1) The stock dividends distributable account is listed in the current liability section of

the balance sheet.

2) The cost of a patent with a remaining legal life of 10 years and an estimated useful

life of 7 years is amortized over 10 years.

3) Job order cost systems can be used to compare unit costs of similar jobs to determine

if costs are staying within expected ranges.

4) The production budget is the starting point for preparation of the direct labor cost

budget.

5) A new partner contributes accounts receivable to a partnership which appear in the

ledger of his sole proprietorship at $20,500 and there was an allowance for doubtful

accounts of $750. If $600 of the accounts receivables are completely worthless, the

partnership accounts receivable should be debited for $19,900.

6) The difference between deferred revenue and accrued revenue is that accrued

revenue has been recorded and needs adjusting and deferred revenue has never been

recorded.

7) The adoption of variable costing for managerial decision making is based on the

premise that fixed factory overhead costs are related to productive capacity of the

manufacturing plant and are normally not affected by the number of units produced.

8) When estimated costs are used in applying the cost-plus approach to product pricing,

the estimates should be based upon ideal levels of performance.

9) The balance sheet accounts are referred to as real or permanent accounts.

10) For years one through five, a proposed expenditure of $250,000 for a fixed asset

with a 5-year life has expected net income of $40,000, $35,000, $25,000, $25,000, and

$25,000, respectively, and net cash flows of $90,000, $85,000, $75,000, $75,000, and

$75,000, respectively. The cash payback period is 3 years.

11) Responsibility accounting reports that are given to lower level managers are usually

very detailed, in turn, higher level managers will be given a summary report.

12) In net present value analysis for a proposed capital investment, the expected future

net cash flows are reduced to their present values.

13) The process cost system is appropriate where few products are manufactured and

each product is made to customers’ specifications.

14) If fixed costs are $850,000 and the unit contribution margin is $50, profit is zero

when 15,000 units are sold.

15) One of the most important differences between a service business and a retail

business is in what is sold.

16) The retained earnings statement may be combined with the income statement.

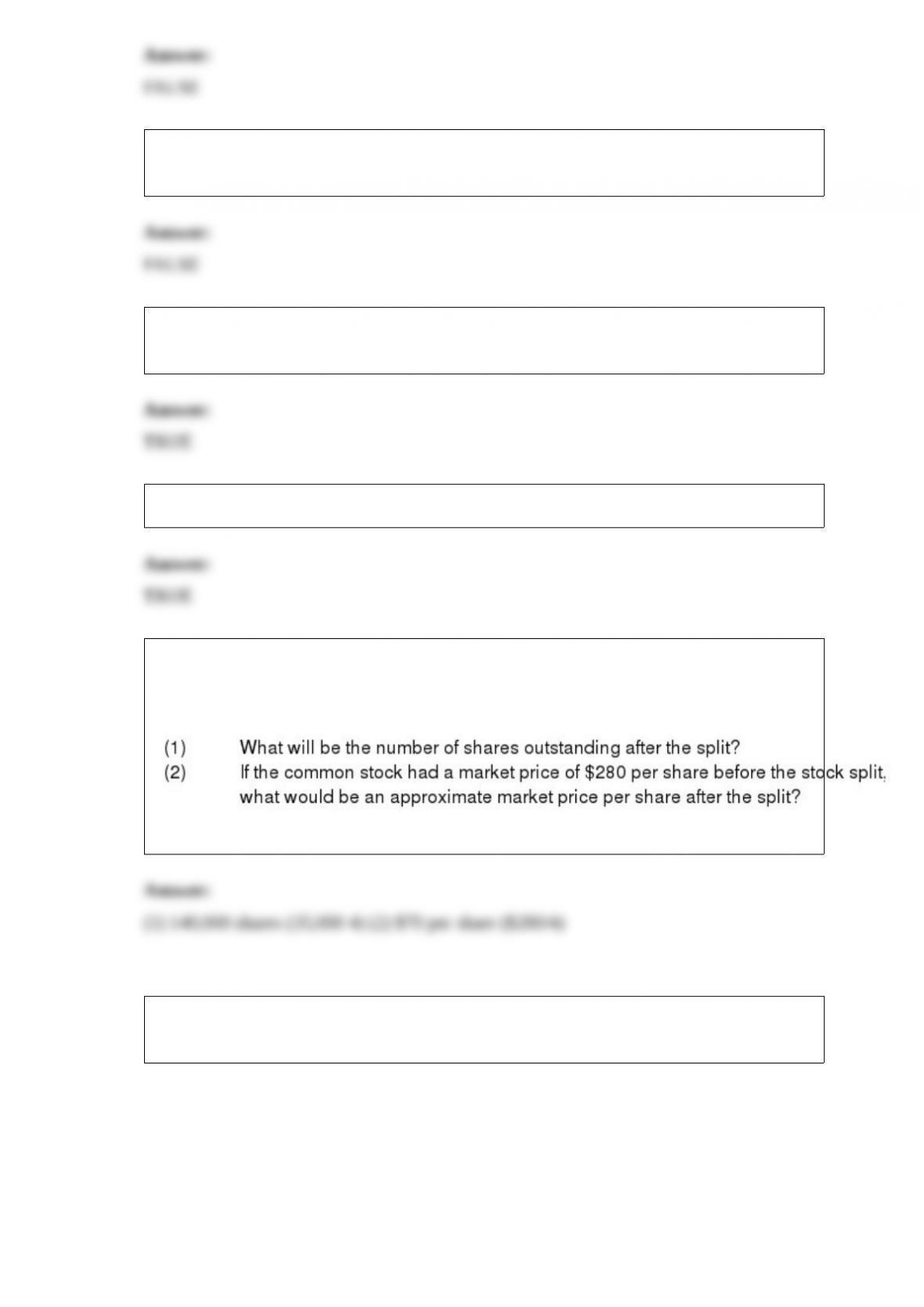

17) Marcos Company, which had 35,000 shares of common stock outstanding, declared

a 4-for-1 stock split.

Required:

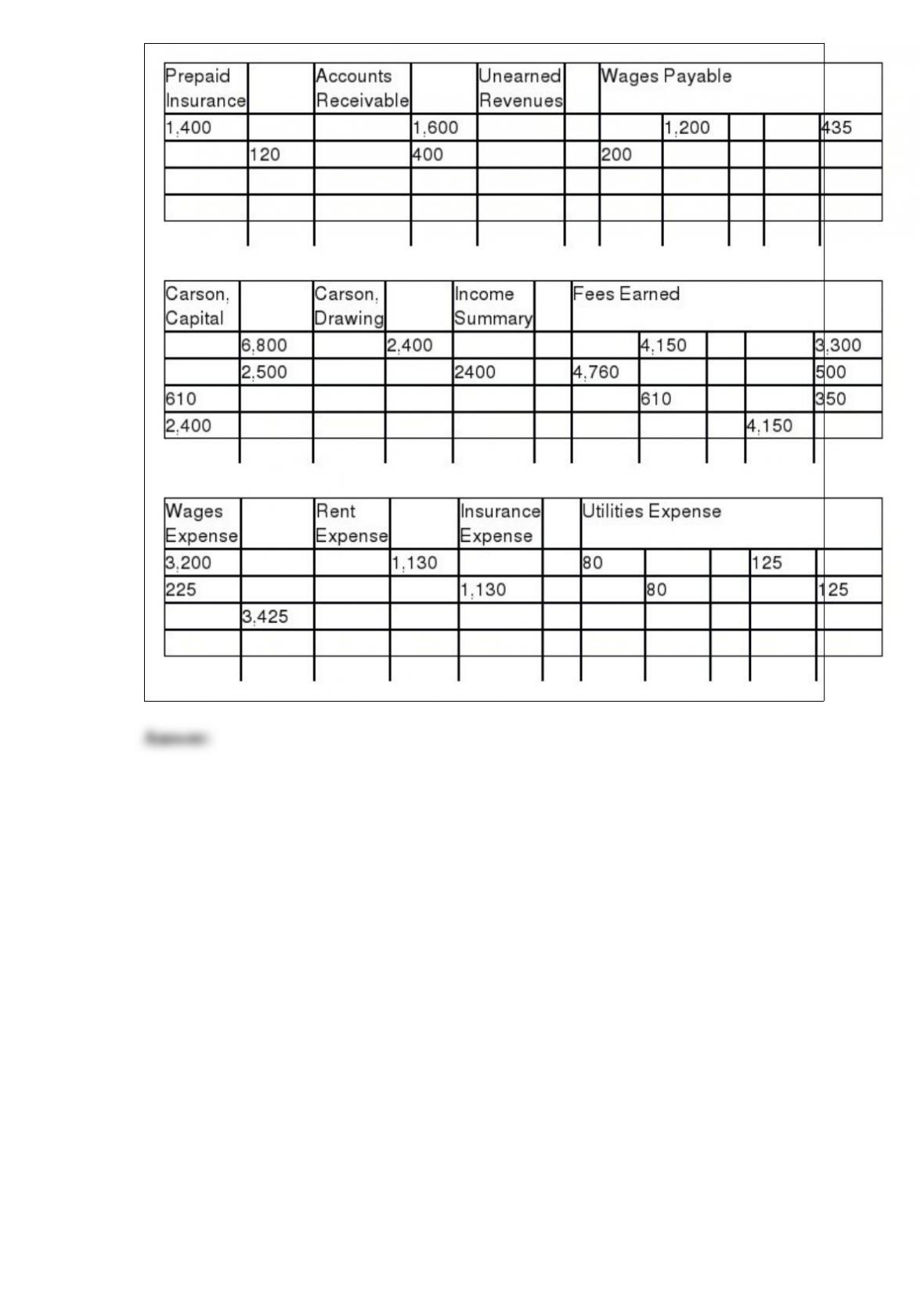

18) Prepare an income statement and a statement of owners equity for the month ended

September 30, 2010 from the T-accounts below of Carson Company.

19) Macon Co. acquired drilling rights for $7,500,000. The oil deposit is estimated at

37,500,000 gallons. During the current year, 3,000,000 gallons were drilled. Journalize

the adjusting entry at December 31, 2011 to recognize the depletion expense.

Journal

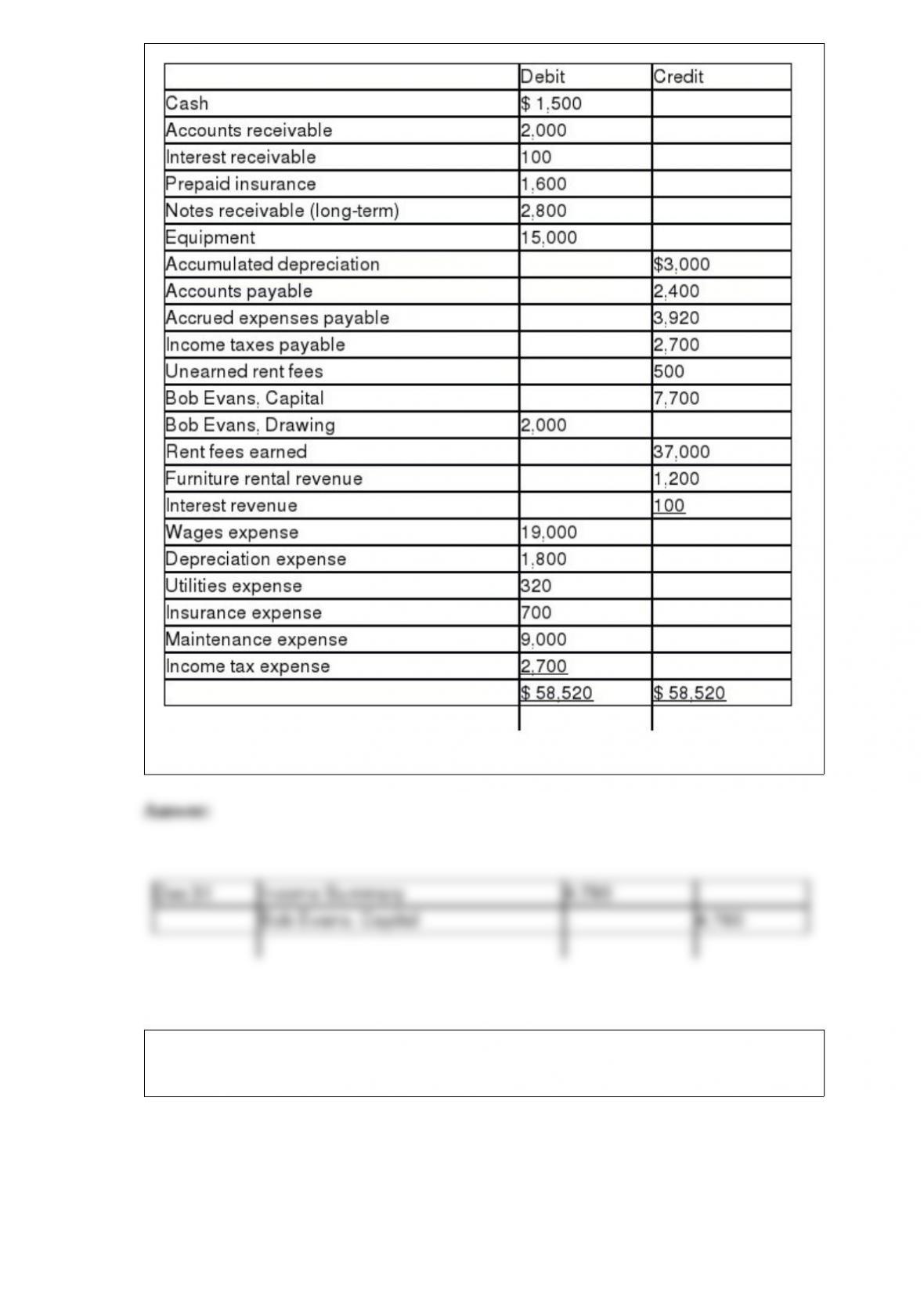

20) Bob Evans owns a business, Beachside Realty, that rents condominiums and

furnishings. Below is the adjusted trial balance at December 31, 2010.

Prepare the closing entry required to transfer the income or loss at the end of the period.

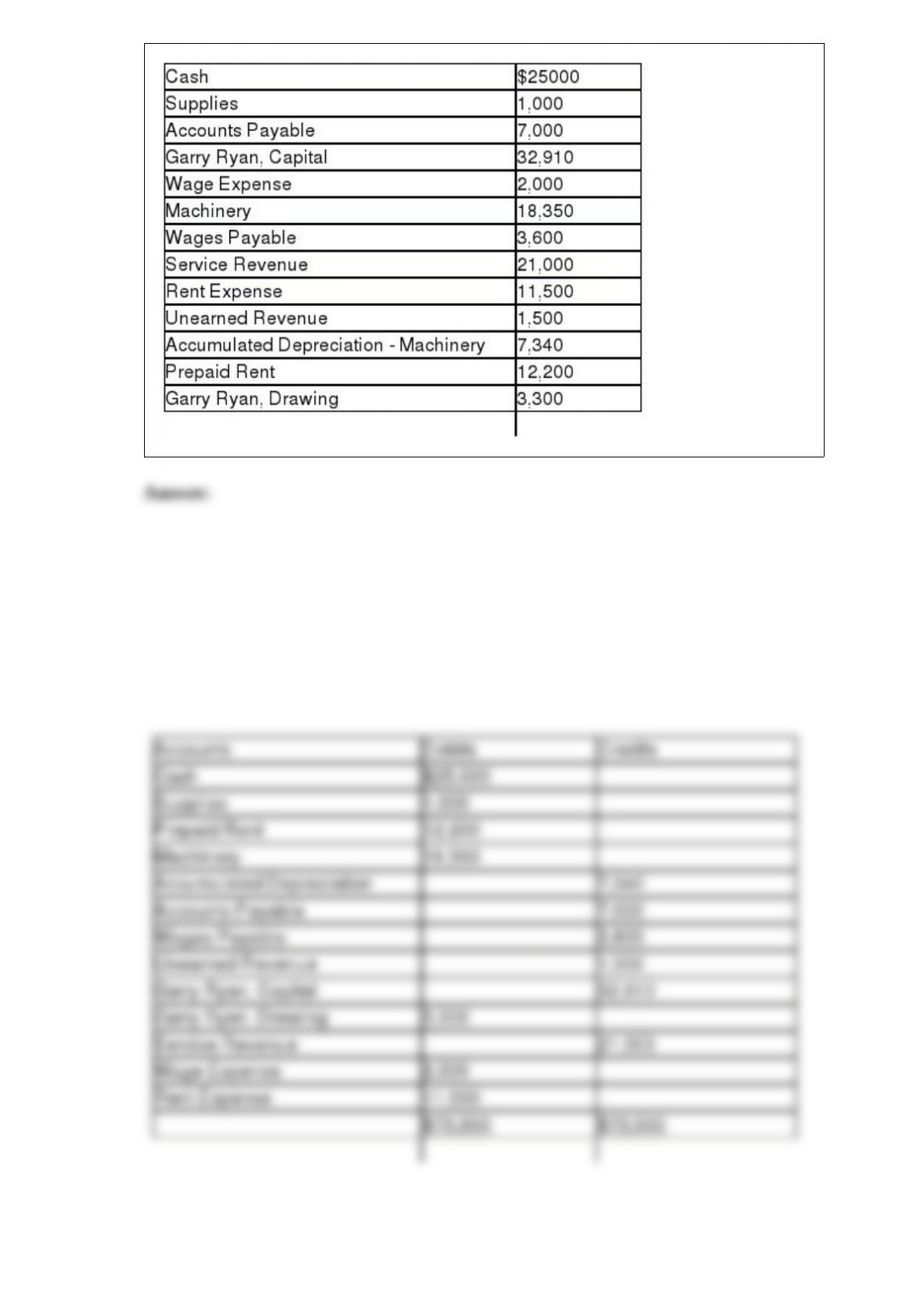

21) Given the following account balances for Garrys Tree Service, prepare a trial

balance.