1) When preparing the operating activities section of the statement of cash flows using

the indirect method, a decrease in accounts receivable is subtracted from net income.

2) The FIFO inventory method assumes that costs for the earliest units purchased are

the first to be charged to the cost of goods sold.

3) An inventory error is sometimes said to be self-correcting because it causes an

offsetting error in the next period.

4) Plant assets are usually listed in order from most liquid to least liquid.

5) Cost accounting systems accumulate costs and then assign them to products or

services.

6) The Income Summary account is used to close the permanent accounts at the end of

an accounting period.

7) A company’s current ratio is 1.2 and its quick ratio is 0.25. This company is probably

an excellent credit risk because the ratios reveal no indication of liquidity problems.

8) The reliability of the gross profit method depends on a good estimate of the gross

profit ratio.

9) Control of cash disbursements is important for companies as most large thefts occur

from payment of fictitious invoices.

10) A company that uses a cost accounting system normally has only two inventory

accounts: Finished Goods Inventory and Goods in Process Inventory.

11) A break-even point can be calculated either in units or in dollars.

12) Financial analysis only refers to the communication of relevant financial

information to decision makers.

13) The acid-test ratio is also called the quick ratio.

14) Investment center is another name for profit center.

15) A materials consumption report is a source document that summarizes the materials

used during a reporting period.

16) In applying the lower of cost or market method to inventory valuation, market is

defined as the current replacement cost.

17) Profit margin reflects the percent of profit in each dollar of revenue.

18) Activity-based costing assigns costs first to activity pools, and then costs from

activity cost pools are assigned to the cost objects benefiting from the activities.

19) A company made a bank deposit on September 30 that did not appear on the bank

statement dated as of September 30. In preparing the September 30 bank reconciliation,

the company should:

A.Deduct the deposit from the bank statement balance

B.Send the bank a debit memorandum

C.Deduct the deposit from the September 30 book balance and add it to the October 1

book balance

D.Add the deposit to the book balance of cash

E.Add the deposit to the bank statement balance

20) Advance ticket sales totaling $6,000,000 cash would be recognized as follows:

A.Debit Sales, credit Unearned Revenue

B.Debit Unearned Revenue, credit Sales

C.Debit Cash, credit Unearned Revenue

D.Debit Unearned Revenue, credit Cash

E.Debit Cash, credit Revenue

21) The voucher system of control:

A.Is a set of procedures and approvals designed to control cash receipts and the

acceptance of obligations

B.Establishes procedures for verifying, approving, and recording obligations for

eventual cash disbursement

C.Establishes procedures for receiving checks for the sale of verified, approved, and

recorded activities

D.Applies only when multiple purchases are made from the same supplier

E.All of these

22) An analysis that explains any differences between the checking account balance

according to the depositor’s records and the balance reported on the bank statement is

a(n):

A.Internal audit

B.Bank reconciliation

C.Bank audit

D.Trial reconciliation

E.Analysis of debits and credits

23) Which of the following is not a result of following a well-designed budgeting

process?

A.Improved decision-making processes

B.Improved performance evaluations

C.Improved coordination of business activities

D.Assurance of future profits

E.All of these are benefits of effective budgeting

24) Sebring Company reports depreciation expense of $40,000 for Year 2. Also,

equipment costing $140,000 was sold for its book value in Year 2. The following

selected information is available for Sebring Company from its comparative balance

sheet. Compute the cash received from the sale of the equipment.

A.$72,000

B.$68,000

C.$28,000

D.$40,000

E.$36,000

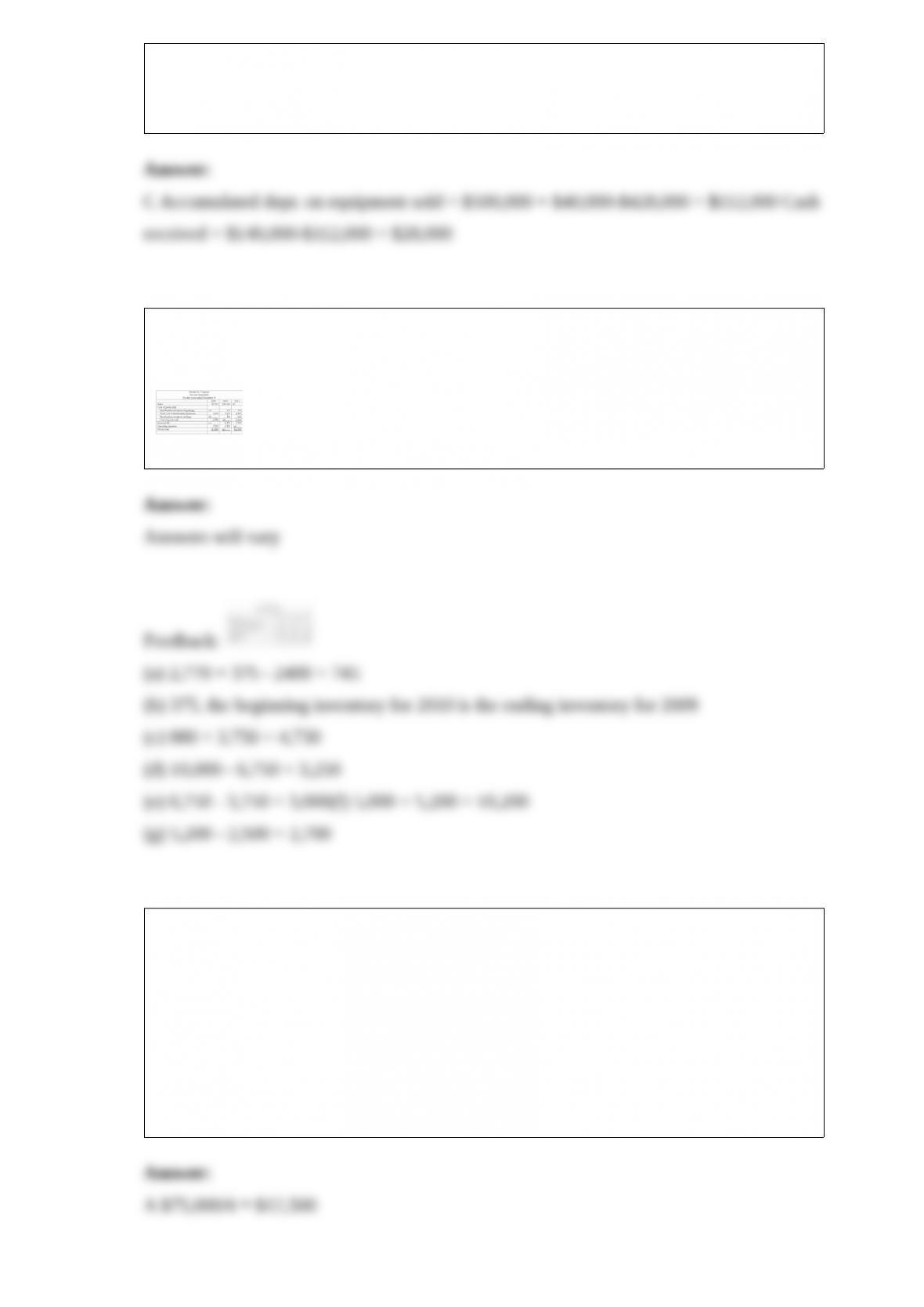

25) Fill in the blanks (a) through (g) for the Hendricks Company for each of the income

statements for 2009, 2010, and 2011.

26) Monte Ray leases office space for $7,000 per month. On January 3, Monte Ray

incurs $75,000 to improve his leased office space. These improvements are expected to

yield benefits for 8 years. Ray has 6 years remaining on his lease. What journal entry

would be needed to record the expense for the first year related to the improvements?

A.Debit Amortization Expense $12,500; credit Accumulated Amortization $12,500

B.Debit Depletion Expense $12,500; credit Accumulated Depletion $12,500

C.Debit Depreciation Expense $12,500; credit Accumulated Depreciation $12,500

D.Debit Depletion Expense $9,375; credit Accumulated Depletion $9,375

E.Debit Amortization Expense $9,375; credit Accumulated Amortization $9,375

27) Jon Shear expects an investment of $25,000 to return $6,595 annually. His

investment is earning 10% per year. How many annual payments will he receive?

A.Five payments

B.Six payments

C.Four payments

D.Three payments

E.More than six payments

28) A document in a job order cost accounting system that is used to record the costs of

producing a job is a(n):

A.Job cost sheet

B.Job lot

C.Finished goods summary

D.Process cost system

E.Units-of-production sheet

29) Journal entries recorded at the end of each accounting period to prepare the

revenue, expense, and withdrawals accounts for the upcoming period and to update the

owner’s capital account for the events of the period just finished are referred to as:

A.Adjusting entries

B.Closing entries

C.Final entries

D.Work sheet entries

E.Updating entries

30) A subsidiary ledger:

A.Includes transactions not covered by special journals

B.Is a listing of all of the accounts of a business

C.Is a listing of individual accounts and amounts with a common characteristic

D.Is also called a general ledger

E.Is also called a special journal

31) Capital budgeting decisions are risky because:

A.The outcome is uncertain

B.Large amounts of money are usually involved

C.The investment involves a long-term commitment

D.The decision could be difficult or impossible to reverse

E.All of these are true

32) Which of the following statements is incorrect?

A.Adjustments to prepaid expenses, depreciation, and unearned revenues involve

previously recorded assets and liabilities

B.Accrued expenses and accrued revenues involve assets and liabilities that had not

previously been recorded

C.Adjusting entries can be used to record both accrued expenses and accrued revenues

D.Prepaid expenses, depreciation, and unearned revenues often require adjusting entries

to record the effects of the passage of time

E.Adjusting entries affect the cash account

33) The set of periodic budgets that are prepared and periodically revised in the practice

of continuous budgeting are called:

A.Production budgets

B.Sales budgets

C.Cash budgets

D.Rolling budgets

E.Capital expenditures budgets

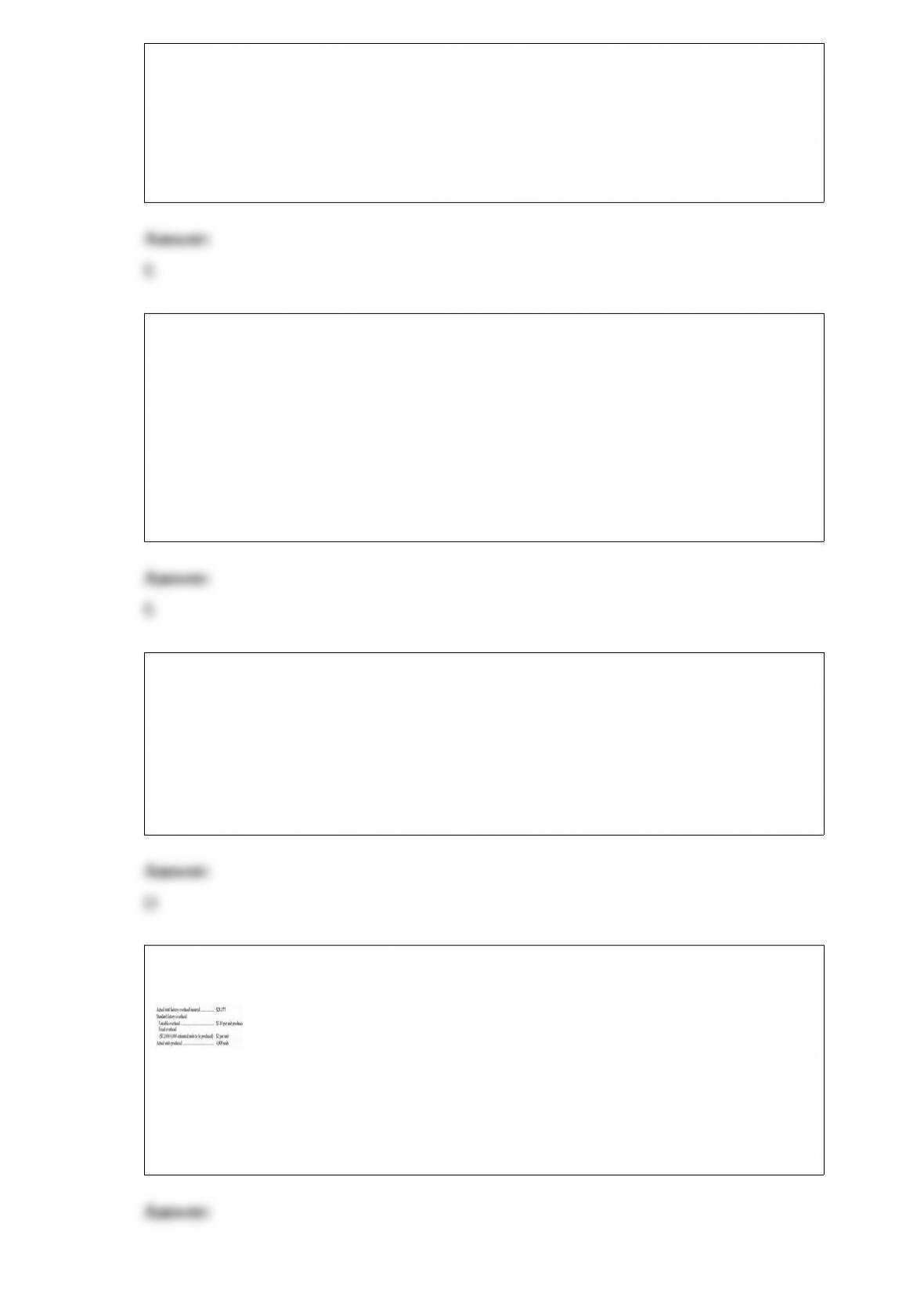

34) Montaigne Corp. has the following information about its standards and production

activity for November. The volume variance is:

A.$1,295U

B.$1,295F

C.$2,400U

D.$2,400F

E.$3,695U

35) External users of financial information:

A.Are those individuals involved in managing and operating the company

B.Include internal auditors and consultants

C.Are not directly involved in operating the company

D.Make strategic decisions for a company

E.Make operating decisions for a company

36) Match each of the following terms with the appropriate definitions.

1>Materiality constraint A.A measure of both the quality and liquidity of accounts

receivable. It indicates how often, on average, receivables are received and collected

during the period.

2>Factor B.Amounts owed by customers from credit sales for which payment is

required in periodic payments over an extended period of time.

3>Full disclosure principle C.The accounting constraint that states that an amount can

be ignored if its effect on the financial statements is unimportant to their users.

4>Accounts receivable turnover D.Refers to a note maker’s inability or refusal to pay

the note at maturity.

5>Direct write-off E.A method of accounting for bad debts that matches the estimated

loss from uncollectible accounts receivable against the sales they helped to produce.

6>Dishonoring a note F.A buyer of accounts receivable who charges the seller a fee and

then receives cash from the receivables as they come due.

7>Installment accounts receivable G.The accounting principle that requires the

financial statements (including the notes) to report all relevant information about

operations and financial condition.

8>Allowance method H.One who signs a note and promises to pay it at maturity.

9>Principal of a note I.A method of accounting for bad debts that records the loss from

an uncollectible account receivable when it is determined to be uncollectible.

10>Maker of a note J.The amount that the signer of a note agrees to pay back when the

note matures, not including interest.

37) Source documents:

A.Include the ledger

B.Are the sources of accounting information

C.Must be in electronic form

D.Are based on accounting entries

E.Include the chart of accounts

38) Marian Mosely is the owner of Mosely Accounting Services. Which accounting

principle requires Marian to keep her personal financial information separate from the

financial information of Mosely Accounting Services?

A.Monetary unit assumption

B.Going-concern assumption

C.Cost principle

D.Business entity assumption

E.Matching principle

39) Which of the following statements regarding reporting under GAAP and IFRS is

not true?

A.Both GAAP and IFRS define the initial asset value as historical cost for nearly all

assets

B.The definition of an asset under GAAP and IFRS involves three basic criteria

C.Both GAAP and IFRS define the initial asset value as replacement value

D.The definition of a liability under GAAP and IFRS involves three basic criteria

E.After acquisition, one of two asset measurement systems is applied

40) The acid-test ratio differs from the current ratio in that:

A.Liabilities are divided by current assets.

B.Prepaid expenses and inventory are excluded from the calculation of the acid-test

ratio.

C.The acid-test ratio measures profitability and the current ratio does not.

D.The acid-test ratio excludes short-term investments from the calculation.

E.The acid-test ratio is a measure of liquidity but the current ratio is not.

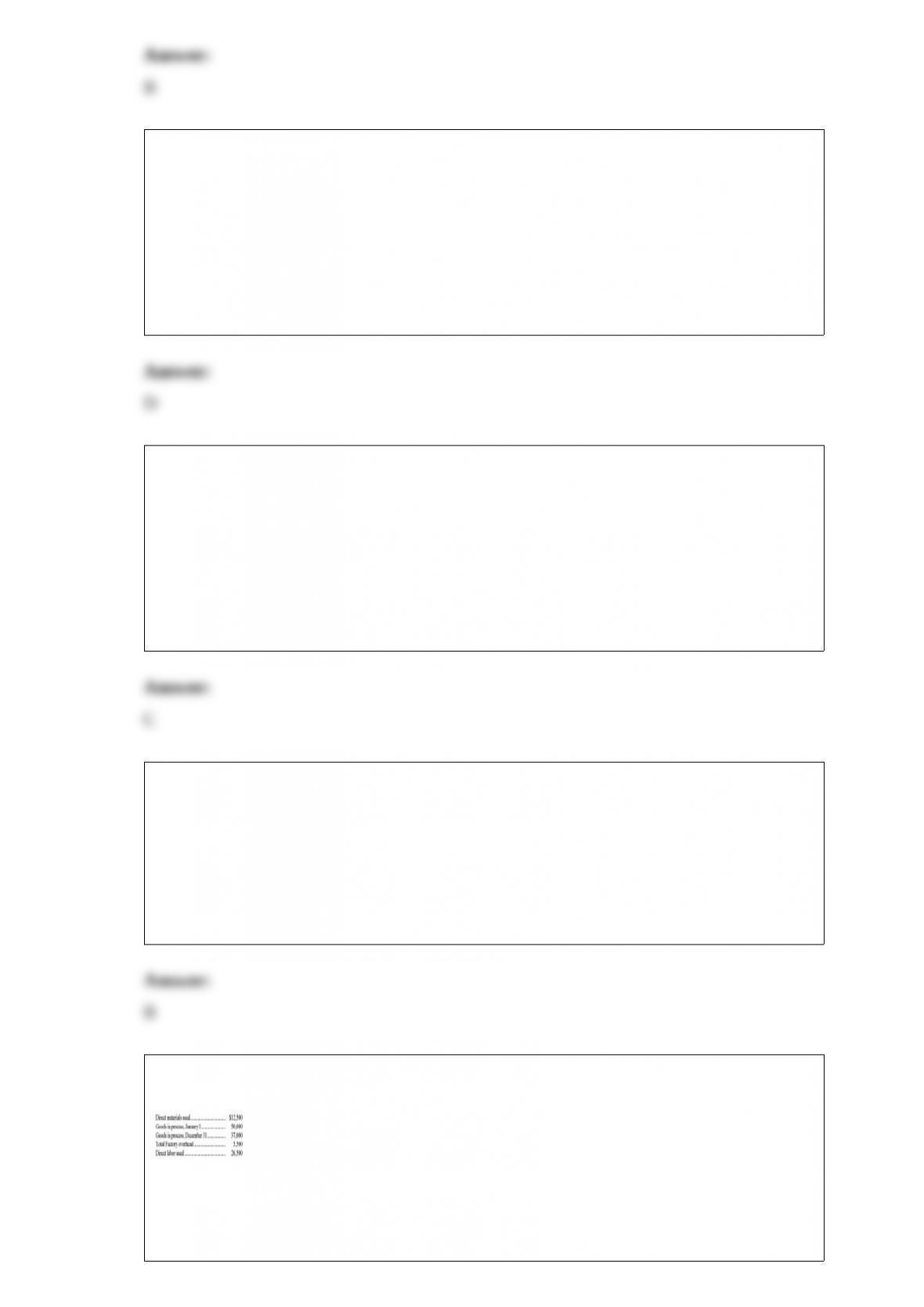

41) Using the information below for Talking Toys, Inc., determine the manufacturing

costs incurred during the year:

A.$13,000

B.$44,500

C.$57,500

D.$94,500

E.$89,000

42) The excess of expenses over revenues for a period is:

A.Net assets

B.Equity

C.Net loss

D.Net income

E.A liability

43) Nee High and Low Jack are partners in an accounting firm and share net income

and loss equally. High’s beginning partnership capital balance for the current year is

$285,000, and Jack’s beginning partnership capital balance for the current year is

$370,000. The partnership had net income of $250,000 for the year. High withdrew

$90,000 during the year and Jack withdrew $100,000. What is Jack’s return on equity?

A.41.3%

B.43.9%

C.32.7%

D.33.8%

E.36.5%

44) A company had sales of $695,000 and cost of goods sold of $278,000. Its gross

margin equals:

A.$(417,000).

B.$695,000.

C.$278,000.

D.$417,000.

E.$973,000.

45) The internal document prepared by a department manager that informs the

purchasing department of its needs that lists the merchandise needed and requests that it

be purchased is the

A.Purchase requisition

B.Purchase order

C.Invoice

D.Receiving report

E.Invoice approval

46) In a firm that manufactures clothing, the department that is responsible for actually

assembling the garments could best be described as a:

A.Service department

B.Operating or production department

C.Cost center

D.Department in which all of the costs incurred are direct expenses

E.Department in which all of the costs incurred are indirect expenses

47) The market value of a bond is equal to:

A.The present value of all future cash payments provided by a bond

B.The present value of all future interest payments provided by a bond

C.The present value of the principal for an interest-bearing bond

D.The future value of all future cash payments provided by a bond

E.The future value of all future interest payments provided by a bond

48) A classification of costs that is useful for assigning responsibility to and evaluating

managers is:

A.Classification by traceability

B.Classification by behavior

C.Classification by relevance

D.Classification by function

E.Classification by controllability

49) On April 1 of the current year, a company paid $150,000 cash to purchase 7%,

10-year bonds with a par value of $150,000; interest is paid semiannually each April 1

and October 1. The company intends to hold these bonds until they mature. Prepare the

journal entries to record the bond purchase, the receipt of the first semiannual interest

payment on October 1 of the current year, and the accrual of interest for the year-end

December 31

50) Ratios may be expressed as (1) _______________________, (2)

_______________________, or (3) _______________________.

51) A company had a building destroyed by fire. The building originally cost $650,000,

and its accumulated depreciation as of the date of the fire was $300,000. The company

received $400,000 cash from an insurance policy that covered the building and will use

that money to help rebuild. Prepare the single journal entry to record the destruction of

the building and the receipt of cash from the insurance company.

52) The cash flow on total assets ratio is computed by dividing _____________ by

__________.

53) The measurement of key relationships between financial statement items is known

as ___________________________.

54) Dividend payment involves three important dates. They are

____________________, _______________________, and

__________________________.

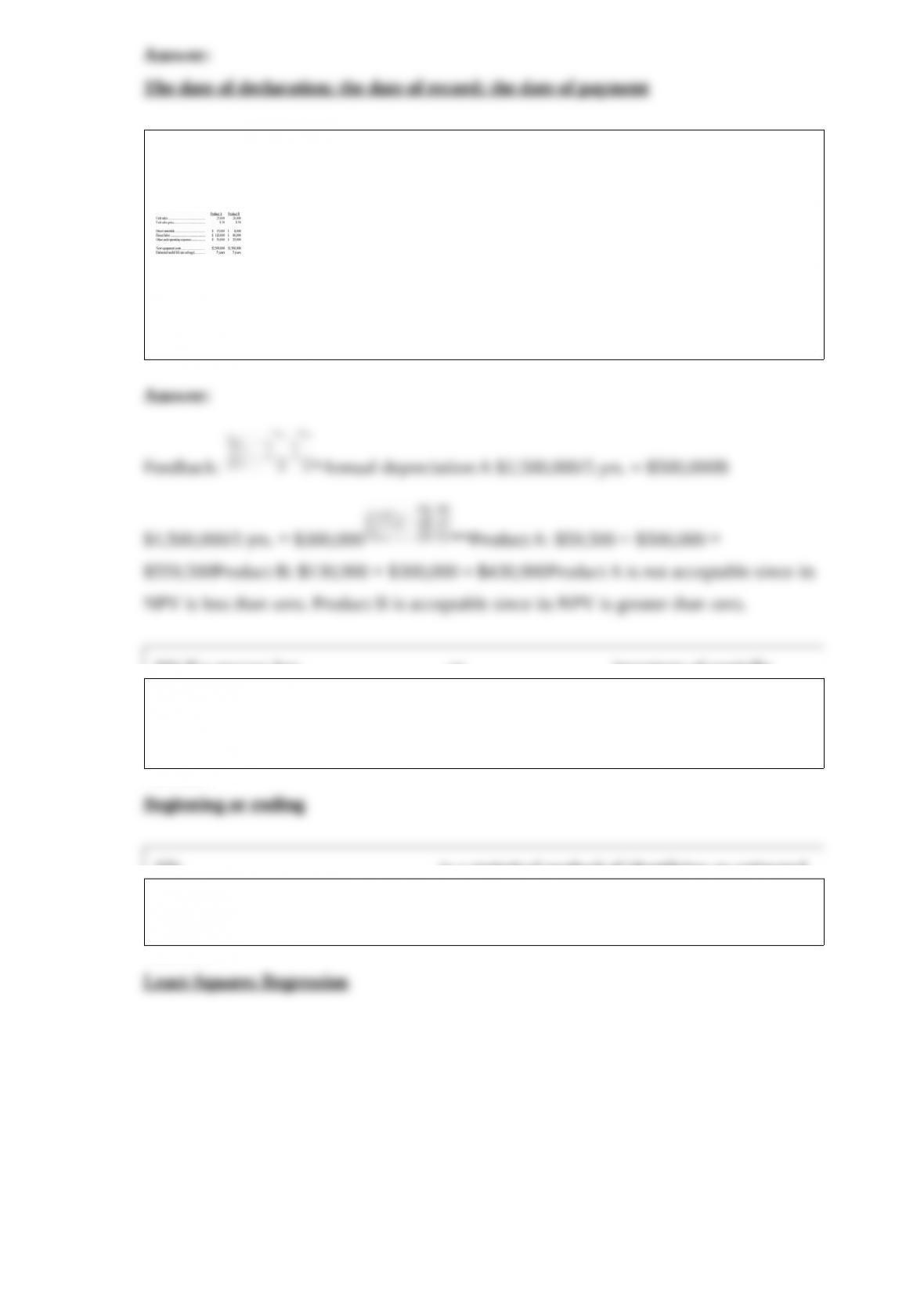

55) A company is trying to decide which of two new product lines to introduce in the

coming year. The company requires a 12% return on investment. The predicted revenue

and cost data for each product line follows:

The company has a 30% tax rate and it uses the straight-line depreciation method. The

present value of an annuity of 1 for 5 years at 12% is 3.6048. Compute the net present

value for each piece of equipment under each of the two product lines. Which, if either

of these two investments is acceptable?

56) If a process has _______________ or _______________ inventory of partially

completed production, equivalent units must be calculated so that total costs incurred

during the period are assigned to all units worked on.

57) ___________________________ is a statistical method of identifying an estimated

line of cost behavior.