1) Pahm Corporation owns 80% of the outstanding voting common stock of Abussi

Corporation, which was purchased for $60,000 over Abussi’s book value. The excess

purchase price was attributable to goodwill. Abussi Corporation owns 60% of the

outstanding common stock of Badock Corporation, which was purchased at book value.

The separate net incomes of Pahm, Abussi, and Badock (excluding investment income)

for the year are $200,000, $240,000, and $260,000, respectively. There were no fair

value/book value differences in the assets and liabilities of Pahm, Abussi and Badock.

Controlling interest share of consolidated net income for the current year is

A) $504,800

B) $516,800

C) $545,200

D) $557,200

2) On January 1, 2011, Pamplin Corporation stockholders’ equity consisted of

$1,000,000 of $10 par value Common Stock, $750,000 of Additional Paid-in Capital,

and $3,000,000 of Retained Earnings. On January 1, 2011, Pamplin purchased 90% of

the outstanding common stock of Sage Corporation for $1,500,000 with all excess

purchase cost assigned to goodwill. The stockholders’ equity of Sage on this date

consisted of $800,000 of $100 par value, 8% cumulative, preferred stock callable at

$105, $900,000 of $10 par value common stock and $500,000 of Retained Earnings.

Sage’s net income for 2011 was $100,000.

On January 1, 2011, no preferred dividends are in arrears. No dividends are declared or

paid in 2011 . In a separate transaction on January 1, 2011, Pamplin purchased 70% of

Sage’s preferred stock for $600,000.

For the year ending December 31, 2011, the amount of Pamplin’s income from Sage

(associated with the common stock investment in Sage) is

A) $32,400

B) $36,000

C) $60,000

D) $90,000

3) The estimated taxable income for Shebill Corporation on January 1, 2011, was

$80,000, $100,000, $100,000, and $120,000, respectively, for each of the four quarters

of 2011 . Shebill’s estimated annual effective tax rate was 30%. During the second

quarter of 2011, the estimated annual effective tax rate was increased to 34%. Given

only this information, Shebill’s second quarter income tax expense was

A) $30,000

B) $34,000

C) $37,200

D) $61,200

4) Which of the following statements are true?

A) A decrease in default risk on corporate bonds lowers the demand for these bonds, but

increases the demand for default-free bonds

B) The expected return on corporate bonds decreases as default risk increases

C) A corporate bond’s return becomes less uncertain as default risk increases

D) As their relative riskiness increases, the expected return on corporate bonds

increases relative to the expected return on default-free bonds

5) According to the liquidity premium theory of the term structure, a flat yield curve

indicates that short-term interest rates are expected to

A) rise in the future

B) remain unchanged in the future

C) decline moderately in the future

D) decline sharply in the future

6) What is the document prepared by the executor or administrator to show

accountability for estate property received and maintained or disbursed in accordance

with the will?

A) The Administrator/Executor’s Fiduciary Report

B) The charge-discharge statement

C) The Administrator/Executor’s Testamentary Report

D) The Administrator/Executor’s Principal/Income Report

7) Bonds with no default risk are called

A) flower bonds

B) no-risk bonds

C) default-free bonds

D) zero-risk bonds

8) Pfadt Inc. had $600,000 par of 8% bonds payable outstanding on January 1, 2011 due

January 1, 2015 with an unamortized discount of $12,000. Senat is a 90%-owned

subsidiary of Pfadt. On January 2, 2011, Senat Corporation purchased $150,000 par

value of Pfadt’s outstanding bonds for $152,000. The bonds have interest payment dates

of January 1 and July 1 . Straight-line amortization is used.

Bonds Payable appeared in the December 31, 2011 consolidated balance sheet of Pfadt

Corporation and Subsidiary in the amount of

A) $398,925

B) $441,000

C) $443,250

D) $450,000

9) A ________ yield curve predicts a future increase in inflation

A) steeply upward sloping

B) slight upward sloping

C) flat

D) downward sloping

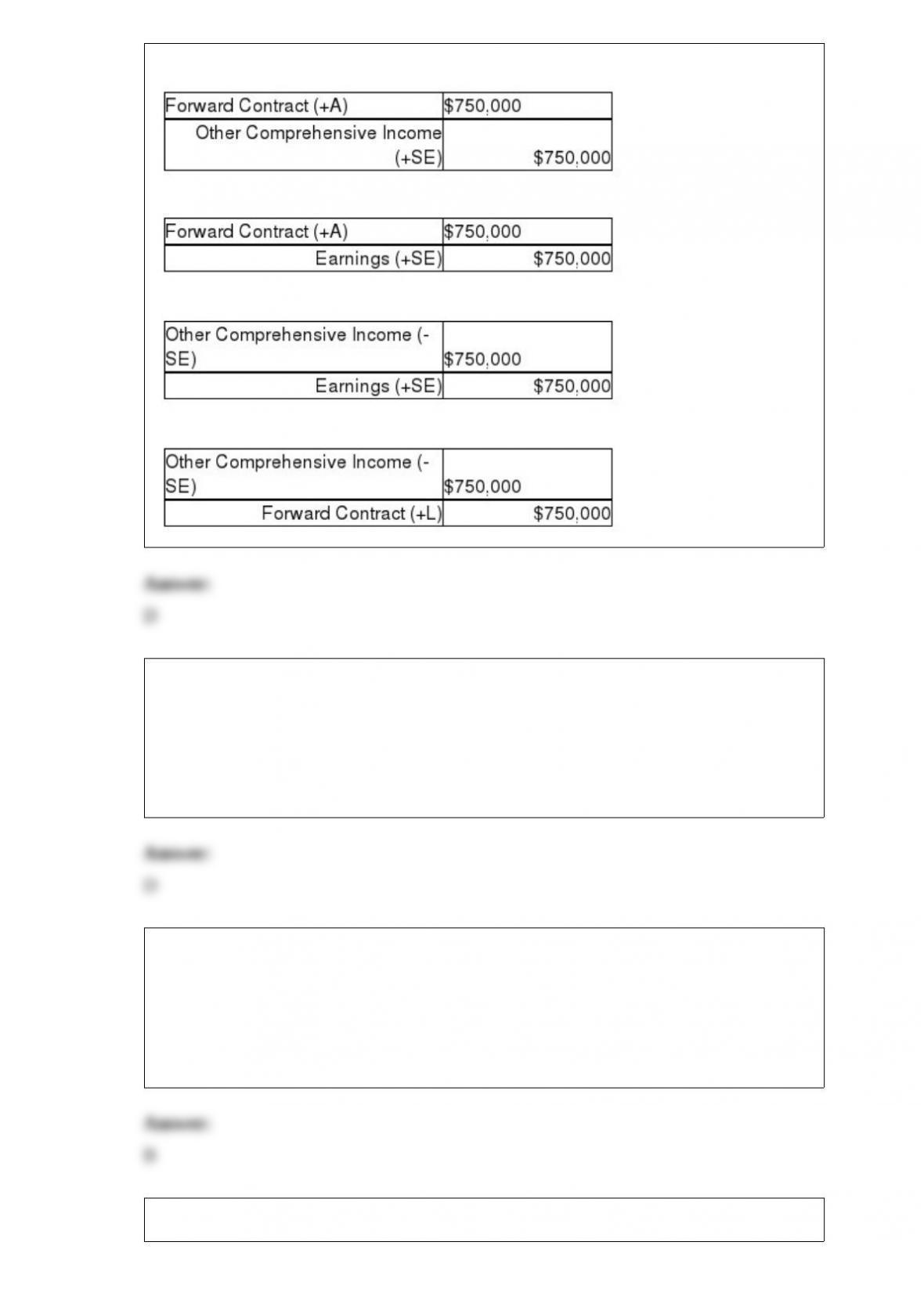

10) Barnes Company entered into a forward contract during the current year to hedge

the risk of a material supply cost increase. Based on the current market, at year-end the

present value of the estimated amount they will have to pay in ten months is $750,000.

What entry would be recorded at year-end closing, assuming that no amount was

recorded for this contract until this time?

A)

B)

C)

D)

11) A(n) ________ sale is a sale by a parent company to a subsidiary. A(n) ________

sale is a sale by a subsidiary to a parent company.

A) deferred; realized

B) realized; deferred

C) upstream; downstream

D) downstream; upstream

12) A simple partnership liquidation requires

A) periodic payments to creditors and partners determined by a safe payments schedule

B) partnership assets to be converted into cash with full payment made to all outside

creditors before remaining cash is distributed to partners

C) only creditors to be paid in an orderly manner

D) periodic payments to partners as cash becomes available

13) Polka Corporation exchanges 100,000 shares of newly issued $1 par value common

stock with a fair market value of $20 per share for all of the outstanding $5 par value

common stock of Spot Inc. and Spot is then dissolved. Polka paid the following costs

and expenses related to the business combination:

Costs of special shareholders’ meeting

to vote on the merger$12,000

Registering and issuing securities10,000

Accounting and legal fees18,000

Salaries of Polka’s employees assigned

to the implementation of the merger27,000

Cost of closing duplicate facilities13,000

In the business combination of Polka and Spot,

A) all of the items listed above are treated as expenses

B) all of the items listed above except the cost of registering and issuing the securities

are included in the purchase price

C) the costs of registering and issuing the securities are deducted from the fair market

value of the common stock used to acquire Spot

D) only the costs of closing duplicate facilities, the salaries of Polka’s employees

assigned to the merger, and the costs of the shareholders’ meeting would be treated as

expenses

14) In 2011, Parla Corporation sold land to its subsidiary, Sidd Corporation, for

$38,000. It had a book value of $24,000. In the next year, Sidd sold the land for

$41,000 to an unaffiliated firm.

Which of the following is correct?

A) No consolidation working paper entry is required for this transaction in 2011

B) A consolidation working paper entry is required only if the subsidiary was less than

100% owned in 2011

C) A consolidation working paper entry is required each year that Sidd has the land

D) A consolidated working paper entry was required only if the land was held for resale

in 2011

15) Saveed Corporation purchased the net assets of Penny Inc. on January 2, 2011 for

$1,690,000 cash and also paid $15,000 in direct acquisition costs. Penny dissolved as of

the date of the acquisition. Penny’s balance sheet on January 2, 2011 was as follows:

Accounts receivable-net$190,000Current liabilities$235,000

Inventory480,000Long term debt650,000

Land10,000Common stock ($1 par)25,000

Building-net630,000Paid-in capital150,000

Equipment-net 240,000Retained earnings 590,000

Total assets$1,650,000Total liab. & equity $1,650,000

Fair values agree with book values except for inventory, land, and equipment, which

have fair values of $640,000, $140,000 and $230,000, respectively. Penny has customer

contracts valued at $20,000.

Required:

Prepare Saveed’s general journal entry for the cash purchase of Penny’s net assets.

16) At December 31, 2010, the stockholders’ equity of Pearson Corporation and its

80%-owned subsidiary, Trompeter Corporation, are as follows:

PearsonTrompeter

Common stock, $10 par value$20,000$12,000

Retained earnings8,0006,000

Totals$28,000$18,000

Pearson’s Investment in Trompeter is equal to 80 percent of Trompeter’s book value.

Trompeter Corporation issued 400 additional shares of common stock directly to

Pearson on January 1, 2011 at $10 per share.

Required:

1> Compute the balance in Pearson’s Investment in Trompeter account on January 1,

2011 after the new investment is recorded.

2> Determine the increase or decrease in goodwill from Pearson’s new investment in

the 400 Trompeter shares. Use four decimal places for the ownership percentage.

Assume the fair value and book value of Trompeter’s assets and liabilities are equal.

17) Phauna paid $120,000 for its 80% interest in Schrub on January 1, 2009 when

Schrub had $150,000 of total stockholders’ equity.

On January 1, 2012, Phauna purchased $50,000 of Schrub Corporation’s 8% bonds for

$48,000. At that time, $100,000 of bonds had been issued by Schrub, and unamortized

premium was $2,000. The bonds pay interest on June 30 and December 31 and mature

on December 31, 2016. Both Phauna and Schrub use straight-line amortization. Phauna

uses the equity method of accounting for its investment in Schrub.

Required:

Prepare eliminating/adjusting entries for the bonds on the consolidating work papers for

the year ended December 31, 2012 .

18) Pastern Industries has an 80% ownership stake in Sascon Incorporated. At the time

of purchase, the book value of Sascon’s assets and liabilities were equal to the fair

value. The cost of the 80% investment was equal to 80% of the book value of Sascon’s

net assets. At the end of 2011, they issued the following consolidated income statement:

Sales$930,000

Cost of sales(470,000)

Operating expenses(202,000)

Noncontrolling interest share(23,000)

Controlling interest share$235,000

Shortly after the statements were issued, Pastern discovered that the 2011 intercompany

sales transactions had not been properly eliminated in consolidation. In fact, Pastern

had sold inventory that cost $80,000 to Sascon for $90,000, and Sascon had sold

inventory that cost $50,000 to Pastern for $65,000. Half of the products from both

transactions still remained in inventory at December 31, 2011 .

Required: Prepare a corrected income statement for Pastern and Subsidiary for 2011 .

19) For internal decision-making purposes, Elom Corporation’s operating segments

have been identified as follows:

Operating

ProfitIdentifiable

Operating SegmentRevenuesor LossAssets

Appliances$110,000$(15,000)$120,000

Lawn and Garden85,00015,00015,000

Auto Accessories100,00010,00020,000

Service Contracts65,000(5,000)10,000

Catalog Sales230,0005,00050,000

Corporate________________25,000

$590,000$10,000$240,000

Corporate assets are typically allocated back evenly to the segments for internal

analysis purposes.

Required:

1> In applying the “asset” test to identify reporting segments, what is the test value for

Elom Corporation?

2> Using the “asset” test, which of Elom’s operating segments will also be reporting

segments?