Under GAAP, the declaration of a property dividend may require the recognition of a

gain or loss if the fair value of the property is different from its book value on the

declaration date.

Using the balance sheet approach, bad debt expense is an indirect result of estimating

the net realizable value of accounts receivable.

The statement of shareholders’ equity discloses the changes in the temporary

shareholders’ equity accounts.

Prepaid expenses are classified as current assets if the services purchased are expected

to expire within 12 months or the operating cycle, whichever is longer.

The net method of accounting for cash discounts requires adjusting entries for discounts

taken.

If the lessee is expected to take ownership of a leased asset at the end of the lease term,

the lessor must use an estimated residual value when calculating the lease payments

necessary to achieve a desired rate of return.

According to International Financial Reporting Standards (IFRS), the costs to

successfully defend an intangible right normally are capitalized and amortized.

Dividends in arrears on cumulative preferred stock are liabilities to be paid at a later

date.

“Determine whether it is probable the seller will collect the consideration it is entitled to

receive” is one of the five steps to applying the core revenue recognition principle.

Use of the installment sales method requires that firms track the gross profit percentage

associated with a particular sale.

Other things being equal, the present value of an annuity due will be less than the

present value of an ordinary annuity.

Amortizing a net gain for pensions and other postretirement benefit plans will:

a. Increase retained earnings and increase accumulated other comprehensive income.

b. Decrease retained earnings and decrease accumulated other comprehensive income.

c. Increase retained earnings and decrease accumulated other comprehensive income.

d. Decrease retained earnings and increase accumulated other comprehensive income.

The accounting equation can be stated as:

a. A + L – OE = 0.

b. A – L + OE = 0.

c. -A + L – OE = 0.

d. A – L – OE = 0.

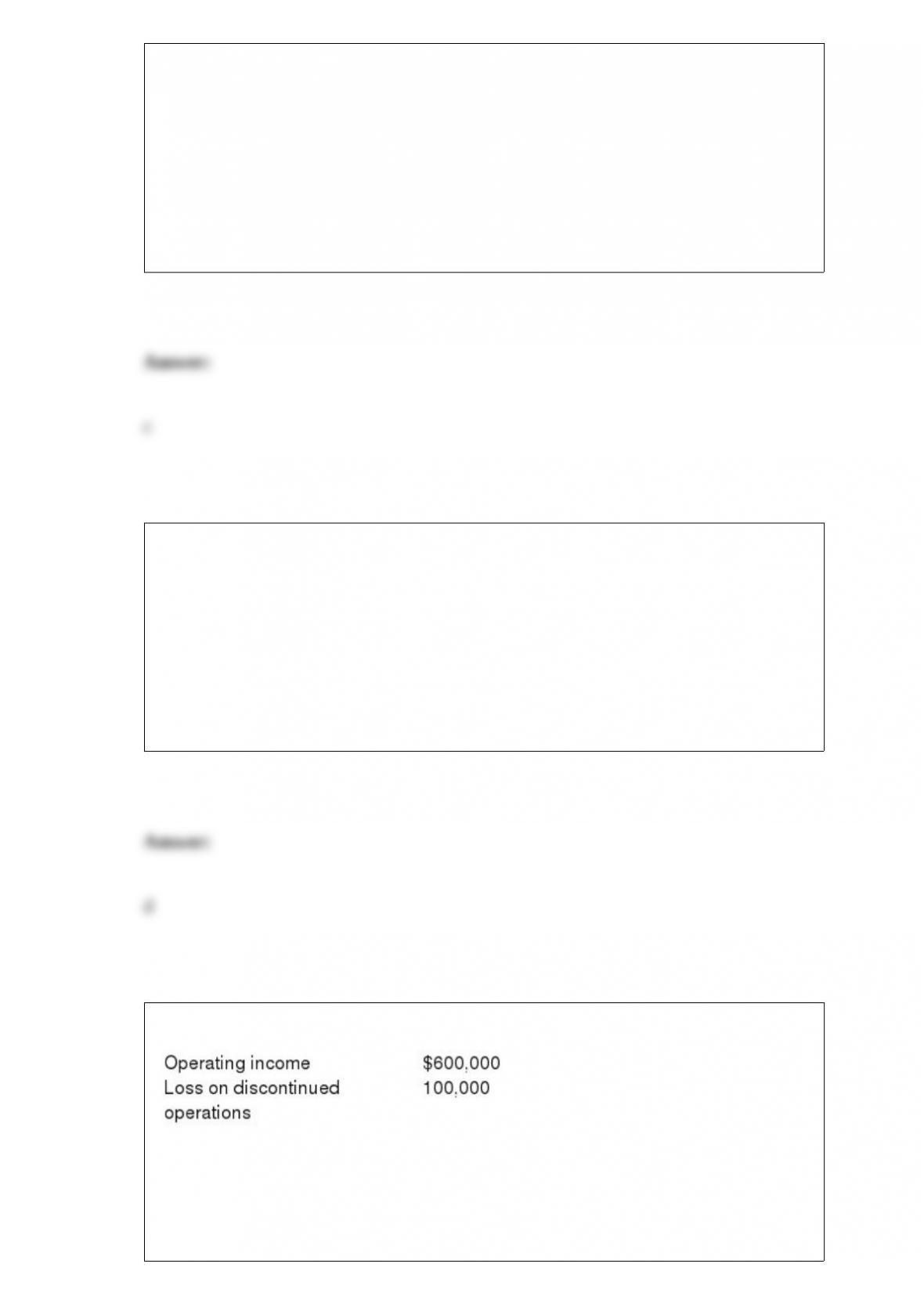

Provincial Inc. reported the following before-tax income statement items:

Provincial has a 30% income tax rate.

Provincial would report the following amount of income tax expense as a line item in

the income statement:

a. $198,000.

b. $180,000.

c. $168,000.

d. $150,000.

Tri Fecta, a partnership, had revenues of $360,000 in its first year of operations. The

partnership has not collected on $35,000 of its sales and still owes $40,000 on $150,000

of merchandise it purchased. There was no inventory on hand at the end of the year. The

partnership paid $25,000 in salaries. The partners invested $40,000 in the business and

$25,000 was borrowed on a five-year note. The partnership paid $3,000 in interest that

was the amount owed for the year and paid $8,000 for a two-year insurance policy on

the first day of business.

Compute net income for the first year for Tri Fecta.

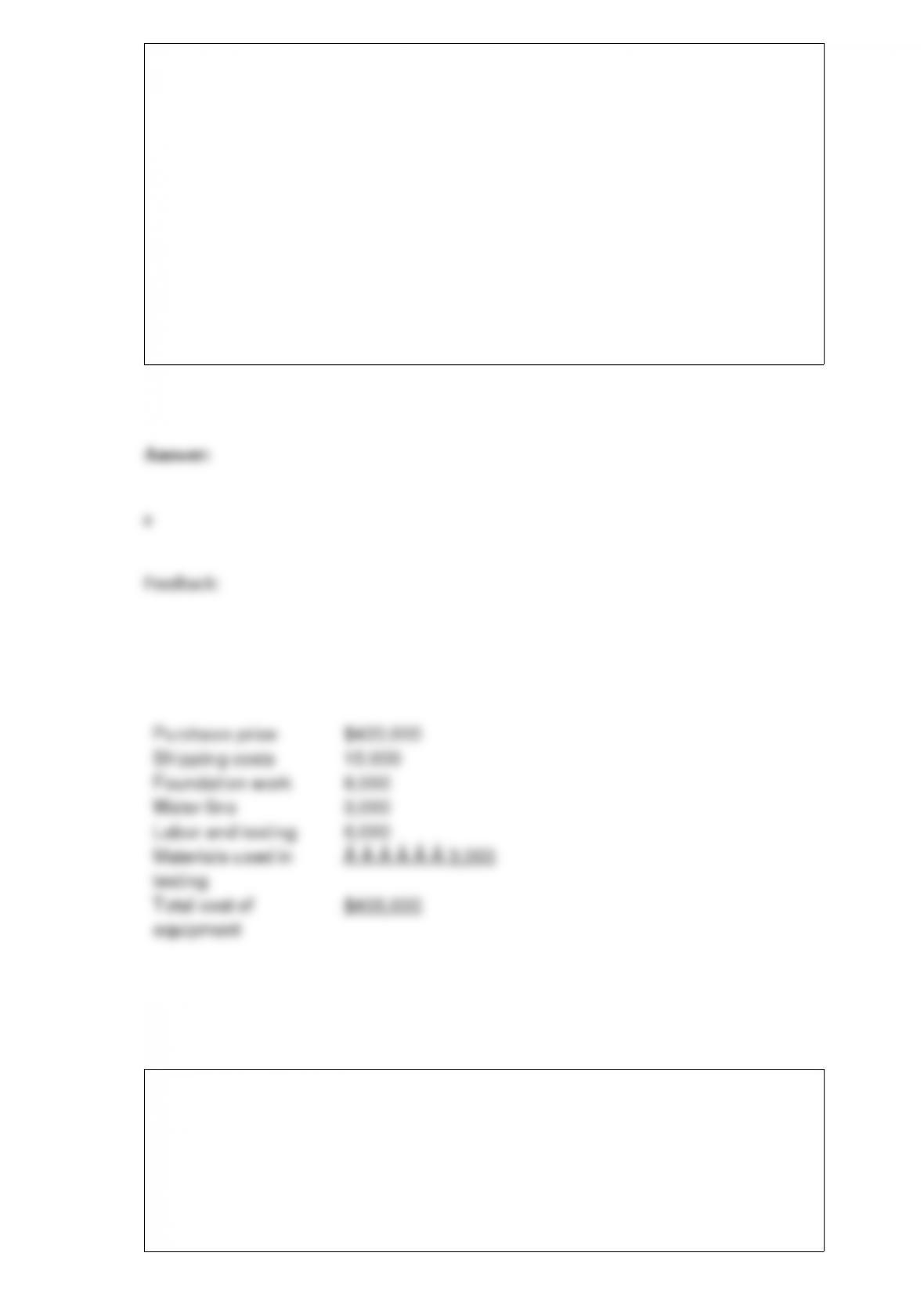

Holiday Laboratories purchased a high-speed industrial centrifuge at a cost of

$420,000. Shipping costs totaled $15,000. Foundation work to house the centrifuge cost

$8,000. An additional water line had to be run to the equipment at a cost of $3,000.

Labor and testing costs totaled $6,000. Materials used up in testing cost $3,000. The

capitalized cost is:

a. $455,000.

b. $446,000.

c. $437,000.

d. $435,000.

Revenue and expense items and components of other comprehensive income can be

reported in a single statement of comprehensive income using:

a. U.S. GAAP.

b. IFRS.

c. Both U.S. GAAP and IFRS.

d. Neither U.S. GAAP nor IFRS.

Which of the following never requires an outflow of cash?

a. Early extinguishment of debt.

b. Retirement of common stock.

c. Payment of dividends.

d. Amortization of patent.

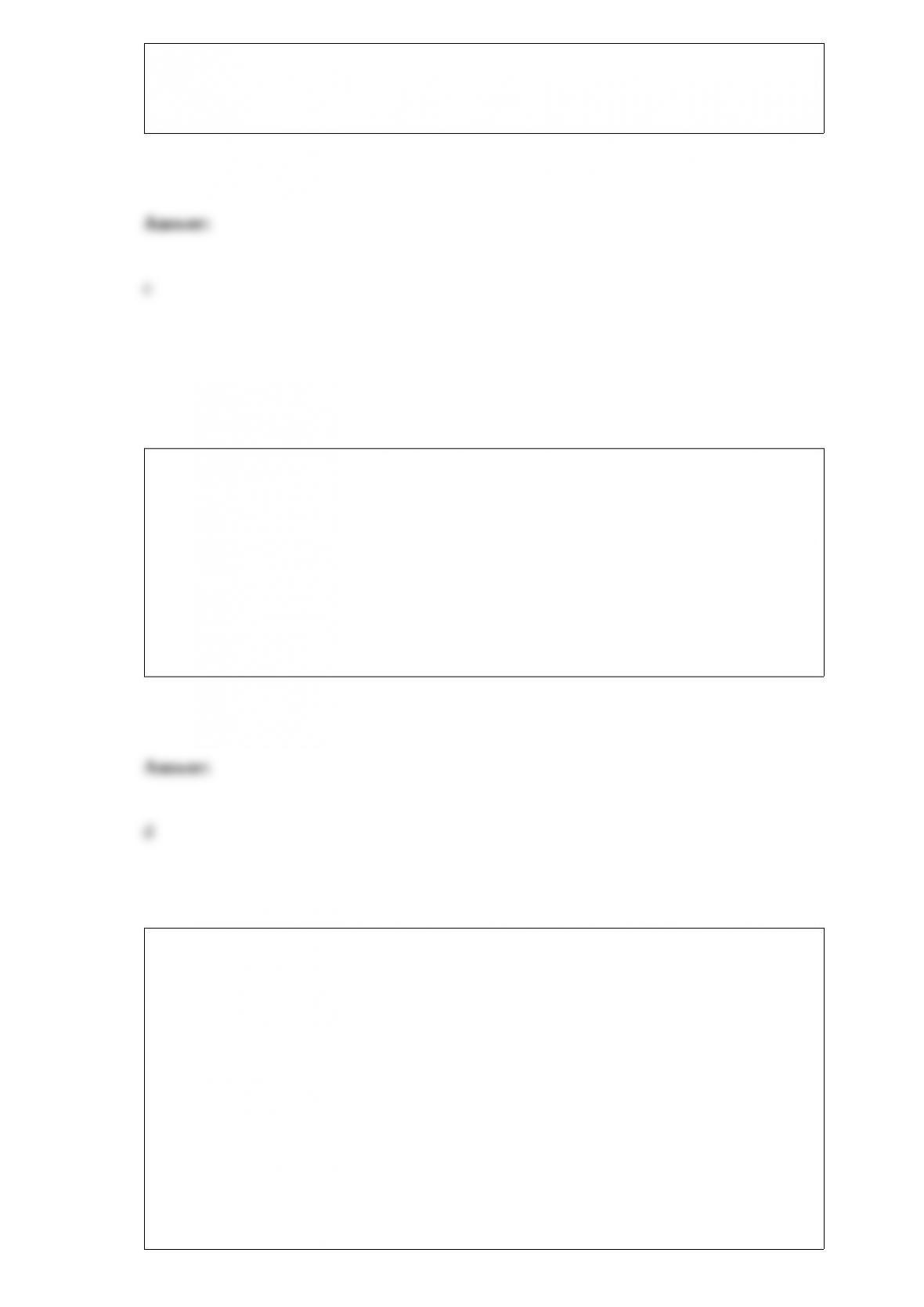

At the start of the current year, SBC Corp. purchased 30% of Sky Tech Inc. for $45

million. At the time of purchase, the carrying value of Sky Tech’s net assets was $75

million. The fair value of Sky Tech’s depreciable assets was $15 million in excess of

their book value. For this year, Sky Tech reported a net income of $75 million and

declared and paid $15 million in dividends.

The total amount of additional depreciation to be recognized by SBC over the

remaining life of the assets is:

a. $4.5 million.

b. $15 million.

c. $27 million.

d. None of these answer choices is correct.

Maas LLP developed software that helps farmers to plow their fields in a manner that

prevents erosion and maximizes the effectiveness of irrigation. Sunny Dale paid a

licensing fee of $20,000 for a copy of the software. Although Sunny Dale can use the

software as long as it wants, Maas expects that Sunny Dale will use the software for

approximately 5 years. Maas does not anticipate any further interaction with Sunny

Dale following transfer of the license. How much revenue should Maas recognize in the

first year of the contract?

a. $0

b. $4,000

c. $5,000

d. $20,000

Carter Appliances is preparing its annual report for the current fiscal year. The

company’s controller has asked for your help in determining how best to disclose

information about the following items: 1> A subsequent event.

2> Inventory costing method.

3> Composition of accrued liabilities.

4> Useful lives of depreciable assets.

5> Information on long-term leases.

6> Allowance for uncollectible accounts.

7> Revenue recognition policy.

8> Pension plans.

Required: Indicate whether the above items should be disclosed (a) in the summary of

significant accounting policies note, (b) in a separate disclosure note, or (c) on the face

of the balance sheet

If a company’s deferred tax asset is not reduced by a valuation allowance, the company

believes it is:

a. Probable that sufficient taxable income will be generated in future years to realize the

full tax benefit.

b. Probable that sufficient financial income will be generated in future years to realize

the full tax benefit.

c. More likely than not that sufficient taxable income will be generated in future years

to realize the full tax benefit.

d. More likely than not that sufficient financial income will be generated in future years

to realize the full tax benefit.

As of January 1, 2016, Farley Co. had a credit balance of $520,000 in its allowance for

uncollectible accounts. Based on experience, 2% of Farley’s credit sales have been

uncollectible. During 2016, Farley wrote off $650,000 of accounts receivable. Credit

sales for 2016 were $18,000,000. In its December 31, 2016, balance sheet, what amount

should Farley report as allowance for uncollectible accounts?

a. $230,000.

b. $360,000.

c. $590,000.

d. $880,000.

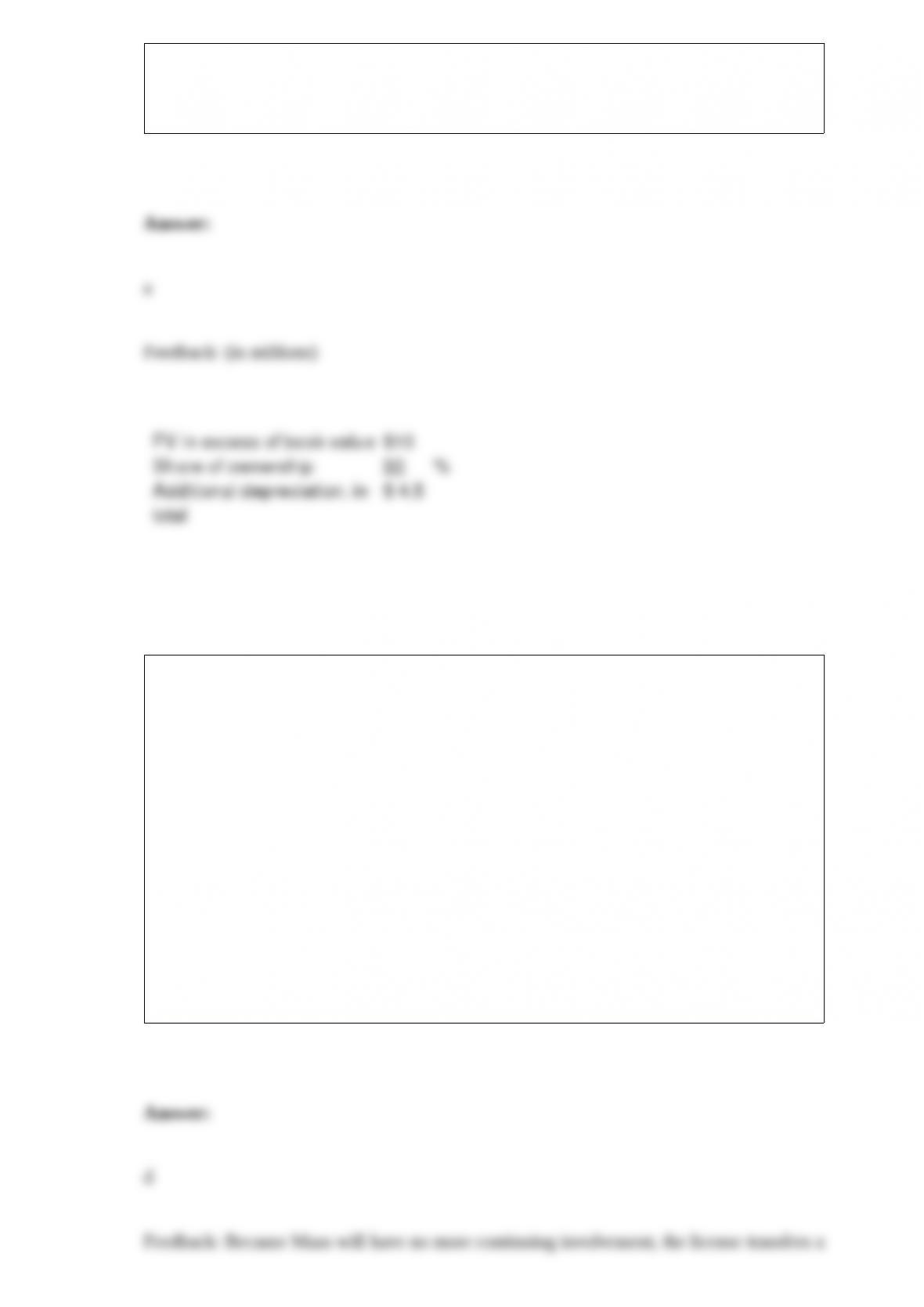

Assume that, on January 1, 2016, Sosa Enterprises paid $3,000,000 for its investment in

36,000 shares of Orioles Co. Further, assume that Orioles has 120,000 total shares of

stock issued and estimates an eight-year remaining useful life and straight-line

depreciation with no residual value for its depreciable assets.

At January 1, 2016, the book value of Orioles’ identifiable net assets was $7,000,000,

and the fair value of Orioles was $10,000,000. The difference between Orioles’ fair

value and the book value of its identifiable net assets is attributable to $1,800,000 of

land and the remainder to depreciable assets. Goodwill was not part of this transaction.

The following information pertains to Orioles during 2016:

What amount would Sosa Enterprises report in its year-end 2016 balance sheet for its

investment in Orioles Co.?

a. $3,200,000.

b. $3,180,000.

c. $3,135,000.

d. $3,027,000.

The following facts apply to TinyPart Toy Company’s pending litigation as of

December 31, 2016: a. TinyPart is defending against a lawsuit and believes there is a

51% chance it will lose in court. If it loses, TinyPart estimates that damages will be

$100,000.

b. TinyPart is defending against another lawsuit for which management believes it is

virtually certain to lose in court. If it loses the lawsuit, management estimates damages

will fall somewhere in the range of $30,000 to $50,000, with each amount in that range

equally likely to occur.

c. TinyPart is defending against another lawsuit that is identical to item (b), but the

relevant losses will only occur far into the future. The present values of the endpoints of

the range are $15,000 and $25,000. TinyPart’s management believes the effects of time

value of money on these amounts are material, but also believes the timing of these

amounts is uncertain.

d. TinyPart is defending against a fourth lawsuit and believes there is only a 25%

chance it will lose in court. If TinyPart loses, it believes damages will fall somewhere in

the range of $35,000 to $40,000, with each amount in that range equally likely to occur.

Indicate how TinyPart would disclose or account for the lawsuit described in part (d)

under U.S. GAAP and under IFRS in the financial statements for the year ended

December 31, 2016.

Tru Fashions has bonds outstanding during a year in which the market rate of interest

has declined. If Tru has elected the fair value option for the bonds, will it report a gain

or a loss on the bonds for the year? Explain.

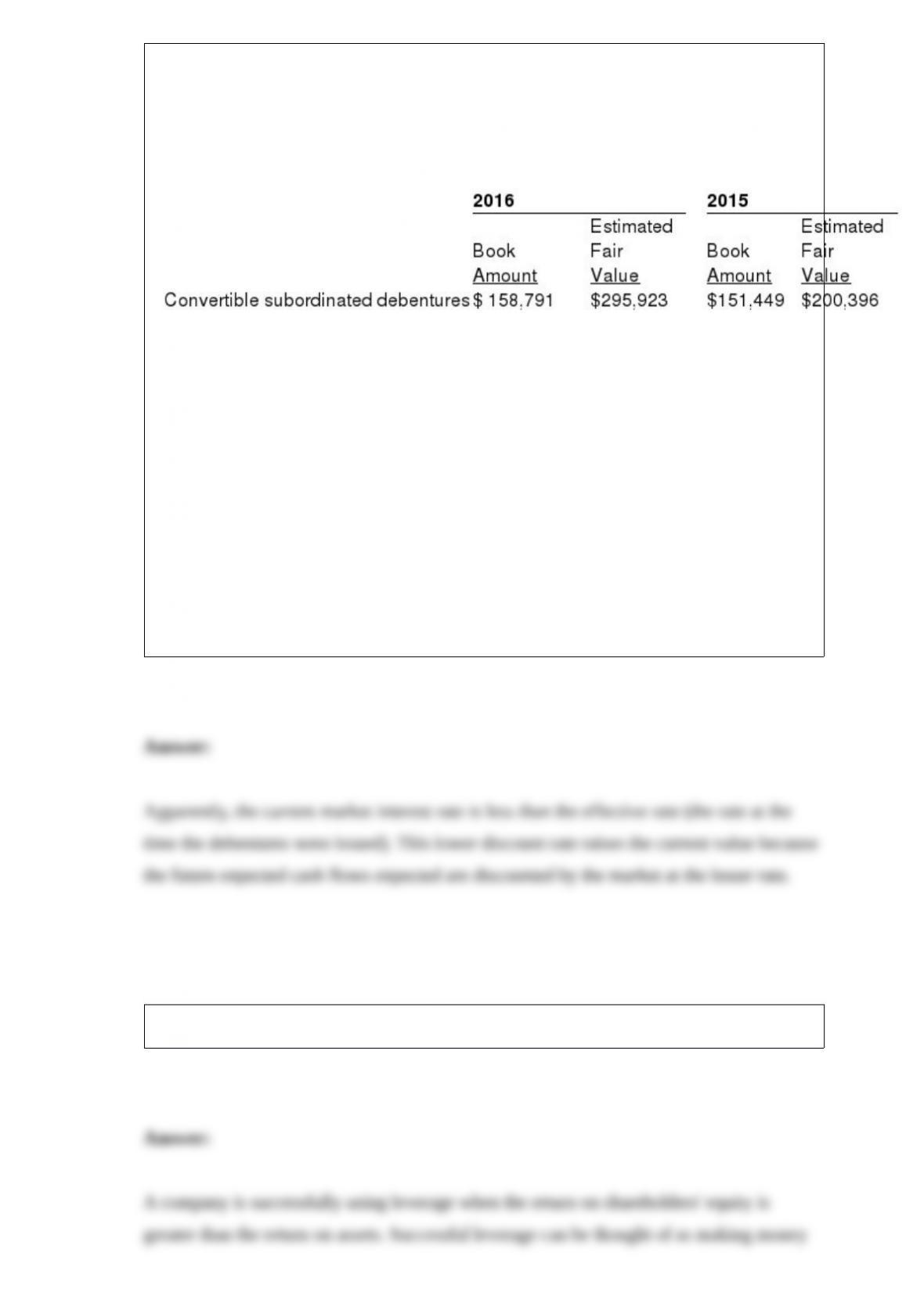

In its 2016 annual report to shareholders, Health Foods, Inc., disclosed the following

information about some of its indebtedness: The fair value of convertible subordinated

debentures is estimated using quoted market prices. Book amounts and estimated fair

values of our financial instruments other than those for which book amounts

approximate fair values as noted above are as follows (in thousands)

In addition, the company disclosed the following: We have outstanding zero coupon

convertible subordinated debentures which had a book amount of approximately $158.8

million and $151.4 million at September 26, 2016, and September 28, 2015,

respectively. The debentures have an effective yield to maturity of 5 percent and a

principal amount at maturity on March 2, 2030, of approximately $308.8 million. The

debentures are convertible at the option of the holder, at any time on or prior to

maturity, unless previously redeemed or otherwise purchased. The debentures have a

conversion rate of 10.64 shares per $1,000 principal amount at maturity, representing

3,285,632 shares. The debentures may be redeemed at the option of the holder on

March 2, 2020, or March 2, 2025, at the issue price plus accrued original discount

totaling approximately $188 million and $241 million, respectively.

Required: Explain why the estimated fair value of the debentures exceeds their book

amount at the end of fiscal year 2016.

Briefly explain how you can determine if a company is effectively using leverage.

On January 1, 2016, Whittington Stoves issued $800 million of its 8% bonds for $736

million. The bonds were priced to yield 10%. Interest is payable semiannually on June

30 and December 31. Whittington records interest at the effective rate and elected the

option to report these bonds at their fair value. One million dollars of the increase in fair

value was due to a change in the general (risk-free) rate of interest. On December 31,

2016, the fair value of the bonds was $752 million as determined by their market value

on the NYSE. Required:

1> Prepare the journal entry to record interest on June 30, 2016 (the first interest

payment).

2> Prepare the journal entry to record interest on December 31, 2016 (the second

interest payment).

3> Prepare the journal entry to adjust the bonds to their fair value for presentation in the

December 31, 2016, balance sheet.

Why did the loss result in a reduction in accumulated other comprehensive income?

M, Inc., supplies consumer products used in the United States and other markets. In its

2016 Annual Report to Shareholders, M, Inc., disclosed the following note about its

EPS:

Basic earnings per share are computed using the weighted average number of common

shares outstanding during the period. Diluted earnings per common share incorporate

the incremental shares issuable upon the assumed exercise of stock options and upon

the assumed conversion of the Company’s Convertible Notes in fiscal 2016 as if

conversion to common shares had occurred at the beginning of the fiscal year. Earnings

have also been adjusted for interest expense on the Convertible Notes in fiscal 2016.

Explain why M mentioned the adjustment in the last sentence of the disclosure note.

Texon Oil is being sued for price fixing and environmental damage. The litigation

started this year and is expected to last five years. There is no doubt that Texon is guilty,

but the settlement cost will be between $3 billion and $22 billion. Briefly explain how

Texon would address this in its current year financial statements.

How are customer advances and refundable deposits similar and yet different?

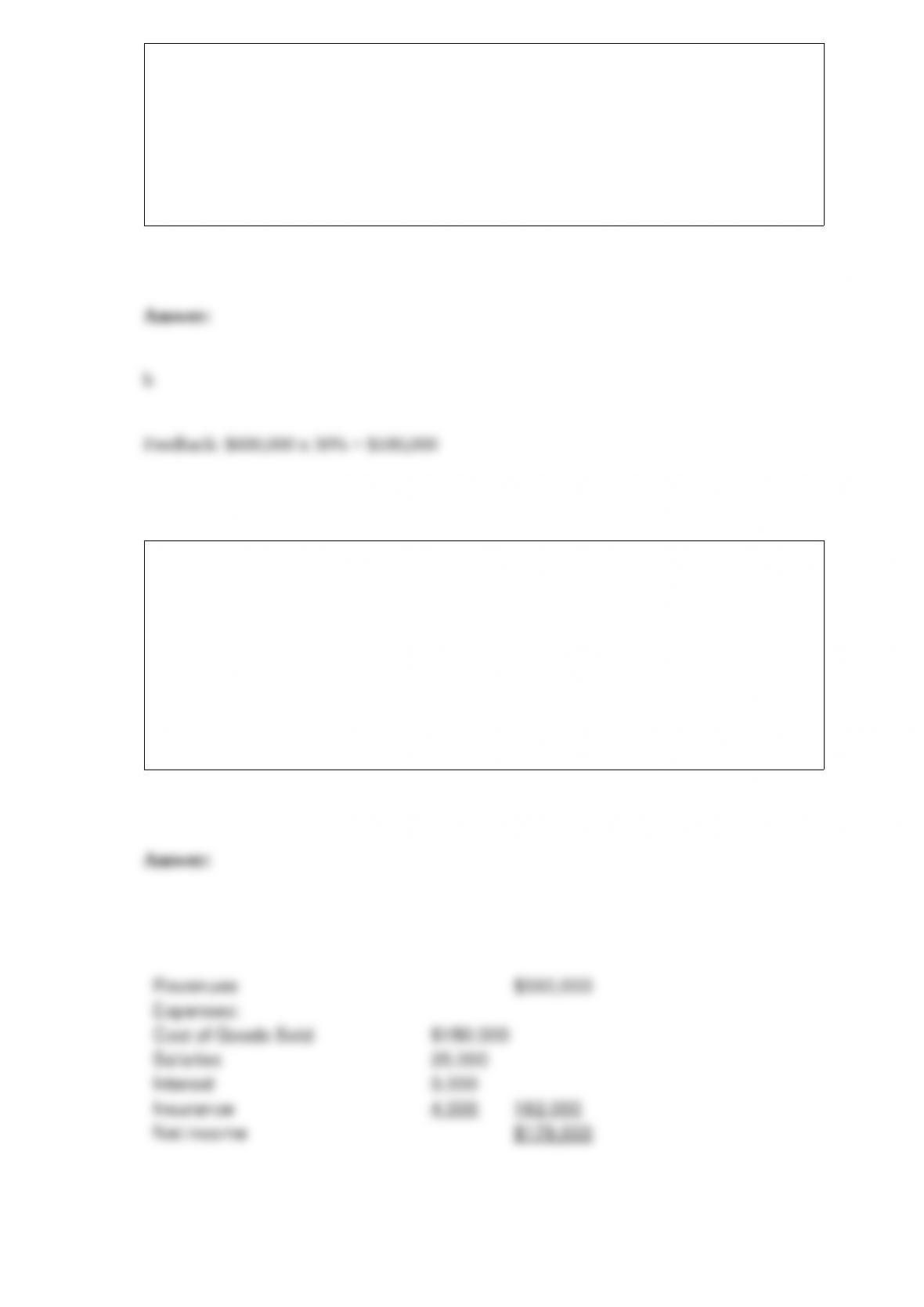

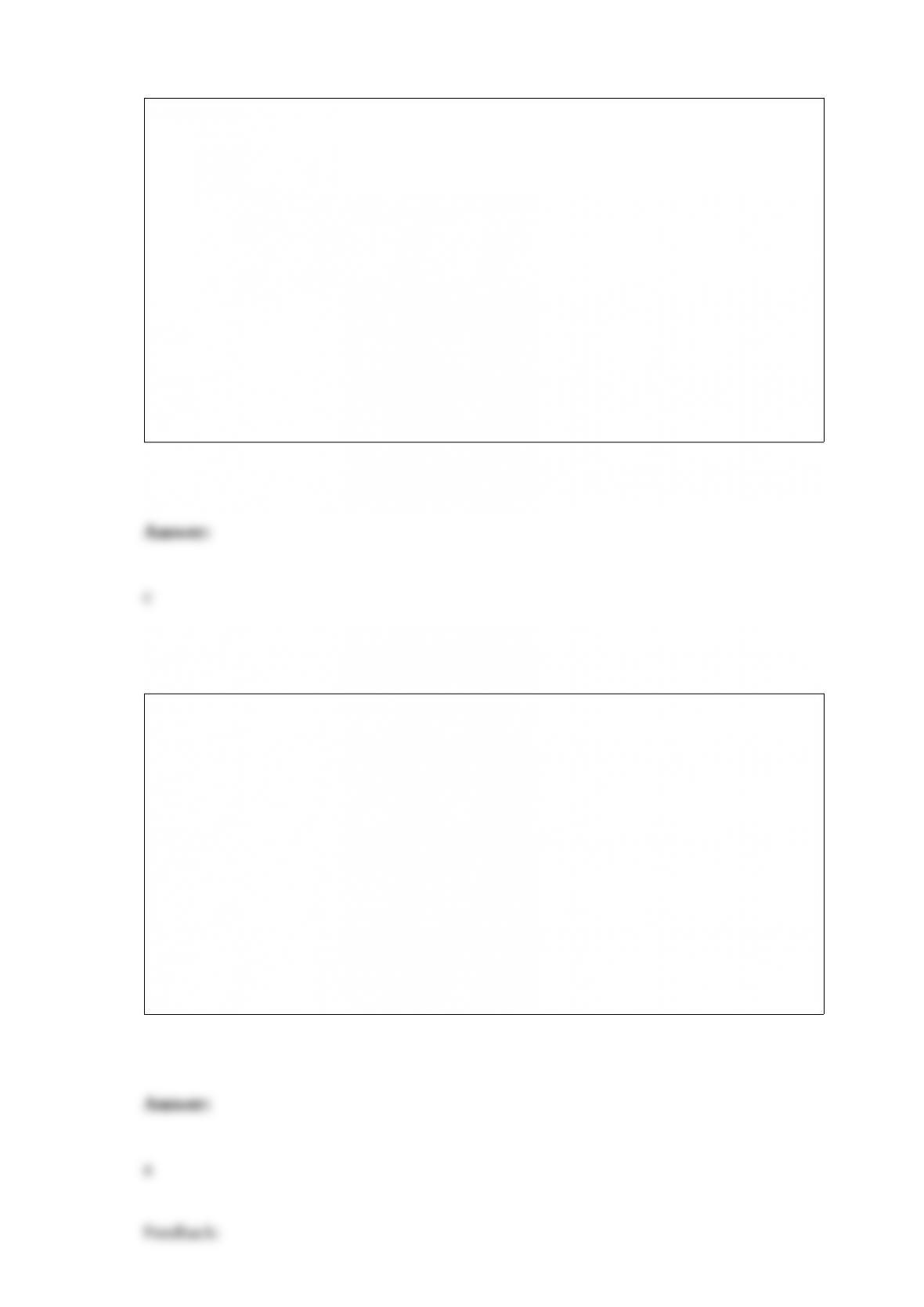

Ellen’s Antiques reported the following in its December 31, 2016, balance sheet:

In a disclosure note, Ellen’s indicates that it uses straight-line depreciation over eight

years and estimates salvage value at 10% of cost.

Required: Compute the average age of Ellen’s equipment at 12/31/2015.