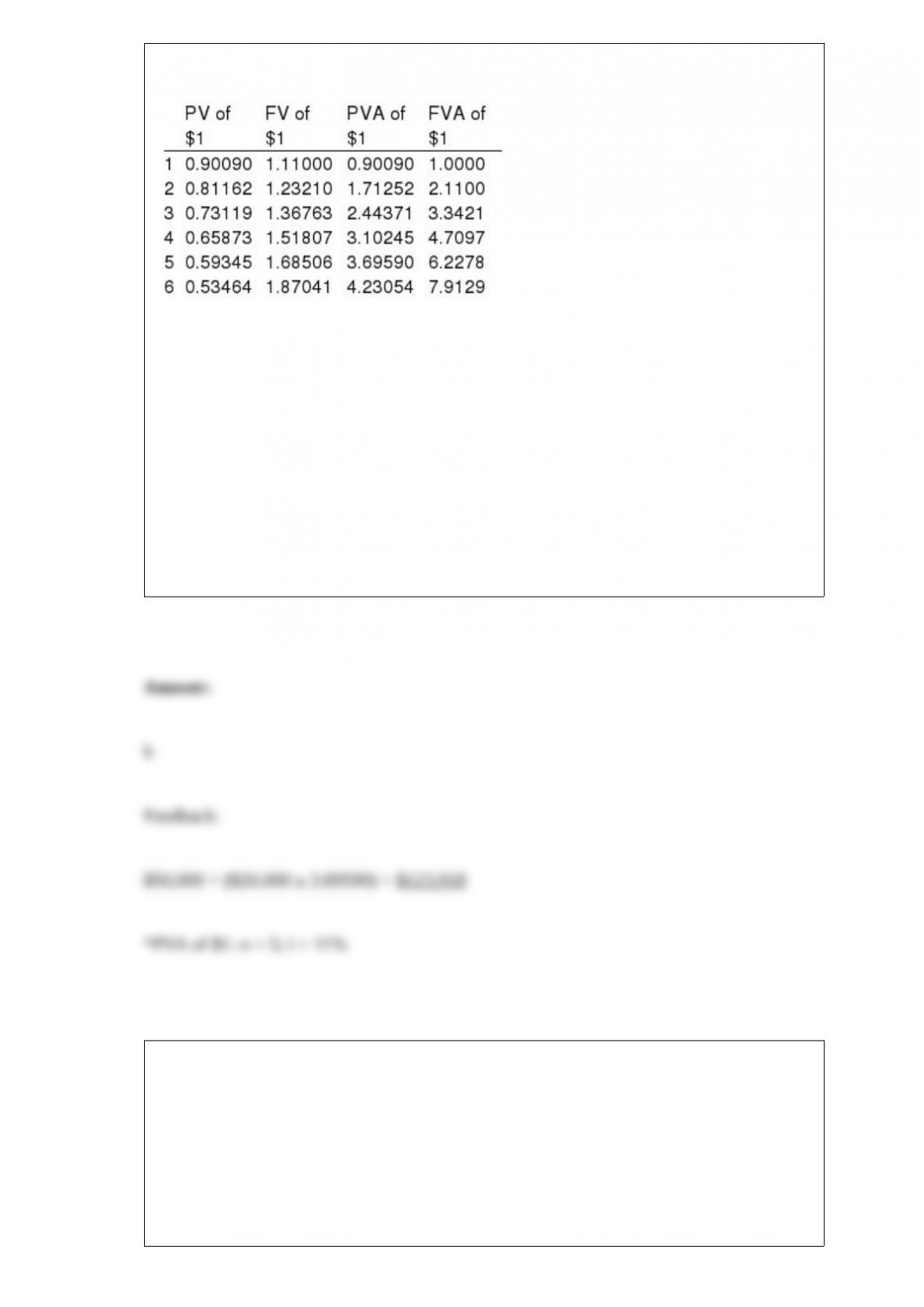

Present and future value tables of 1 at 11% are presented below.

Polo Publishers purchased a multi-color offset press with terms of $50,000 down and a

noninterest-bearing note requiring payment of $20,000 at the end of each year for five

years. The interest rate implicit in the purchase contract is 11%. Polo would record the

asset at:

a. $73,918.

b. $123,918.

c. $130,000.

d. $169,560.

The amount of impairment loss is the excess of book value over:

a. Amortized cost.

b. Undiscounted future cash flows.

c. Fair value.

d. Future revenues.

On January 31, 2016, B Corp. issued $600,000 face value, 12% bonds for $600,000

cash. The bonds are dated December 31, 2015, and mature on December 31, 2025.

Interest will be paid semiannually on June 30 and December 31. What amount of

accrued interest payable should B report in its September 30, 2016, balance sheet?

a. $18,000.

b. $36,000.

c. $54,000.

d. $48,000.

When a company sells land for cash and recognizes a $25,000 gain:

a. Its acid-test ratio decreases.

b. Its current ratio decreases.

c. Its debt to equity ratio decreases.

d. Cannot determine from the given information.

Pro forma earnings:

a. Could be considered management’s view of permanent earnings.

b. Are needed for the correction of errors.

c. Are standardized under generally accepted accounting principles

d. Are useful to compare two different firms’ performance.

The FASB issues accounting standards in the form of:

a. Accounting Research Bulletins.

b. Accounting Standards Updates.

c. Financial Accounting Standards.

d. Financial Technical Bulletins.

Rent collected in advance is:

a. An asset account in the balance sheet.

b. A liability account in the balance sheet.

c. A shareholders’ equity account in the balance sheet.

d. A temporary account, not in the balance sheet at all.

Which of the following is not included among the assumptions needed to estimate

postretirement health care benefits?

a. Employee turnover.

b. Expected retirement age of plan participants.

c. Life expectancy of plan participants.

d. Return on plan assets.

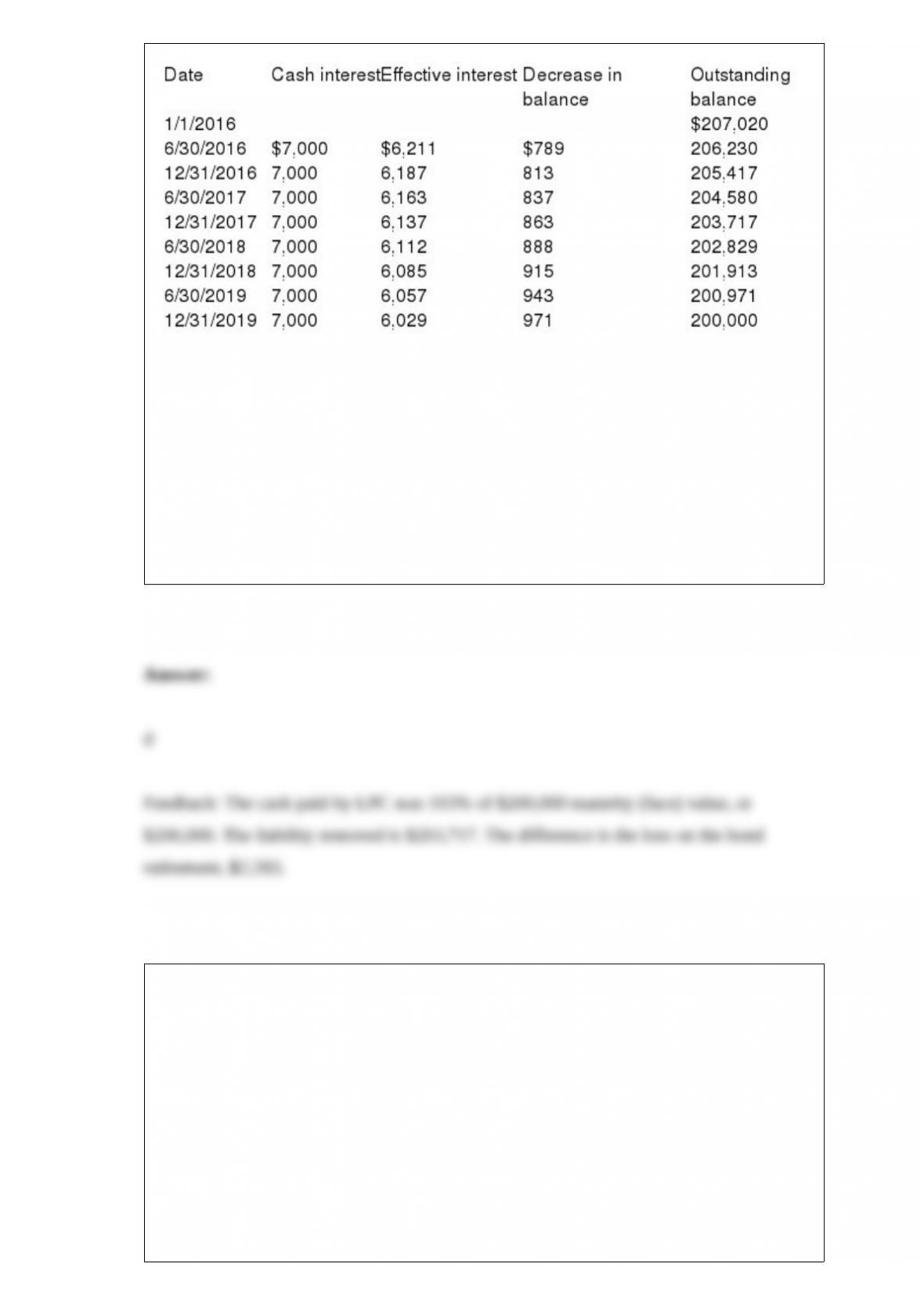

Lopez Plastics Co. (LPC) issued callable bonds on January 1, 2016. LPC’s accountant

has projected the following amortization schedule from issuance until maturity:

LPC calls the bonds at 103 immediately after the interest payment on 12/31/2017 and

retires them. What gain or loss, if any, would LPC record on this date?

a. No gain or loss

b. $3,717 gain

c. $6,000 loss

d. $2,283 loss

On January 1, 2016, G Corp. granted stock options to key employees for the purchase

of 80,000 shares of the company’s common stock at $25 per share. The options are

intended to compensate employees for the next two years. The options are exercisable

within a four-year period beginning January 1, 2018, by the grantees still in the employ

of the company. No options were terminated during 2016, but the company does have

an experience of 4% forfeitures over the life of the stock options. The market price of

the common stock was $31 per share at the date of the grant. G Corp. used the Binomial

pricing model and estimated the fair value of each of the options at $10. What amount

should G charge to compensation expense for the year ended December 31, 2016?

a. $307,200.

b. $320,000.

c. $384,000.

d. $400,000.

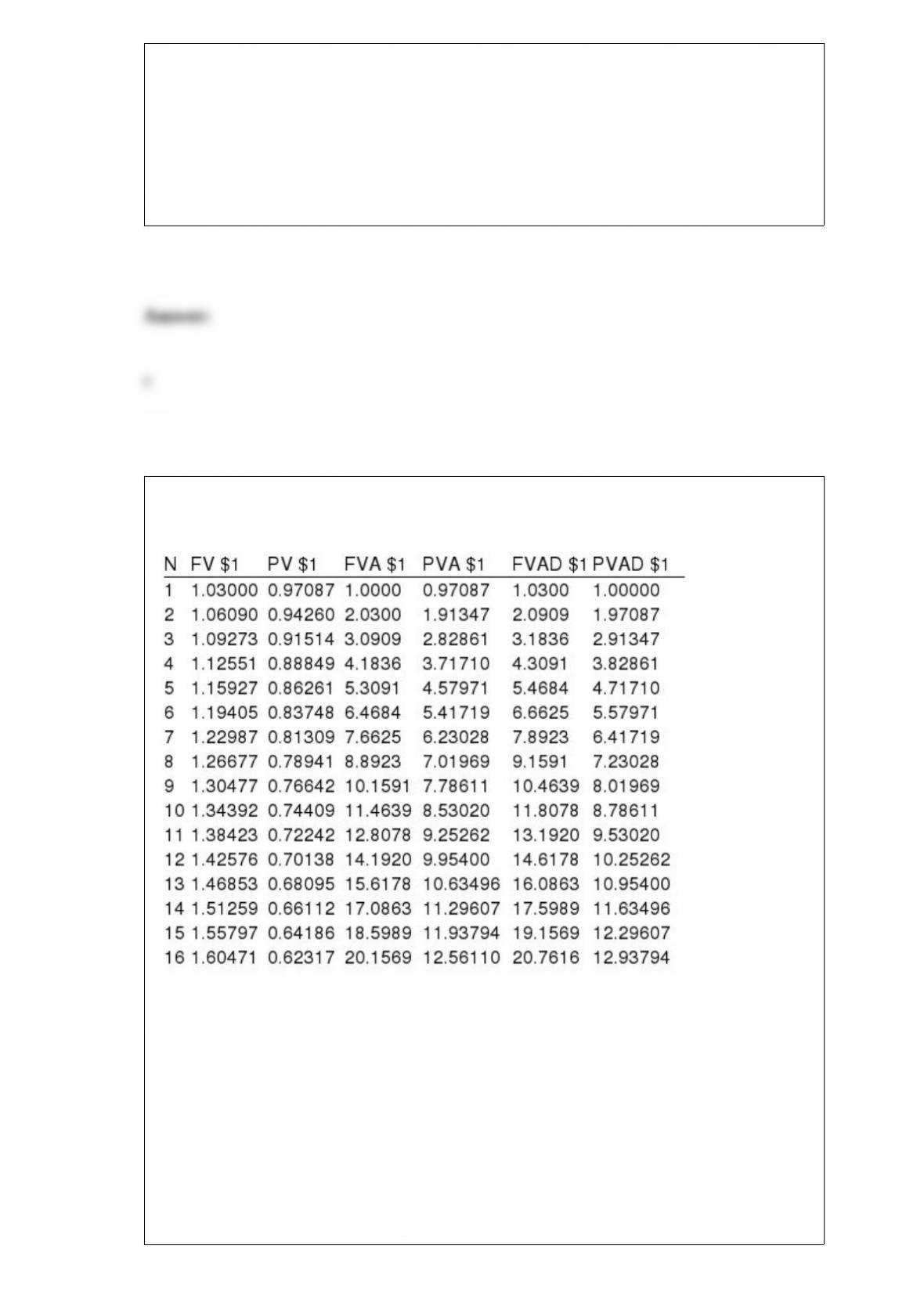

Present and future value tables of $1 at 3% are presented below:

Carol wants to invest money in a 6% CD account that compounds semiannually. Carol

would like the account to have a balance of $50,000 five years from now. How much

must Carol deposit to accomplish her goal?

a. $35,069.

b. $43,131.

c. $37,220.

d. $35,000.

Cutter Enterprises purchased equipment for $72,000 on January 1, 2016. The equipment

is expected to have a five-year life and a residual value of $6,000. Using the

double-declining balance method, the book value at December 31, 2017, would be:

a. $14,400.

b. $24,960.

c. $27,360.

d. $25,920.

What is the stated annual rate of interest on the bonds?

a. 3%.

b. 4%.

c. 6%.

d. 8%.

a) What non-accounting factors are important before evaluating whether a pending

lawsuit should be accrued as a liability and reflected in the financial statements?

b) What accounting factors should be considered in determining whether a pending

lawsuit should be accrued as a liability and reflected in the financial statements?

Distinguish between:

(a) Secured and unsecured bonds.

(b) Coupon and registered bonds.

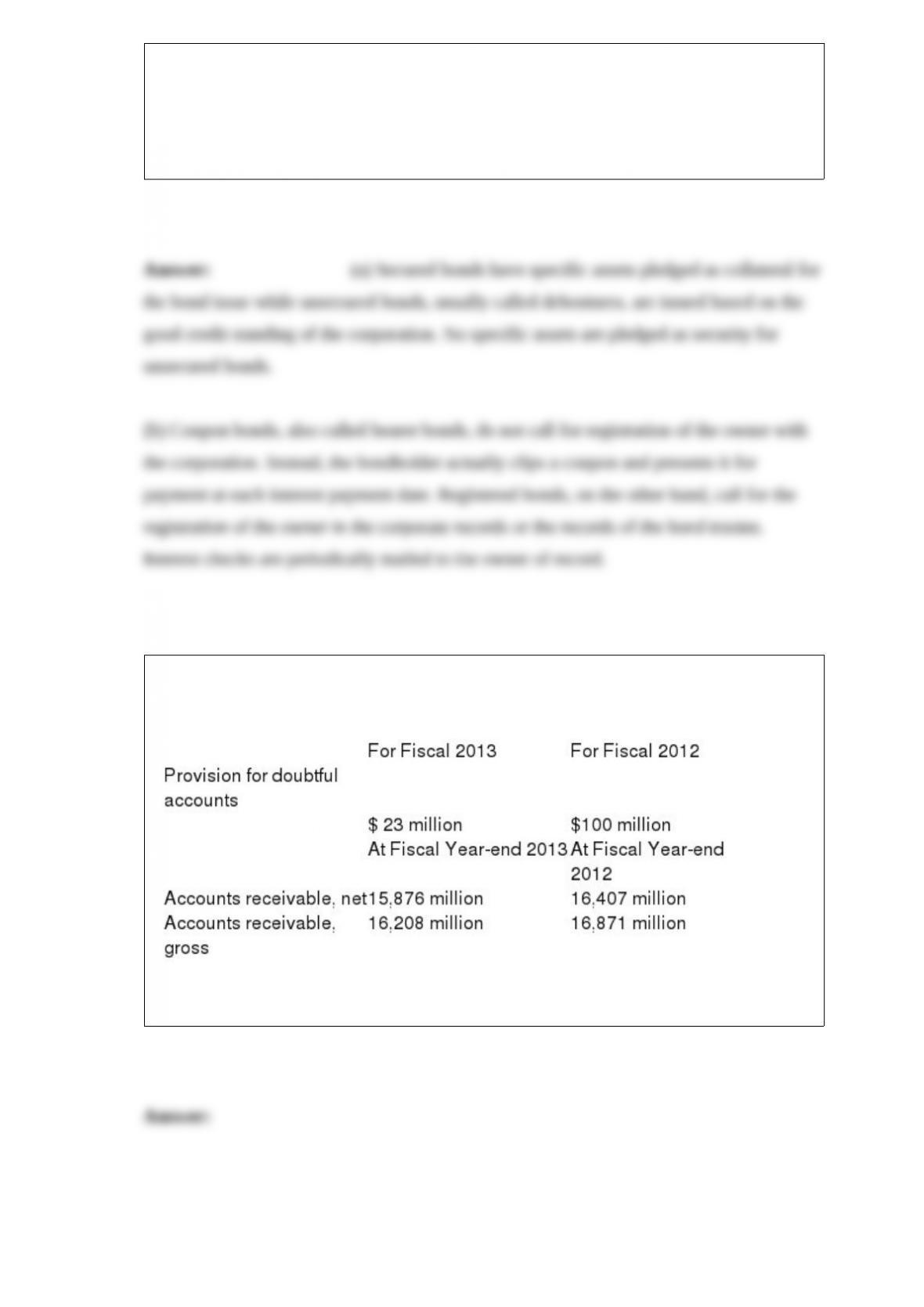

The following information is taken from the 2013 annual report to shareholders of

Hewlett-Packard (HP) Co.

Using a T-account for the allowance for doubtful accounts, identify the changes in the

account during fiscal year 2013.

What provisions did the Public Company Accounting Reform and Investor Protection

(Sarbanes-Oxley) Act of 2002 make for performance of nonaudit services by an audit

firm?

Optimus Pools, Inc. constructs outdoor swimming pools for wealthy individuals.

Recently it obtained an order to build a three-lane swimming pool of 25 yards in length

in the customer’s backyard. Under the contract, Optimus is also obligated to install a

water heater and a filtration system, which are necessary to make a swimming pool

fully functional. Total price for the construction was $55,000. Each of these smaller

components would typically cost $40,000, $10,000, and 20,000 if installed separately.

Required: Given the information above, how many performance obligations are

included in this contract?

Assuming that Composition had Dividends Payable of $17,450 thousand at December

31, 2014, compute the balance in that account at December 31, 2016.

How do U.S. GAAP and International Financial Reporting Standards (IFRS) differ with

respect to debt and equity for preferred stock?

Listed below are five terms followed by a list of phrases that describe or characterize

each of the terms. Match each phrase with the number for the correct term.

Give an example of a violation of the stable monetary unit assumption. How would it

affect the quality of financial statement information?

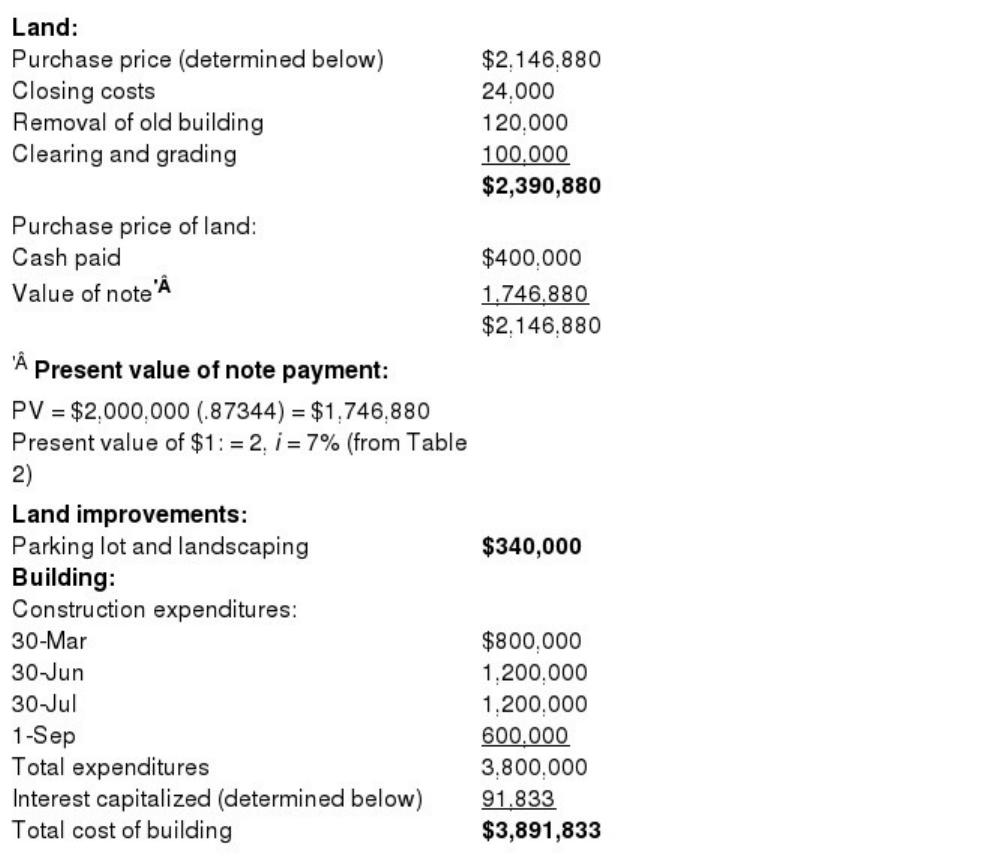

On January 3, 2016, Michelson & Sons acquired a tract of land just outside the city

limits. The land and existing building were purchased for $2.4 million. Michelson paid

$400,000 and signed a noninterest-bearing note requiring the company to pay the

remaining $2,000,000 on December 31, 2017. An interest rate of 7% properly reflects

the time value of money for this type of loan agreement. Transfer taxes, title insurance,

and other costs totaling $24,000 were paid at closing.

During February, the old building was demolished at a cost of $120,000, and an

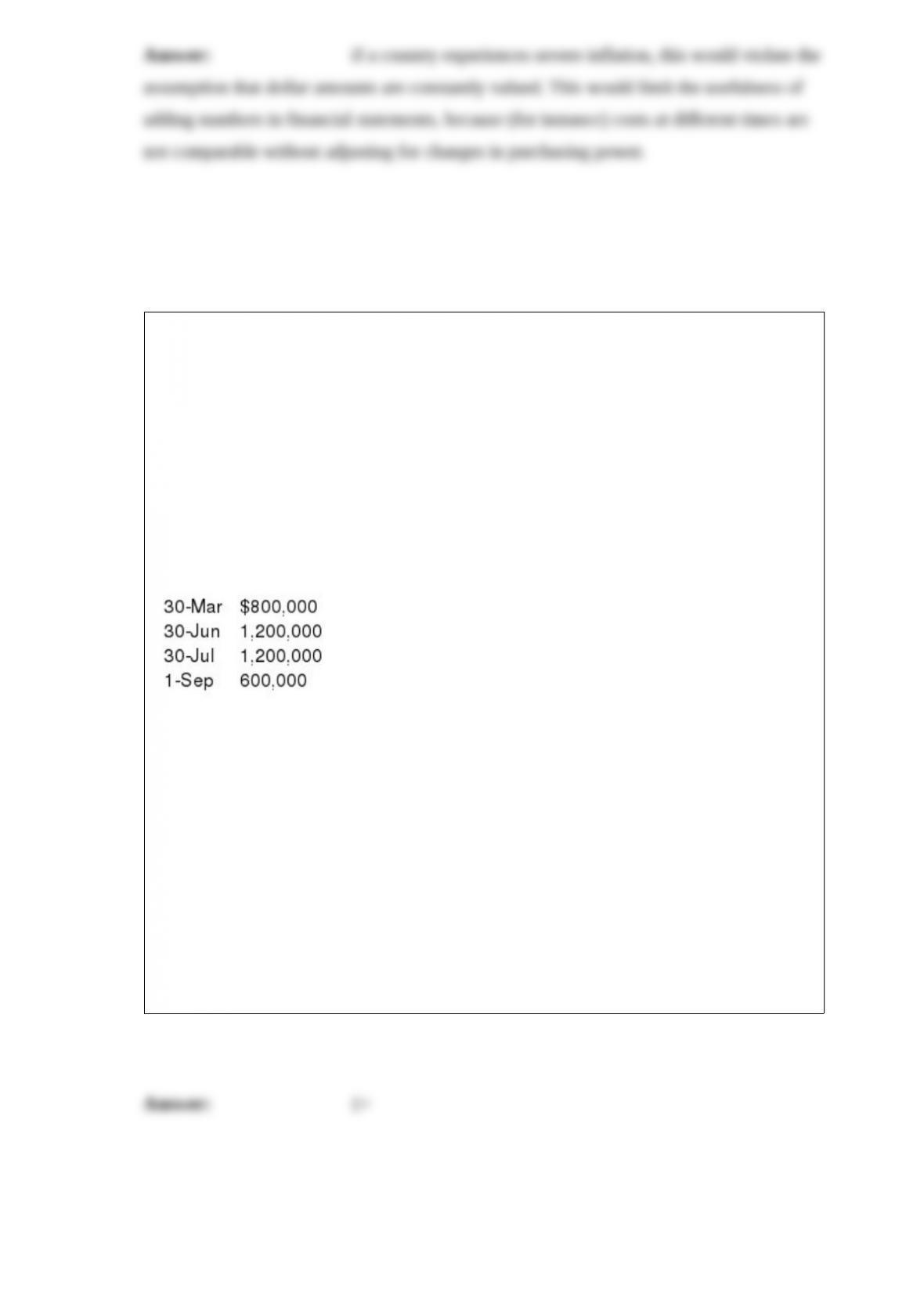

additional $100,000 was paid to clear and grade the land. Construction of a new

building began on March 1 and was completed on October 30. Construction

expenditures were as follows:

Michelson did not borrow specifically for the construction project, but did have the

following debt outstanding throughout 2016: $6,000,000, 8% long-term note payable

$2,000,000, 5% long-term note payable In December, the company purchased

equipment and office furniture and fixtures for a lump-sum price of $800,000. The fair

values of the equipment and the furniture and fixtures were $540,000 and $360,000,

respectively. In December, Michelson paid $340,000 for the construction of parking lots

and landscaping.Required:

1> Determine the initial values of the various assets that Michelson acquired or

constructed during 2016.

2> How much interest expense will Michelson report in its 2016 income statement?

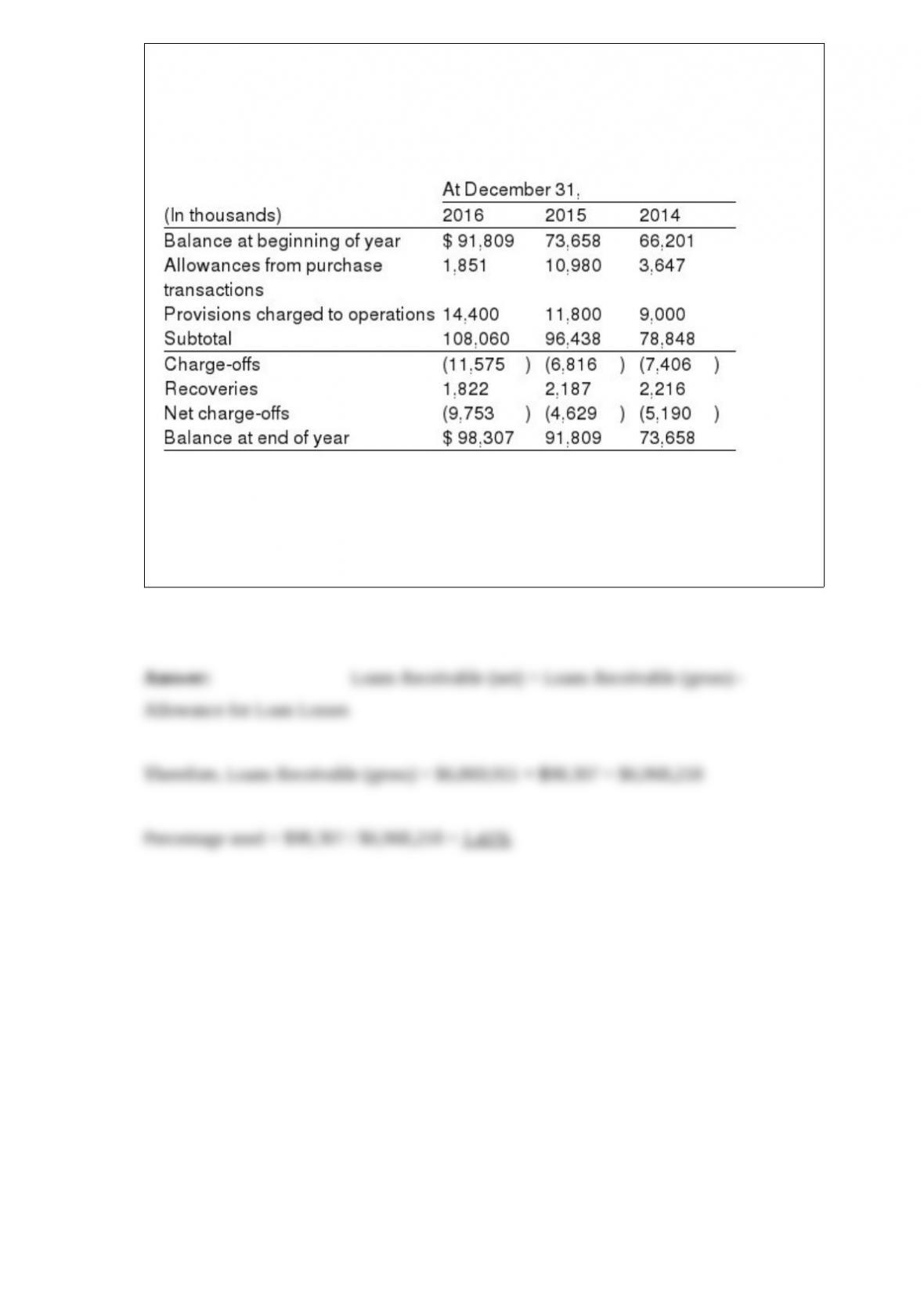

The following note disclosure is taken from the 2016 annual report to shareholders of

Winchester International Corporation. NOTE 5: ALLOWANCE FOR LOAN LOSSES

The allowance for loan loss is maintained at a level to absorb probable losses inherent

in the loan portfolio. This allowance is increased by provisions charged to operating

expense and by recoveries on loans previously charged off, and reduced by charge-offs

on loans. The following is a summary of the changes in the allowances for loan losses

for three years:

Winchester also reported (in thousands) in its comparative balance sheet that it held

Loans receivable, net, of $6,869,911 and $6,819,209 at December 31, 2016, and

December 31, 2015, respectively. If Winchester is using the balance sheet approach to

determining loan losses and the Allowance account balance, what percentage did it use

in 2016?