1) When the auditor evaluates the effect of a change in accounting principle, the

materiality of the change should be evaluated based on:

A) the prior years presented

B) the current year

C) guidelines included in GAAS

D) the effect on total assets

2) Under the Securities Exchange Act of 1934, most of the litigation against the auditor

has been generated because of the auditor’s involvement with the:

A) 8-K form

B) 10-K form

C) 10-Q form

D) S-1 form

3) For each significant internal control deficiency identified by the auditor, he or she

should design one or more tests of controls to assess the extent of the deficiency and its

effect on the financial statements.

A) True

B) False

4) Form 10-K must be filed with the SEC whenever a public company experiences a

significant event.

A) True

B) False

5) As acceptable audit risk is decreased, the likely cost of conducting an audit increases.

A) True

B) False

6) When there are no perpetual inventory files and inventory is material:

A) an audit cannot be performed, so the auditor must issue a disclaimer

B) a physical inventory should be taken by the client near year-end

C) the auditor will have to perform the inventory count and determine valuation

D) the auditor need not observe inventory counts but must do test counts

7) An auditor must evaluate a specialist’s professional qualifications and understand the

objectives of the specialist’s work.

A) True

B) False

8) The test details of balances procedure that requires the auditor to trace the book

balance on the reconciliation to the general ledger is an attempt to satisfy the audit

objective of:

A) detail tie-in

B) existence

C) completeness

D) accuracy

9) Brown Co.’s financial statements adequately disclose uncertainties that concern

future events, the outcome of which are not reasonably estimable. The auditor’s report

should be a(n):

A) unqualified opinion

B) disclaimer

C) qualified opinion

D) adverse opinion

10) Rule 505 of the

A) proprietorships or partnerships only

B) proprietorships, partnerships, or professional corporations

C) proprietorships, general partnerships, general corporations, professional

corporations, limited liability companies, and limited liability partnerships if permitted

by state law

D) single proprietorships, partnerships, professional corporations if permitted by state

law, or regular corporations

11) The date of the auditor’s report is indicative of the last day of the auditor’s

responsibility for the review of significant events occurring after the balance sheet date.

A) True

B) False

12) The letter of representation is prepared on the CPA firm’s letterhead, addressed to

the client’s chief executive officer, and signed by the audit engagement partner.

A) True

B) False

13) The introductory paragraph of the standard audit report states that the financial

statements are:

A) the responsibility of the auditor

B) the responsibility of management

C) the joint responsibility of management and the auditor

D) none of the above

14) Which one of the choices below is most correct regarding a cause of sampling risk?

A) ineffective use of audit procedures

B) testing less than the entire population

C) use of extensive tests of controls

D) the possibility that a properly-selected sample still may not be representative

15) When the auditor determines the financial statements are fairly stated and then

determines that the auditor lacks independence, the auditor should issue:

A) an adverse opinion

B) a disclaimer of opinion

C) either a qualified opinion or an adverse opinion

D) either a qualified opinion or an unqualified opinion with modified wording

16) Most companies, with the exception of small ones, have effective controls over the

payroll cycle.

A) True

B) False

17) Tests of controls should be performed after substantive tests of transactions.

A) True

B) False

18) The payroll and personnel cycle ends with which of the following events?

A) interviewing job candidates

B) hiring a new employee

C) existing employees submitting requests for payment for work performed

D) issuance of paychecks

19) One difference between the procedures used to obtain an understanding of internal

control and procedures used to test those controls is that tests of controls are more

extensive.

A) True

B) False

20) In determining that the accounts payable cutoff is correct, it is essential that the

cutoff tests be coordinated with the:

A) confirmation of payables

B) tests on long-term liabilities

C) observation of inventory

D) cash count

21) The fieldwork for the December 31, 2011 audit of Schmidt Corporation ended on

March 17, 2012 . The financial statements and auditor’s report were issued and mailed

to stockholders on March 29, 2012 . In each of the material situations (1 through 5)

below, indicate the appropriate action (a, b, c, d, or e). The possible actions are as

follows:

a.Adjust the December 31, 2011 financial statements.

b.Disclose the information in a footnote in the December 31, 2011 financial statements.

c.Request the client revise and reissue the December 31, 2011 financial statements. The

revision should involve an adjustment to the December 31, 2011 financial statements.

d.Request the client revise and reissue the December 31, 2011 financial statements. The

revision should involve the addition of a footnote, but no adjustment, to the December

31, 2011 financial statements.

e.No action is required.

The situations are as follows:

________ 1> On April 5, 2012, you discovered that, on February 16, 2012 a flood

destroyed the entire uninsured inventory in one of Schmidt’s warehouses.

________ 2> On February 17, 2012, you discovered that, on February 16, 2012, a flood

destroyed the entire uninsured inventory in one of Schmidt’s warehouses.

________ 3> On February 17, 2012, you discovered that, on November 30, 2011, a

flood destroyed the entire uninsured inventory in one of Schmidt’s warehouses.

________ 4> On April 5, 2012, you discovered that, on March 30, 2012, a fire

destroyed one of Schmidt’s 13 plants.

________ 5> On April 7, 2012, you discovered that a debtor of Schmidt went bankrupt

on January 6, 2012, due to gradual declining financial health.

22) A ________ is a document that is matched with the customer order to assure that

the correct quantity and type of goods are shipped.

A) sales order

B) customer order

C) vendor invoice

D) sales invoice

23) The two most important qualities for an internal auditor to possess are

independence and competence.

A) True

B) False

24) When the auditor has completed the tests of details of balances and enters phase 4

of the audit process, she must still perform audit procedures for which of the following?

A) contingent liabilities and employee compensation

B) contingent liabilities and subsequent events

C) subsequent events and contractual commitments

D) subsequent events and unrecorded liabilities

25) The five steps in applying materiality are listed below in random order.

1>Estimate the combined misstatement.

2>Estimate the total misstatement in the segment.

3>Set preliminary judgment about materiality.

4>Allocate preliminary judgment about materiality to segments.

5>Compare combined estimate with preliminary judgment about materiality.

The first three steps in correct sequence would be:

A) 1, 2, 5

B) 3, 4, 2

C) 2, 1, 5

D) 3, 2, 4

26) One common use of generalized audit software is to help the auditor identify

weaknesses in the client’s IT control procedures.

A) True

B) False

27) When performing a parallel simulation the auditor may use generalized audit

software (GAS). Which of the following is not seen as an advantage to using GAS?

A) Auditors can learn the software in a short period of time

B) Can be applied to a variety of client’s after detailed customizations

C) Can be applied to a variety of client’s with minimal adjustments to the software

D) Greatly accelerates audit testing over manual procedures

28) The main focus taken by the auditor in verifying liability balances is on the

discovery of:

A) understated liabilities

B) overstated liabilities

C) unrecorded liabilities

D) overstated or extraneous liabilities

29) The two most important balance related audit objectives for notes payable are:

A) completeness and detail tie-in

B) completeness and valuation

C) accuracy and valuation

D) accuracy and completeness

30) The financial statements most commonly audited by external auditors are the

balance sheet, the income statement, and the statement of changes in retained earnings.

A) True

B) False

31) Discuss each of the following documents and records used in the timekeeping and

payroll preparation function in the payroll and personnel cycle: time card, job time

ticket, summary payroll report, payroll journal and payroll master file.

32) In pricing inventory, it is necessary to consider whether replacement cost is lower

than historical cost. When applying lower of cost or market tests, what basis should

auditors use for each of the following categories of inventory:

Raw materials

Work-in-process

Purchased finished goods

33) Presented below is an independent auditor’s report for a private company prepared

by the firm of Harrington and Perry, LLP.

Auditor’s Report

To the president and management of EPM, Inc.

We have examined the accompanying balance sheets and statements of income, retained

earnings, and cash flows of EPM, Inc., as of December 31, 2012 and 2011 . We

performed our examination in accordance with auditing standards generally accepted in

the United States of America and examined, on a test basis, evidence supporting the

accounting principles used and estimates made by management.

In our opinion, the financial statements referred to above accurately present the

financial position of EPM, Inc., in conformity with generally accepted accounting

principles.

Harrington and Perry, LLP

December 31, 2012

Other information:

EPM, Inc., is a for-profit corporation and publishes comparative financial statements for

distribution to shareholders, potential investors, and the general public. The client has a

calendar year-end. For the most recent audit, the auditor completed all significant

fieldwork on March 5, 2013 and issued the audit report on March 16, 2013 . During

2012, EPM changed its method of depreciating long-term assets and properly reflected

the effect of the change in the current year’s financial statements, restated the prior

year’s financial statements, and properly discussed the change in a footnote (Note 4) to

those statements. The auditors are satisfied that the change was preferable.

Required:

Consider all the facts given and rewrite the complete auditor’s report, including report

title, address, body of report, name of firm, and audit report date.

34) Discuss the three matters which Sarbanes-Oxley requires auditors of public

companies to report to the audit committee.

35) There are four important purposes of analytical procedures. Identify three of these

four purposes and, for each purpose, give a specific example of an analytical procedure

that an auditor might perform.

36) You are an audit manager for Rodgers & Co. and have recently taken on as a client

Manufacturing Company. You are in the initial stages of planning the audit and have

decided to start gathering information about the Sales/Collection Cycle of the business.

List below the classes of transactions that you need to gather audit evidence for in

designing your audit procedures.

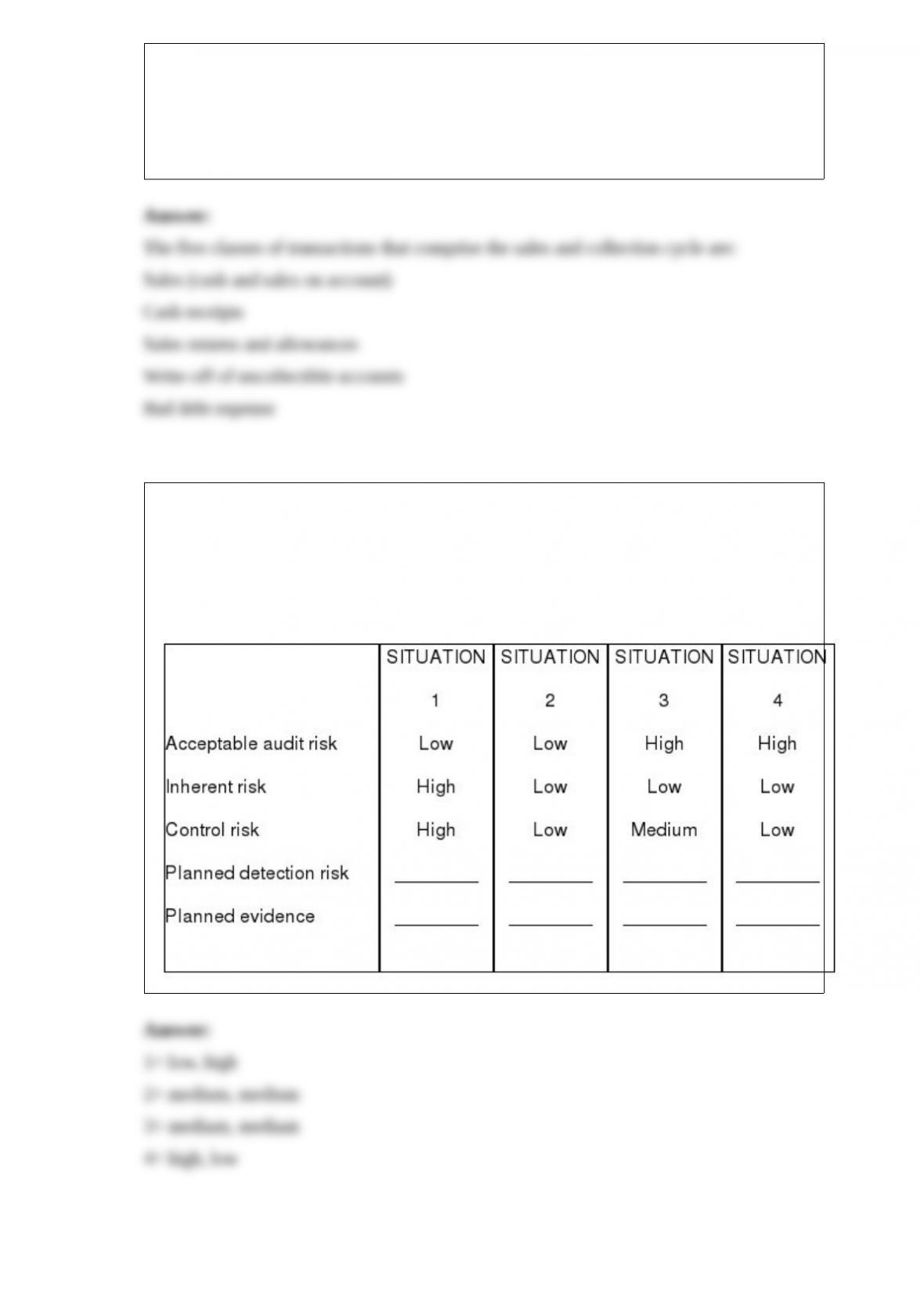

37) In practice, auditors rarely assign numerical probabilities to inherent risk, control

risk, or acceptable audit risk. It is more common to assess these risks as high, medium,

or low. For each of the four situations below, fill in the blanks for planned detection risk

and the amount of evidence you would plan to gather (“planned evidence”) using the

terms high, medium, or low.

38) There are three stages of the audit in which analytical procedures are performed.

Identify each of these three stages and, for each stage, discuss the purpose of

performing analytical procedures in that stage. Also indicate in which stage(s)

analytical procedures are required by current professional auditing standards.