1) For privately held companies who of the following is responsible for establishing

auditing standards?

A) Securities and Exchange Commission

B) Public Company Accounting Oversight Board

C) Auditing Standards Board

D) National Association of Accounting

2) A member in public practice shall neither receive from, nor pay to, a client a

commission when the member or member’s firm also performs certain services for that

client. Are commissions allowed if the CPA performs:

A)

B)

C)

D)

3) Rather than maintain an internal IT center, many companies outsource their basic IT

functions such as payroll to an:

A) external general service provider

B) external application service provider

C) internal control service provider

D) internal auditor

4) If an auditor discovers that previously issued financial statements are misleading, the

most desirable approach to follow is to request that the client issue an immediate

revision of the financial statements containing an explanation of the reasons for the

revision.

A) True

B) False

5) The understatement of sales and accounts receivable is best uncovered by:

A) confirming receivables

B) reviewing the aged trial balance

C) test of transactions for shipments made but not recorded

D) reconciling the accounts receivable general ledger account with the schedule of

accounts receivable

6) In addition to confirming bank balances of your audit client, a bank confirmation

would normally contain:

A) the client’s bank loans with due date, interest rate, and collateral requested

B) the client’s credit history as regards to paying back loans

C) the client’s managements bank account information

D) the client’s business prospects

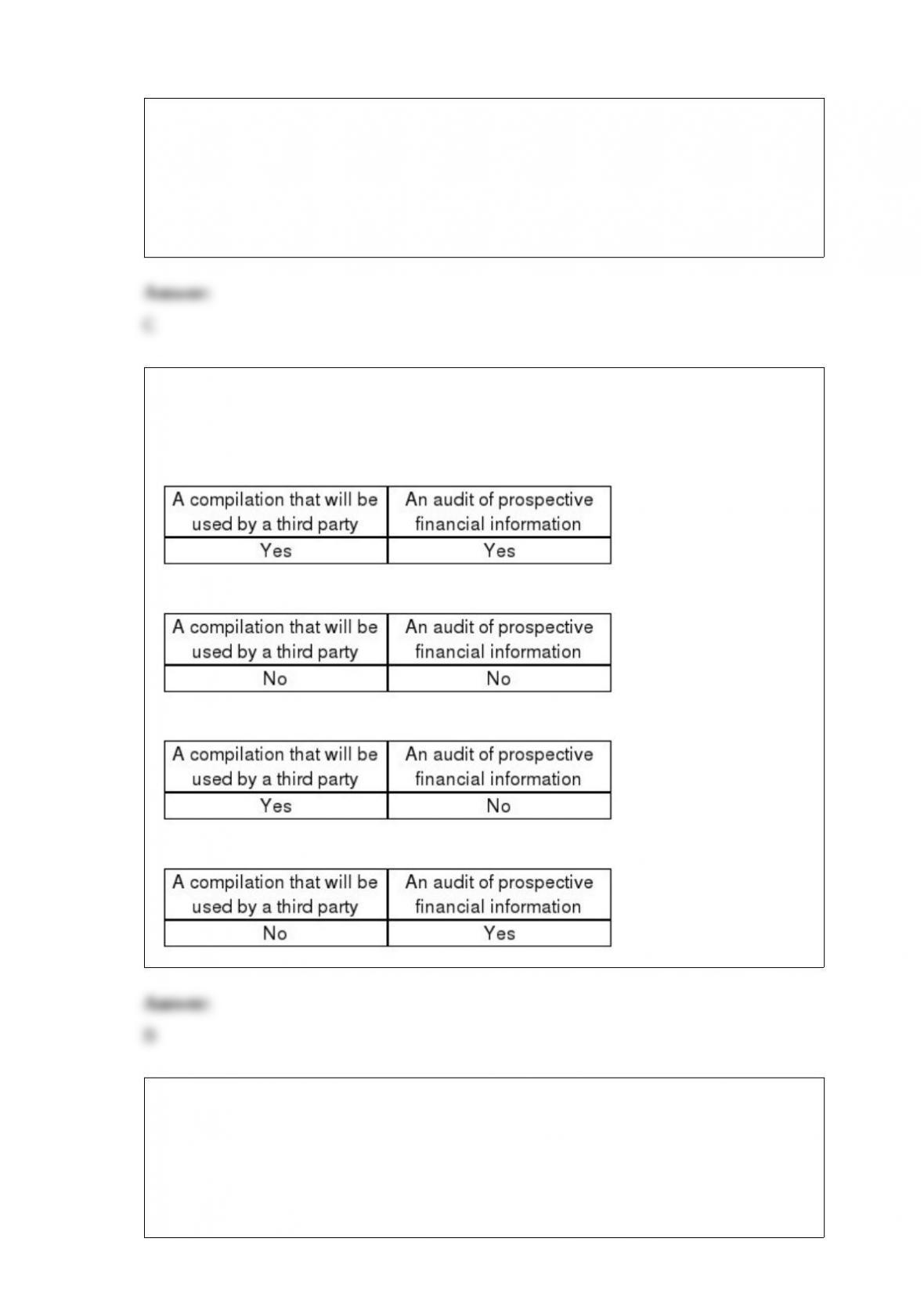

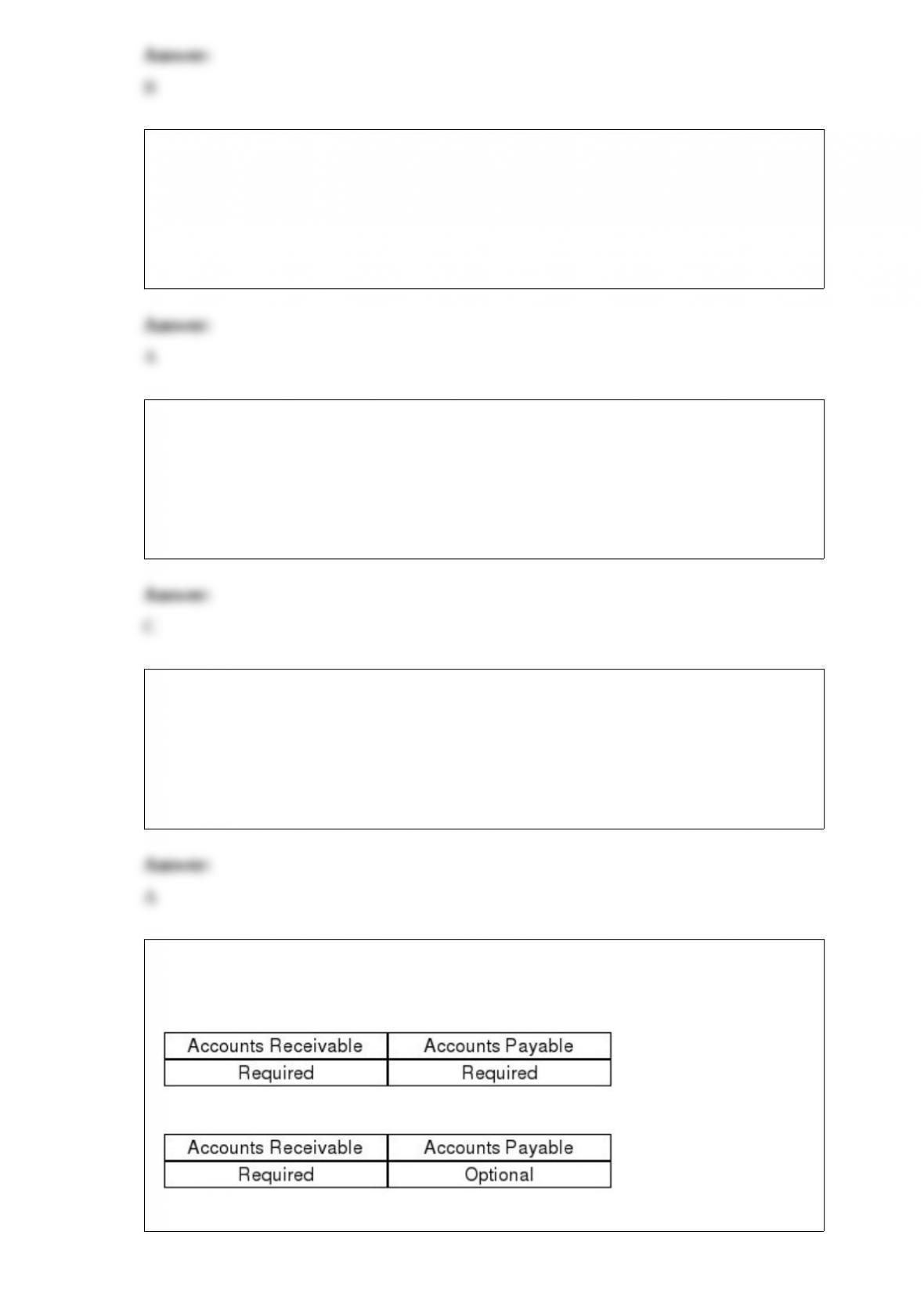

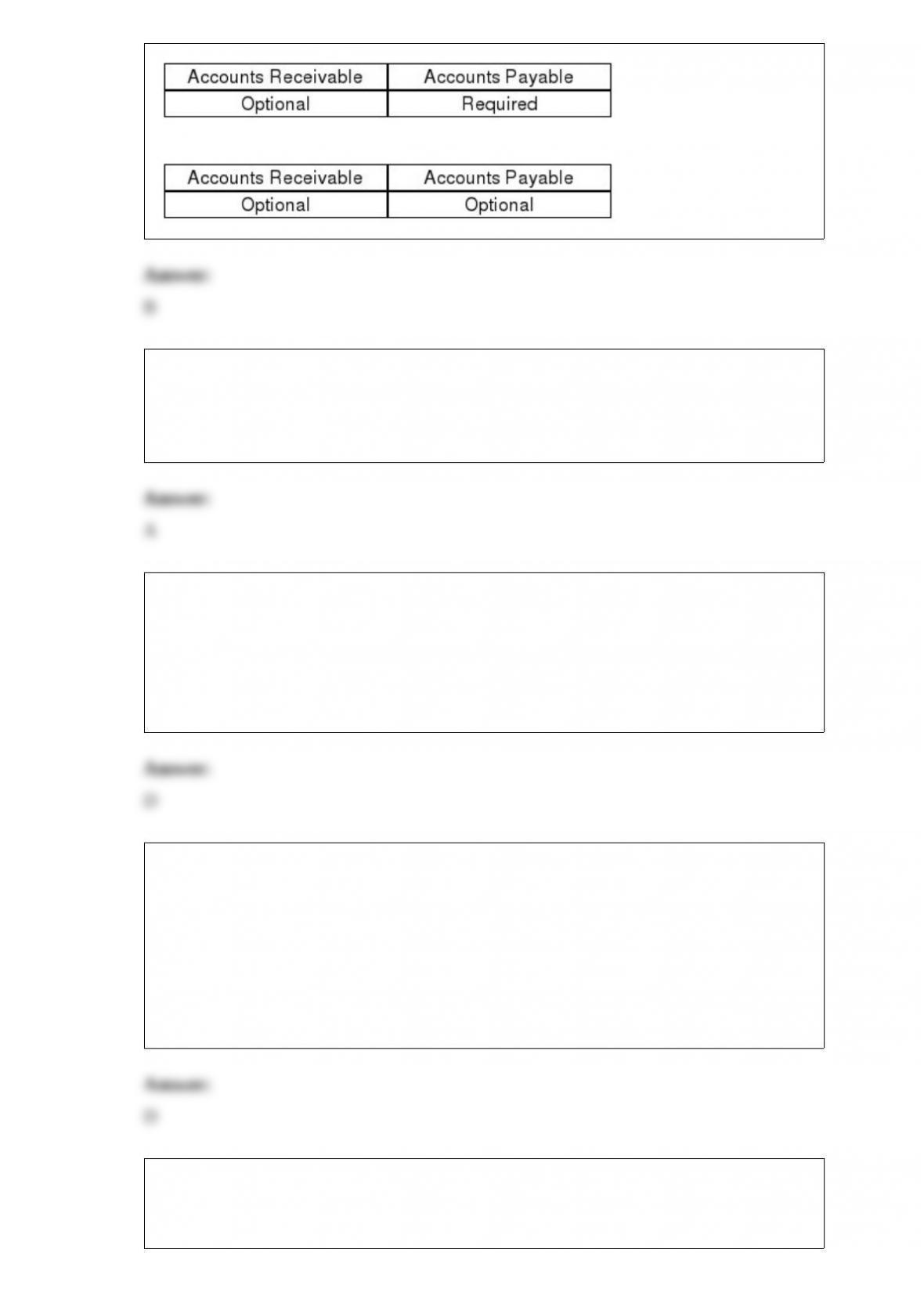

7) Indicate whether confirmation of accounts receivable and accounts payable, provided

they each are significant accounts, is required or optional:

A)

B)

C)

D)

8) The auditor’s review of current year acquisition’s cutoff is normally done as part of

accounts payable cutoff tests.

A) True

B) False

9) Pricing manufactured inventory is difficult. Auditors must evaluate the method of

allocating manufacturing overhead for all but which of the following?

A) reasonableness

B) computational correctness

C) compliance with accounting standards

D) consistency

10) An accountant’s standard report on a compilation of a projection should not include

a:

A) statement that a compilation of a projection is limited in scope

B) separate paragraph that describes the limitations on the presentation’s usefulness

C) disclaimer of responsibility to update the report for events occurring after the report’s

date

D) statement that the accountant expresses only limited assurance that the results may

be achieved

11) An auditor is vouching a sample of hourly employees from the payroll master file to

approved time clock or time sheet data in order to provide evidence that:

A) employees work the number of hours for which they are paid

B) payments are made at the contractual rate

C) product cost information is accurate

D) segregation of duties is present between the payroll function and the payment

function for cash disbursements

12) Inadequate controls and misstatements discovered through tests of controls and

substantive tests of transactions are an indication of the likelihood of misstatements in:

A) the balance sheet

B) the income statement

C) the cash flow statement

D) both the income statement and the balance sheet

13) Auditing standards (SAS No. 99 and SAS No. 54) require the auditor to

communicate all management frauds and illegal acts to the audit committee:

A) only if the act is immaterial

B) only if the act is material

C) only if the act is highly material

D) regardless of materiality

14) A type of positive confirmation known as a blank confirmation:

A) requests the recipient to fill in the amount of the balance

B) is considered less reliable than the regular positive confirmation

C) generates as high a response rate as the regular positive confirmation form

D) is used when the auditor is confirming several small balances

15) The primary characteristic that distinguishes property, plant, and equipment from

inventory, prepaid expenses, and investments is the intention to use property, plant, and

equipment as a part of the operations of the client’s business over their expected life.

A) True

B) False

16) When auditing a client that uses batch processing the problem with error detection

is that:

A) transaction trails in a batch system are available only for a limited period of time

B) there are time delays in processing transactions in a batch system

C) errors in some transactions cause rejection of other transactions in the batch

D) random errors are more likely in a batch system than in an online system

17) The auditor’s best estimate of the population exception rate is the:

A) current year’s sample exception rate

B) tolerable exception rate

C) prior year’s sample exception rate

D) computed upper exception rate

18) If a prospective client has been audited in the past, the successor auditor will

typically rely solely on the representations about the client by the predecessor auditor.

A) True

B) False

19) The third general standard states that due care is to be exercised in the performance

of an audit. This standard is generally interpreted to require:

A) objective review of the adequacy of the technical training of firm personnel

B) thorough review of the existing internal control structure

C) critical review of work done at every level of supervision

D) periodic review of a CPA firm’s quality control procedures

20) Which are prospective financial statements that present an entity’s expected

financial position, results of operations, and cash flows, to the best of the responsible

party’s knowledge and belief?

A)

B)

C)

D)

21) Auditors are normally more concerned about violations of the completeness

objective for acquisitions than about violations of the occurrence objective for

acquisitions.

A) True

B) False

22) Hansen Corporation’s stock is listed on a national stock exchange and registered

with the Securities and Exchange Commission. Hansen’s management hires a CPA to

perform an independent audit of Hansen’s financial statements. The primary objective

of this audit is to provide assurance to the:

A) investors in Hansen Corporation’s stock

B) stock exchange

C) Securities and Exchange Commission

D) management of Hansen Corporation

23) The conjoined sample exception rate is the auditor’s “best estimate” of the actual

exception rate in the entire population.

A) True

B) False

24) Auditors may assess inherent risk and control risk:

A)

B)

C)

D)

25) Which of the following is an internal control weakness for a company whose

inventory of supplies consists of a large number of individual items?

A) The cycle basis is used for physical counts

B) Supplies of relatively little value are expensed when purchased

C) Perpetual inventory records are maintained only for items of significant value

D) The storekeeper is responsible for maintenance of perpetual inventory records

26) The criterion used by most merchandising and manufacturing clients for

determining when revenue recognition takes place is whether title to the goods has

passed.

A) True

B) False

27) In monetary-unit sampling, the values of the estimated likely maximum

misstatements are referred to as the:

A) point estimates

B) precision intervals

C) confidence intervals

D) misstatement bounds

28) A proof of cash receipts is not useful for uncovering the theft of cash receipts or the

recording and deposit of an improper amount of cash.

A) True

B) False

29) To best ascertain that a company has properly included merchandise that it owns in

its ending inventory, the auditor should review and test the:

A) terms of the open purchase orders

B) purchase cutoff procedures

C) contractual commitments made by the purchasing department

D) purchase invoices received on or around year-end

30) All of the following are conditions requiring a departure from a standard

unqualified audit report except:

A) management refused to allow the auditor to confirm significant accounts receivable

for which there were no alternative procedures performed

B) Mmnagement decided not to allow the auditor to confirm significant accounts

receivable, but the auditor obtained sufficient appropriate evidence by examining

subsequent cash receipts

C) part of the audit was performed by other auditors whose report was furnished to the

principle auditor

D) management has determined that fixed assets should be reported in the balance sheet

at their replacement values rather than historical costs. The auditors do not concur

31) Programmers should do all but which of the following?

A) Test programs for proper performance

B) Evaluate representational faithfulness of transaction data input

C) Develop flowcharts for new applications

D) Programmers should perform each of the above

32) Tests of controls and substantive tests of transactions are an important determinant

of the extent of the auditor’s use of tests of details of balances. Which of the following

is true?

A) They are likely to be performed prior to the clients end of the fiscal year

B) They are likely to eliminate the need for tests of details of balances

C) They are likely to have no impact on the planned tests of details of balances

D) They are likely to be used only in the audit of internal control

33) An effective procedure to test for unbilled shipments is to trace from the:

A) sales journal to the shipping documents

B) shipping documents to the sales journal

C) sales journal to the accounts receivable ledger

D) sales journal to the general ledger sales account

34) Which of the following audit procedures used to obtain an understanding of the

client’s general controls would the auditor use to identify program changes in

application software?

A) interviews with IT personnel

B) examination of system documentation

C) reviews of detailed questionnaires completed by the IT staff

D) review of the client’s IT architecture

35) Acceptable audit risk and the amount of substantive evidence required are inversely

related.

A) True

B) False

36) Which of the following is a form of earnings management in which revenues and

expenses are shifted between periods to reduce fluctuations in earnings?

A) fraudulent financial reporting

B) expense smoothing

C) income smoothing

D) each of the above is correct

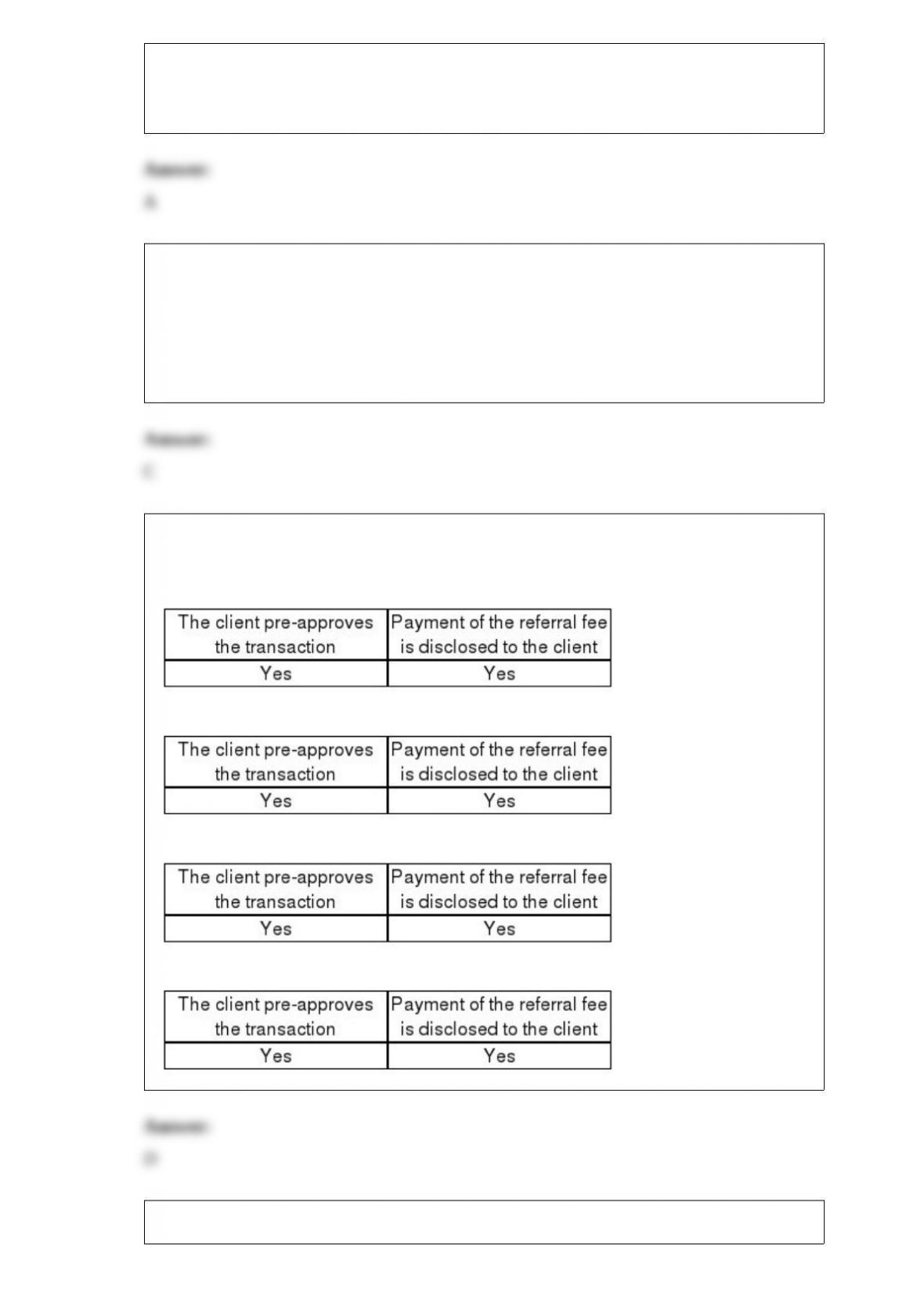

37) A CPA is allowed to accept a referral fee for recommending a client to another CPA

if:

A)

B)

C)

D)

38) The objective of the computer audit technique known as the test data approach is to

determine whether the client’s computer programs can correctly process valid and

invalid transactions.

A) True

B) False

39) Describe two ways the verification of existence and tests for omissions of the

client’s insurance policies in force can be performed.

40) Discuss the purposes of (1) substantive tests of transactions, (2) tests of controls,

and (3) tests of details of balances. Give an example of each.

41) List and describe the six organizational structures available to CPA firms.

42) Discuss how an auditor can test for kiting.

43) Explain professional skepticism and the need for maintaining professional

skepticism during an audit.