1) The following are transactions for the city of Greenville.

a.Issued $50,000 10-year bonds.

b.Used $30,000 of the cash to buy a truck.

c.Sold the truck that was replaced which had cost $28,000, for $2,000. The old truck

was fully depreciated. Residual value is zero.

d.Computed depreciation on the new truck for the year of $6,000.

Required:

Analyze the above transactions by using the accounting equation for a proprietary fund.

2) Interest payments on loans outstanding that do not relate to acquiring, constructing or

improving capital assets are classified as ________ on the cash flow statement for an

Enterprise Fund.

A) Cash Flows from Operating Activities

B) Cash Flows from Noncapital Financing Activities

C) Cash Flows from Capital and Related Financing Activities

D) Cash Flows from Investing Activities

3) In partnership liquidation, how are partner salary allocations treated?

A) Salary allocations take precedence over creditor payments

B) Salary allocations take precedence over amounts due to partners with respect to their

capital interests, but not profits

C) Salary allocations take precedence over amounts due to partners with respect to their

capital profits, but not capital interests

D) Salary allocations are disregarded

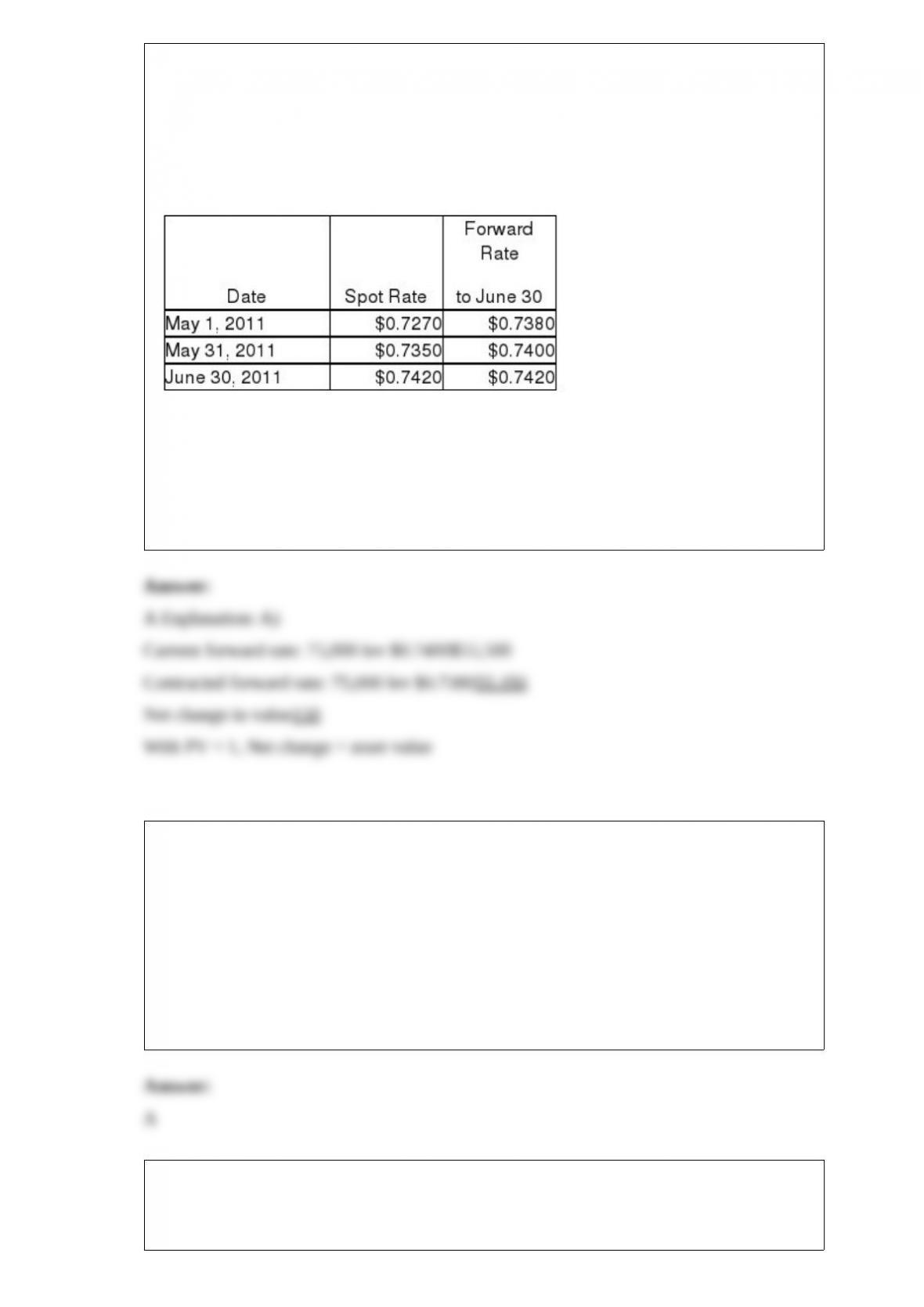

4) On May 1, 2011, Listing Corporation receives inventory items from their Bulgarian

supplier. At the same time, Listing signed a forward contract to purchase 75,000

Bulgarian lev in sixty days to hedge the inventory purchase at $0.738, the 60-day

forward rate. Payment for the inventory will be due in sixty days in Bulgarian lev.

Assume the forward contract will be settled net and this qualifies as a fair value hedge.

The related exchange rates are shown below:

Assuming a present value factor of 1 for simplicity, what is the fair value of this

forward contract on May 31?

A) $150 asset

B) $150 liability

C) $375 asset

D) $375 liability

5) Which statement below is incorrect with respect to the Government-wide financial

statements?

A) All governmental fund categories must convert to the modified accrual basis of

accounting

B) It is necessary to eliminate interfund balances within the governmental funds

C) Capital lease liabilities associated with governmental funds must be included on the

Government-wide financial statements

D) All fixed assets and long-term debt for governmental funds must be included on the

Government-wide financial statements

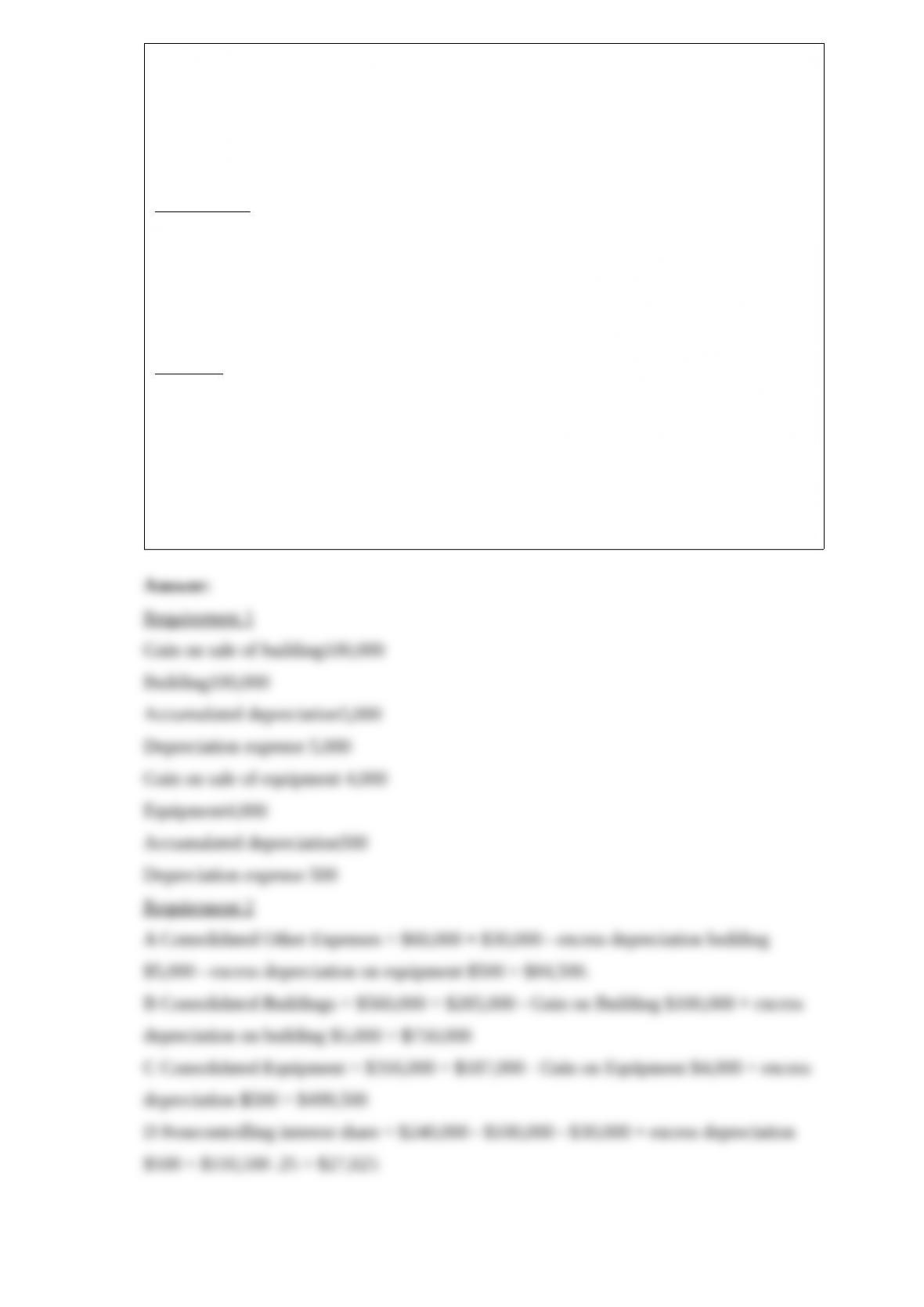

6) Palmer Corporation purchased 75% of Stone Industries’ common stock on January 2,

2010 . On January 1, 2011, Stone sold equipment to Palmer that had a net book value of

$16,000 and an original cost of $24,000 for $20,000. On January 1, 2011, Palmer sold a

building to Stone that had a net book value of $200,000 and an original cost of

$250,000 for $300,000. The equipment had a remaining useful life of 8 years, and the

building had a remaining useful life of 20 years. Neither asset had salvage value. Both

companies use straight-line depreciation.

Selected account balances are shown below for Palmer and Stone for the year ended

December 31, 2011:

PalmerStone

Sales$280,000$240,000

Cost of Goods Sold180,000100,000

Other Expenses60,00030,000

Gain on sale100,0004,000

Building – net560,000285,000

Equipment – net316,000187,000

Required:

1>Prepare the consolidating working paper entries relating to the equipment and

building for the year ended December 31, 2011 .

2>Calculate the following balances for the year ended December 31, 2011:

A. Consolidated “Other Expenses”

B. Consolidated Buildings

C. Consolidated Equipment

D. Noncontrolling interest in Stone’s net income

7) Pascalian Company owns a 90% interest in Sapp Company. On January 1, 2010,

Pascalian had $300,000, 6% bonds outstanding with an unamortized premium of

$9,000. The bonds mature on December 31, 2014 . Sapp acquired one-third of

Pascalian’s bonds in the open market for $97,000 on January 1, 2010 . Both companies

use straight-line amortization of bond discounts/premiums. Interest is paid on

December 31 . On December 31, 2010, the books of the two affiliates held the

following balances:

Pascalian’s books

6% bonds payable$300,000

Premium on bonds7,200

Interest expense16,200

Sapp’s books

Investment in Pascalian bonds$ 97,600

Interest income6,600

Consolidated Interest Expense and consolidated Interest Income, respectively, that

appeared on the consolidated income statement for the year ended December 31, 2010

was

A) $10,800 and $0

B) $10,800 and $6,600

C) $0 and $0

D) $16,200 and $6,600

8) An increase in the liquidity of corporate bonds, other things being equal, shifts the

demand curve for corporate bonds to the ________ and the demand curve for Treasury

bonds shifts to the ________

A) right; right

B) right; left

C) left; left

D) left; right

9) When mutually-held stock involves subsidiaries holding the stock of each other, the

________ method is not used.

A) equity

B) cost

C) conventional

D) treasury stock

10) The gift shop of a nonprofit, private hospital has cash revenue of $24,000. What

account will the hospital credit?

A) Unrestricted support

B) Unrestricted revenue

C) Temporarily restricted revenue

D) Other operating revenue – unrestricted

11) An increase in the riskiness of corporate bonds will ________ the price of corporate

bonds and ________ the price of Treasury bonds, everything else held constant

A) increase; increase

B) reduce; reduce

C) reduce; increase

D) increase; reduce

12) In a nonprofit, nongovernmental hospital, courtesy allowances are

A) charity care services

B) revenue deductions

C) expenses

D) revenues earned even if the standard charge is above or below the allowance

13) According to the liquidity premium theory of the term structure

A) because buyers of bonds may prefer bonds of one maturity over another, interest

rates on bonds of different maturities do not move together over time

B) the interest rate on long-term bonds will equal an average of short-term interest rates

that people expect to occur over the life of the long-term bonds plus a term premium

C) because of the positive term premium, the yield curve will not be observed to be

downward sloping

D) the interest rate for each maturity bond is determined by supply and demand for that

maturity bond

14) Which of the following hedging strategies would a business most likely use?

A) An importer will want to hedge his foreign denominated accounts receivable and

will purchase forward contracts to hedge an exposed net asset position

B) An importer will want to hedge his foreign denominated accounts payable and will

purchase forward contracts to hedge an exposed net liability position

C) An exporter will want to hedge his foreign denominated accounts receivable and will

purchase forward contracts to hedge an exposed net liability position

D) An exporter will want to hedge his foreign denominated accounts payable and will

purchase forward contracts to hedge an exposed net liability position

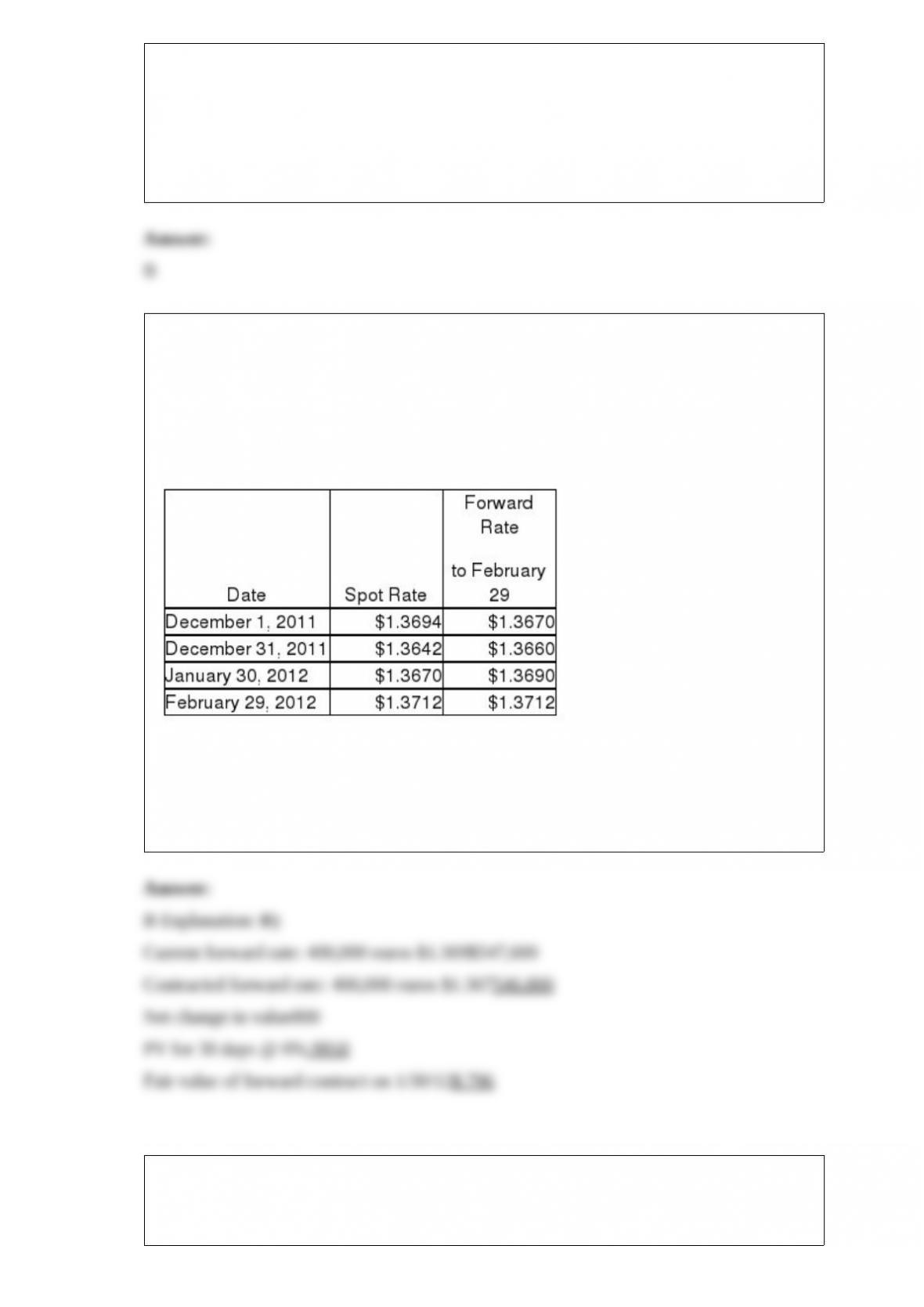

15) On December 1, 2011, Thomas Company, a U.S. corporation, purchases inventory

from a vendor in Italy for 400,000 euros. Payment is due in 90 days. To hedge the

transaction, Thomas signs a forward contract to buy 400,000 euros in 90 days at

$1.3670. Thomas uses a discount rate of 6% (present value factor for 30 days = .9950;

60 days = .9901; 90 days = .9851). Assume the forward contract will be settled net and

this is a cash flow hedge. Currency exchange rates are shown below:

What is the fair value of the forward contract at January 30?

A) $796 liability

B) $796 asset

C) $800 liability

D) $800 asset

16) Mary Contrary is the executor for the estate of Belle Silver. Belle owned a home

with a fair value of $200,000. The home has a remaining mortgage amount of $80,000.

Mary also has personal effects worth $8,000, an investment portfolio with a fair value

of $150,000 on the date of death, and approximately $7,500 in cash in various accounts.

The home was left to her daughter in the valid will that Belle had executed prior to her

death.

Belle did not have a surviving spouse, but her daughter is a minor, who is independently

wealthy after inventing a cutting-edge software program. The state in which Belle

resided, allows a $15,000 homestead allowance, and a $10,000 personal effects

entitlement.

After taking an inventory, and converting all of the assets, except for the home and the

personal effects, into cash, there is $159,000 for Mary to distribute to the appropriate

devises, beneficiaries, and creditors.

Mary has identified the following expenses and devises:

1>Belle’s unpaid final medical expenses were $24,000.

2>Belle left a devise of $100,000 to her church.

3>The costs and expenses of administering the estate were $21,000.

4>Real estate taxes of $3,600 are past due.

5>The unpaid funeral expenses were $8,700.

Required:

Prepare a schedule that will list the disbursements of assets. Assume that the state in

which Belle resided has adopted the Uniform Probate Code.

17) Pashley Corporation purchased 75% of Sargent Corporation on January 1, 2011, for

$115,000. Balance sheets for the two companies on this date, prepared just prior to the

purchase, are provided below.

PashleySargentSargent

Book ValuesBook ValuesFair Values

Cash$165,000$5,000$5,000

Inventory135,00035,00045,000

Buildings & equipment-net250,00060,00095,000

Total assets$550,000$100,000$145,000

Common stock$150,000$47,500

Retained earnings400,00052,500

Total equities$550,000$100,000

Required:

Prepare a consolidated balance sheet using the entity theory of consolidation.

18) The balance sheet of the partnership of Jim, Kim, and Larry is shown below as of

September 1, 2011 . The partners had decided to dissolve the partnership earlier in the

year, and all assets were converted into cash and all partnership liabilities were paid.

The remains of the partnership (with partner residual profit and loss sharing

percentages) was as follows:

Cash$150,000Jim, capital (20%)$(300,000)

Kim, capital (40%)(150,000)

Larry, capital (40%)600,000

Total assets$150,000Total liab./equity$150,000

The value of partners’ personal assets and liabilities on July 1, 2011 were as follows:

JimKimLarry

Personal assets$450,000$370,000$400,000

Personal liabilities200,000210,000195,000

Required:

Prepare the final statement of partnership liquidation.

19) On July 1, 2011, Joe, Kline, and Lama began a partnership in which Joe and Kline

each contributed cash of $200,000; and Lama contributed property with a fair value of

$100,000 and a tax basis $150,000. Joe receives a 10% bonus of partnership income.

Kline and Lama receive salaries of $40,000 each. The partnership agreement of Joe,

Kline, and Lama provides that all partners receive 5% interest on capital and that profits

and losses of the remaining income be distributed to Joe, Kline, and Lama by a 1:1:3

ratio.

Required:

Prepare a schedule to distribute $225,000 of partnership net income to the partners.

20) Middlefield County incurred the following transactions during 2011:

1>The county authorized a new general obligation bond issue of $5 million par to

construct an office building with a contract price of $4,975,000. The bonds were issued

for $4,980,000.

2>The county levied real property taxes of $10,000,000. Eighty-five percent of the net

taxes were collected immediately. Two percent of the total levy was estimated to be

uncollectible.

3>The office building was completed and the county paid the contract price to the

contractor.

4>The General Fund transferred $500,000 to the Debt Service Fund.

5>The county paid $200,000 for interest on the bonds from the Debt Service Fund.

Required:

Prepare journal entries for each of the above transactions. Identify the appropriate fund

or funds used by Middlefield County.

21) On November 4, 2011, the Oak Corporation, a U.S. corporation, purchased

components for an assembly machine from Maple Industries, a Canadian Company,

which were put into Parts Inventory. The purchase price was 80,000 Canadian dollars

and Oak agreed to pay in Canadian dollars in 90 days. Both corporations are on a

calendar year accounting period. Assume that the spot rates for the Canadian dollar on

November 4, 2011, December 31, 2011, and February 2, 2012, are $0.9985, $1.0191,

and $1.0064, respectively.

Required:

Record the November 4, December 31, and February 2 transactions in the General

Journals of Oak Corporation and Maple Industries. If no entry is required on a

particular date, indicate “No entry” in the General Journal.

22) The profit and loss sharing agreement for the Jill, Kelly, and Lila partnership

provides that each partner receives a bonus of 5% on the original amount of partnership

net income if net income is above $25,000. Jill and Kelly receive a salary allowance of

$7,500 and $10,500, respectively. Lila has an average capital balance of $260,000, and

receives a 10% interest allocation on the amount by which her average capital account

balance exceeds $200,000. Residual profits and losses are allocated to Jill, Kelly, and

Lila in their respective ratios of 7:5:8.

Required:

Prepare a schedule to allocate $88,000 of partnership net income to the partners.