1) What would be an advantage of having all countries adopt and follow the same

accounting standards?

a.Agreement

b.Comparability

c.Lower preparation costs

d.Comparability and lower preparation costs

2) Which of the following is not one of the basic questions that must be answered

before the amount of depreciation charge can be computed?

a.What is the depreciation base to use for the asset?

b.What is the asset’s useful life?

c.What method of cost apportionment is best for this asset?

d.What product or service is the asset related to?

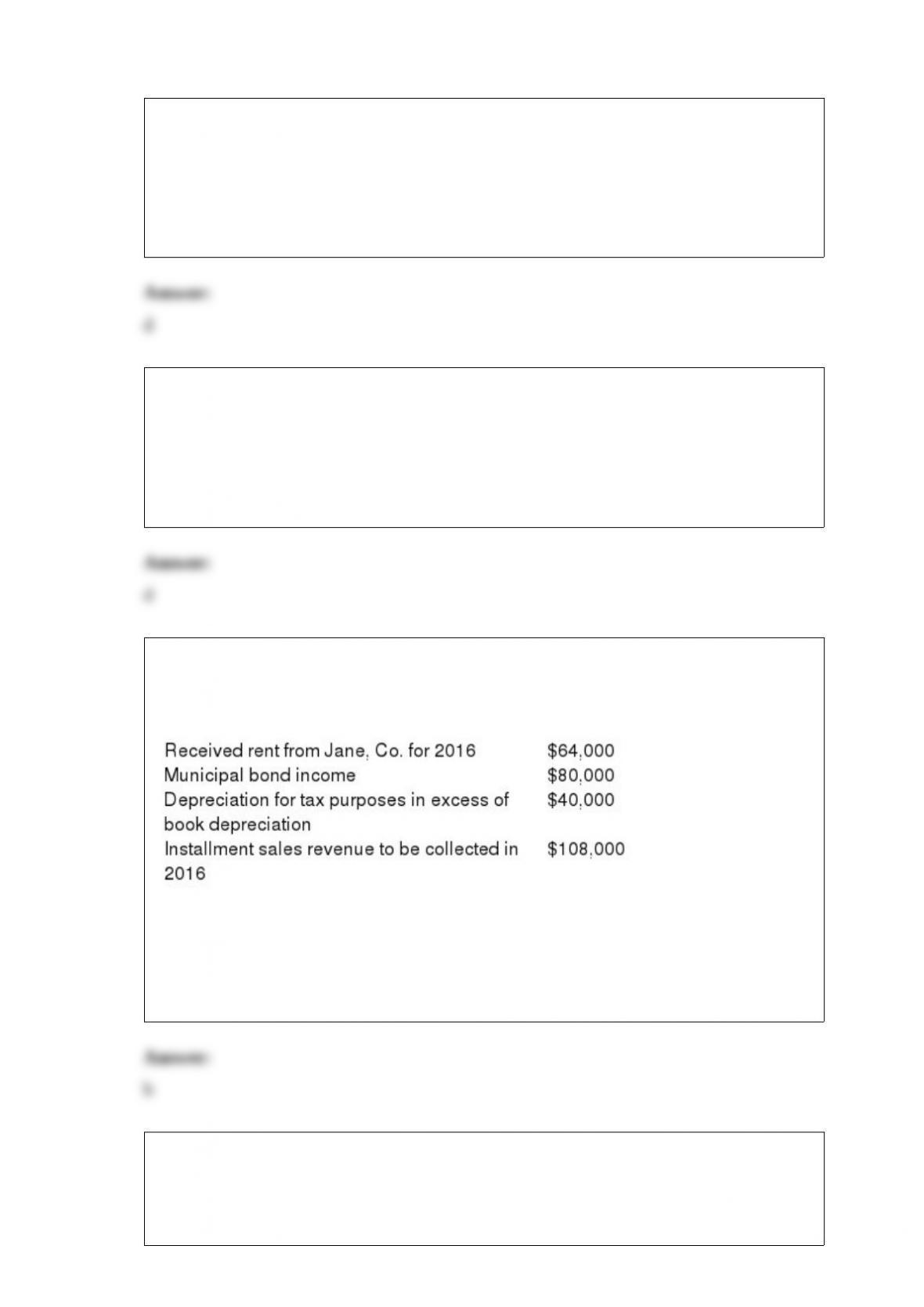

3) Rowen, Inc. had pre-tax accounting income of $1,800,000 and a tax rate of 40% in

2015, its first year of operations. During 2015 the company had the following

transactions:

For 2015, what is the amount of income taxes payable for Rowen, Inc?

a.$603,200

b.$654,400

c.$686,400

d.$772,800

4) Dividends are not paid on

a.noncumulative preferred stock

b.nonparticipating preferred stock

c.treasury common stock

d.Dividends are paid on all of these

5) When an investor’s accounting period ends on a date that does not coincide with an

interest receipt date for bonds held as an investment, the investor must

a.make an adjusting entry to debit Interest Receivable and to credit Interest Revenue for

the amount of interest accrued since the last interest receipt date

b.notify the issuer and request that a special payment be made for the appropriate

portion of the interest period

c.make an adjusting entry to debit Interest Receivable and to credit Interest Revenue for

the total amount of interest to be received at the next interest receipt date

d.do nothing special and ignore the fact that the accounting period does not coincide

with the bond’s interest period

6) Acceptable depreciation methods under IFRS include

a.Straight-line

b.Accelerated

c.Units-of-production

d.All of these answers are correct

7) Which of the following is not an acceptable way of displaying the components of

other comprehensive income?

a.Combined statement of retained earnings

b.One statement approach

c.Two statement approach

d.All of these are acceptable ways

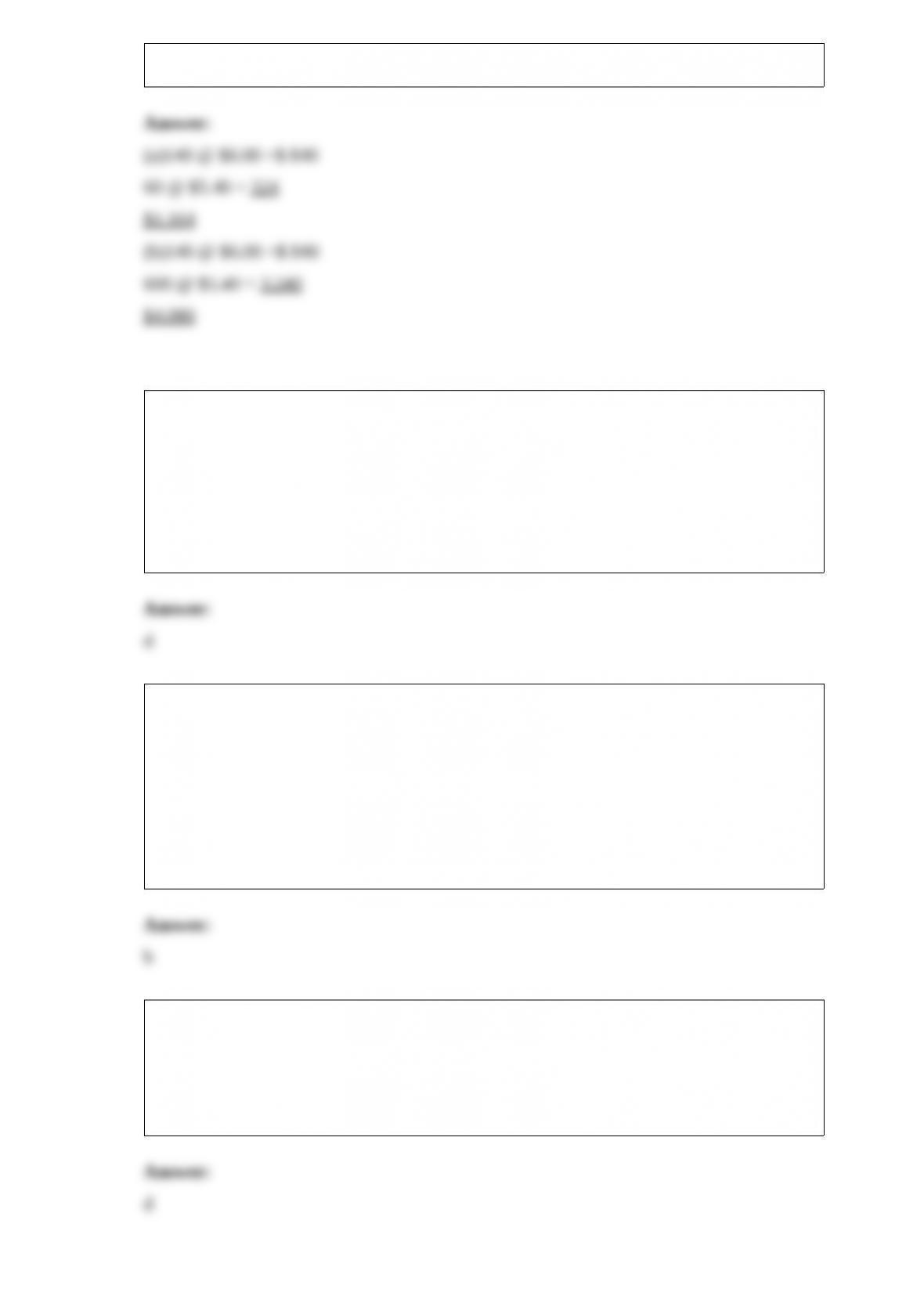

8) The Rock Shop shows the following data related to an item of inventory:

Inventory, January 1200 units @ $5.00

Purchase, January 9600 units @ $5.40

Purchase, January 19140 units @ $6.00

Inventory, January 31200 units

Instructions

(a)What value should be assigned to the ending inventory using FIFO?

(b)What value should be assigned to cost of goods sold using LIFO?

9) Lynne Corporation acquired a patent on May 1, 2014 . Lynne paid cash of $45,000 to

the seller. Legal fees of $1,000 were paid related to the acquisition. What amount

should be debited to the patent account?

a.$1,000

b.$44,000

c.$45,000

d.$46,000

10) Turner Corporation acquired two inventory items at a lump-sum cost of $100,000.

The acquisition included 3,000 units of product LF, and 7,000 units of product 1B. LF

normally sells for $30 per unit, and 1B for $10 per unit. If Turner sells 1,000 units of

LF, what amount of gross profit should it recognize?

a.$3,750

b.$11,250

c.$20,000

d.$23,750

11) Stock dividends distributable should be classified on the

a.income statement as an expense

b.balance sheet as an asset

c.balance sheet as a liability

d.balance sheet as an item of stockholders’ equity

12) Benjamin Company uses IFRS, while Iris, Inc. uses U.S. GAAP, for their external

financial reporting. On January 16, 2015, both companies settled lawsuits relating to

industrial accidents that occurred in 2013 . Benjamin Company paid $550,000 and Iris,

Inc.

paid $230,000. Assuming that no accrual had been previously made, what amount of

loss

should be reported on the income statement for the year ended December 31, 2014 for

each company?

Benjamin CompanyIris, Inc.

a.$-0-$-0-

b.$550,000$230,000

c.$-0-$230,000

d.$550,000$-0-

13) Bishop Co. began operations on January 1, 2014 . Financial statements for 2014 and

2015 con- tained the following errors:

Dec. 31, 2014Dec. 31, 2015

Ending inventory$132,000 too high$146,000 too low

Depreciation expense84,000 too high

Insurance expense60,000 too low60,000 too high

Prepaid insurance60,000 too high

In addition, on December 31, 2015 fully depreciated equipment was sold for $28,800,

but the sale was not recorded until 2016 . No corrections have been made for any of the

errors. Ignore income tax considerations.

The total effect of the errors on Bishop’s 2015 net income is

a.understated by $366,800

b.understated by $234,800

c.overstated by $117,200

d.overstated by $249,200

14) Rich, Inc. acquired 30% of Doane Corporation’s voting stock on January 1, 2014 for

$800,000. During 2014, Doane earned $320,000 and paid dividends of $200,000. Rich’s

30% interest in Doane gives Rich the ability to exercise significant influence over

Doane’s operating and financial policies. During 2015, Doane earned $400,000 and paid

dividends of $120,000 on April 1 and $120,000 on October 1 . On July 1, 2015, Rich

sold half of its stock in Doane for $528,000 cash.

What should be the gain on sale of this investment in Rich’s 2015 income statement?

a.$128,000

b.$110,000

c.$98,000

d.$80,000