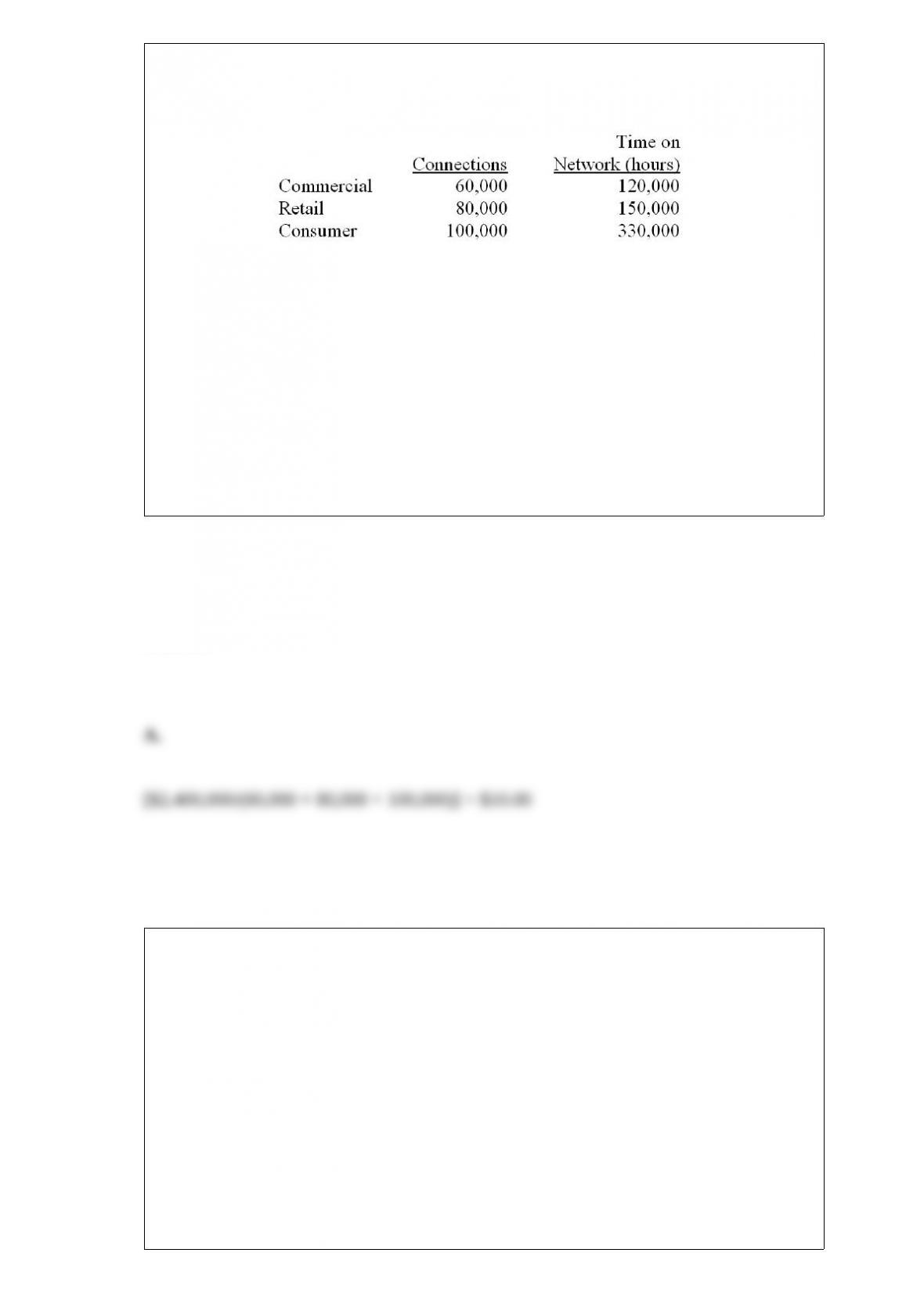

Fenway Telcom has three divisions, commercial, retail and consumer, that share the

common costs of the company’s computer server network. The annual common costs

are $2,400,000. You have been provided with the following information for the

upcoming year:

What is the allocation rate for the upcoming year assuming Fenway Telcom uses the

single-rate method and allocates common costs based on the number of connections?

A. $10.00

B. $15.00

C. $20.00

D. $40.00

Answer:

Which of the following statements regarding quality costs is (are) false?

(A) In a cost of quality system, internal and external failure costs are called

conformance costs.

(B) Prevention costs are costs incurred to detect individual units of product that do not

conform to its specifications.

A. Only A is false.

B. Only B is false.

C. Both A and B are false.

D. Neither A nor B is false.

Answer:

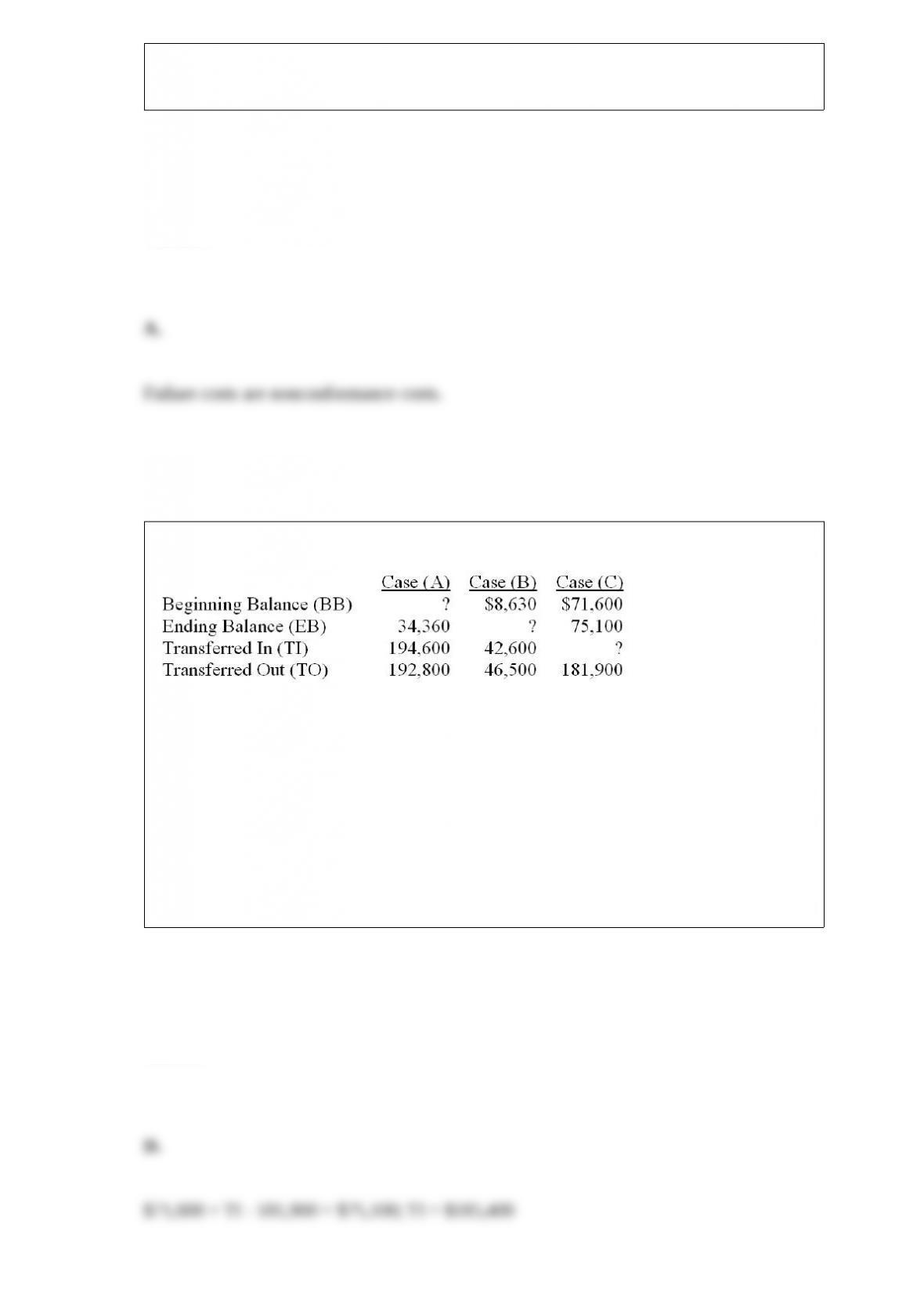

For Case (C) above, what is the Transferred-In (TI)?

A. $146,700

B. $178,400

C. $190,790

D. $185,400

Answer:

Stearns Division can sell externally for $60 per unit. Its variable manufacturing costs

are $35 per unit, and its fixed costs are $12 per unit.

Required:

a) What is the optimal transfer price for transferring internally, assuming the division is

operating at capacity?

b) What is the optimal transfer price for transferring internally, assuming the division is

operating at well below capacity?

Answer:

Which of the following costs are irrelevant for a special order that will allow an

organization to utilize some of its present idle capacity?

A. Direct materials

B. Indirect materials

C. Variable overhead

D. Unavoidable fixed overhead

E. Differential sales commission

Answer:

Which of the following items would not be used as the cost driver for a volume-level

cost in an activity-based cost management (ABM) system?

A. Direct labor hours

B. Machine hours

C. Units produced

D. Square footage

Answer:

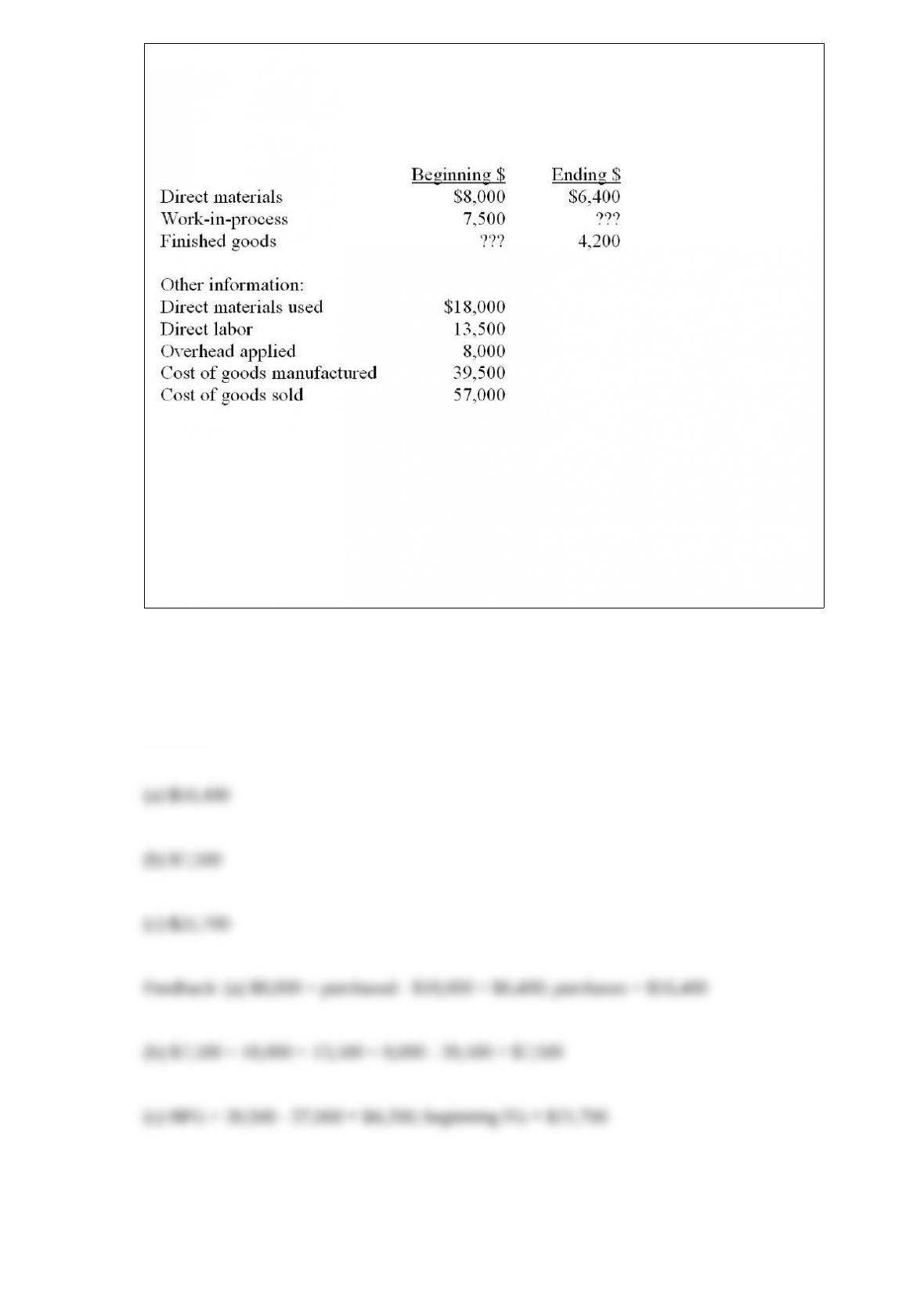

The financial records for the Lee Manufacturing Company have been destroyed in a

flood. The following information has been obtained from a separate set of books

maintained by the cost accountant. The cost accountant now asks for your assistance in

computing the missing amounts.

Required: Compute the following:

(a) direct materials purchased

(b) ending Work-in-process inventory

(c) beginning Finished goods inventory

Answer:

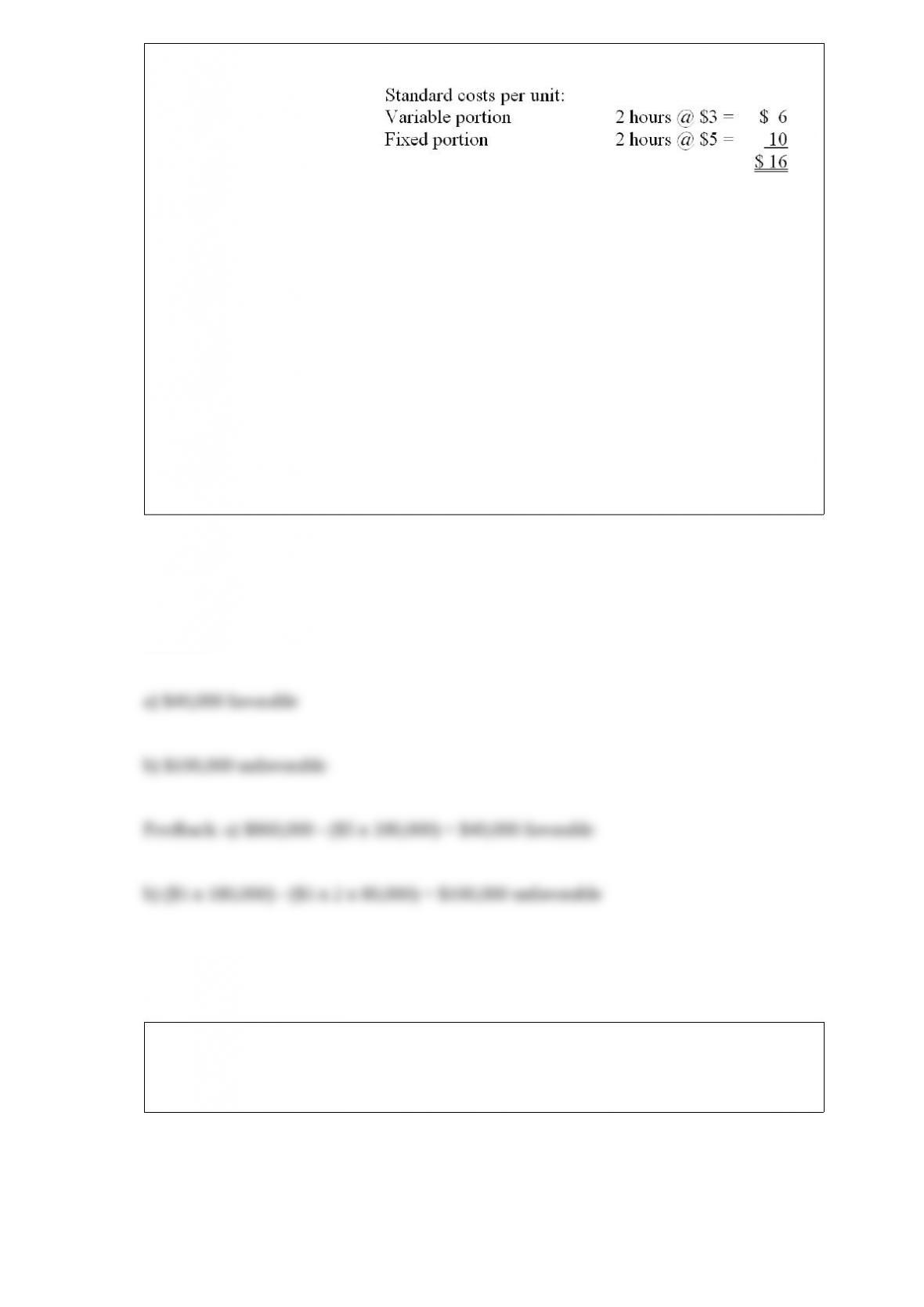

The Standard Company has developed standard overhead costs based upon a capacity

of 180,000 direct labor hours:

During April, 85,000 units were scheduled for production; however, only 80,000 units

were actually produced. The following data relate to April:

Actual direct labor cost incurred was $644,000 for 165,000 actual hours of work.

Actual overhead incurred totaled $1,378,000; $518,000 variable and $860,000 fixed.

All inventories are carried at standard cost.

Required: (Be sure to indicate whether the variances are favorable or unfavorable.)

a) Compute the fixed overhead spending (budget) variance.

b) Compute the production volume variance.

Answer:

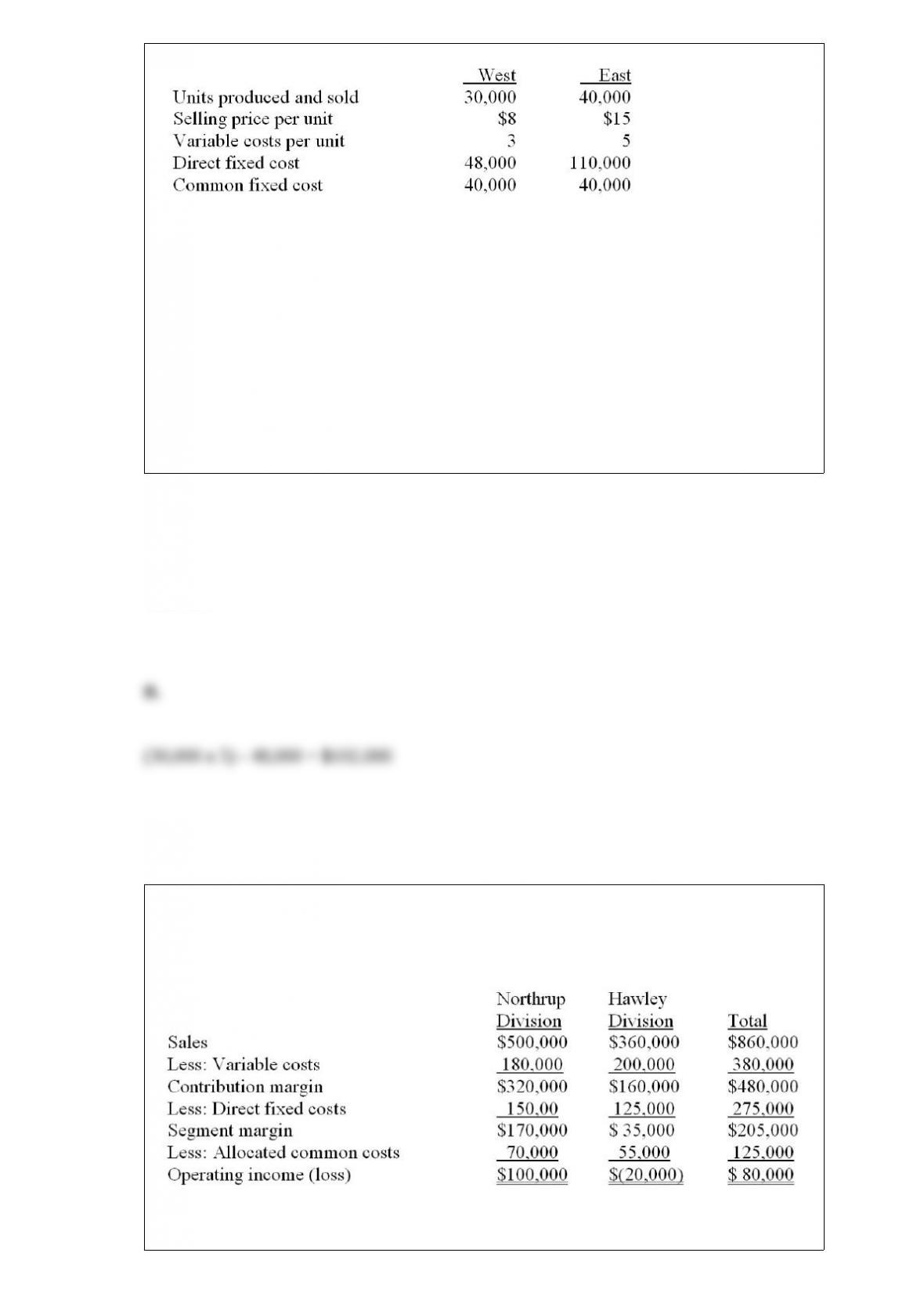

Miller Industries has two divisions: the West Division and the East Division.

Information relating to the divisions for the year just ended is as follows:

Common fixed expenses have been allocated equally to each of the two divisions.

Miller’s segment margin for the West Division is

A. $150,000

B. $102,000

C. $30,000

D. $110,000

Answer:

The operations of Superior Corporation are divided into the Northrup Division and the

Hawley Division. Projections for the next year are as follows:

Operating income for Superior Corporation, as a whole, if the Hawley Division were

dropped would be

A. $45,000

B. $80,000

C. $100,000

D. $120,000

Answer:

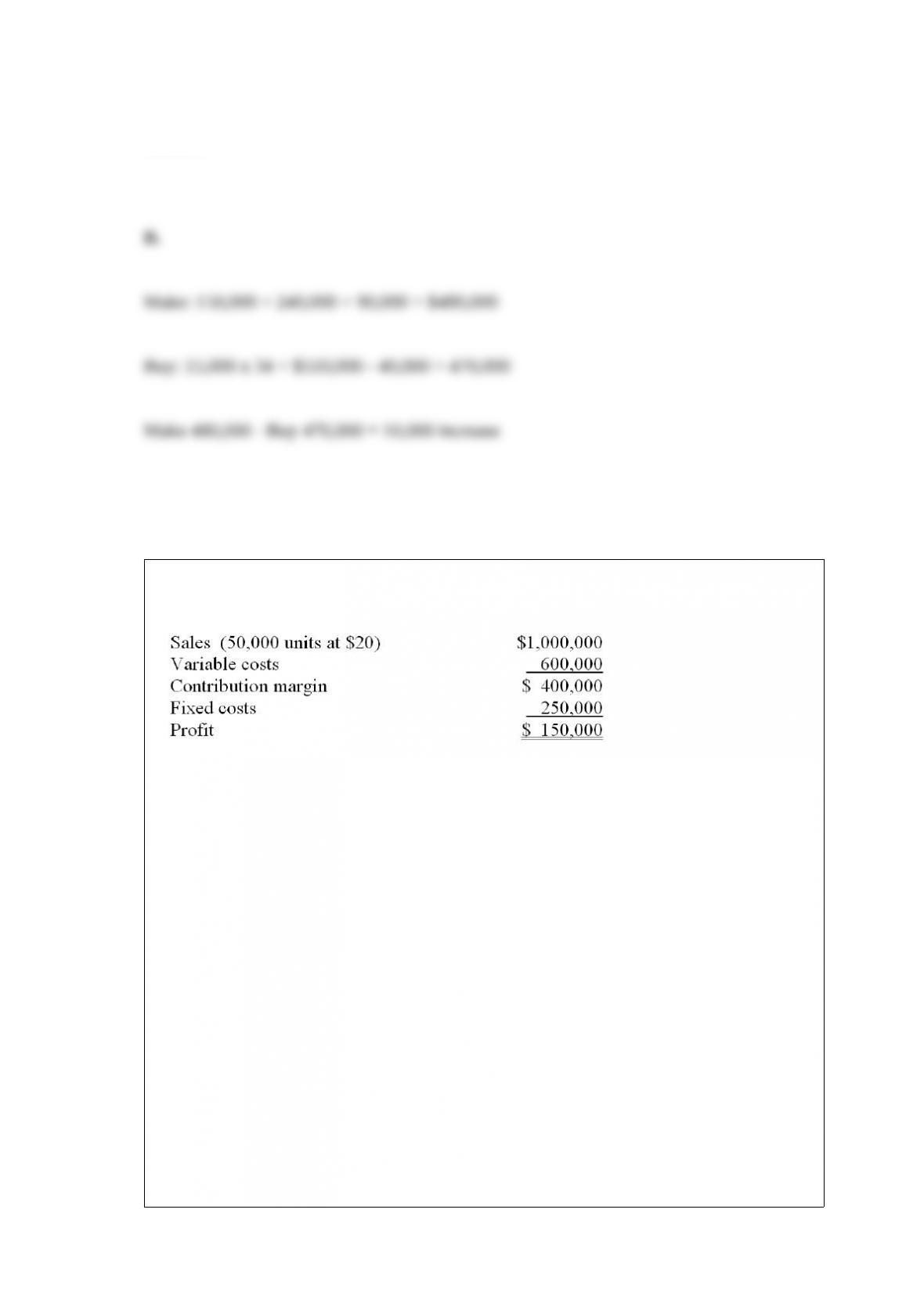

You have been provided with the following information regarding the York

Manufacturing Company:

This information is based on forecasted sales of 30,000 units.

Required:

(a) What are the expected operating profits for the upcoming year?

(b) What is the break-even point in units?

(c) If $160,000 of operating profits is desired, how many units must be sold?

Answer:

An intermediate market is perfect when

A. there is no quality differences between inside and outside suppliers.

B. there is no quality differences between inside and outside customers.

C. buyers and sellers can sell any quantity without affecting the market price.

D. buyers and sellers are motivated to make decisions that are consistent with those of

the organization.

Answer:

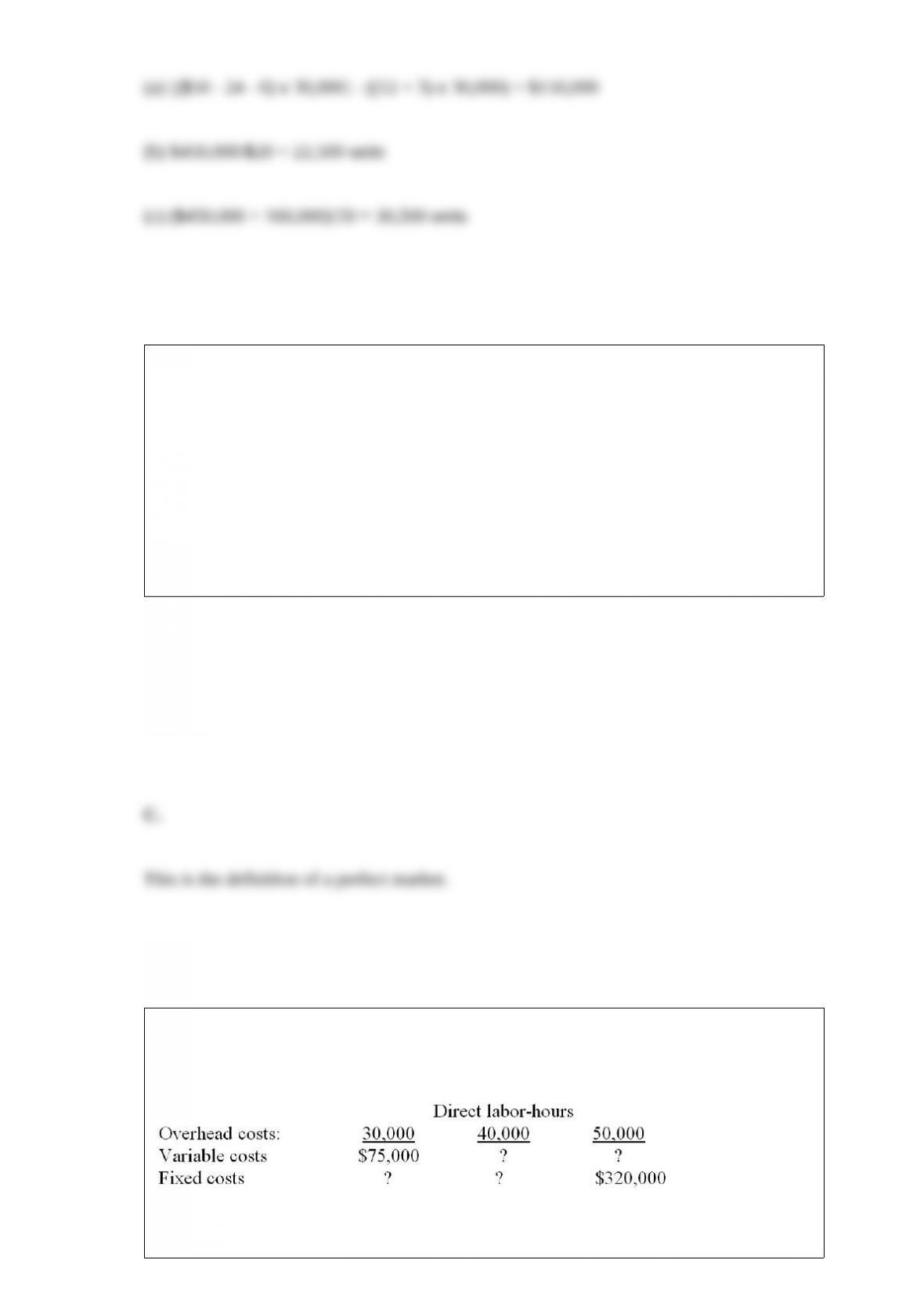

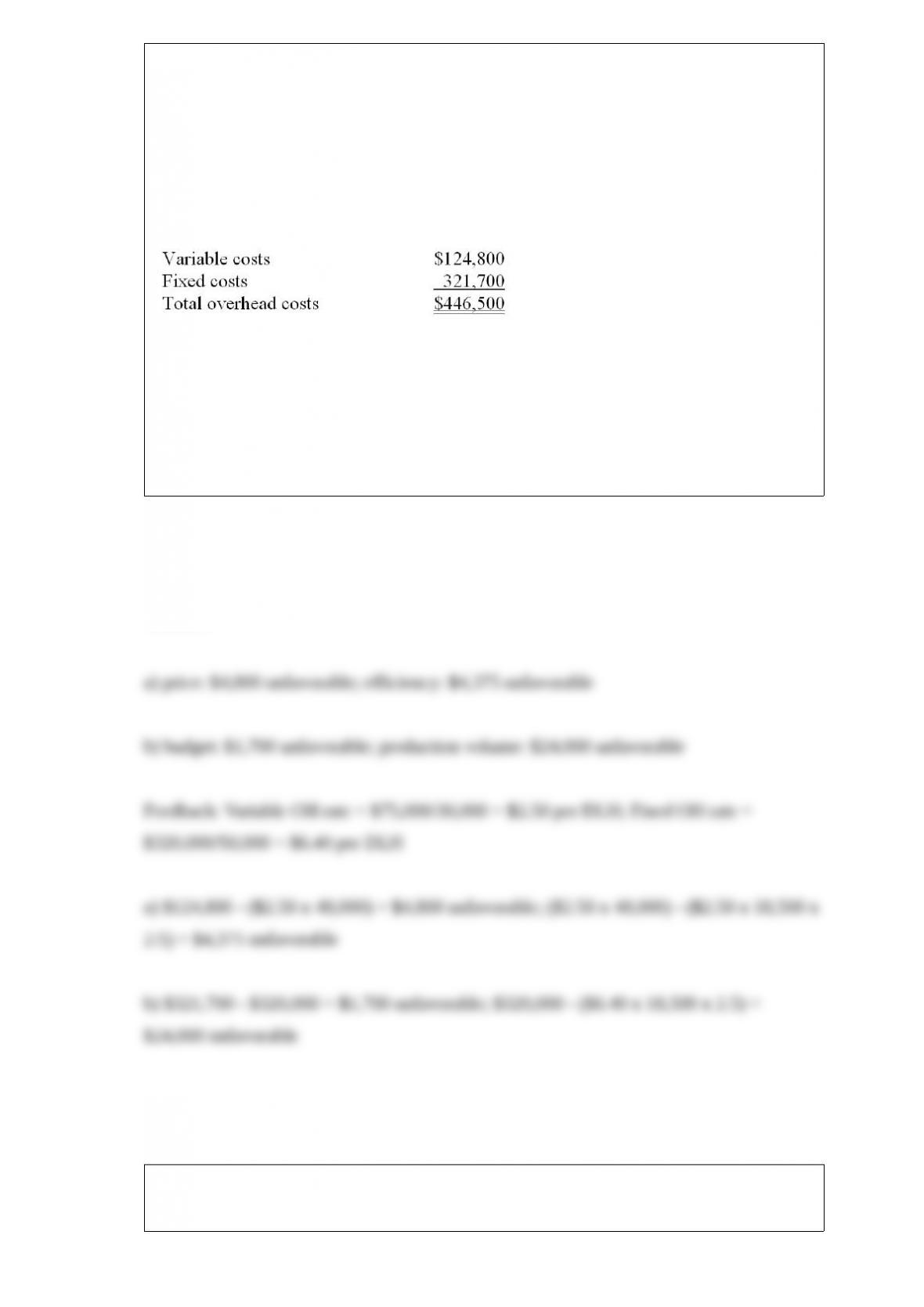

The condensed flexible budget of the Scott Company for the year is given below:

Direct labor-hours

The company produces a single product that requires 2.5 direct labor-hours to complete.

The direct labor wage rate is $7.50 per hour. Three yards of raw material are required

for each unit of product, at a cost of $5 per yard.

Assume that the company chooses 50,000 direct labor-hours as the denominator level of

activity, but actually worked 48,000 hours during the year producing 18,500 units.

Actual overhead costs for the year are:

Required: (Be sure to indicate whether the variances are favorable or unfavorable.)

a) Compute the variable overhead price variance and the variable overhead efficiency

variance.

b) Compute the fixed overhead spending (budget) variance and the production volume

variance.

Answer:

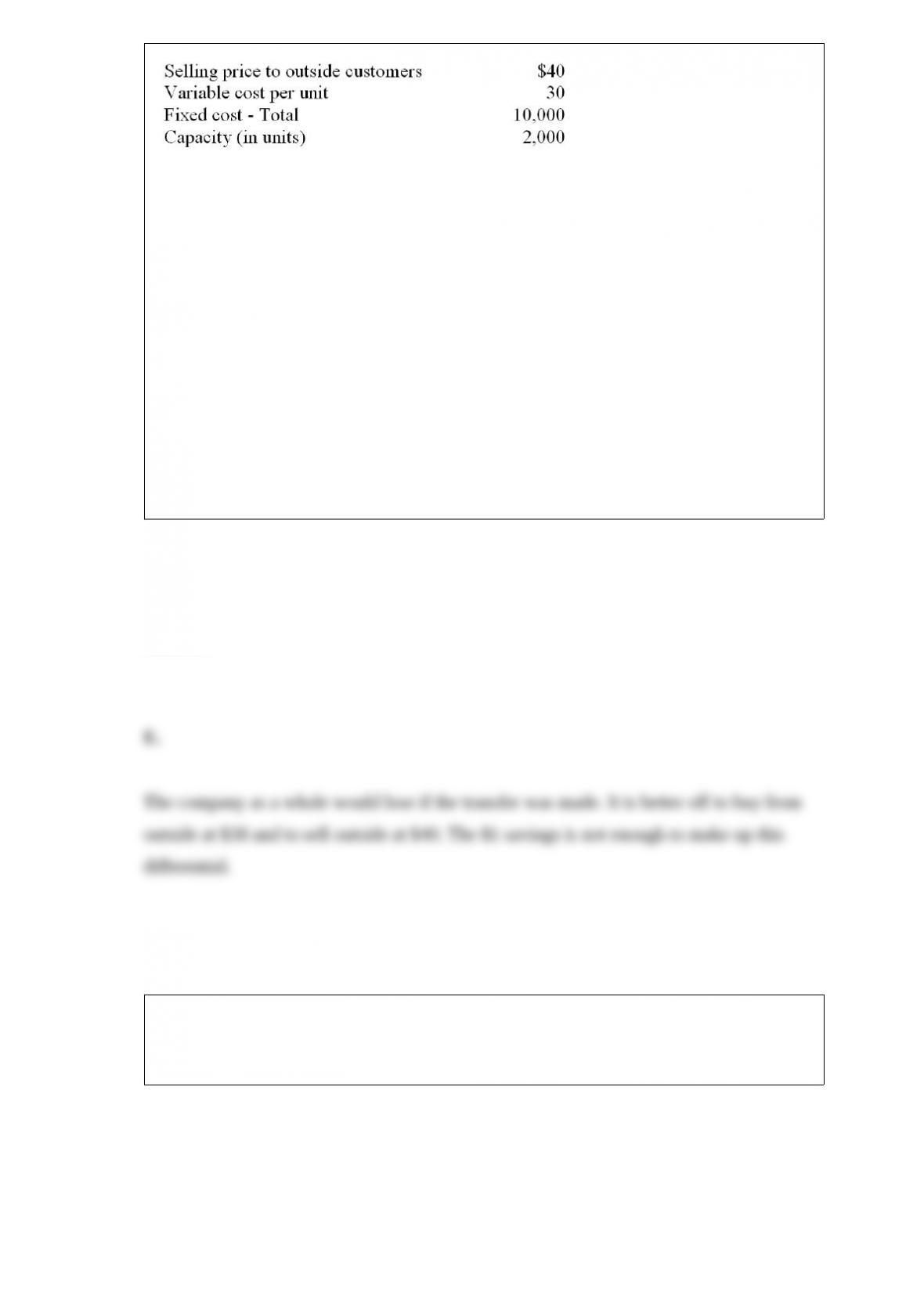

Given the following data for Division A:

Assume that Division A is selling all it can produce to outside customers. If it sells to

Division B, $1 can be avoided in variable cost per unit. Division B is presently

purchasing from an outside supplier at $38 per unit. From the point of view of the

company as a whole, any sales to Division B should be priced at

A. $40.

B. $39.

C. $38.

D. $37.

E. The company would not want the transfer to take place.

Answer:

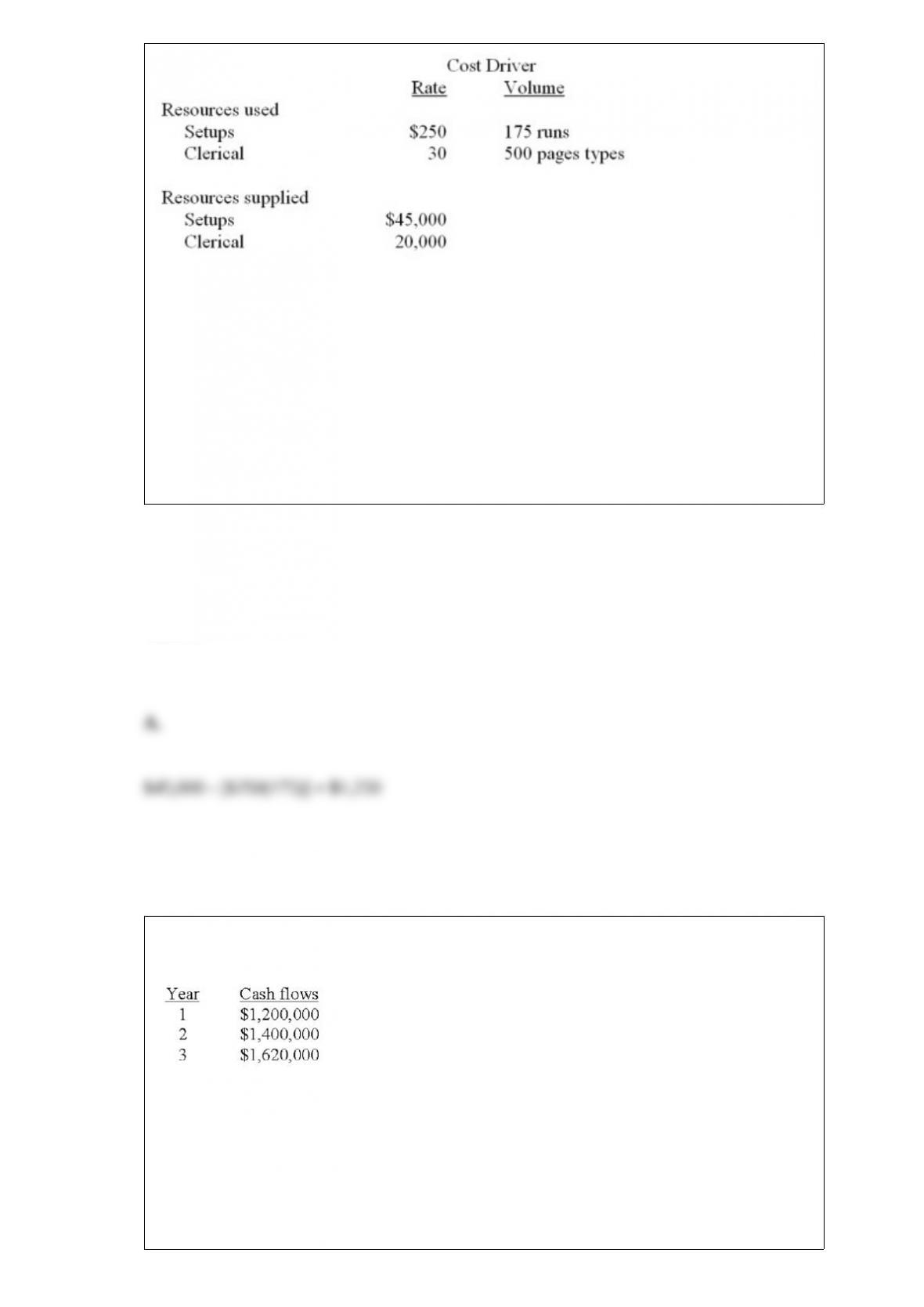

Gundy Press reports the following information about resources. At the beginning of

the year, Gundy estimated it would spend $42,000 for setups and $21,000 for clerical.

Compute unused resource capacity for setups for Gundy Press.

A. $1,250

B. $3,000

C. $1,750

D. $5,000

Answer:

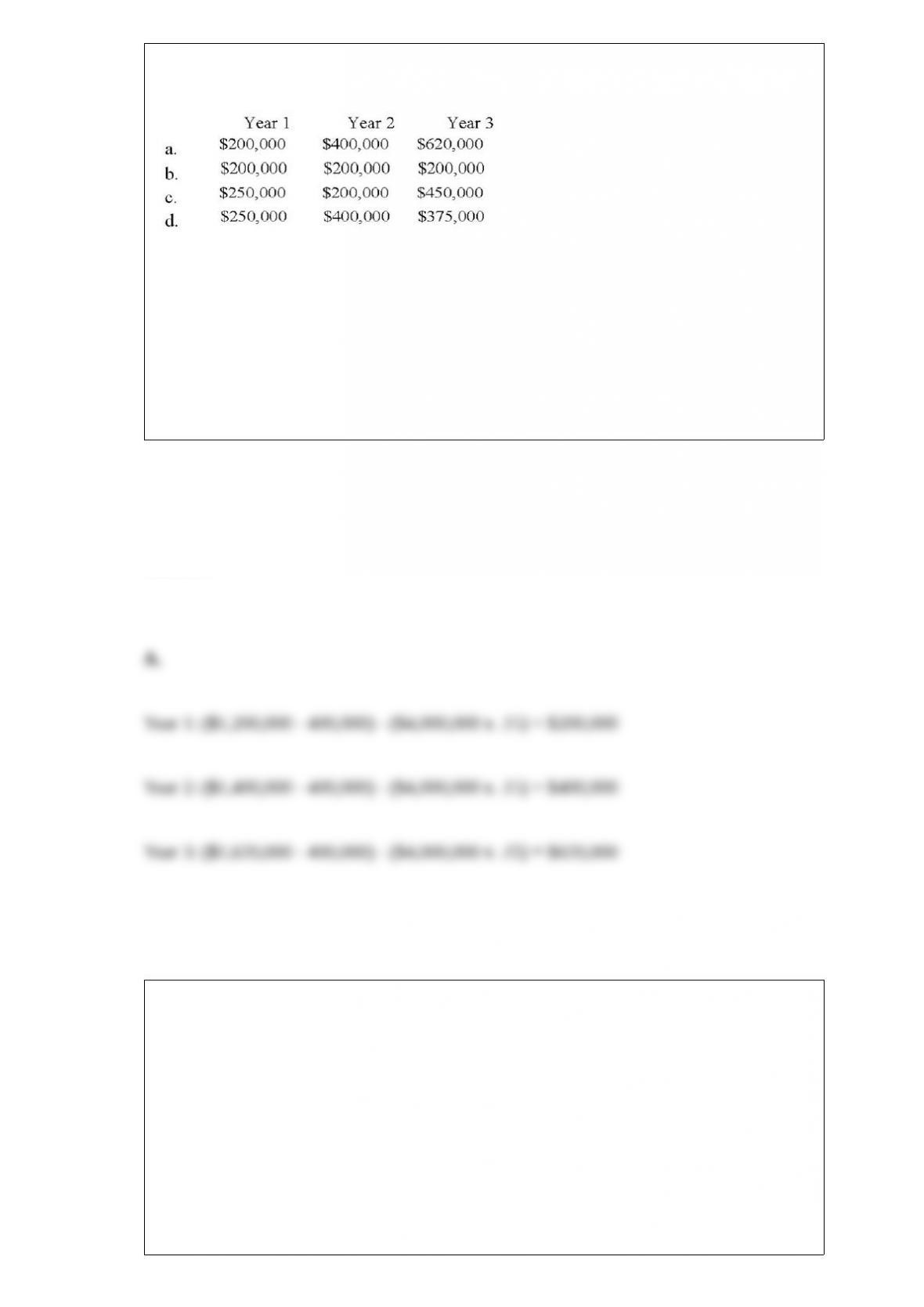

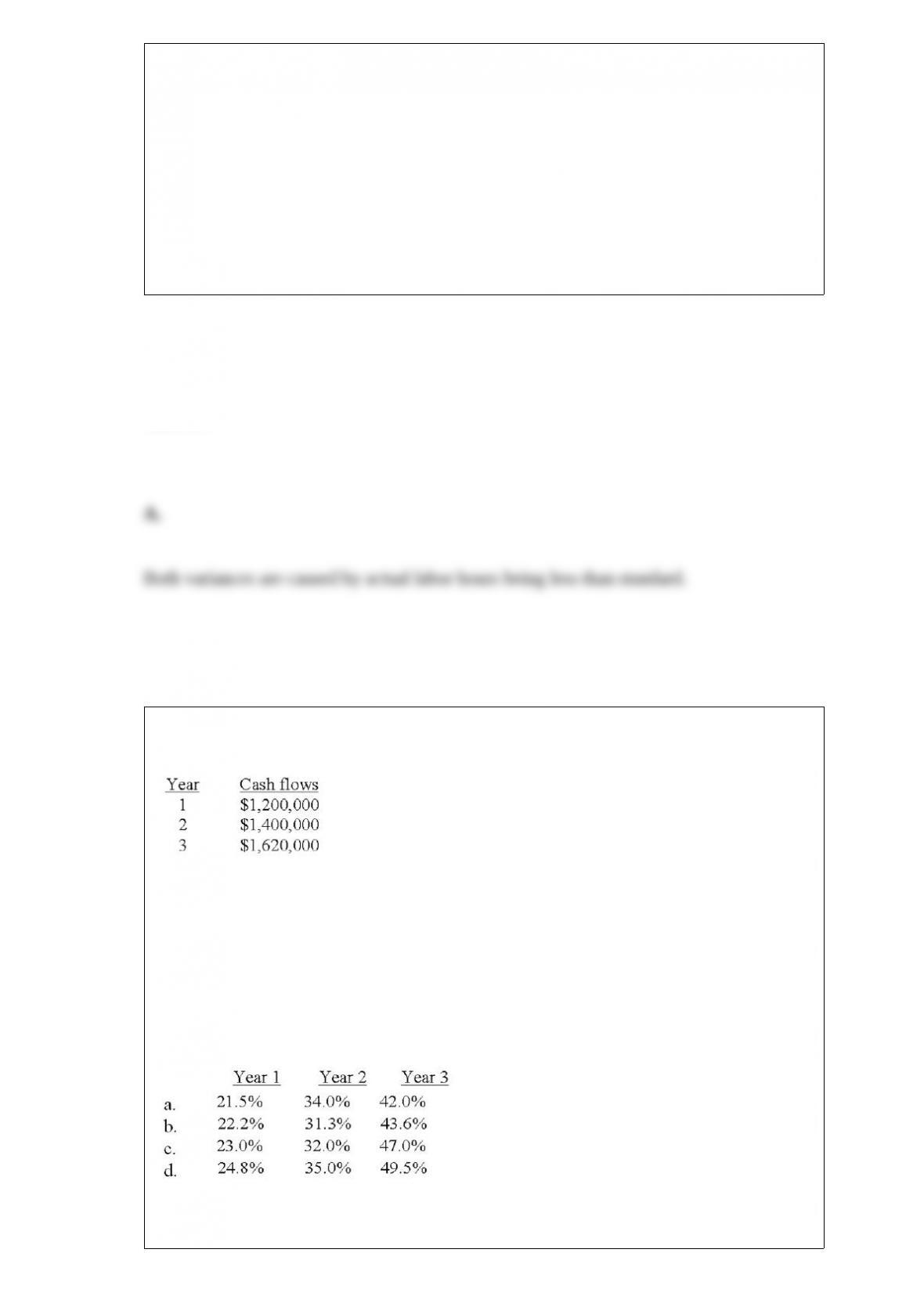

One division of the RST Enterprise Company has depreciable assets costing

$4,000,000. The cash flows from these assets for the past three years have been:

The current (i.e., replacement) costs of these assets were expected to increase 25% each

year. RST used the straight-line depreciation method; the estimated useful life is

10-years with no salvage value. For return on investment (ROI) calculations, RST uses

end-of-year balances.

What is the residual income for each year, assuming the cost of capital is 15% and RST

uses historical costs and gross book values to compute residual income?

A. a

B. b

C. c

D. d

Answer:

In order to compute equivalent units of production using the FIFO method of process

costing, work for the period must be broken down to units

A. completed during the period and units in ending inventory.

B. started during the period and units transferred out during the period.

C. completed from beginning inventory, started and completed during the month, and

units in ending inventory.

D. processed during the period and units completed during the period.

Answer:

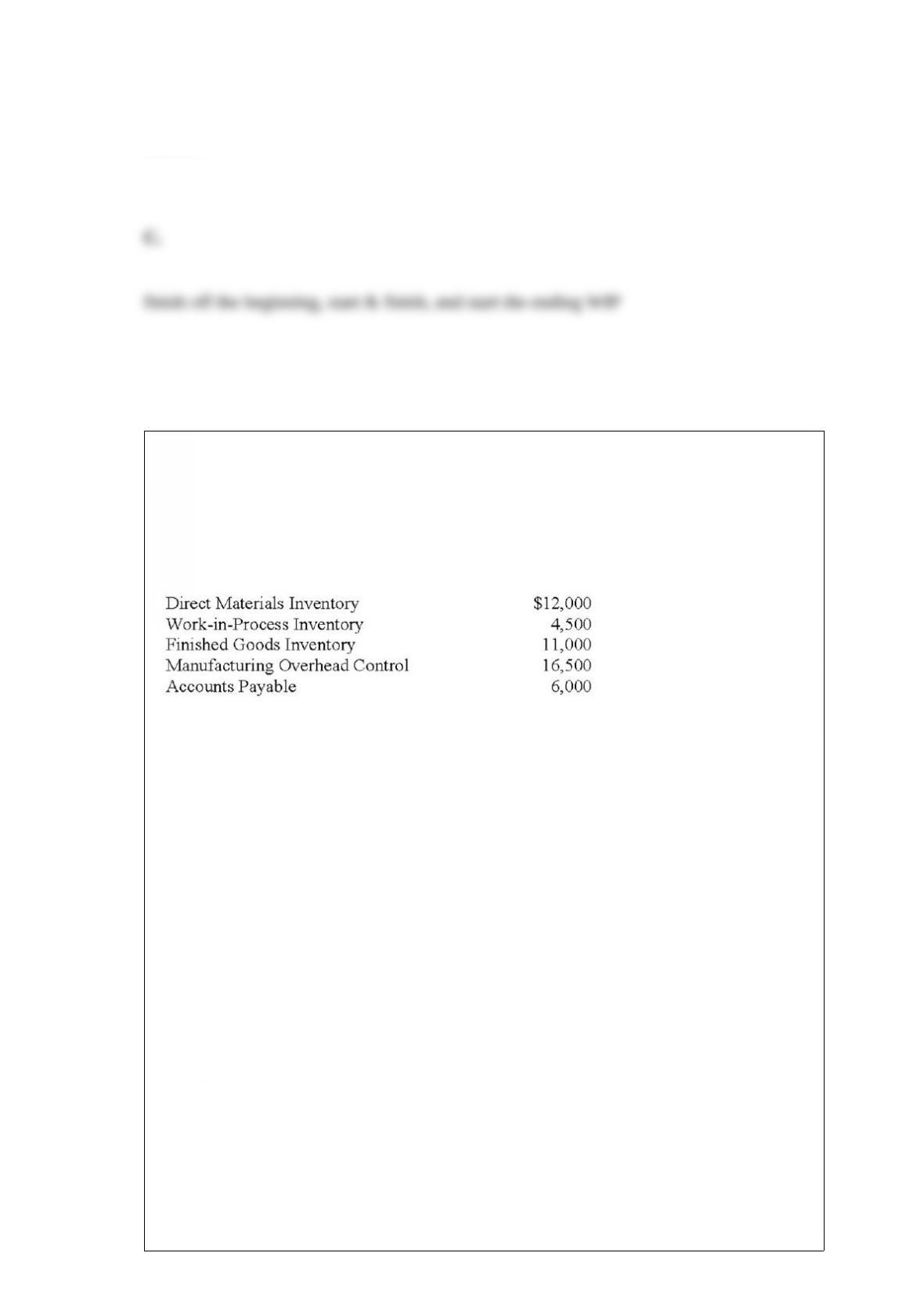

The Update Company does not maintain backup documents for its computer files. In

June, some of the current data were lost, and you have been asked to help reconstruct

the data. The following beginning balances on June 1 are known:

Reviewing old documents and interviewing selected employees have generated the

following additional information:

The production superintendent’s job cost sheets indicated that materials of $2,600 were

included in the June 30 Work-in-Process Inventory. Also, 300 direct labor hours had

been paid at $6.00 per hour for the jobs in process on June 30.

The Accounts Payable account is only for direct material purchases. The clerk

remembers clearly that the balance in the Accounts Payable on June 30 was $8,000. An

analysis of canceled checks indicated payments of $40,000 were made to suppliers

during June.

Payroll records indicate that 5,200 direct labor hours were recorded for June. It was

verified that there were no variations in pay rates among employees during June.

Records at the warehouse indicate that the Finished Goods Inventory totaled $16,000 on

June 30.

Another record kept manually indicates that the Cost of Goods Sold in June totaled

$84,000.

The predetermined overhead rate was based on an estimated 60,000 direct labor hours

for the year and an estimated $180,000 in manufacturing overhead costs.

How much manufacturing overhead was applied to the Work-in-Process Inventory

during June?

A. $12,000

B. $15,600

C. $18,400

D. $20,500

Answer:

The Brisebois Company had the following transactions and events during its first year

of operations. Estimated overhead for the year was $770,000; estimated direct labor

cost for the year was $350,000.

a) Purchased materials on account, $567,000.

b) Requisitioned materials for production as follows: direct materials – 85 percent of

purchases, indirect materials – 12 percent of purchases

c) Direct labor for production is $331,000, indirect labor is $125,000.

d) Overhead incurred (not including materials or labor): $529,000.

e) Overhead is applied to production based on direct labor cost at the rate of ___

percent.

f) Goods costing $976,000 were completed during the period.

g) Goods costing $513,200 were sold on account for $776,000.

Required:

(1) Prepare the journal entries to record the transactions for the year.

(2) Prepare the journal entry to prorate the over- or underapplied overhead to the

appropriate accounts.

Answer:

Sweet Lu Industries applies manufacturing overhead to its products on the basis of

50% of direct material cost. If a job had $35,000 of manufacturing overhead applied to

it during May, the direct materials assigned to the job was:

A. $17,500

B. $35,000

C. $70,000

D. $140,000

Answer:

At a break-even point of 400 units, variable costs were $400 and fixed costs were

$200. What will the 401st unit sold contribute to operating profits before income taxes?

A. $.50

B. $1.00

C. $1.50

D. $2.00

Answer:

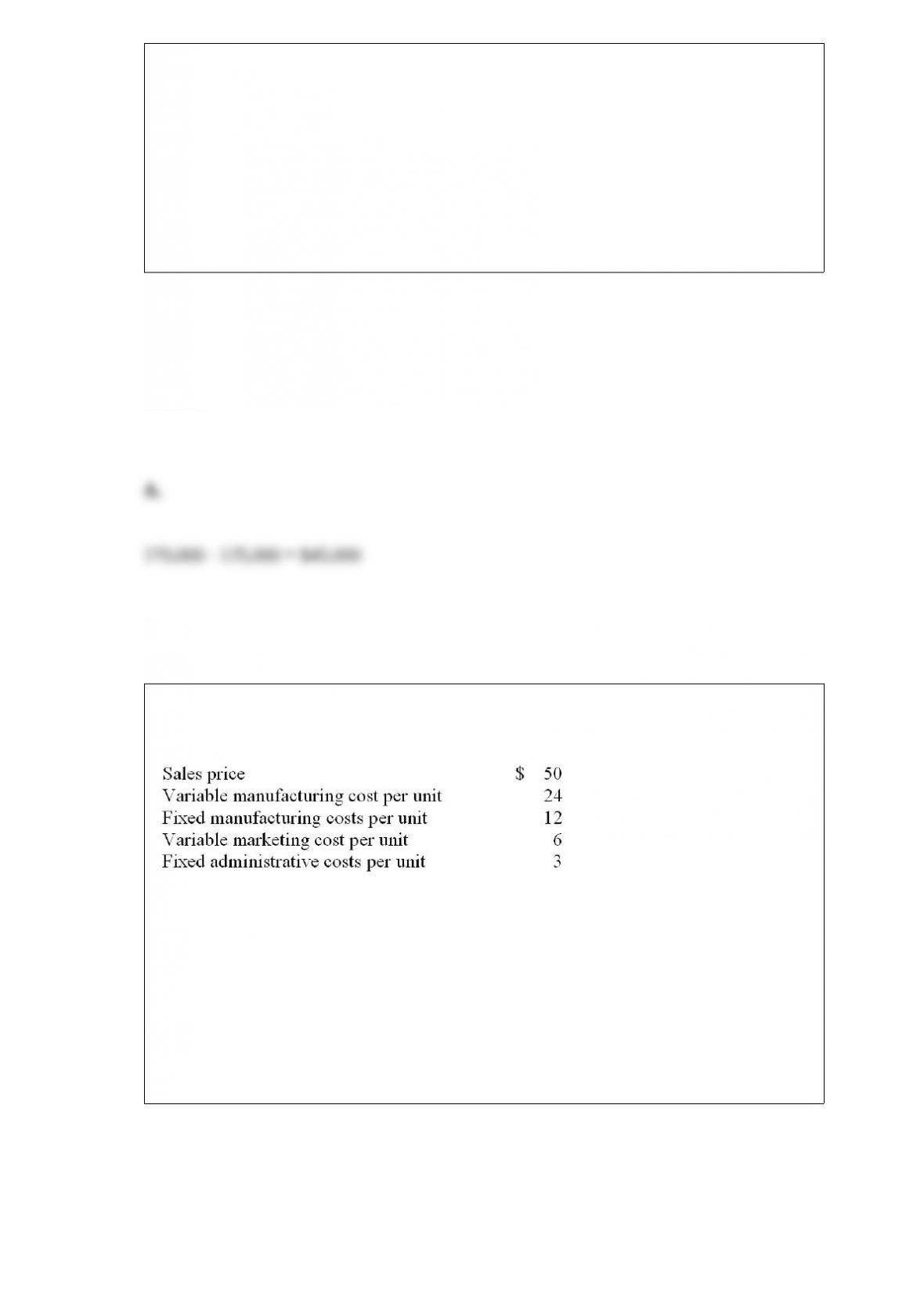

A division can sell externally for $40 per unit. Its variable manufacturing costs are $15

per unit, and its variable marketing costs are $6 per unit. What is the opportunity cost of

transferring internally, assuming the division is operating at capacity?

A. $15

B. $19

C. $21

D. $25

Answer:

In the balanced scorecard, the internal business process perspective addresses which of

the following questions?

A. “To achieve our mission, how will we sustain our ability to change and improve?”

B. “To succeed financially, how should we appear to our shareholders?”

C. “To satisfy our shareholders and customers, in what business process must we

excel?”

D. “To achieve our mission, how should we appear to our customers?”

Answer:

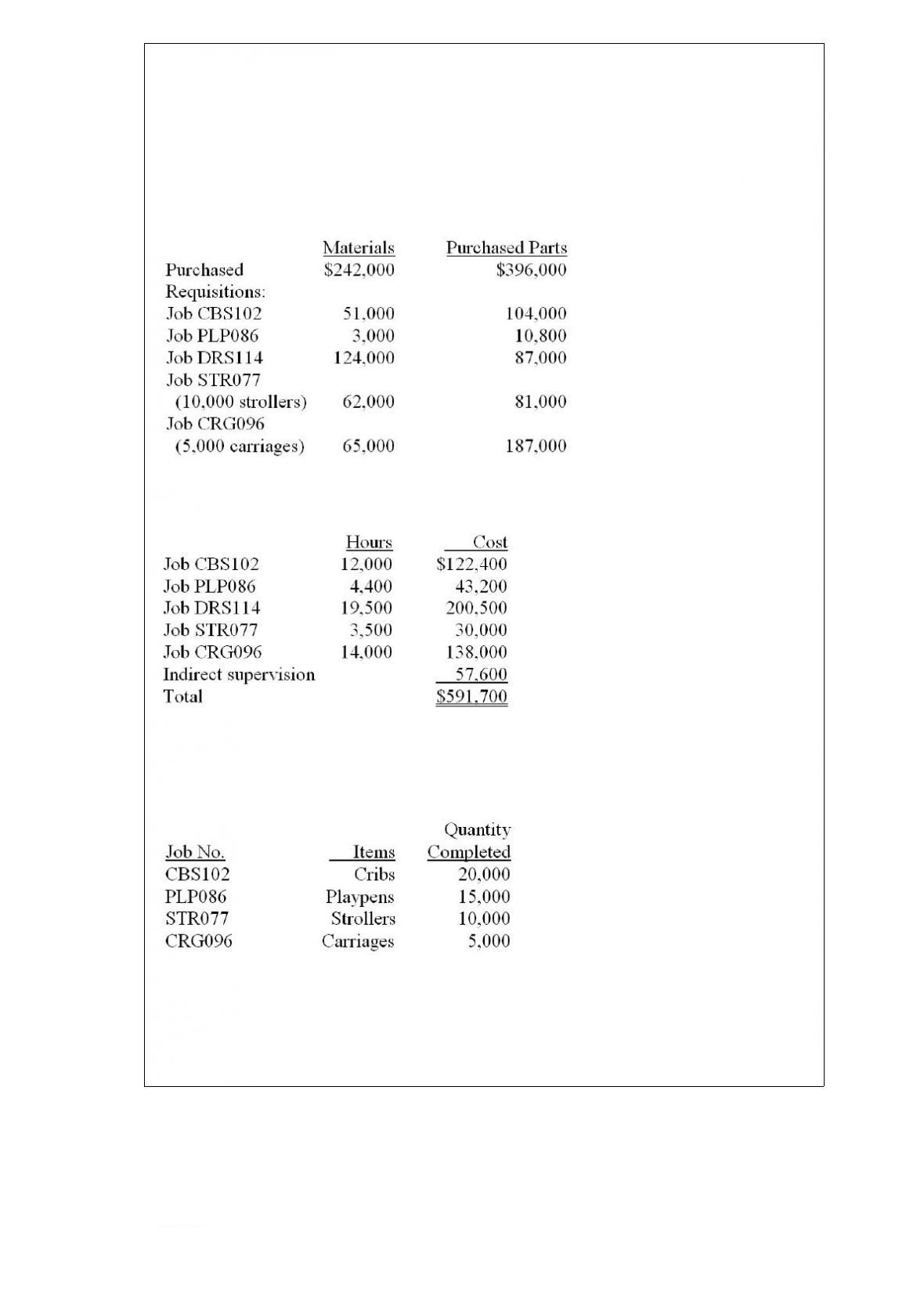

Baby Care Manufacturing Company is a manufacturer of furnishings for infants and

children. The company uses job costing and employs a full absorption accounting

method for cost accumulation. Baby Care’s Work-in-Process Inventory on April 30

consisted of the following jobs:

Baby Care applies manufacturing overhead on the basis of direct labor hours. The

company’s estimated manufacturing overhead for the period ending May 31 totals

$4,500,000; the company estimated it would use 600,000 direct labor hours during the

year.

At the end of April, the balance in Baby Care’s Materials Inventory, which includes

both materials and purchased parts, was $668,000. Additions to, and requisitions from,

the materials inventory during the month of May included the following:

During the month of May, Baby Care’s factory payroll consisted of the following:

Listed below are the jobs that were completed and the units that were sold during the

month of May.

Required:

(a) Compute the value of Baby Care’s Work-in-Process Inventory on May

(b) Compute the value of Baby Care’s Cost of Goods Manufactured for May.

Answer:

Chetek Industries manufactures 15,000 components per year. The manufacturing cost

of the components was determined to be as follows:

Assume Chetek Industries could avoid $40,000 of fixed manufacturing overhead if it

purchases the component from an outside supplier. An outside supplier has offered to

sell the component for $34. If Chetek purchases the component from the supplier

instead of manufacturing it, the effect on income would be a

A. $60,000 increase

B. $10,000 increase

C. $100,000 decrease

D. $140,000 increase

Answer:

Howard Company operates several investment centers. The manager of Genco

Division expects the following results for the coming year.

Included in Genco’s variable cost is $7 for a component it buys from an outside

supplier. One of these components is required in each unit of Genco’s product. The

manager of Genco has just found that she can buy the component from Danner

Division, another division of Howard Company. Danner sells 300,000 units of the

component to outsiders at $8 and its variable cost is $4 per unit. Danner offers to sell

the component to Genco at a price of $6.

Danner has a capacity of 330,000 units. Assume that Genco wants to buy all of its needs

from one source, so that Danner must supply all or none of Genco’s need for 50,000

units.

Required

a) Determine the change in income of Danner Division of supplying the component to

Genco at $6 as opposed to not supplying Genco.

b) Determine the change in income of Howard Company if Danner supplies Genco at

$6.

Answer:

A company’s break-even point will not be increased by:

A. an increase in total fixed costs.

B. a decrease in the selling price per unit.

C. an increase in the variable cost per unit.

D. a decrease in the contribution margin ratio.

E. an increase in the number of units produced and sold.

Answer:

If overhead is applied to production using direct labor hours and the direct labor

efficiency variance is favorable, then the variable overhead efficiency variance is

A. favorable.

B. unfavorable.

C. either favorable or unfavorable.

D. neither favorable not unfavorable.

Answer:

One division of the RST Enterprise Company has depreciable assets costing

$4,000,000. The cash flows from these assets for the past three years have been:

The current (i.e., replacement) costs of these assets were expected to increase 25% each

year. RST used the straight-line depreciation method; the estimated useful life is

10-years with no salvage value. For return on investment (ROI) calculations, RST uses

end-of-year balances.

What is the ROI using historical cost and net book value?

A. a

B. b

C. c

D. d

Answer:

The predetermined manufacturing overhead rate for the year was 140% of direct labor

cost; employees were paid $17.50 per hour. If the estimated direct labor hours were

15,000, what was the estimated manufacturing overhead?

A. $210,000

B. $187,500

C. $262,500

D. $367,500

Answer:

It is possible that the total cost of a job started in April and completed in May will not

include:

A. direct material added in April.

B. direct labor added in May.

C. applied overhead in April.

D. applied overhead in May.

E. direct material purchased in May.

Answer:

Folly Beach Industries decides to price delivery service according to the results of a

recent activity-based costing (ABC) study. The study indicates Folly Beach should

charge $16 per order, 1% of the order’s value for general delivery costs, $2.50 per item,

and $45 for delivery.

A year later, Folly Beach collected the following information for three of its customers:

What are the total delivery costs charged to Customer C during the year?

A. $16,863

B. $20,000

C. $31,272

D. $32,272

Answer:

The Trey Company experienced a $100,000 shortfall in sales revenues for the year. Top

management is quite disturbed about this and has decided to use variance analysis in

assigning the responsibility for the decline. Which of the following variances would be

most within the control of the marketing department?

A. Sales mix

B. Market share

C. Sales quantity

D. Industry volume

Answer:

Mount Company incurred a total cost of $8,600 to produce 400 units of pulp. Each unit

of pulp required five (5) direct labor hours to complete. What is the total fixed cost if

the variable cost was $1.50 per direct labor hour?

A. $1,700

B. $3,000

C. $5,600

D. $8,000

Answer:

The statistical method of forecasting that relies heavily on regression models is called

A. econometric models.

B. Delphi technique.

C. scatter graph method.

D. participative budgeting.

Answer: