of the above

2. Which of the following is not true about purchase accounting?

a. For financial reporting purposes, all M&As must be recorded using the purchase method of accounting.

b. Under the purchase method of accounting, the excess of the purchase price over the target’s net asset value is treated as

goodwill on the combined firm’s balance sheet.

c. Goodwill may be amortized up to 40 years.

d. If the fair value of the target’s net assets later falls below its carrying value, the acquirer must record a loss equal to the

difference.

e. None of the above

3. Which of the following is true about purchase accounting?

a. Cash and accounts receivable, reduced for bad debt and returns, are valued at their values on

the books of the target before the acquisition..

b. Marketable securities are valued at their realizable value after transactions costs.

c. Property, plant and equipment are valued at fair market value.

d. Intangible assets are booked at their appraised values.

e. All of the above.

4. Which of the following is not true about goodwill ?

a. Goodwill must be written off over 20 years.

b. Goodwill must be checked for impairment at least annually.

c. The loss of key customers could impair the value of goodwill.

d. Goodwill does not have to be amortized.

e. Goodwill is shown as an asset on the balance sheet.

6

5. Which of the following are not true of net operating loss carrybacks and carryforwards?

a. Net operating loss carrybacks enable firms to recover previous taxes paid.

b. Net operating loss carryforwards enable firms to shelter future taxable income.

c. Net operating loss carryforwards may be applied to income up to 5 years into the future..

d. Loss corporations” cannot use a net operating loss carry forward unless they remain viable and in essentially the same

business for at least 2 years following the closing of the acquisition.

e. None of the above

6. Which of the following is not considered a tax-free reorganization?

a. Type A transactions

b. Type B transactions

c. Type C Transactions

d. Forward triangular merger

e. Cash purchase of assets

7. Which of the following is not true of a 338 election ?

a. It applies to asset purchases only.

b. It applies to stock purchases only.

c. It allows a purchase of stock to be treated as an asset purchase for tax purposes.

d. The buyer must adopt the 338 election.

e. The seller must agree with the adoption of the 338 election.

8. Which of the following is not true of a forward triangular cash merger?

a. It is considered by the IRS as a purchase of target assets.

b. It is generally followed by a liquidation of the target firm.

c. Target shareholders must recognize a gain or loss as if they had sold their shares.

d. The target’s tax attributes carry over to the buyer.

e. Taxes are paid by the target firm on any gain on the sale of its assets and again by shareholders who receive a

liquidating dividend.

9. Which of the following is not true of purchase accounting?

a. Total purchase price paid for the target firm is reflected on the books of the combined companies

b. All liabilities are transferred at the NPV of their future cash payments

c. The cost of the acquired entity becomes the new basis for recording the acquirer’s investment in the assets of the target

company.

d. Goodwill equals the difference between the purchase price paid for the target firm and the book value of acquired

assets.

e. Goodwill must be reduced if it is believed to be impaired.

10. Which of the following is not true of taxable asset purchases?

a. Net operating losses carry over to the acquiring firm

b. The acquiring firm may step up its basis in the acquired assets.

c. The target firm is subject to recapture of tax credits and excess depreciation

d. Target firm shareholders’ are subject to a potential immediate tax liability

e. Target firm net operating losses and tax credits cannot be transferred to the acquiring firm

11. Which of the following is not true of a taxable purchase of stock?

a. Taxable transactions usually involve the purchase of the target’s voting stock with acquirer stock.

b. Taxable transactions usually involve the purchase of the target’s voting stock, because the purchase of assets

automatically will trigger a taxable gain for the target if the fair market value of the acquired assets exceeds the target

firm’s tax basis in the assets.

c. All stockholders are affected equally in a taxable purchase of assets.

7

d. The target firm does not pay any taxes on the transaction.

e. The effect of the tax liability will vary depending on the individual shareholder’s tax basis.

12. The tax status of the transaction may influence the purchase price by

a. Raising the price demanded by the seller to offset potential tax liabilities

b. Reducing the price demanded by the seller to offset potential tax liabilities

c. Causing the buyer to reduce the purchase price if the transaction is taxable to the target firm’s shareholders

d. Forcing the seller to agree to defer a portion of the purchase price

e. Forcing the buyer to agree to defer a portion of the purchase price

13. Which of the following represent taxable transactions?

a. Purchase of assets with cash

b. Purchase of stock with cash

c. Purchase of stock or assets with cash

d. Statutory cash merger or consolidation

e. All of the above

14. Which of the following are true?

a. Taxes are important in any transaction.

b. Taxes should never be the overarching reason for the transaction.

c. Tax savings accruing to the buyer should simply reinforce the decision to acquire.

d. The sale of stock, rather than assets, is generally preferable to the target firm shareholders to avoid double taxation, if

the target firm is structured as a C corporation.

e. All of the above.

15. Which of the following are non-taxable transactions?

a. Statutory stock merger or consolidation

b. Stock for stock merger

c. Stock for assets merger

d. Triangular reverse stock merger

e. All of the above

16. Which of the following are required for an acquisition to be considered tax-free?

a. Continuity of interest

b. A legitimate business purpose other than tax avoidance

c. The use of predominately acquirer shares to buy the target’s shares

d. An all cash acquisition of the target firm’s shares

e. A, B, and C only

17. Which one of the following statements is true?

a. Target firm shareholders may accept cash or acquirer stock in exchange for their shares for the transaction to be

considered tax free

b. To be tax free, the target firm shareholders must receive acquirer firm shares for all of the target firm’s shares

outstanding

c. At least one-half of the assets of the target firm are recorded on the balance sheet of the acquirer at their book rather

than market value in a tax free transaction

d. If the assets of a firm are written up to fair market value as part of the transaction, the increase in value is considered a

taxable gain

e. Target firm shareholders are required by law to pay taxes on any writeup of the firm’s assets to fair market value

18. Purchase accounting requires that

8

a. The excess amount paid for the target firm be recorded as an intangible asset on the books of the acquirer and

immediately written off

b. Target firm assets must be recorded on the acquirer’s balance sheet at their fair market value

c. The excess of the purchase price of the purchase price of the target firm must be recorded as asset and expensed over a

period of 10 years

d. Goodwill once established is never written off

e. Target firm liabilities are recorded on the balance sheet of the acquirer at their book value

19. For financial reporting purposes, goodwill resulting from an acquisition

a. Must equal the fair market value of the target firm’s assets

b. Immediately impacts the acquirer’s profits

c. Is expensed over 20 years

d. Is reviewed annually or whenever there is reason to believe it has lost value and amortized to the extent its value has

declined

e. Never affects the profits of the acquirer

Case Study Short Essay Examination Questions

Merck and Schering-Plough Merger: When Form Overrides Substance

If it walks like a duck and quacks like a duck, is it really a duck? That is a question Johnson & Johnson might ask about a 2009

transaction involving pharmaceutical companies Merck and Schering-Plough. On August 7, 2009, shareholders of Merck and Company

(“Merck”) and Schering–Plough Corp. (Schering-Plough) voted overwhelmingly to approve a $41.1 billion merger of the two firms. With

annual revenues of $42.4 billion, the new Merck will be second in size only to global pharmaceutical powerhouse Pfizer Inc.

At closing on November 3, 2009, Schering-Plough shareholders received $10.50 and 0.5767 of a share of the common stock of the

combined company for each share of Schering-Plough stock they held, and Merck shareholders received one share of common stock of

the combined company for each share of Merck they held. Merck shareholders voted to approve the merger agreement, and Schering–

Plough shareholders voted to approve both the merger agreement and the issuance of shares of common stock in the combined firms.

Immediately after the merger, the former shareholders of Merck and Schering-Plough owned approximately 68 percent and 32 percent,

respectively, of the shares of the combined companies.

The motivation for the merger reflects the potential for $3.5 billion in pretax annual cost savings, with Merck reducing its workforce

by about 15 percent through facility consolidations, a highly complementary product offering, and the substantial number of new drugs

under development at Schering-Plough. Furthermore, the deal increases Merck’s international presence, since 70 percent of Schering–

Plough’s revenues come from abroad. The combined firms both focus on biologics (i.e., drugs derived from living organisms). The new

firm has a product offering that is much more diversified than either firm had separately.

The deal structure involved a reverse merger, which allowed for a tax-free exchange of shares and for Schering-Plough to argue that it

was the acquirer in this transaction. The importance of the latter point is explained in the following section.

To implement the transaction, Schering-Plough created two merger subsidiaries (i.e., Merger Subs 1 and 2) and moved $10 billion in

cash provided by Merck and 1.5 billion new shares (i.e., so–called “New Merck” shares approved by Schering-Plough shareholders) in the

combined Schering-Plough and Merck companies into the subsidiaries. Merger Sub 1 was merged into Schering-Plough, with Schering-

Plough the surviving firm. Merger Sub 2 was merged with Merck, with Merck surviving as a wholly-owned subsidiary of Schering-

Plough. The end result is the appearance that Schering-Plough (renamed Merck) acquired Merck through its wholly-owned subsidiary

(Merger Sub 2). In reality, Merck acquired Schering-Plough.

Former shareholders of Schering–Plough and Merck become shareholders in the new Merck. The “New Merck” is simply Schering–

Plough renamed Merck. This structure allows Schering-Plough to argue that no change in control occurred and that a termination clause

in a partnership agreement with Johnson & Johnson should not be triggered. Under the agreement, J&J has the exclusive right to sell a

rheumatoid arthritis drug it had developed called Remicade, and Schering-Plough has the exclusive right to sell the drug outside the

United States, reflecting its stronger international distribution channel. If the change of control clause were triggered, rights to distribute

the drug outside the United States would revert back to J&J. Remicade represented $2.1 billion or about 20 percent of Schering–Plough’s

2008 revenues and about 70 percent of the firm’s international revenues. Consequently, retaining these revenues following the merger was

important to both Merck and Schering-Plough.

9

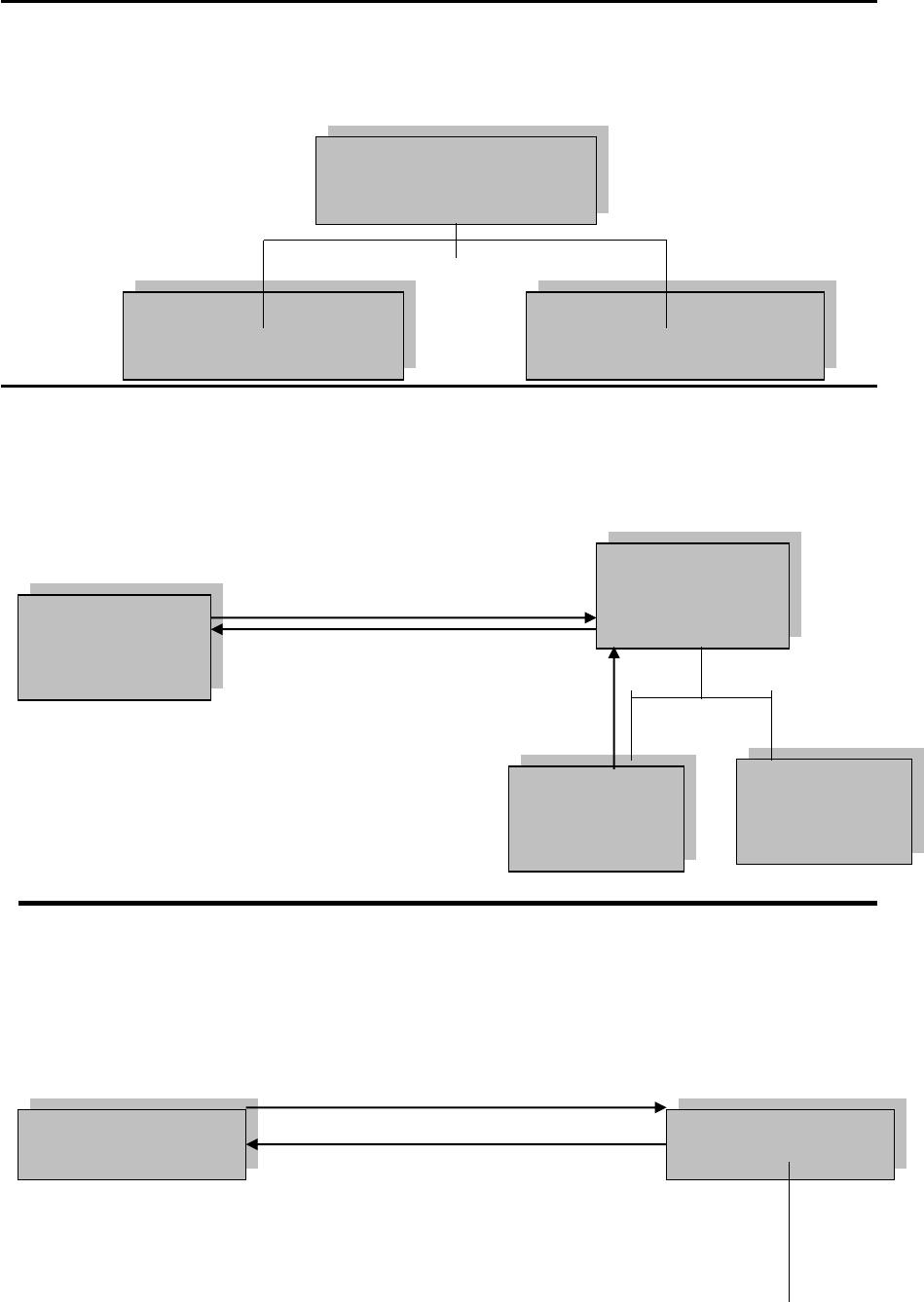

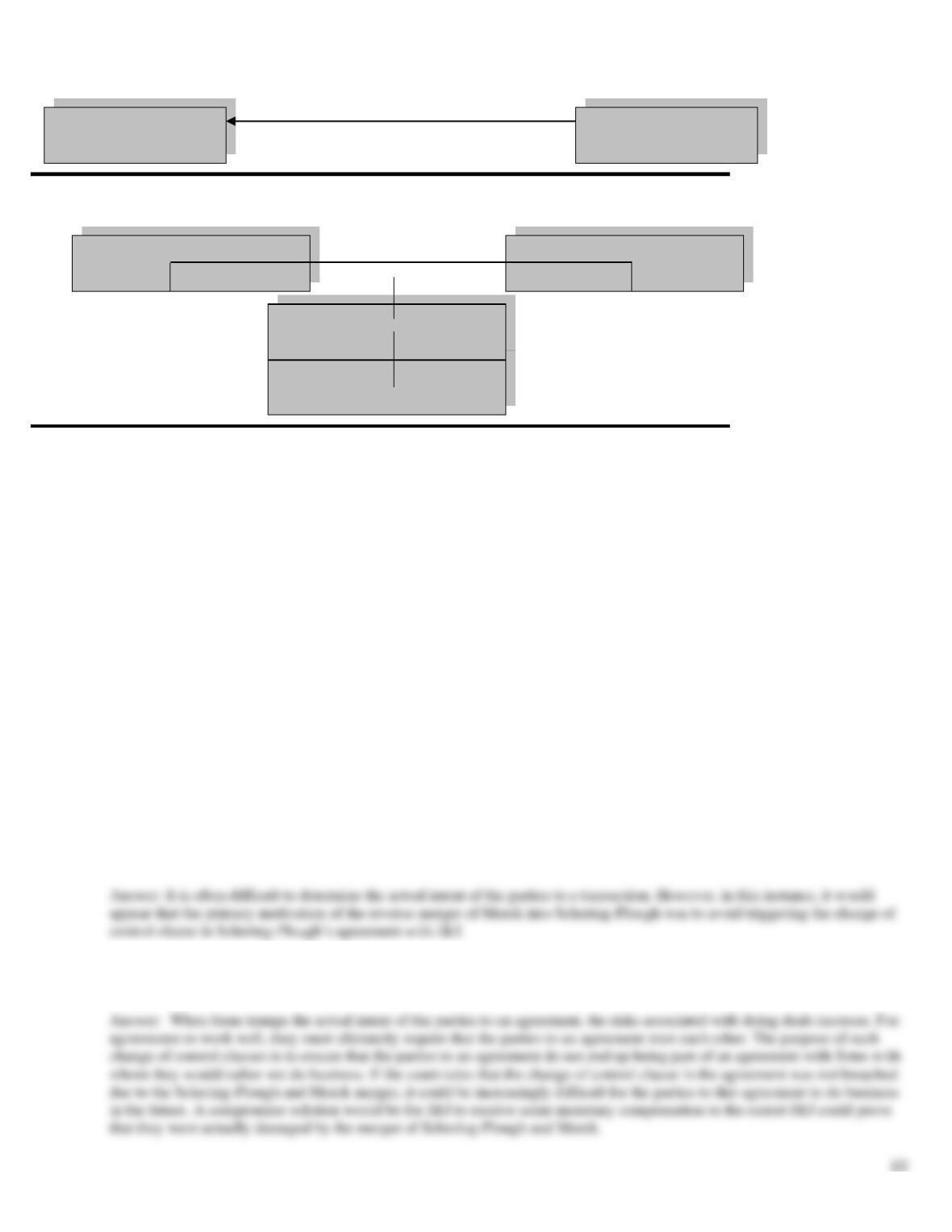

The multi-step process for implementing this transaction is illustrated in the following diagrams. From a legal perspective, all these

actions occur concurrently.

Step 1: Schering-Plough renamed Merck (denoted in the diagrams as “New Merck”)

a. Schering-Plough creates two wholly-owned merger subs

b. Schering-Plough transfers cash provided by Merck and newly issued “New Merck” stock

into Merger Sub 1 and only “New Merck” stock into Merger Sub 2.

Step 2: Schering-Plough Merger:

a. Merger Sub 1 merges into Schering-Plough in a reverse merger with Schering-Plough

surviving

b. To compensate shareholders, Schering-Plough shareholders exchange their

shares for cash and stock in “New Merck”

c. Former Schering-Plough shareholders now hold stock in “New Merck”

Step 3: Merck Merger:

a. Merger Sub 2 merges into Merck with Merck surviving

b. To compensate shareholders, Merck shareholders exchange their shares for

shares in “New Merck”

c. Former shareholders in Merck now hold shares in “New Merck” (i.e.,

a renamed Schering-Plough)

e. Merger Sub 2, a subsidiary of “New Merck,” now owns Merck.

“New Merck”

(Schering Plough)

Merger Sub 2 (Holds “New

Merck” Stock only)

Merger Sub 1 (Holds Cash

and “New Merck” Stock)

Schering-Plough

Shareholders

“New Merck”

(Schering-Plough)

Merger Sub 1

(Merged into

Parent)

Merger Sub 2

(Holds “New

Merck Stock)

$10.50 Cash + .5767 Shares of

“New Merck” Common

1 Share of Schering-Plough

Common

Merck Shareholders

“New Merck”

(Schering-Plough)

1 Share of “New Merck” common

1 Share of Merck Common

Merger

10

Combined Company Resulting from Steps 1-3

Concluding Comments

In reality, Merck was the acquirer. Merck provided the money to purchase Schering-Plough, and Richard Clark, Merck’s chairman and

CEO, will run the newly combined firm when Fred Hassan, Schering–Plough’s CEO, steps down. The new firm has been renamed Merck

to reflect its broader brand recognition. Three–fourths of the new firm’s board consists of former Merck directors, with the remainder

coming from Schering-Plough’s board. These factors would give Merck effective control of the combined Merck and Schering-Plough

operations. Finally, former Merck shareholders own almost 70 percent of the outstanding shares of the combined companies.

J&J initiated legal action in August 2009, arguing that the transaction was a conventional merger and, as such, triggered the change of

control provision in its partnership agreement with Schering-Plough. Schering-Plough argued that the reverse merger bypasses the change

of control clause in the agreement, and, consequently, J&J could not terminate the joint venture. In the past, U.S. courts have tended to

focus on the form rather than the spirit of a transaction. The implications of the form of a transaction are usually relatively explicit, while

determining what was actually intended (i.e., the spirit) in a deal is often more subjective.

In late 2010, an arbitration panel consisting of former federal judges indicated that a final ruling would be forthcoming in 2011.

Potential outcomes could include J&J receiving rights to Remicade with damages to be paid by Merck; a finding that the merger did not

constitute a change in control, which would keep the distribution agreement in force; or a ruling allowing Merck to continue to sell

Remicade overseas but providing for more royalties to J&J.

Discussion Questions

Discussion Questions:

1. Do you agree with the argument that the courts should focus on the form or structure of an agreement and not try to interpret

the actual intent of the parties to the transaction? Explain your answer.

2. How might allowing the form of a transaction to override the actual spirit or intent of the deal impact the cost of doing business

for the parties involved in the distribution agreement? Be specific.

Merck

Merger Sub 2

Former Merck Shareholders

Merck

“New Merck”

(Schering-Plough)

Former Schering-Plough

Shareholders

11

3. How did the use of a reverse merger facilitate the transaction?

Cablevision Uses Tax Benefits to Help Justify the Price Paid for Bresnan Communications

In mid-2010, Cablevision Systems announced that it had reached an agreement to buy privately owned Bresnan Communications for

$1.37 billion in a cash for stock deal. CVS’ motivation for the deal reflected the board’s belief that the firm’s shares were undervalued

and their desire to expand coverage into the western United States.

CVS is the most profitable cable operator in the industry in terms of operating profit margins, due primarily to the firm’s heavily

concentrated customer base in the New York City area. Critics immediately expressed concern that the acquisition would provide few

immediate cost savings and relied almost totally on increasing the amount of revenue generated by Bresnan’s existing customers.

CVS saw an opportunity to gain market share from satellite TV operators providing services in BC’s primary geographic market.

Bresnan, the nation’s 13th largest cable operator, serves Colorado, Montana, Wyoming, and Utah. CVS believes it can sell bundles of

services, including Internet and phone services, to current Bresnan customers. Bresnan’s primary competition comes from DirecTV and

DISH Network, which cannot offer phone and Internet access services.

In order to gain shareholder support, CVS announced a $500 million share repurchase to placate shareholders seeking a return of cash.

The deal was financed by a $1 billion nonrecourse loan and $370 in cash from Cablevision. CVS points out that the firm’s direct

investment in BC will be more than offset by tax benefits resulting from the structure of the deal in which both Cablevision and Bresnan

agreed to treat the purchase of Bresnan’s stock as an asset purchase for tax reporting purposes (i.e., a 338 election). Consequently, CVS

will be able to write up the net acquired Bresnan assets to their fair market value and use the resulting additional depreciation to generate

significant future tax savings. Such future tax savings are estimated by CVS to have a net present value of approximately $400 million

Discussion Question:

1. How is the 338 election likely to impact Cablevision System’s earnings per share immediately following closing? Why?

2. As an analyst, how would you determine the impact of the anticipated tax benefits on the value of the firm?

3. What is the primary risk to realizing the full value of the anticipated tax benefits?

Teva Pharmaceuticals Buys Ivax Corporation

Teva Pharmaceutical Industries’, a manufacturer and distributor of generic drugs, takeover of Ivax Corp for $7.4 billion created the

world’s largest manufacturer of generic drugs. For Teva, based in Israel, and Ivax, headquartered in Miami, the merger eliminated a large

competitor and created a distribution chain that spans 50 countries.

To broaden the appeal of the proposed merger, Teva offered Ivax shareholders the option to receive for each of their shares either

0.8471 of American depository receipts (ADRs) representing Teva shares or $26 in cash. ADRs represent the receipt given to U.S.

investors for the shares of a foreign-based corporation held in the vault of a U.S. bank. Ivax shareholders wanting immediate liquidity

chose to exchange their shares for cash, while those wanting to participate in future appreciation of Teva stock exchanged their shares for

Teva shares.

At closing, each outstanding share of Ivax common stock was cancelled. Each cancelled share represented the right to receive either of

these two previously mentioned payment options. The merger agreement also provided for the acquisition of Ivax by Teva through a

merger of Merger Sub, a newly formed and wholly-owned subsidiary of Teva, into Ivax. As the surviving corporation, Ivax would be a

wholly-owned subsidiary of Teva. The merger involving the exchange of Teva ADRs for Ivax shares was considered as tax-free for those

Ivax shareholders receiving Teva stock under U.S. law as it consisted of predominately acquirer shares.

12

Case Study. JDS Uniphase–SDL Merger Results in Huge Write-Off

What started out as the biggest technology merger in history up to that point saw its value plummet in line with the declining stock

market, a weakening economy, and concerns about the cash-flow impact of actions the acquirer would have to take to gain regulatory

approval. The $41 billion mega-merger, proposed on July 10, 2000, consisted of JDS Uniphase (JDSU) offering 3.8 shares of its stock for

each share of SDL’s outstanding stock. This constituted an approximate 43% premium over the price of SDL’s stock on the

announcement date. The challenge facing JDSU was to get Department of Justice (DoJ) approval of a merger that some feared would

result in a supplier (i.e., JDS Uniphase–SDL) that could exercise enormous pricing power over the entire range of products from raw

components to packaged products purchased by equipment manufacturers. The resulting regulatory review lengthened the period between

the signing of the merger agreement between the two companies and the actual closing to more than 7 months. The risk to SDL

shareholders of the lengthening of the time between the determination of value and the actual receipt of the JDSU shares at closing was

that the JDSU shares could decline in price during this period.

Given the size of the premium, JDSU’s management was unwilling to protect SDL’s shareholders from this possibility by providing a

“collar” within which the exchange ratio could fluctuate. The absence of a collar proved particularly devastating to SDL shareholders,

which continued to hold JDSU stock well beyond the closing date. The deal that had been originally valued at $41 billion when first

announced more than 7 months earlier had fallen to $13.5 billion on the day of closing.

JDSU manufactures and distributes fiber-optic components and modules to telecommunication and cable systems providers

worldwide. The company is the dominant supplier in its market for fiber-optic components. In 1999, the firm focused on making only

certain subsystems needed in fiber-optic networks, but a flurry of acquisitions has enabled the company to offer complementary products.

JDSU’s strategy is to package entire systems into a single integrated unit. This would reduce the number of vendors that fiber optic

network firms must deal with when purchasing systems that produce the light that is transmitted over fiber. SDL’s products, including

pump lasers, support the transmission of data, voice, video, and internet information over fiber-optic networks by expanding their fiber–

optic communications networks much more quickly and efficiently than would be possible using conventional electronic and optical

technologies. SDL had approximately 1700 employees and reported sales of $72 million for the quarter ending March 31, 2000.

As of July 10, 2000, JDSU had a market value of $74 billion with 958 million shares outstanding. Annual 2000 revenues amounted to

$1.43 billion. The firm had $800 million in cash and virtually no long–term debt. Including one-time merger-related charges, the firm

recorded a loss of $905 million. With its price–to-earnings (excluding merger-related charges) ratio at a meteoric 440, the firm sought to

use stock to acquire SDL, a strategy that it had used successfully in eleven previous acquisitions. JDSU believed that a merger with SDL

would provide two major benefits. First, it would add a line of lasers to the JDSU product offering that strengthened signals beamed

across fiber–optic networks. Second, it would bolster JDSU’s capacity to package multiple components into a single product line.

Regulators expressed concern that the combined entities could control the market for a specific type of pump laser used in a wide

range of optical equipment. SDL is one of the largest suppliers of this type of laser, and JDS is one of the largest suppliers of the chips

used to build them. Other manufacturers of pump lasers, such as Nortel Networks, Lucent Technologies, and Corning, complained to

regulators that they would have to buy some of the chips necessary to manufacture pump lasers from a supplier (i.e., JDSU), which in

combination with SDL, also would be a competitor.

As required by the Hart–Scott–Rodino (HSR) Antitrust Improvements Act of 1976, JDSU had filed with the DoJ seeking regulatory

approval. On August 24 th, the firm received a request for additional information from the DoJ, which extended the HSR waiting period.

On February 6, JDSU agreed as part of a consent decree to sell a Swiss subsidiary, which manufactures pump laser chips, to Nortel

Networks Corporation, a JDSU customer, to satisfy DoJ concerns about the proposed merger. The divestiture of this operation set up an

alternative supplier of such chips, thereby alleviating concerns expressed by other manufacturers of pump lasers that they would have to

buy such components from a competitor.

On July 9, 2000, the boards of both JDSU and SDL unanimously approved an agreement to merge SDL with a newly formed, wholly

owned subsidiary of JDS Uniphase, K2 Acquisition, Inc. K2 Acquisition, Inc. was created by JDSU as the acquisition vehicle to complete

the merger. In a reverse triangular merger, K2 Acquisition Inc. was merged into SDL, with SDL as the surviving entity. The post-closing

organization consisted of SDL as a wholly owned subsidiary of JDS Uniphase. The form of payment consisted of exchanging JDSU

common stock for SDL common shares. The share exchange ratio was 3.8 shares of JDSU stock for each SDL common share

outstanding. Instead of a fraction of a share, each SDL stockholder received cash, without interest, equal to dollar value of the fractional

share at the average of the closing prices for a share of JDSU common stock for the 5 trading days before the completion of the merger.

Under the rules of the NASDAQ National Market, on which JDSU’s shares are traded, JDSU is required to seek stockholder approval

for any issuance of common stock to acquire another firm. This requirement is triggered if the amount issued exceeds 20% of its issued

13

and outstanding shares of common stock and of its voting power. In connection with the merger, both SDL and JDSU received fairness

opinions from advisors employed by the firms.

The merger agreement specified that the merger could be consummated when all of the conditions stipulated in the agreement were

either satisfied or waived by the parties to the agreement. Both JDSU and SDL were subject to certain closing conditions. Such conditions

were specified in the September 7, 2000 S4 filing with the SEC by JDSU, which is required whenever a firm intends to issue securities to

the public. The consummation of the merger was to be subject to approval by the shareholders of both companies, the approval of the

regulatory authorities as specified under the HSR, and any other foreign antitrust law that applied. For both parties, representations and

warranties (statements believed to be factual) must have been found to be accurate and both parties must have complied with all of the

agreements and covenants (promises) in all material ways.

The following are just a few examples of the 18 closing conditions found in the merger agreement. The merger is structured so that

JDSU and SDL’s shareholders will not recognize a gain or loss for U.S. federal income tax purposes in the merger, except for taxes

payable because of cash received by SDL shareholders for fractional shares. Both JDSU and SDL must receive opinions of tax counsel

that the merger will qualify as a tax-free reorganization (tax structure). This also is stipulated as a closing condition. If the merger

agreement is terminated as a result of an acquisition of SDL by another firm within 12 months of the termination, SDL may be required to

pay JDSU a termination fee of $1 billion. Such a fee is intended to cover JDSU’s expenses incurred as a result of the transaction and to

discourage any third parties from making a bid for the target firm.

Despite dramatic cost-cutting efforts, the company reported a loss of $7.9 billion for the quarter ending June 31, 2001 and $50.6 billion

for the 12 months ending June 31, 2001. This compares to the projected pro forma loss reported in the September 9, 2000 S4 filing of

$12.1 billion. The actual loss was the largest annual loss ever reported by a U.S. firm up to that time. The fiscal year 2000 loss included a

reduction in the value of goodwill carried on the balance sheet of $38.7 billion to reflect the declining market value of net assets acquired

during a series of previous transactions. Most of this reduction was related to goodwill arising from the merger of JDS FITEL and

Uniphase and the subsequent acquisitions of SDL, E–TEK, and OCLI..

The stock continued to tumble in line with the declining fortunes of the telecommunications industry such that it was trading as low as

$7.5 per share by mid-2001, about 6% of its value the day the merger with SDL was announced. Thus, the JDS Uniphase–SDL merger

was marked by two firsts—the largest purchase price paid for a pure technology company and the largest write-off (at that time) in

history. Both of these infamous “firsts” occurred within 12 months.

Case Study Discussion Questions

1. What is goodwill? How is it estimated? Why did JDS Uniphase write down the value of its goodwill in 2001? Why does this

reflect a series of poor management decisions with respect to mergers completed between 1999 and early 2001?

2. How might the use of stock, as an acquisition “currency,” have contributed to the sustained decline in JDS Uniphase’s stock

through mid-2001? In your judgment what is the likely impact of the glut of JDS Uniphase shares in the market on the future

appreciation of the firm’s share price? Explain your answer.

3. What are the primary differences between a forward and a reverse triangular merger? Why might JDS Uniphase have chosen to

merge its K2 Acquisition Inc. subsidiary with SDL in a reverse triangular merger? Explain your answer.

14

4. Discuss various methodologies you might use to value assets acquired from SDL such as existing technologies, “core”

technologies, trademarks and trade names, assembled workforce, and deferred compensation?

5. Why do boards of directors of both acquiring and target companies often obtain so–called “fairness opinions” from outside

investment advisors or accounting firms? What valuation methodologies might be employed in constructing these opinions?

Should stockholders have confidence in such opinions? Why/why not?

Consolidation in the Wireless Communications Industry:

Vodafone Acquires AirTouch

.

Deregulation of the telecommunications industry has resulted in increased consolidation. In Europe, rising competition is the catalyst

driving mergers. In the United States, the break up of AT&T in the mid-1980s and the subsequent deregulation of the industry has led to

key alliances, JVs, and mergers, which have created cellular powerhouses capable of providing nationwide coverage. Such coverage is

being achieved by roaming agreements between carriers and acquisitions by other carriers. Although competition has been heightened as

a result of deregulation, the telecommunications industry continues to be characterized by substantial barriers to entry. These include the

requirement to obtain licenses and the need for an extensive network infrastructure. Wireless communications continue to grow largely at

the expense of traditional landline services as cellular service pricing continues to decrease. Although the market is likely to continue to

grow rapidly, success is expected to go to those with the financial muscle to satisfy increasingly sophisticated customer demands. What

follows is a brief discussion of the motivations for the merger between Vodafone and AirTouch Communications. This discussion

includes a description of the key elements of the deal structure that made the Vodafone offer more attractive than a competing offer from

Bell Atlantic.

Vodafone

Company History

Vodafone is a wireless communications company based in the United Kingdom. The company is located in 13 countries in Europe,

Africa, and Australia/New Zealand. Vodafone reaches more than 9.5 million subscribers. It has been the market leader in the United

Kingdom since 1986 and as of 1998 had more than 5 million subscribers in the United Kingdom alone. The company has been very

15

successful at marketing and selling prepaid services in Europe. Vodafone also is involved in a venture called Globalstar, LP, a limited

partnership with Loral Space and Communications and Qualcomm, a phone manufacturer. “Globalstar will construct and operate a

worldwide, satellite-based communications system offering global mobile voice, fax, and data communications in over 115 countries,

covering over 85% of the world’s population”.

Strategic Intent

Vodafone’s focus is on global expansion. They are expanding through partnerships and by purchasing licenses. Notably, Vodafone lacked

a significant presence in the United States, the largest mobile phone market in the world. For Vodafone to be considered a truly global

company, the firm needed a presence in the Unites States. Vodafone’s strategy is focused on maintaining high growth levels in its markets

and increasing profitability; maintaining their current customer base; accelerating innovation; and increasing their global presence through

acquisitions, partnerships, or purchases of new licenses. Vodafone’s current strategy calls for it to merge with a company with substantial

market share in the United States and Asia, which would fill several holes in Vodafone’s current geographic coverage.

Company Structure

The company is very decentralized. The responsibilities of the corporate headquarters in the United Kingdom lie in developing corporate

strategic direction, compiling financial information, reporting and developing relationships with the various stock markets, and evaluating

new expansion opportunities. The management of operations is left to the countries’ management, assuming business plans and financial

measures are being met. They have a relatively flat management structure. All of their employees are shareowners in the company. They

have very low levels of employee turnover, and the workforce averages 33 years of age.

AirTouch

Company History

AirTouch Communications launched it first cellular service network in 1984 in Los Angeles during the opening ceremonies at the 1984

Olympics. The original company was run under the name PacTel Cellular, a subsidiary of Pacific Telesis. In 1994, PacTel Cellular spun

off from Pacific Telesis and became AirTouch Communications, under the direction of Chair and Chief Executive Officer Sam Ginn.

Ginn believed that the most exciting growth potential in telecommunications is in the wireless and not the landline services segment of the

industry. In 1998, AirTouch operated in 13 countries on three continents, serving more than 12 million customers, as a worldwide carrier

of cellular services, personal communication services (PCS), and paging services. AirTouch has chosen to compete on a global front

through various partnerships and JVs. Recognizing the massive growth potential outside the United States, AirTouch began their global

strategy immediately after the spin-off.

Strategic Intent

AirTouch has chosen to differentiate itself in its domestic regions based on the concept of “Superior Service Delivery.” The company’s

focus is on being available to its customers 24 hours a day, 7 days a week and on delivering pricing options that meet the customer’s

needs. AirTouch allows customers to change pricing plans without penalty. The company also emphasizes call clarity and quality and

extensive geographic coverage. The key challenges AirTouch faces on a global front is in reducing churn (i.e., the percentage of

customers leaving), implementing improved digital technology, managing pressure on service pricing, and maintaining profit margins by

focusing on cost reduction. Other challenges include creating a domestic national presence.

Company Structure

AirTouch is decentralized. Regions have been developed in the U.S. market and are run autonomously with respect to pricing decisions,

marketing campaigns, and customer care operations. Each region is run as a profit center. Its European operations also are run

independently from each other to be able to respond to the competitive issues unique to the specific countries. All employees are

shareowners in the company, and the average age of the workforce is in the low to mid–30s. Both companies are comparable in terms of

size and exhibit operating profit margins in the mid-to-high teens. AirTouch has substantially less leverage than Vodafone.

Merger Highlights

Vodafone began exploratory talks with AirTouch as early as 1996 on a variety of options ranging from partnerships to a merger. Merger

talks continued informally until late 1998 when they were formally broken off. Bell Atlantic, interested in expanding its own mobile

phone business’s geographic coverage, immediately jumped into the void by proposing to AirTouch that together they form a new

16

wireless company. In early 1999, Vodafone once again entered the fray, sparking a sharp takeover battle for AirTouch. Vodafone

emerged victorious by mid-1999.

Motivation for the Merger

Shared Vision

The merger would create a more competitive, global wireless telecommunications company than either company could achieve

separately. Moreover, both firms shared the same vision of the telecommunications industry. Mobile telecommunications is believed to be

the among the fastest-growing segment of the telecommunications industry, and over time mobile voice will replace large amounts of

telecommunications traffic carried by fixed-line networks and will serve as a major platform for voice and data communication. Both

companies believe that mobile penetration will reach 50% in developed countries by 2003 and 55% and 65% in the United States and

developed European countries, respectively, by 2005.

Complementary Assets

Scale, operating strength, and complementary assets were given as compelling reasons for the merger. The combination of AirTouch and

Vodafone would create the largest mobile telecommunication company at the time, with significant presence in the United Kingdom,

United States, continental Europe, and Asian Pacific region. The scale and scope of the operations is expected to make the combined

firms the vendor of choice for business travelers and international corporations. Interests in operations in many countries will make

Vodafone AirTouch more attractive as a partner for other international fixed and mobile telecommunications providers. The combined

scale of the companies also is expected to enhance its ability to develop existing networks and to be in the forefront of providing

technologically advanced products and services.

Synergy

Anticipated synergies include after-tax cost savings of $340 million annually by the fiscal year ending March 31, 2002. The estimated net

present value of these synergies is $3.6 billion discounted at 9%. The cost savings arise from global purchasing and operating efficiencies,

including volume discounts, lower leased line costs, more efficient voice and data networks, savings in development and purchase of

third-generation mobile handsets, infrastructure, and software. Revenues should be enhanced through the provision of more international

coverage and through the bundling of services for corporate customers that operate as multinational businesses and business travelers.

AirTouch’s Board Analyzes Options

Morgan Stanley, AirTouch’s investment banker, provided analyses of the current prices of the Vodafone and Bell Atlantic stocks, their

historical trading ranges, and the anticipated trading prices of both companies’ stock on completion of the merger and on redistribution of

the stock to the general public. Both offers were structured so as to constitute essentially tax-free reorganizations. The Vodafone proposal

would qualify as a Type A reorganization under the Internal Revenue Service Code; hence, it would be tax-free, except for the cash

portion of the offer, for U.S. holders of AirTouch common and holders of preferred who converted their shares before the merger. The

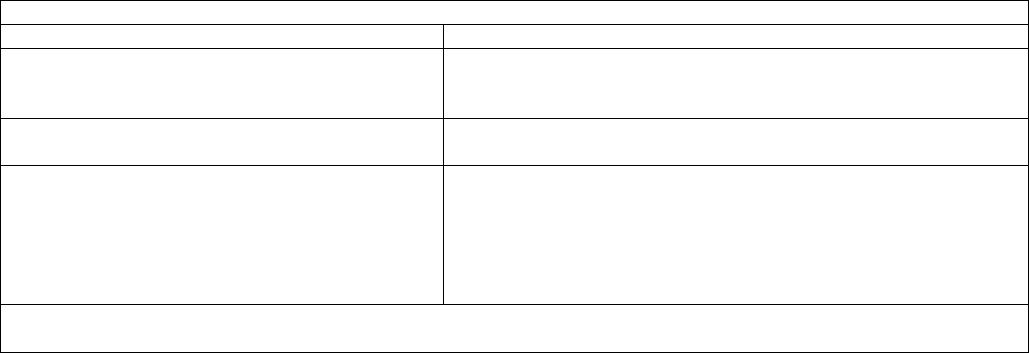

Bell Atlantic offer would qualify as a Type B tax-free reorganization. Table 1 highlights the primary characteristics of the form of

payment (total consideration) of the two competing offers.

Table 1. Comparison of Form of Payment/Total Consideration

Vodafone

Bell Atlantic

5 shares of Vodafone common plus $9 for each

share of AirTouch common

1.54 shares of Bell Atlantic for each share of AirTouch common

subject to the transaction being treated as a pooling of interest under

U.S. GAAP.

Share exchange ratio adjusted upward 9 months out to reflect the

payment of dividends on the Bell Atlantic stock.

A share exchange ratio collar would be used to ensure that AirTouch

shareholders would receive shares valued at $80.08. If the average

closing price of Bell Atlantic stock were less than $48, the exchange

ratio would be increased to 1.6683. If the price exceeded $52, the

exchange rate would remain at 1.54.1

1The collar guarantees the price of Bell Atlantic stock for the AirTouch shareholders because $48 1.6683 and $52 1.54

both equal $80.08.

Morgan Stanley’s primary conclusions were as follows:

1. Bell Atlantic had a current market value of $83 per share of AirTouch stock based on the $53.81 closing price of Bell Atlantic common

stock on January 14, 1999. The collar would maintain the price at $80.08 per share if the price of Bell Atlantic stock during a specified

period before closing were between $48 and $52 per share.

2. The Vodafone proposal had a current market value of $97 per share of AirTouch stock based on Vodafone’s ordinary shares (i.e.,

common) on January 17, 1999.

3. Following the merger, the market value of the Vodafone American Depository Shares (ADSs) to be received by AirTouch shareholders

under the Vodafone proposal could decrease.

4. Following the merger, the market value of Bell Atlantic’s stock also could decrease, particularly in light of the expectation that the

proposed transaction would dilute Bell Atlantic’s EPS by more than 10% through 2002.

In addition to Vodafone’s higher value, the board tended to favor the Vodafone offer because it involved less regulatory uncertainty.

As U.S. corporations, a merger between AirTouch and Bell Atlantic was likely to receive substantial scrutiny from the U.S. Justice

Department, the Federal Trade Commission, and the FCC. Moreover, although both proposals could be completed tax-free, except for the

small cash component of the Vodafone offer, the Vodafone offer was not subject to achieving any specific accounting treatment such as

pooling of interests under U.S. generally accepted accounting principles (GAAP).

Recognizing their fiduciary responsibility to review all legitimate offers in a balanced manner, the AirTouch board also considered a

number of factors that made the Vodafone proposal less attractive. The failure to do so would no doubt trigger shareholder lawsuits. The

major factors that detracted from the Vodafone proposal were that it would not result in a national presence in the United States, the

higher volatility of its stock, and the additional debt Vodafone would have to assume to pay the cash portion of the purchase price.

Despite these concerns, the higher offer price from Vodafone (i.e., $97 to $83) won the day.

Acquisition Vehicle and Post Closing Organization

In the merger, AirTouch became a wholly owned subsidiary of Vodafone. Vodafone issued common shares valued at $52.4 billion based

on the closing Vodafone ADS on April 20, 1999. In addition, Vodafone paid AirTouch shareholders $5.5 billion in cash. On completion

of the merger, Vodafone changed its name to Vodafone AirTouch Public Limited Company. Vodafone created a wholly owned

subsidiary, Appollo Merger Incorporated, as the acquisition vehicle. Using a reverse triangular merger, Appollo was merged into

AirTouch. AirTouch constituted the surviving legal entity. AirTouch shareholders received Vodafone voting stock and cash for their

AirTouch shares. Both the AirTouch and Appollo shares were canceled. After the merger, AirTouch shareholders owned slightly less than

50% of the equity of the new company, Vodafone AirTouch. By using the reverse merger to convey ownership of the AirTouch shares,

Vodafone was able to ensure that all FCC licenses and AirTouch franchise rights were conveyed legally to Vodafone. However,

Vodafone was unable to avoid seeking shareholder approval using this method. Vodafone ADS’s traded on the New York Stock

Exchange (NYSE). Because the amount of new shares being issued exceeded 20% of Vodafone’s outstanding voting stock, the NYSE

required that Vodafone solicit its shareholders for approval of the proposed merger.

Following this transaction, the highly aggressive Vodafone went on to consummate the largest merger in history in 2000 by combining

with Germany’s telecommunications powerhouse, Mannesmann, for $180 billion. Including assumed debt, the total purchase price paid

by Vodafone AirTouch for Mannesmann soared to $198 billion. Vodafone AirTouch was well on its way to establishing itself as a global

cellular phone powerhouse.

Discussion Questions:

1. Did the AirTouch board make the right decision? Why or why not?

2. How valid are the reasons for the proposed merger?

18

3. What are the potential risk factors related to the merger?

4. Is this merger likely to be tax free, partially tax free, or taxable? Explain your answer.

5. What are some of the challenges the two companies are likely to face while integrating the businesses?

Determining Deal Structuring Components

BigCo has decided to acquire Upstart Corporation, a leading supplier of a new technology believed to be crucial to the successful

implementation of BigCo’s business strategy. Upstart is a relatively recent start-up firm, consisting of about 200 employees averaging

about 24 years of age. HiTech has a reputation for developing highly practical solutions to complex technical problems and getting the

resulting products to market very rapidly. HiTech employees are accustomed to a very informal work environment with highly flexible

hours and compensation schemes. Decision-making tends to be fast and casual, without the rigorous review process often found in larger

firms. This culture is quite different from BigCo’s more highly structured and disciplined environment. Moreover, BigCo’s decision

making tends to be highly centralized.

While Upstart’s stock is publicly traded, its six co-founders and senior managers jointly own about 60 percent of the outstanding stock.

In the four years since the firm went public, Upstart stock has appreciated from $5 per share to its current price of $100 per share.

Although they desire to sell the firm, the co-founders are interested in remaining with the firm in important management positions after

the transaction has closed. They also expect to continue to have substantial input in both daily operating as well as strategic decisions.

Upstart competes in an industry that is only tangentially related to BigCo’s core business. Because BigCo’s senior management

believes they are somewhat unfamiliar with the competitive dynamics of Upstart’s industry, BigCo has decided to create a new

corporation, New Horizons Inc., which is jointly owed by BigCo and HiTech Corporation, a firm whose core technical competencies are

more related to Upstart’s than those of BigCo. Both BigCo and HiTech are interested in preserving Upstart’s highly innovative culture.

Therefore, they agreed during negotiations to operate Upstart as an independent operating unit of New Horizons. During negotiations,

both parties agreed to divest one of Upstart’s product lines not considered critical to New Horizon’s long–term strategy immediately

following closing.

New Horizons issued stock through an initial public offering. While the co-founders are interested in exchanging their stock for New

Horizon’s shares, the remaining Upstart shareholders are leery about the long-term growth potential of New Horizons and demand cash in

exchange for their shares. Consequently, New Horizons agreed to exchange its stock for the co–founders’ shares and to purchase the

remaining shares for cash. Once the tender offer was completed, New Horizons owned 100 percent of Upstart’s outstanding shares.

19

Discussion Questions:

1. What is the acquisition vehicle used to acquire the target company, Upstart Corporation? Why was this legal structure used?

2. How would you characterize the post-closing organization? Why was this organizational structure used?

3. What is the form of payment? Why was it used?

4. What was the form of acquisition? How does this form of acquisition protect the acquiring company’s rights to HiTech’s

proprietary technology?

5. How would the use of purchase accounting affect the balance sheets of the combined companies?

6. Was the transaction non-taxable, partially taxable, or wholly taxable to HiTech shareholders? Why?