Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

All employers of one or more persons must file an application for an identification

number.

a. True

b. False

Form 941 is due on or before the 15th day of the month following the close of the

calendar quarter for which the return is made.

a. True

b. False

Selfemployed persons include their selfemployment taxes in their quarterly payment of

estimated federal income taxes.

a. True

b. False

Under the Consumer Credit Protection Act, disposable earnings are the earnings

remaining after any deductions for health insurance.

a. True

b. False

FIT Payable is a liability account used to record employees' withheld federal income tax

and also the employer's match of that tax.

a. True

b. False

Each year, the FICA (OASDI portion) taxable wage base is automatically adjusted

whenever a cost of living raise in social security benefits becomes available.

a. True

b. False

In calculating a "grossup" amount of a bonus payment, an employer does not use the

OASDI/HI tax rates in the formula.

a. True

b. False

To calculate the overtime pay rate for a commissioned worker, divide the total

commission by the hours worked, and then take onehalf of the resulting rate of pay.

a. True

b. False

Before any federal income taxes may be withheld, there must be, or must have been, an

employeremployee relationship.

a. True

b. False

In its definition of employee, FICA clearly distinguishes between classes or grades of

employees.

a. True

b. False

The Social Security Act requires workers to obtain a new account number each time

they change jobs.

a. True

b. False

The SelfEmployment Contributions Act imposes a tax on the net earnings from

selfemployment derived by an individual from any trade or business.

a. True

b. False

Rest periods and coffee breaks may be required by all of the following except:

a. a union contract.

b. a state legislation.

c. a municipal legislation.

d. the FLSA.

e. none of the above.

The FICA taxes on the employer represent both business expenses and liabilities of the

employer.

a. True

b. False

An employer must pay the quarterly FUTA tax liability if the liability is more than:

a. $3,000.

b. $500.

c. $1,000.

d. $1.

e. $100.

The requisition for personnel form is sent to the Payroll Department so that the new

employee can be properly added to the payroll.

a. True

b. False

FUTA was designed to ensure that workers who are covered by pension plans receive

benefits from those plans.

a. True

b. False

Union Dues Payable is a liability account credited with the deductions made from union

members' wages for their union dues.

a. True

b. False

Violators of the overtime provision of the FLSA are required to pay the unpaid overtime

at a rate of triple the employee's rate.

a. True

b. False

When withheld union dues are turned over to the union by the employer, a journal entry

is made debiting the liability account and crediting the cash account.

a. True

b. False

Noncash fringe benefits that are provided employees are treated as nontaxable income

and thus are excluded from federal income tax withholding.

a. True

b. False

Each payday, the total of net pays that the employer incurs is the wage expense that

must be debited.

a. True

b. False

FICA includes partnerships in its definition of employer.

a. True

b. False

Deductions from gross pay in the payroll register are reflected on the credit side of the

journal entry to record the payroll.

a. True

b. False

On Schedule B of Form 941, the employer does not show the date of each tax deposit

during the quarter.

a. True

b. False

Under the federal income tax withholding law, income taxes are not withheld from the

value of meals that employers furnish workers on the employers’ premises for the

employers’ convenience.

a. True

b. False

A waiter receives cash tips amounting to $120 in a month. The waiter must report the

amount of the cash tips to the employer by the 10th of the month following the month

they receive the tips.

a. True

b. False

FICA does not consider the first six months of sick pay as taxable wages.

a. True

b. False

All taxable noncash fringe benefits received during the year can only be added to the

employees' taxable pay on the last payday of the year.

a. True

b. False

Tips received by employees in excess of tip credit amount are not included as

disposable earnings subject to garnishment

a. True

b. False

Under the provisions of the Consumer Credit Protection Act, an employer can discharge

an employee simply because the employee's wage is subject to garnishment for a single

indebtedness.

a. True

b. False

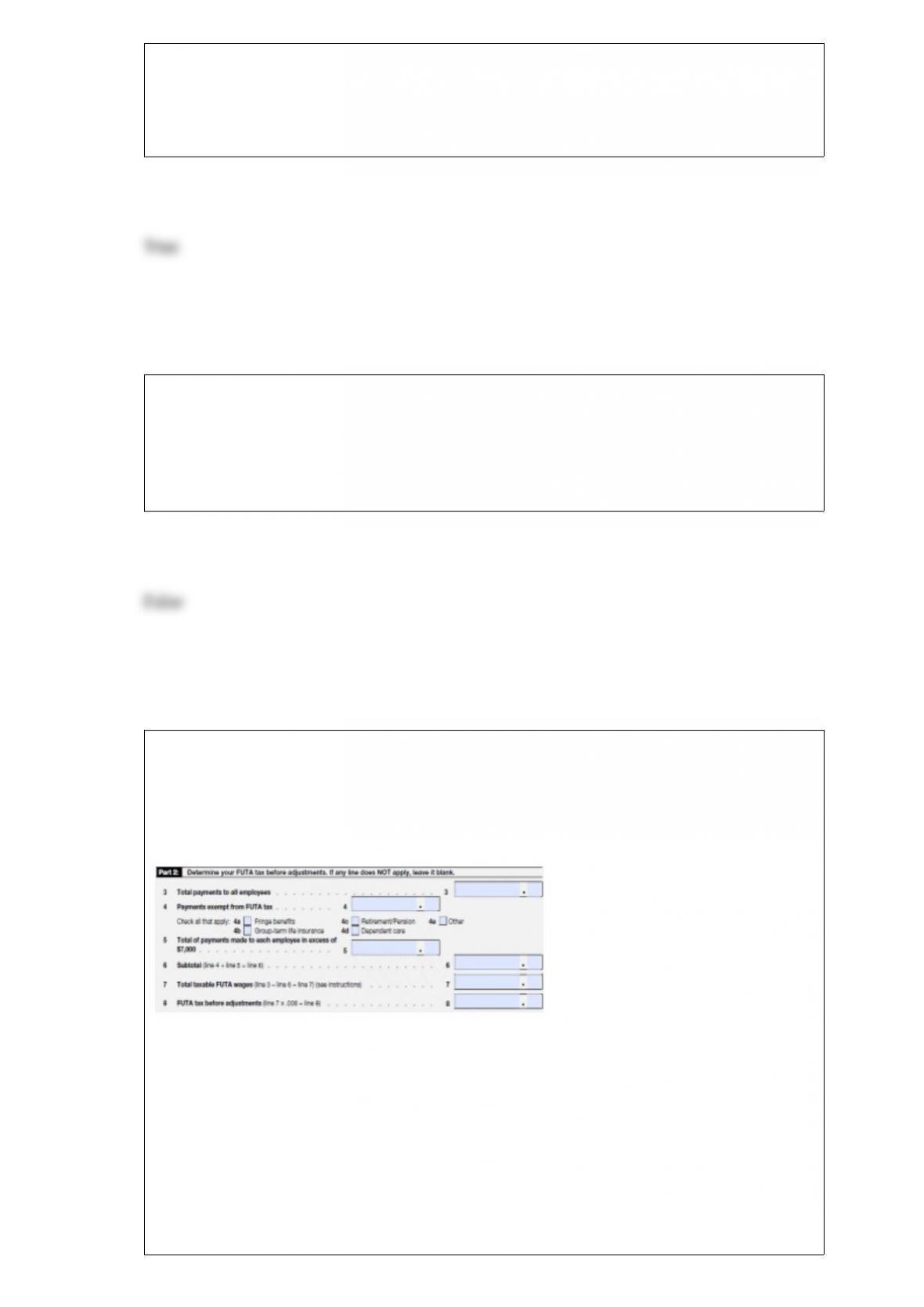

a. Complete Part 2 of Form 940 based on the following information:

Total payroll for the year $913,590

Payroll to employees in excess of $7,000 $421,930

Employer contributions into employees' 401(k) plans $23,710

Source: Internal Revenue Service

b. If the employer is located in California, which has a credit reduction of 1.5%,

what would be the amount of the credit reduction?

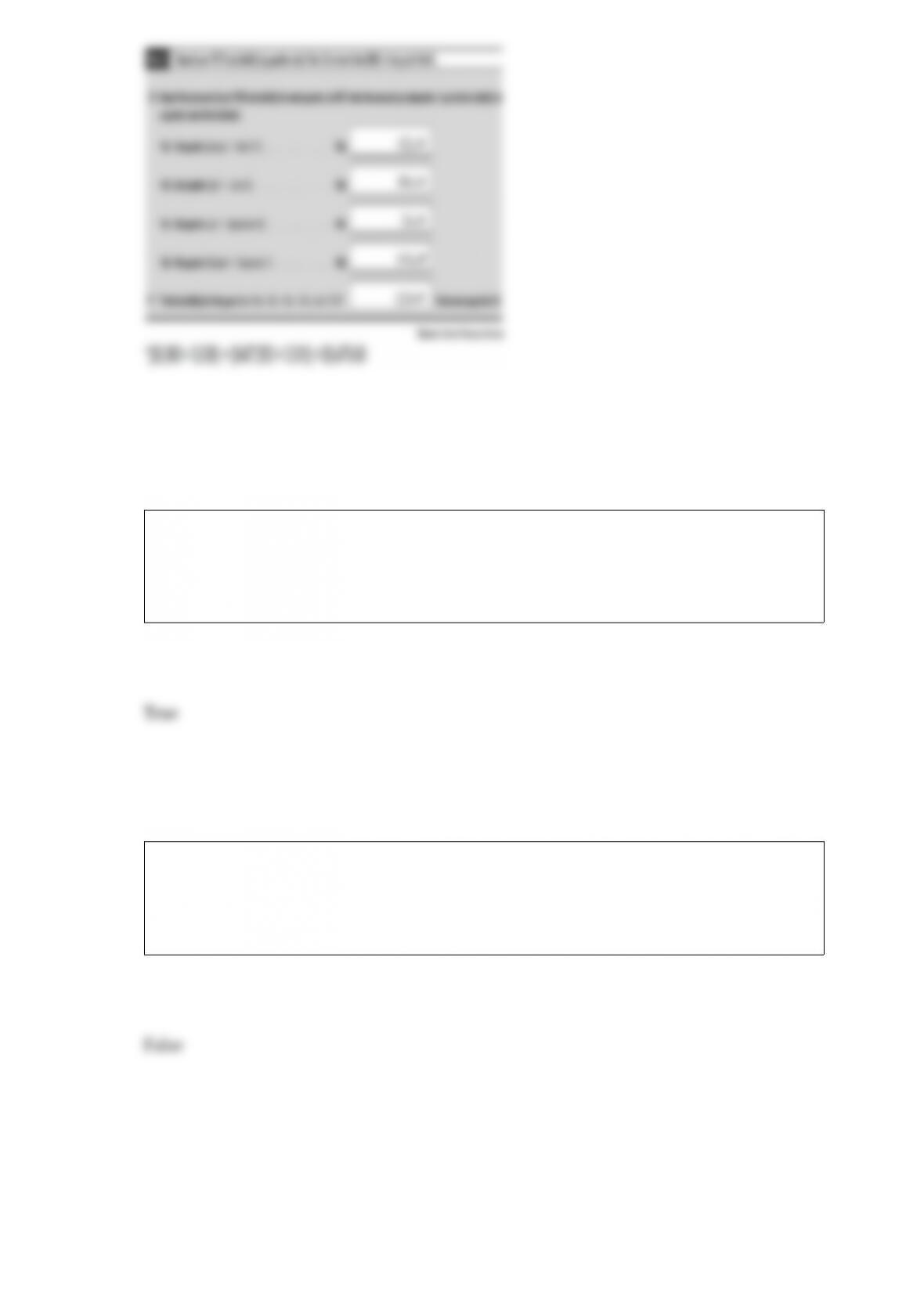

c. Complete Part 5 of Form 940 for the California employer given the breakdown of

FUTA taxable

wages for the year to be:

First quarter $237,000

Second quarter $168,000

Third quarter $54,000

Fourth quarter $8,950

Yearly total $467,950

Monthly depositors are required to deposit their taxes by the 15th day of the following

month.

a. True

b. False

For FUTA purposes, the cash value of remuneration paid in any medium other than cash

is not considered taxable wages.

a. True

b. False