Zippy Company has a process costing system. Information about units processed and

processing costs incurred during a recent month in the Refining Department follow:

The beginning work in process inventory had $10,946 of processing cost attached to it

at the beginning of the month. During the month, the Department incurred an additional

$289,954 in processing cost.

Assuming that the company uses the FIFO method, what are the equivalent units for

processing costs for the Department for the month?

A. 97,300

B. 91,300

C. 94,000

D. 100,300

Answer:

The break-even point in unit sales is found by dividing total fixed expenses by:

A. the contribution margin ratio.

B. the variable expenses per unit.

C. the sales price per unit.

D. the contribution margin per unit.

Answer:

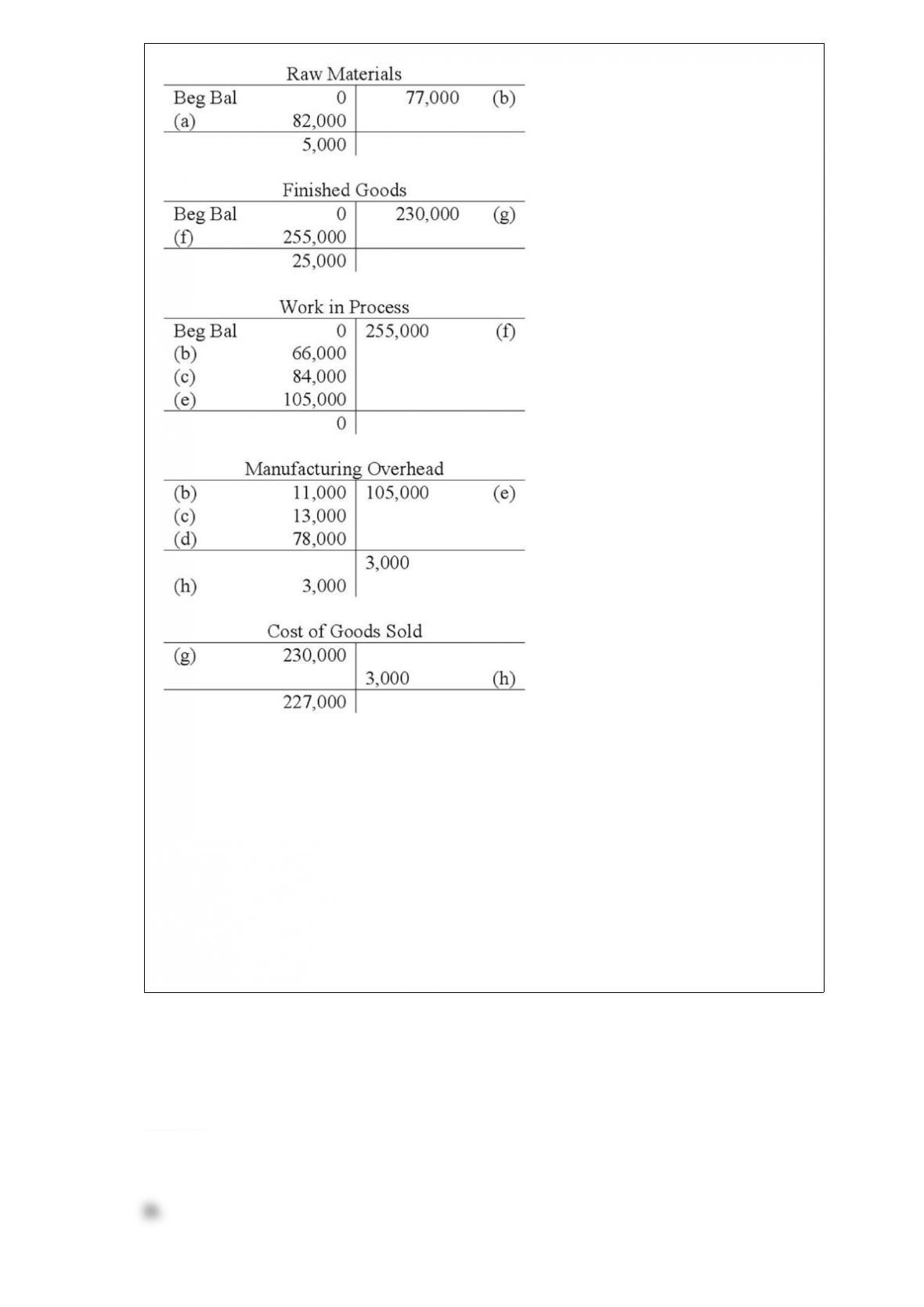

The following accounts are from last year’s books at Sharp Manufacturing:

Sharp uses job-order costing and applies manufacturing overhead to jobs based on

direct labor costs. What is the amount of cost of goods manufactured for the year?

A. $252,000

B. $227,000

C. $230,000

D. $255,000

Answer:

Reference: 8A-3

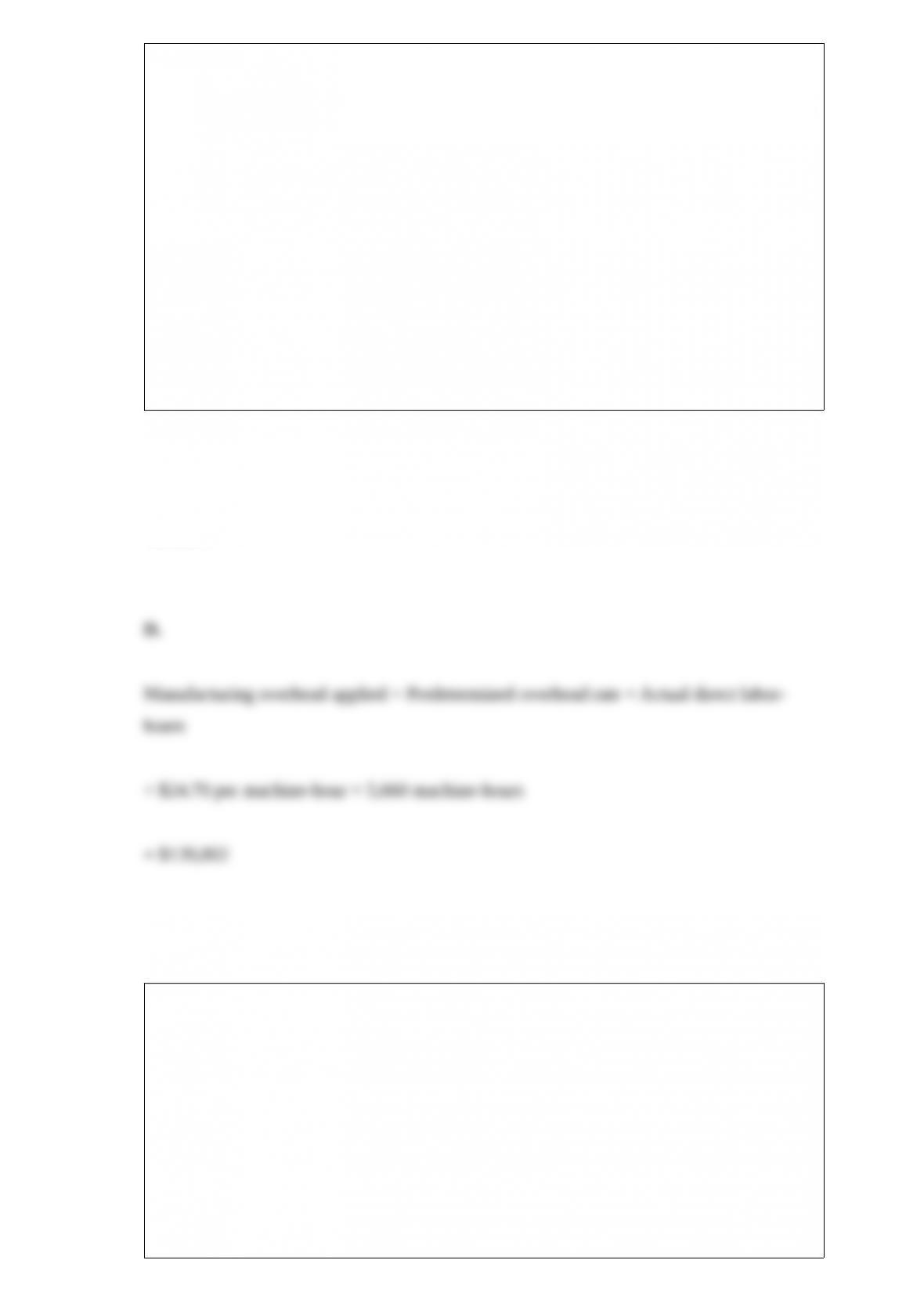

The Chase Company uses a standard cost system in which manufacturing overhead

costs are applied to products on the basis of standard machine-hours. For November, the

companys flexible budget for manufacturing overhead showed the following total

budgeted costs at the denominator activity level of 40,000 machine-hours:

During November 42,000 machine-hours were used to complete 13,200 units of product

with the following actual overhead costs:

The standard time allowed to complete one unit of product is 3.6 machine-hours.

The variable overhead rate variance for maintenance cost for November was:

A) $7,420 unfavorable

B) $2,400 favorable

C) $9,820 unfavorable

D) $5,620 unfavorable

Answer:

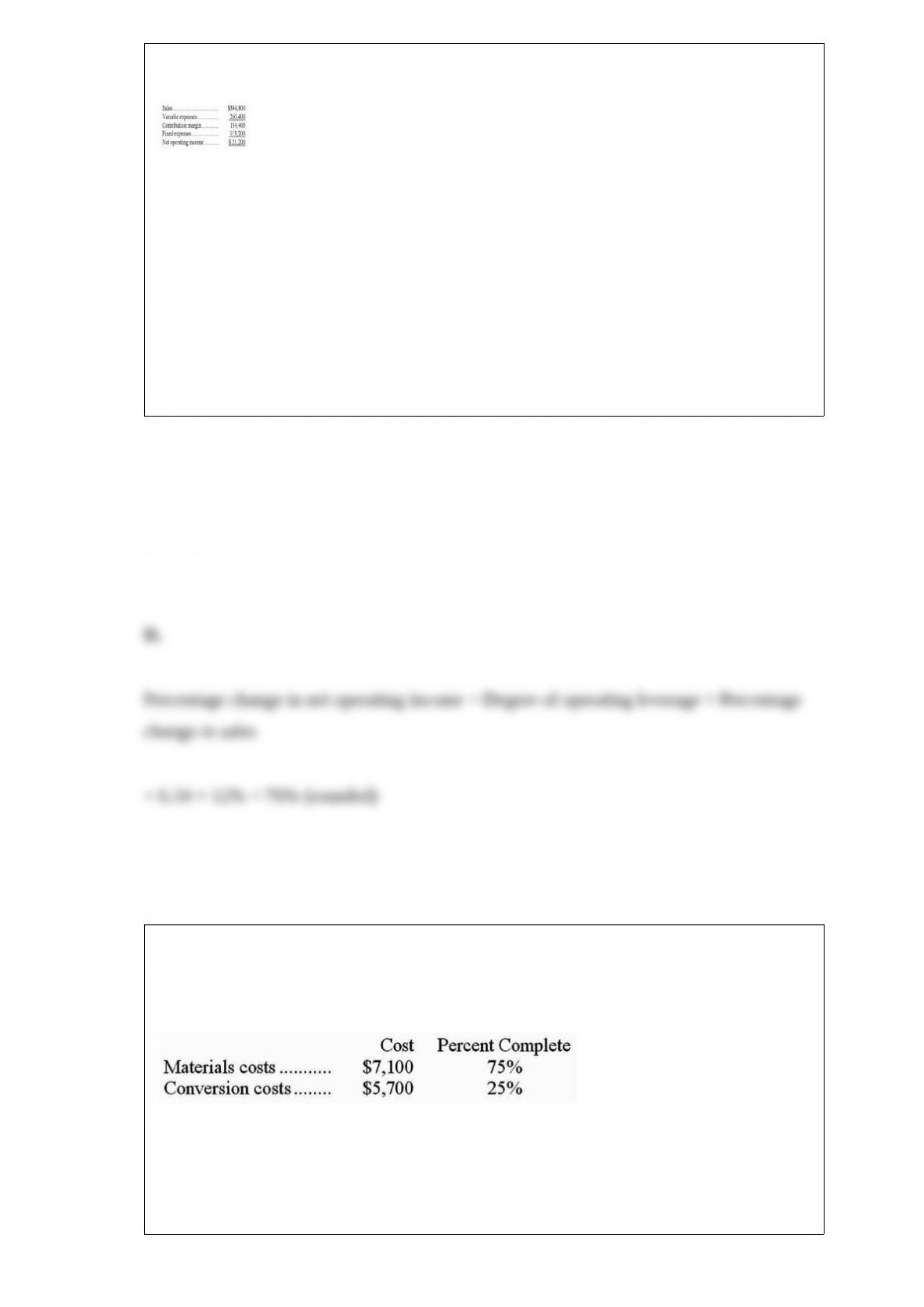

Jackson Company’s operating results for last year are given below:

If the company’s fixed expenses decrease by 20% next year, the break-even point will

change from its previous level by:

A. 150 unit increase

B. 360 unit decrease

C. 150 unit decrease

D. no change in the break-even point

Answer:

Qdynamic Corporation uses the FIFO method in its process costing system. Data

concerning the first processing department for the most recent month are listed below:

Note: Your answers may differ from those offered below due to rounding error. In all

cases, select the answer that is the closest to the answer you computed. To reduce

rounding error, carry out all computations to at least three decimal places.

The cost per equivalent unit for conversion costs for the first department for the month

is closest to:

A. $42.49

B. $43.96

C. $45.00

D. $41.87

Answer:

Sperberg Corporation’s operating leverage is 3.7. If the company’s sales increase by

12%, its net operating income should increase by about:

A. 44.4%

B. 3.7%

C. 12.0%

D. 30.8%

Answer:

Eagle Corporation manufactures a picnic table. Shown below is Eagle’s cost structure:

In its first year of operations, Eagle produced and sold 10,000 tables. The tables sold for

$120 each.

How would Eagle’s absorption costing net operating income have been affected in its

first year if 12,000 tables were produced instead of 10,000 and Eagle still sold 10,000

tables?

A. net operating income would not have been affected

B. net operating income would have been $27,000 higher

C. net operating income would have been $31,500 higher

D. net operating income would have been $116,000 lower

Answer:

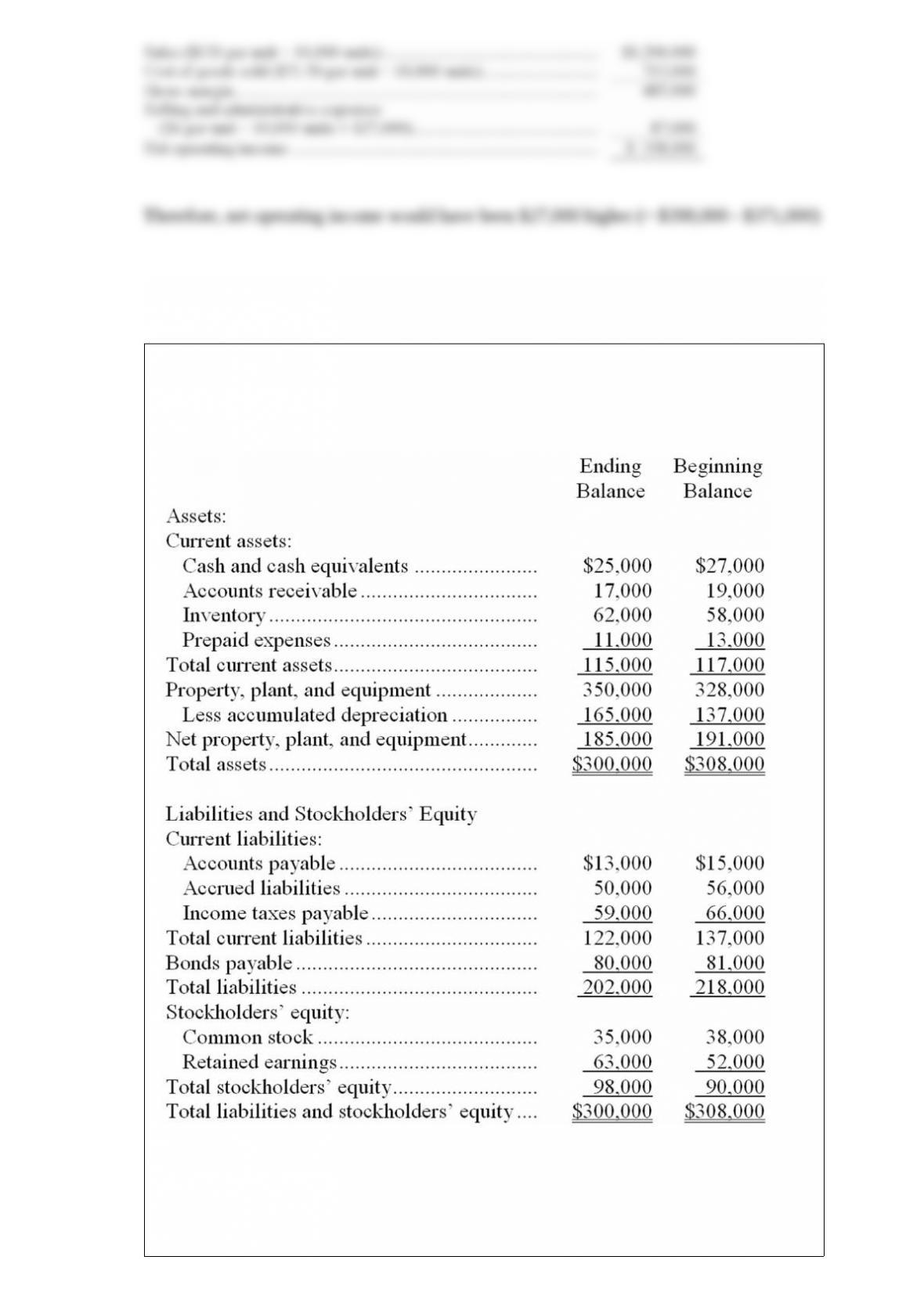

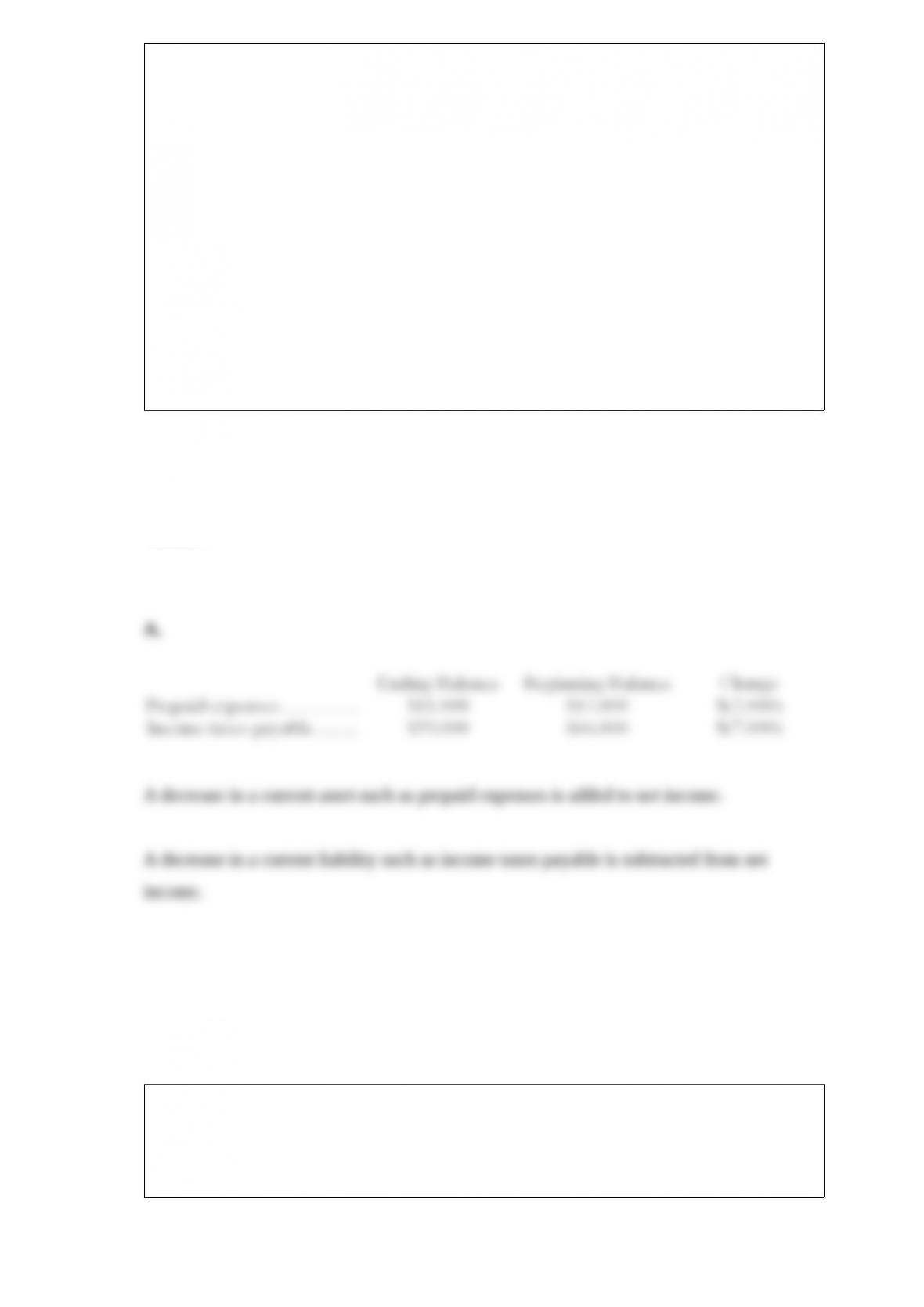

The most recent comparative balance sheet of Broekemeier Corporation appears below:

The company uses the indirect method to construct the operating activities section of its

statements of cash flows.

Which of the following is correct regarding the operating activities section of the

statement of cash flows?

A. The change in Prepaid Expenses will be added to net income; The change in Income

Taxes Payable will be subtracted from net income

B. The change in Prepaid Expenses will be subtracted from net income; The change in

Income Taxes Payable will be subtracted from net income

C. The change in Prepaid Expenses will be subtracted from net income; The change in

Income Taxes Payable will be added to net income

D. The change in Prepaid Expenses will be added to net income; The change in Income

Taxes Payable will be added to net income

Answer:

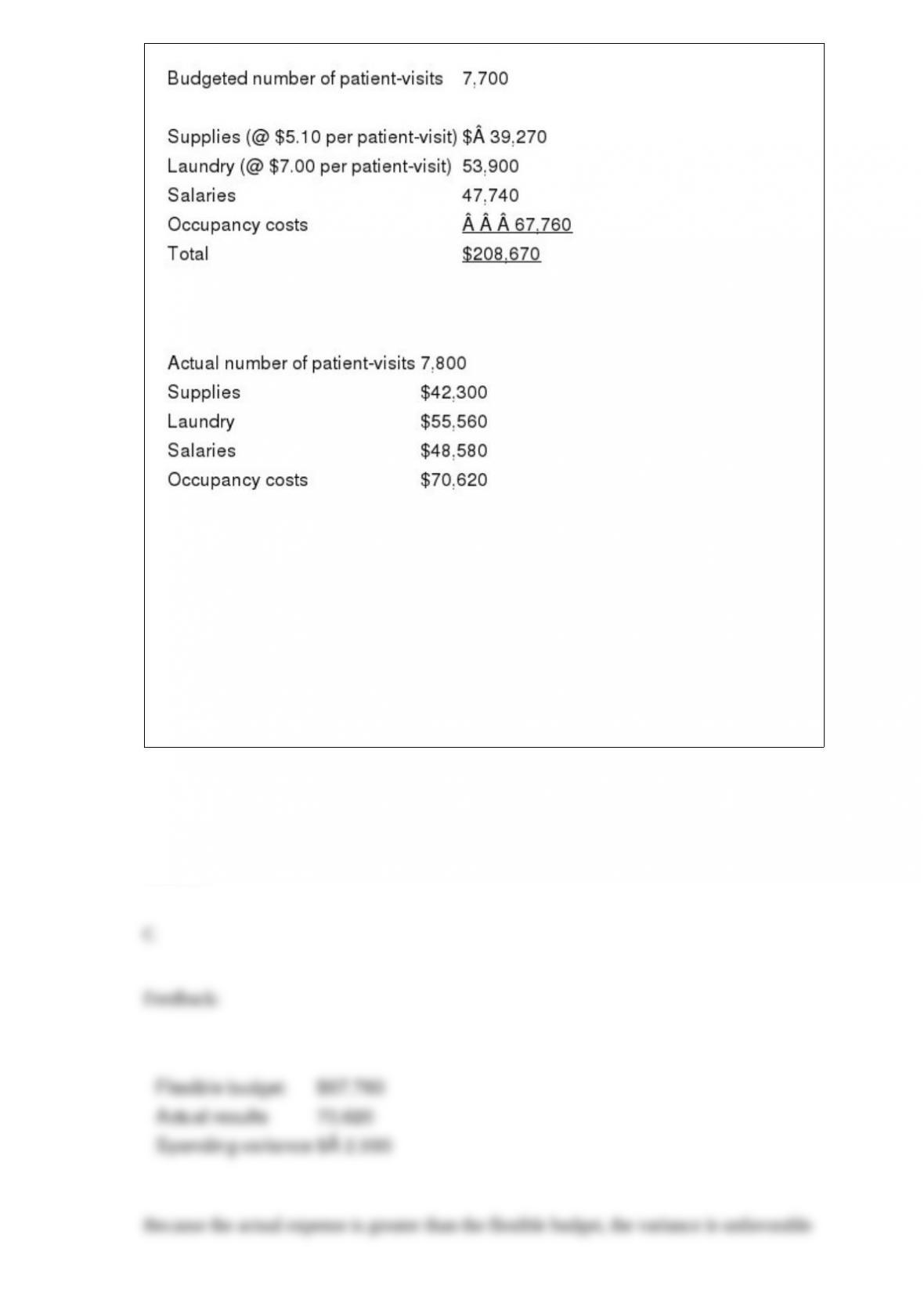

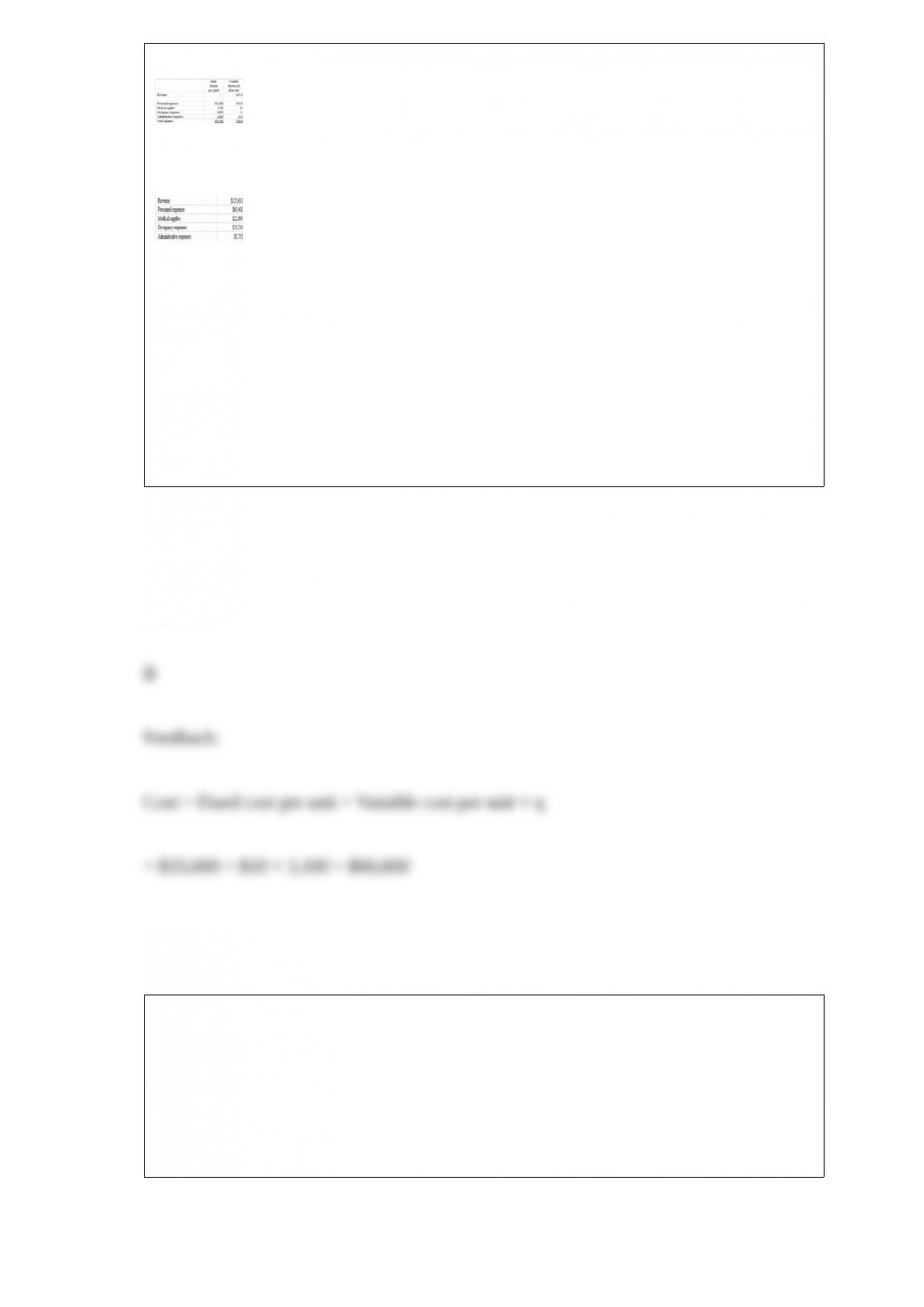

Reference: 8-24

Rushton Hospital bases its budgets on patient-visits. The hospitals static planning

budget for May appears below:

Actual results for the month were:

The spending variance for occupancy costs for the month is:

A) $1,980 F

B) $1,980 U

C) $2,860 U

D) $2,860 F

Answer:

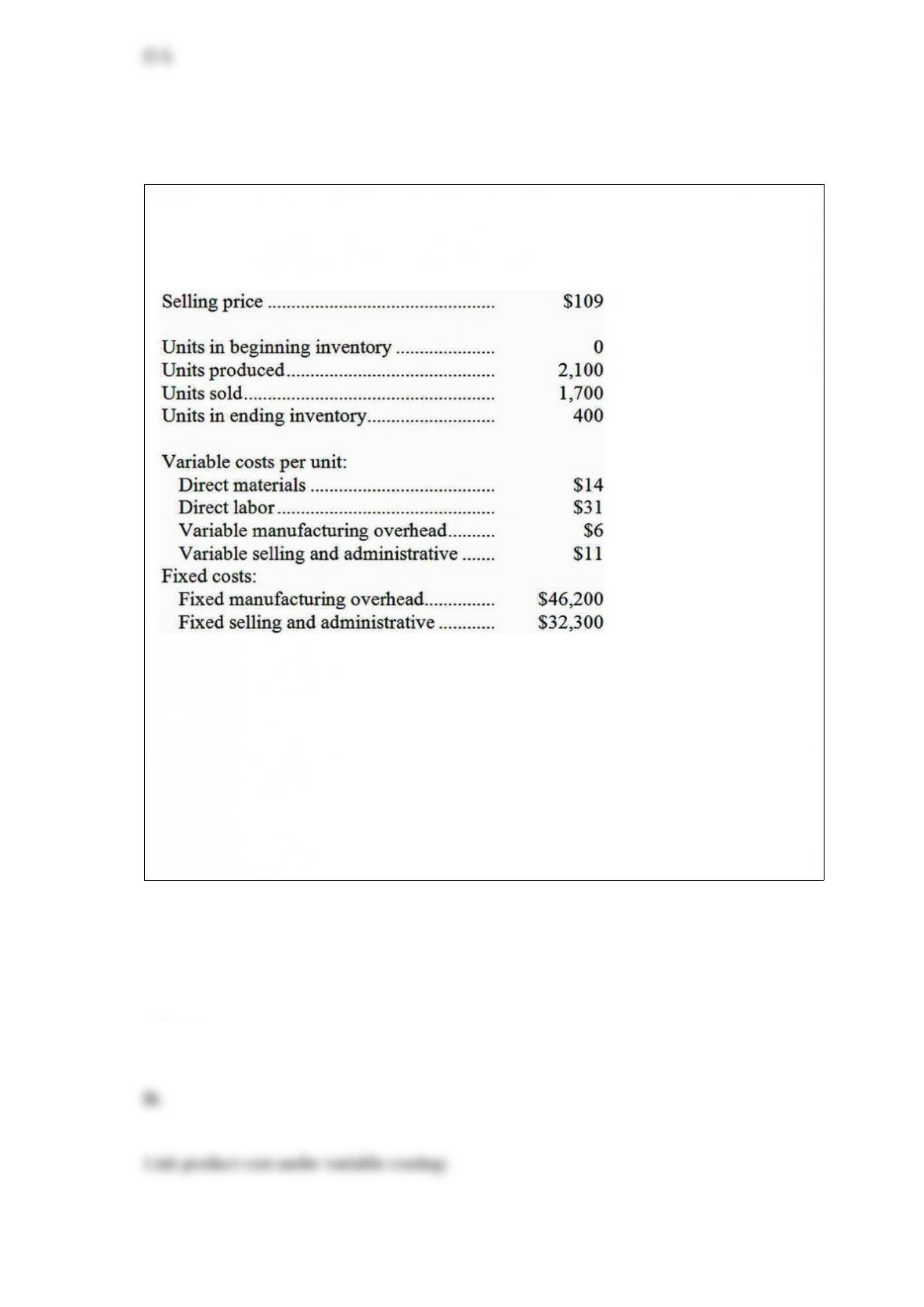

Elbon Company, which has only one product, has provided the following data

concerning its most recent month of operations:

What is the net operating income for the month under variable costing?

A. $10,200

B. $(19,000)

C. $8,800

D. $1,400

Answer:

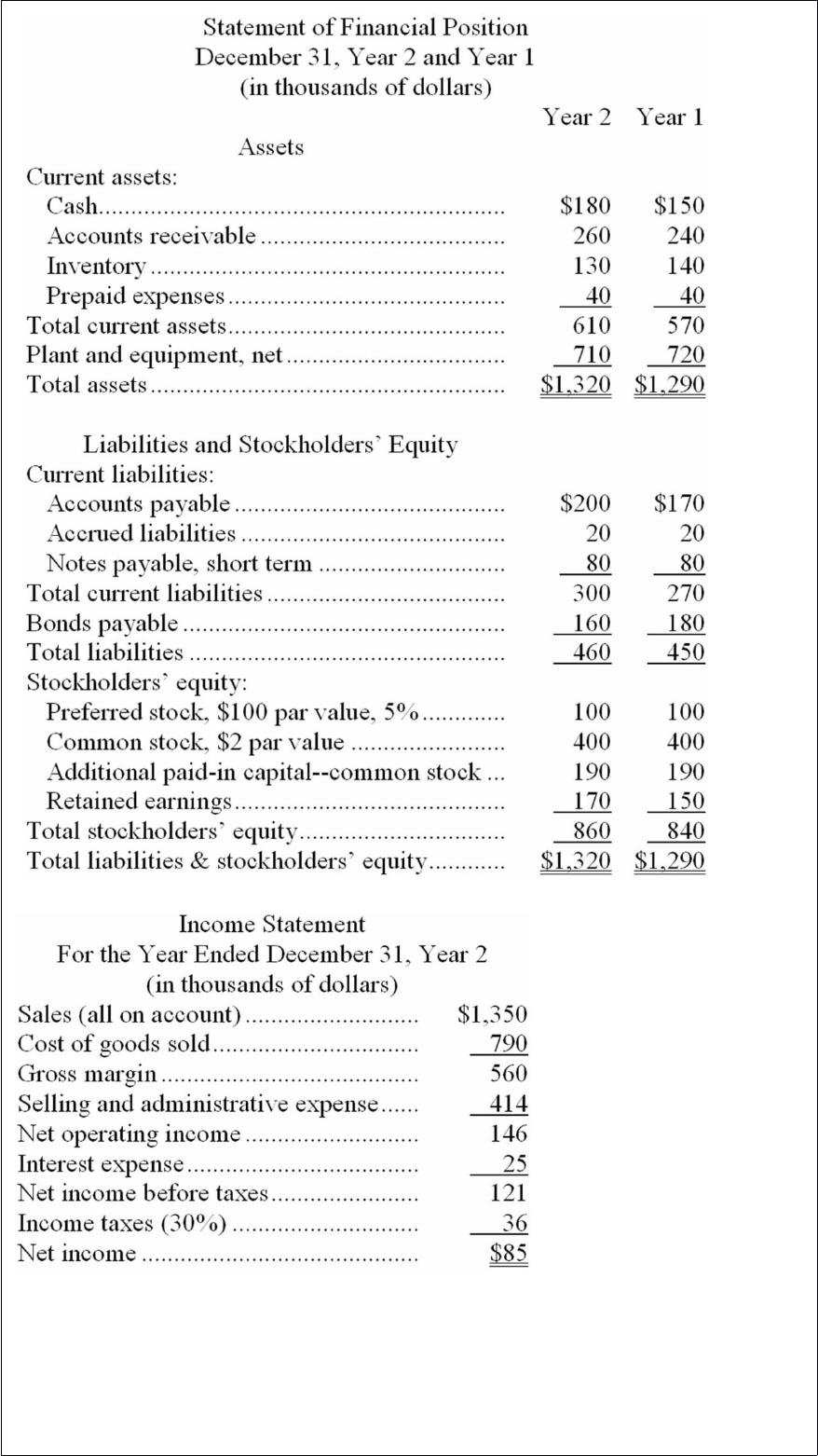

Hartzog Corporation’s most recent balance sheet and income statement appear below:

Dividends on common stock during Year 2 totaled $60 thousand. Dividends on

preferred stock totaled $5 thousand. The market price of common stock at the end of

Year 2 was $7.04 per share.

The return on common stockholders’ equity for Year 2 is closest to:

A. 11.33%

B. 10.00%

C. 10.67%

D. 9.41%

Answer:

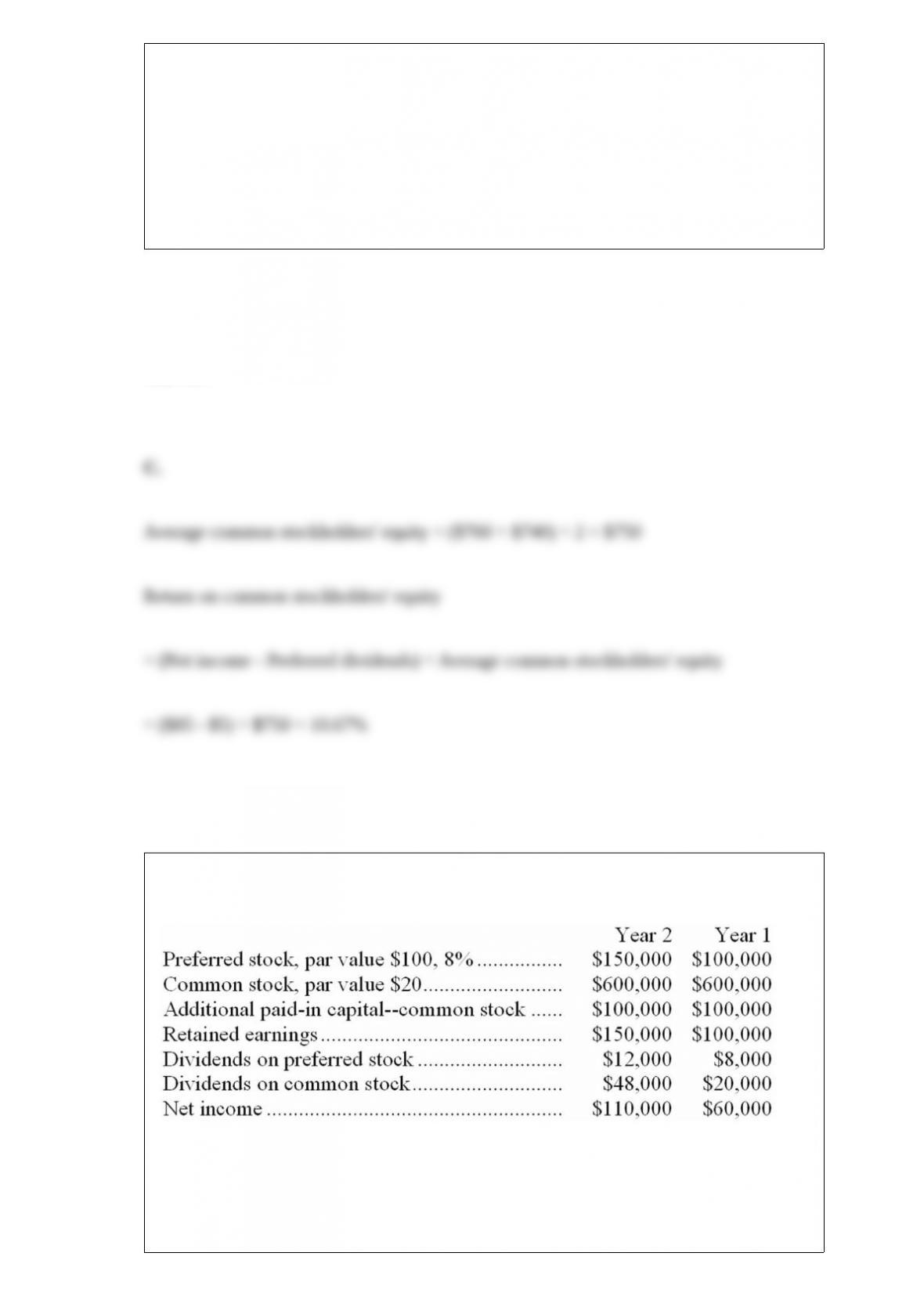

The following selected data are for Geneva Company:

Geneva Company’s return on common stockholders’ equity for Year 2 is closest to:

A. 11%

B. 12%

C. 13%

D. 6%

Answer:

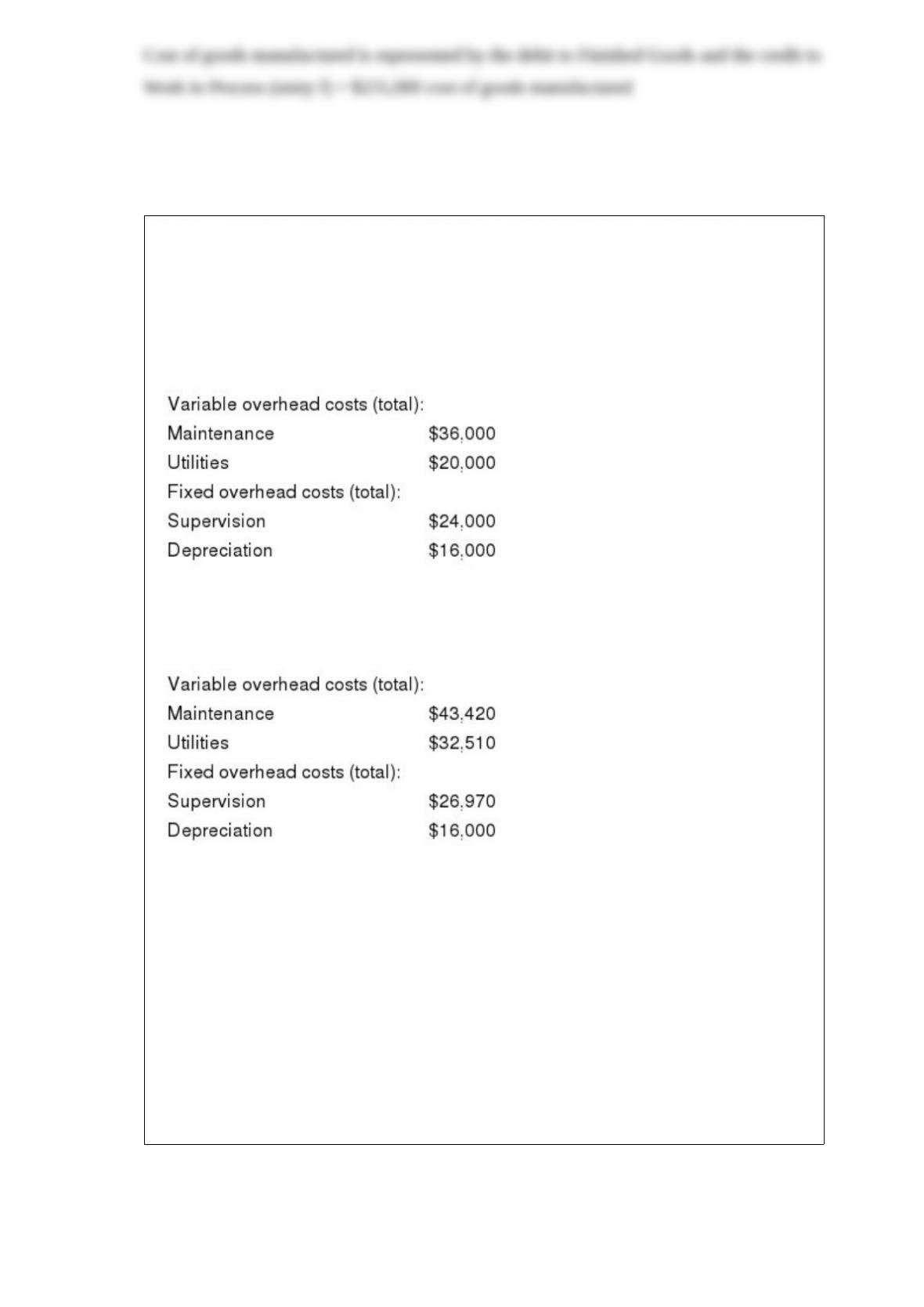

The fixed manufacturing overhead applied to Franklins production for the year is:

A) $484,200

B) $575,000

C) $594,000

D) $600,000

Answer:

Ingrum Framings cost formula for its supplies cost is $1,120 per month plus $11 per

frame. For the month of June, the company planned for activity of 611 frames, but the

actual level of activity was 607 frames. The actual supplies cost for the month was

$8,150. The spending variance for supplies cost in June would be closest to:

A) $353 F

B) $309 U

C) $353 U

D) $309 F

Answer:

Reference: 8-38

The Thompson Company uses standard costing and has established the following direct

material and direct labor standards for each unit of Lept.

Direct materials: 2 gallons at $4 per gallon

Direct labor: 0.5 hours at $8 per hour

During September, the company made 6,000 Lepts and incurred the following costs:

Direct materials purchased: 13,400 gallons at $4.10 per gallon

Direct materials used: 12,600 gallons

Direct labor used: 2,800 hours at $7.65 per hour

The materials quantity variance for September was:

A) $2,460 unfavorable

B) $5,600 unfavorable

C) $2,400 unfavorable

D) $5,740 unfavorable

Answer:

The Odle Company makes and sells a single product called a Kitt. Odle uses a standard

costing system. Each Kitt has a standard cost of 5 pounds of material at $12 per pound

and 0.9 direct labor-hours at $15 per hour. There were no inventories of any kind on

June 1. During June, the following events occurred:

– Purchased 17,000 pounds of material at a total cost of $190,000.

– Used 15,000 pounds of material to produce 2,400 Kitts.

– Used 1,900 hours of direct labor time at a total cost of $38,000.

To record the incurrence of direct labor cost and its use in production, the general ledger

would include what kind of entry to the Labor Efficiency Variance account?

A. $7,500 credit

B. $5,600 debit

C. $5,600 credit

D. $3,900 credit

Answer:

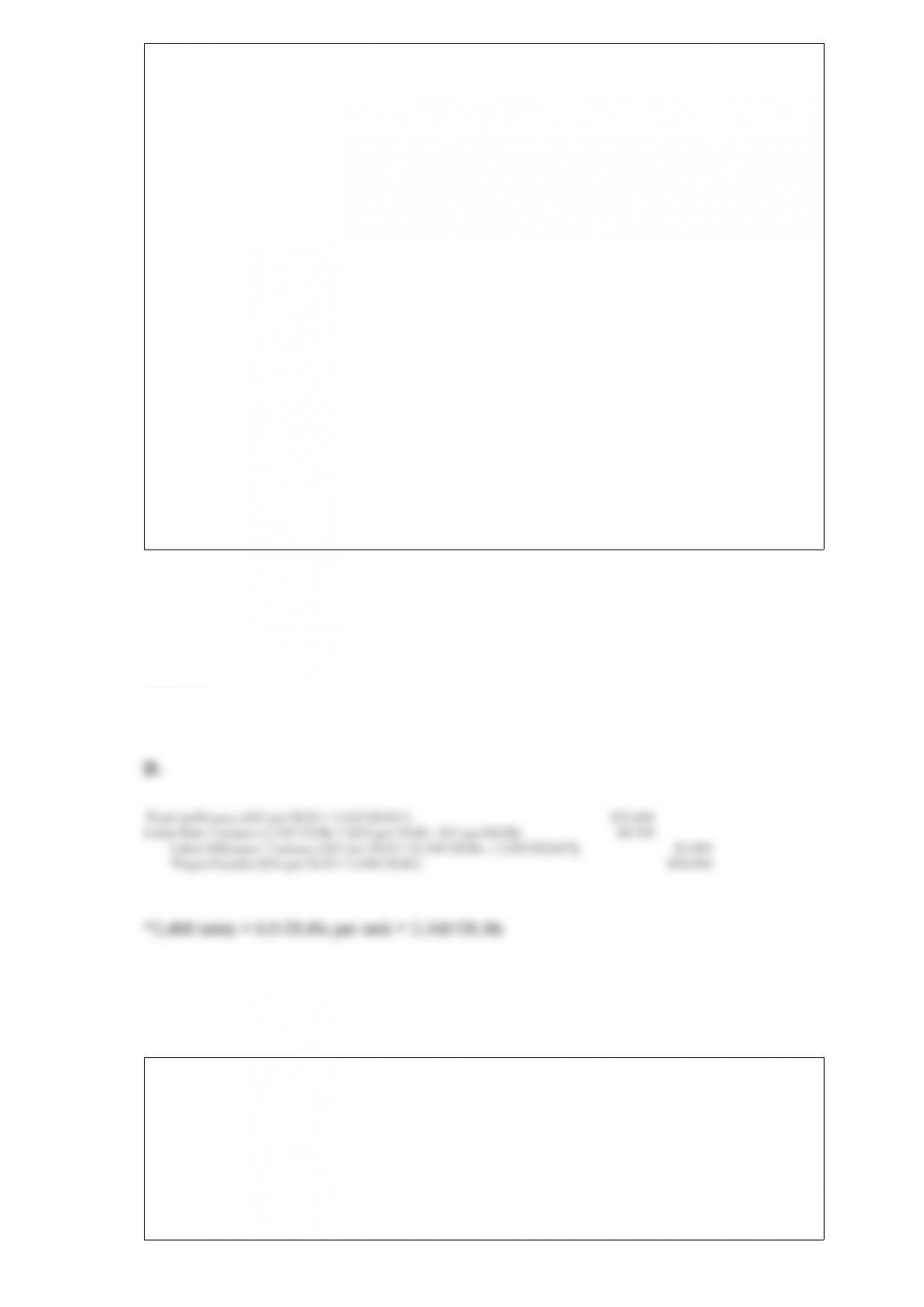

Reference: 8-10

Caballes Clinic uses client-visits as its measure of activity. During November, the clinic

budgeted for 3,100 client-visits, but its actual level of activity was 3,070 client-visits.

The clinic has provided the following data concerning the formulas used in its

budgeting and its actual results for November:

Data used in budgeting:

Actual results for November:

The personnel expenses in the planning budget for November would be closest to:

A) $63,400

B) $66,600

C) $64,020

D) $66,300

Answer:

Reference: 8A-5

The Dodge Company makes and sells a single product and uses a standard cost system

in which manufacturing overhead costs are applied to units of product on the basis of

standard direct labor-hours. The standard cost card shows that 5 direct labor-hours are

required per unit of product. The Dodge Company had the following budgeted and

actual data for the year:

The budgeted direct labor-hours is used as the denominator activity for the month.

The fixed manufacturing overhead volume variance as:

A) $7,500 F

B) $1,500 F

C) $3,750 U

D) $7,500 U

Answer:

Carter Corporation applies manufacturing overhead on the basis of machine-hours. At

the beginning of the most recent year, the company based its predetermined overhead

rate on total estimated overhead of $135,850. Actual manufacturing overhead for the

year amounted to $145,000 and actual machine-hours were 5,660. The company’s

predetermined overhead rate for the year was $24.70 per machine-hour.

The applied manufacturing overhead for the year was closest to:

A. $135,850

B. $149,218

C. $143,869

D. $139,802

Answer:

The standard cost card for a product shows that the product should use 4 kilograms of

material B per finished unit and that the standard price of material B is $4.50 per

kilogram. During April, when the budgeted production level was 1,000 units, 1,040

units were actually made. A total of 4,100 kilograms of material B were used in

production and the inventories of material B were reduced by 300 kilograms during

April. The total cost of material B purchased during April was $14,400. The material

variances for material B during April were:

Material Price Variance Material Quantity Variance

A) $2,700 F $1,620 F

B) $2,700 F $270 F

C) $4,050 F $270 F

D) $4,050 F $1,620 F

Answer:

Toye Corporation has provided its contribution format income statement for March.

If the company’s sales increase by 12%, its net operating income should increase by

about:

A. 5%

B. 12%

C. 223%

D. 76%

Answer:

Chae Corporation uses the weighted-average method in its process costing system. This

month, the beginning inventory in the first processing department consisted of 500

units. The costs and percentage completion of these units in beginning inventory were:

A total of 8,100 units were started and 7,500 units were transferred to the second

processing department during the month. The following costs were incurred in the first

processing department during the month:

The ending inventory was 80% complete with respect to materials and 75% complete

with respect to conversion costs.

Note: Your answers may differ from those offered below due to rounding error. In all

cases, select the answer that is the closest to the answer you computed. To reduce

rounding error, carry out all computations to at least three decimal places.

The cost per equivalent unit for materials for the month in the first processing

department is closest to:

A. $16.32

B. $17.17

C. $15.91

D. $16.73

Answer:

At the end of the year, actual manufacturing overhead costs were $110,000 and applied

manufacturing overhead costs were $118,800. If the denominator activity for the year

was 20,000 machine-hours, and if 22,000 standard machine-hours were allowed for the

years production, the predetermined overhead rate per machine-hour was:

A) $5.00

B) $5.94

C) $5.50

D) $5.40

Answer:

Reference: 8-12

Nakhle Kennel uses tenant-days as its measure of activity; an animal housed in the

kennel for one day is counted as one tenant-day. During October, the kennel budgeted

for 3,000 tenant-days, but its actual level of activity was 2,960 tenant-days. The kennel

has provided the following data concerning the formulas used in its budgeting and its

actual results for October:

Data used in budgeting:

Actual results for October:

The net operating income in the planning budget for October would be closest to:

A) $2,757

B) $9,500

C) $2,684

D) $9,900

Answer:

Balmforth Products, Inc. makes and sells a single product called a Bik. It takes three

yards of Material A to make one Bik. Budgeted production of Biks for the next five

months is as follows:

The company wants to maintain monthly ending inventories of Material A equal to 20%

of the following month’s production needs. On January 31, this target had not been

attained since only 2,000 yards of Material A were on hand. The cost of Material A is

$0.80 per yard. The company wants to prepare a Direct Materials Purchases Budget.

The total needs (i.e., production requirements plus desired ending inventory) of

Material A for the month of May are:

A. 37,800 yards

B. 45,360 yards

C. 46,500 yards

D. 38,940 yards

Answer:

Smith Company sells a single product at a selling price of $30 per unit. Variable

expenses are $12 per unit and fixed expenses are $41,400. Smith’s break-even point is:

A. 1,380 units

B. 2,300 units

C. 3,450 units

D. 6,900 units

Answer:

A manufacturing company uses a standard costing system in which standard

machine-hours (MHs) is the measure of activity. Data from the company’s flexible

budget for manufacturing overhead are given below:

The following data pertain to operations for the most recent period:

What was the fixed manufacturing overhead volume variance for the period to the

nearest dollar?

A. $2,565 F

B. $2,810 F

C. $225 U

D. $2,585 F

Answer:

Guillet Inc. produces and sells a single product. The selling price of the product is

$180.00 per unit and its variable cost is $46.80 per unit. The fixed expense is $618,048

per month.

The break-even in monthly unit sales is closest to:

A. 3,434 units

B. 4,640 units

C. 7,093 units

D. 13,206 units

Answer:

Hart Manufacturing operates an automated steel fabrication process. For one operation,

Hart has found that 45% of the total throughput (manufacturing cycle) time is spent on

non-value-added activities. Delivery cycle time is 12 hours, waiting time during the

production process is 3 hours, queue time prior to starting the production process is 2

hours, and inspection time is 1.2 hours.

What is the throughput (manufacturing cycle) time for the operation?

A. 12.0 hours

B. 9.0 hours

C. 10.0 hours

D. 5.8 hours

Answer:

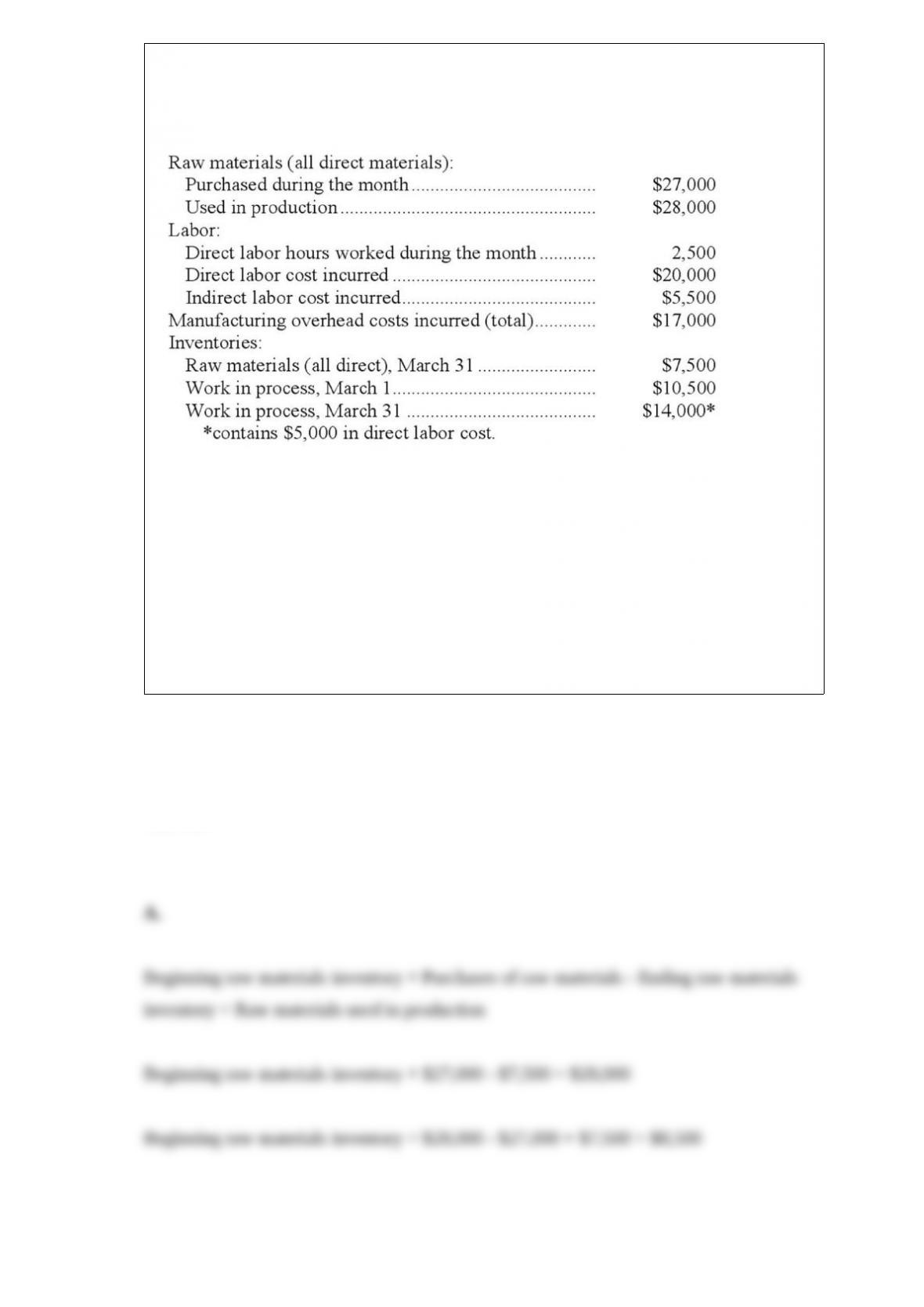

Lund Company applies manufacturing overhead to jobs using a predetermined

overhead rate of 75% of direct labor cost. Any underapplied or overapplied

manufacturing overhead cost is closed out to Cost of Goods Sold at the end of the

month. During March, the following transactions were recorded by the company:

The balance on March 1 in the Raw Materials inventory account was:

A. $8,500

B. $6,500

C. $7,500

D. $9,500

Answer:

In a statement of cash flows, receipts from sales of property, plant, and equipment

should be classified as a(n):

A. Operating activity.

B. Financing activity.

C. Investing activity.

D. Selling activity.

Answer:

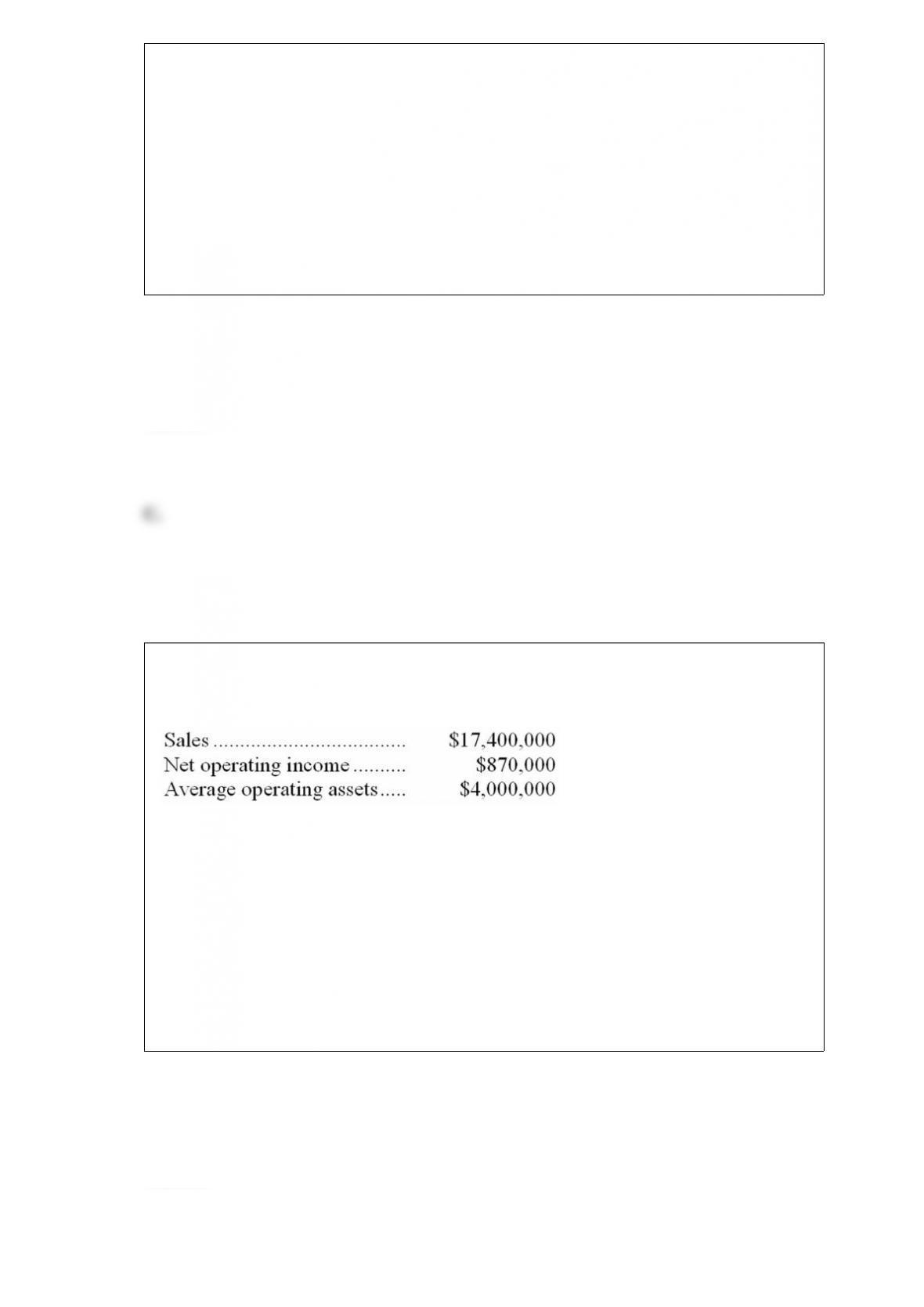

Aide Industries is a division of a major corporation. Data concerning the most recent

year appears below:

The division’s margin is closest to:

A. 21.8%

B. 5.0%

C. 23.0%

D. 28.0%

Answer:

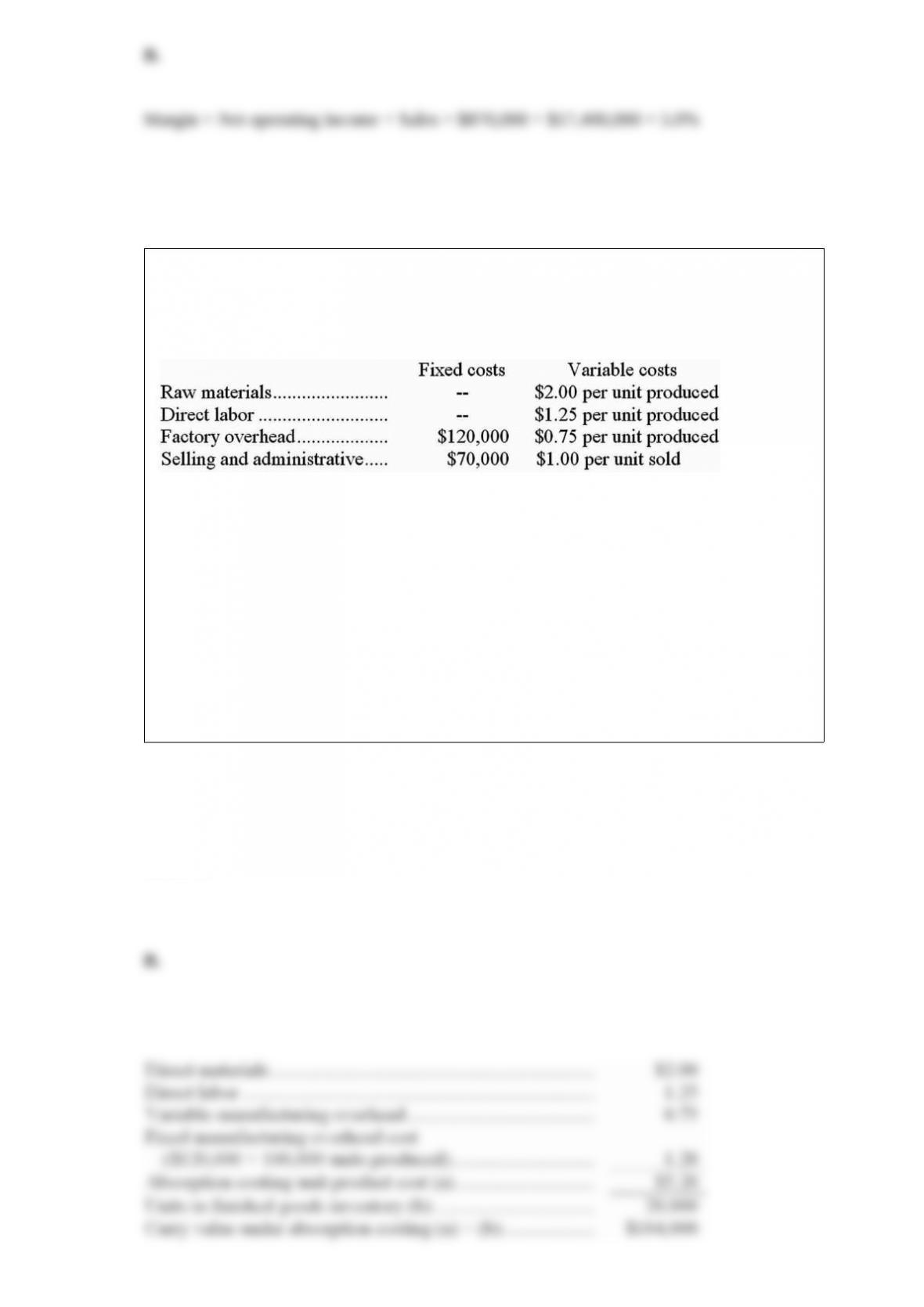

Gordon Company produces a single product that sells for $10 per unit. Last year there

were no beginning inventories, 100,000 units were produced, and 80,000 units were

sold. The company has the following cost structure:

The carrying value on the balance sheet of the ending finished goods inventory under

absorption costing would be:

A. $80,000

B. $104,000

C. $110,000

D. $124,000

Answer: