Which of the following will happen if the accrual adjustment entry is not made to

record an expense incurred but not yet recorded?

A) Both expenses and liabilities will be overstated.

B) Both expenses and liabilities will be understated.

C) Expenses will be understated and liabilities will be overstated.

D) Expenses will be overstated and liabilities will be understated.

The Accumulated Depreciation account is a(n):

A) expense account.

B) liability account.

C) asset account.

D) contra -asset account.

Beginning inventory plus purchases equals:

A) ending inventory.

B) cost of goods sold.

C) goods available for sale.

D) net purchases.

Engstrom Company makes a sale and collects a total of $378, which includes an 8%

sales tax. What is the amount that will be credited to the Sales Revenue account?

A) $378

B) $350

C) $406

D) $348

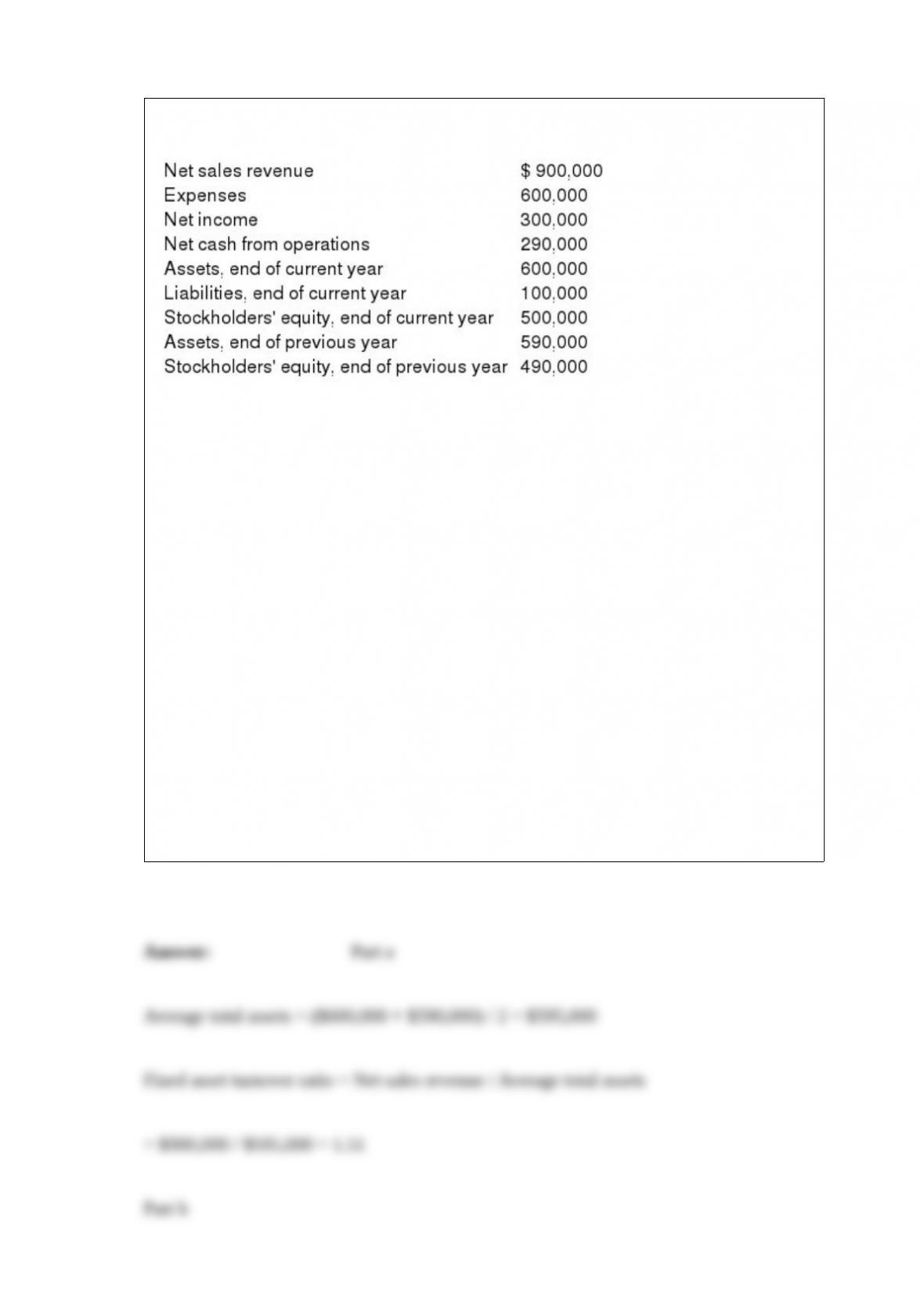

The following information is taken from the financial statements of B. Darin Company:

Expenses include interest of $10,000 and income tax of $90,000. There was an average

of 40,000 shares of common stock outstanding during the year and the market price of

the stock is $15 per share at the end of the year. There was no preferred stock

outstanding during the year.

Required:

Calculate the following ratios for the current year:

Part a. Fixed asset turnover

Part b. Return on equity (ROE)

Part c. Earnings per share (EPS)

Part d. Times interest earned

Part e. Price/Earnings ratio

Part f. Debt-to-assets ratioPart g. Net profit margin

The potential advantages of extending credit to customers include all of the following

except higher:

A) wage expenses.

B) profits.

C) customer satisfaction.

D) revenues.

During June, the Grass is Greener Company mows 100 lawns a week; the company was

paid in advance during May by those customers. The company uses the accrual basis of

accounting. How will these events affect the company’s financial statements?

A) The income statement shows the effects of the transactions in May.

B) The income statement shows the effects of the transactions in June.

C) The balance sheet shows no effect from the transactions in May.

D) The balance sheet shows no effect from these transactions in May or June.

Travis County Bank agrees to lend Brickyard Corporation $200,000 on January 1.

Brickyard signs a $200,000, 4%, 9-month note. Interest is due at maturity on September

30. The company’s fiscal year ends June 30 and adjusting entries are recorded at that

time only.

Use the information above to answer the following question. What adjusting entry

should Brickyard make on June 30 before preparing its annual financial statements?

A) Debit Interest Expense and credit Interest Payable for $4,000

B) Debit Interest Expense and credit Interest Payable for $4,000

C) Debit Interest Payable and credit Interest Expense for $4,000

D) Debit Interest Payable and credit Interest Expense for $4,000

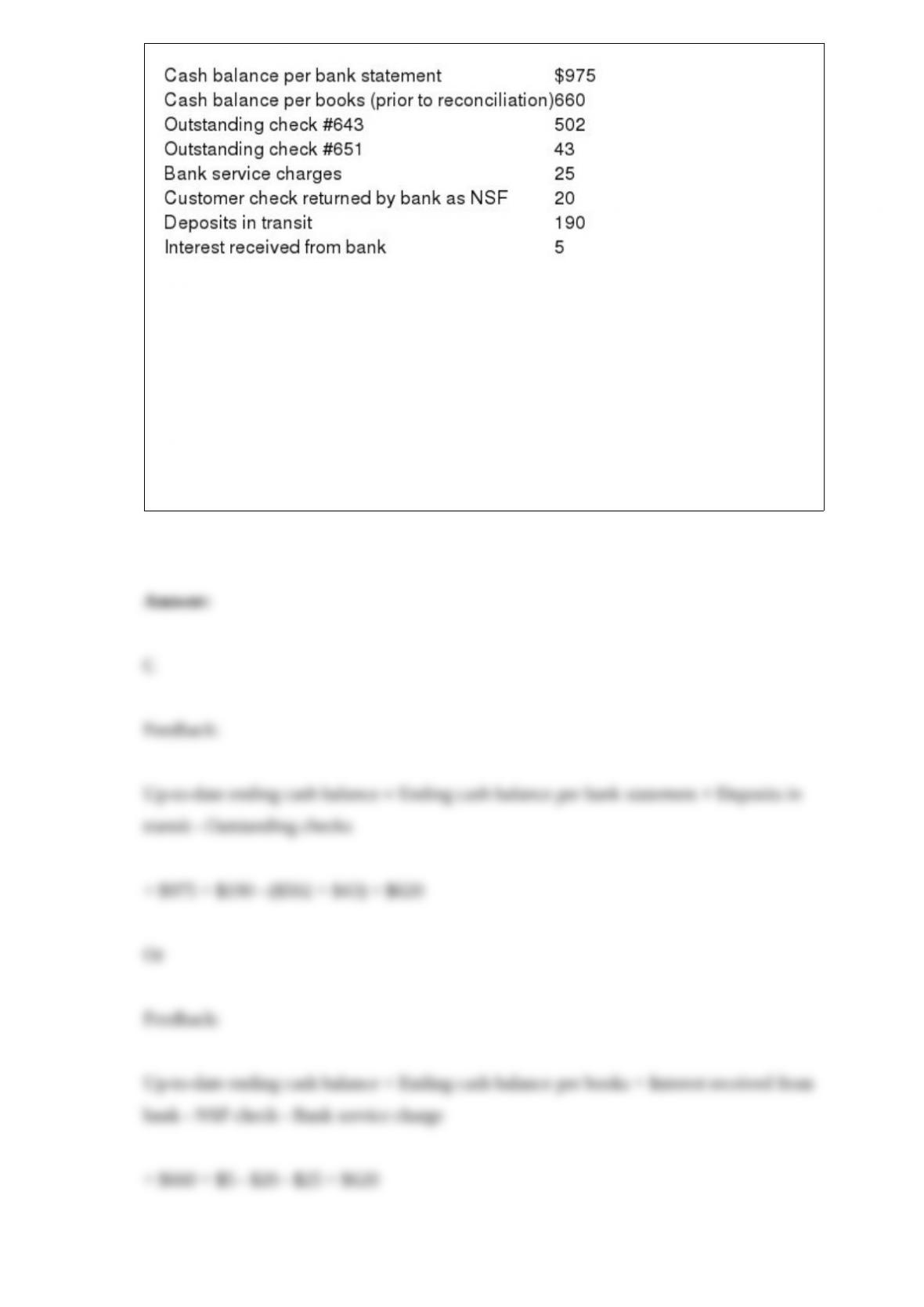

The following information was available to the accountant of Horton Company when

preparing the monthly bank reconciliation:

The amount of cash that should appear on the balance sheet following completion of the

reconciliation and adjustment of the accounting records is:

A) $660.

B) $640.

C) $620.

D) $305.

Which of the following is not a correct statement regarding the Cash Shortage account?

A) It account normally has a debit balance.

B) It is reported on the balance sheet.

C) It is reported as a miscellaneous expense.

D) If the recorded cash exceeds the cash counted, a shortage exists.

Choose the appropriate letter to match the term and the definition. There are more

definitions than terms.

TERM

1> ____ Consignment Inventory

2>____ Cost of Goods Sold

3> ____ Cost of Goods Sold Equation

4> ____ Ending Inventory Equation

5> ____ Finished Goods Inventory

6> ____ Goods in Transit

7> ____ Gross Profit

8> ____ Inventory

9> ____ Merchandise Inventory

10>____ Raw Materials Inventory

11>____ Work in Process Inventory

DEFINITION

A. A valuation rule that requires Inventory to be written down when its market value

falls below its cost.

B. Inventory costing method that assumes that the costs of the first goods purchased are

the costs of the first goods sold.

C. Beginning Inventory + Purchases – Ending Inventory

D. Consists of products acquired in a finished condition, ready for sale without further

processing.

E. The expense that follows directly after Net Sales on a multiple step income

statement.

F. Goods a company is holding on behalf of the goods ‘ owner.

G. Goods that are held for sale in the normal course of business or are used to produce

other goods for sale.

H. Goods that are in the process of being manufactured.

I. Inventory costing method that identifies the cost of the specific item that was sold.

J. The inventory that starts the manufacturing process.

K. Inventory that was in process and now is completed and ready for sale.

L. Inventory items being transported.

M. A measure of the average number of days from the time inventory is bought to the

time it is sold.

N. How many times (on average) that inventory has been bought or sold.

O. Requires that if LIFO is used on the income tax return, it also must be used in

financial statement reporting.

P. Beginning Inventory + Purchases – Cost of Goods Sold

Q. The difference between net sales and cost of goods sold.

R. Inventory costing method that assumes that the costs of the last goods purchased are

the costs of the first goods sold.

S. Inventory costing method that uses the weighted average unit cost of the goods

available for sale for both cost of goods sold and ending inventory.

Which of the following statements is correct?

A) The Accumulated Depreciation account includes cash flows that may be categorized

as both operating and investing.

B) Inventory includes cash flows that may be categorized as both operating and

investing.

C) Retained Earnings includes cash flows that may be categorized as both operating and

investing.

D) Bonds Payable includes cash flows that may be categorized as both operating and

financing.

Assume a voucher system is in use. When the bill for goods or services is obtained,

which control principle(s) must be met when the related control procedures are

designed?

A)Establish responsibility B)Segregate dutiesC)Segregate duties and restrict access

D)Document procedures and independently verify

The ratio that measures the percentage of financing from creditors is the:

A) current ratio.

B) times interest earned ratio.

C) debt-to-assets ratio.

D) Price/Earnings ratio.

Which of the following is an expense of this period?

A) Costs of items used up this period but paid for next period

B) Costs of items paid for in this period but used up next period

C) Cost of land purchased and paid for this period

D) Repayment of debt from a loan in a prior period