On December 31, 2015, a company had assets of $16 billion and stockholders’ equity of

$8 billion. That same company had assets of $20 billion and stockholders’ equity of $9

billion as of December 31, 2016. During 2016, the company reported total sales

revenue of $9 billion and total expenses of $7 billion. What is the company’s

debt-to-assets ratio on December 31, 2016?

A) 0.55

B) 0.45

C) 0.035

D) 0.01

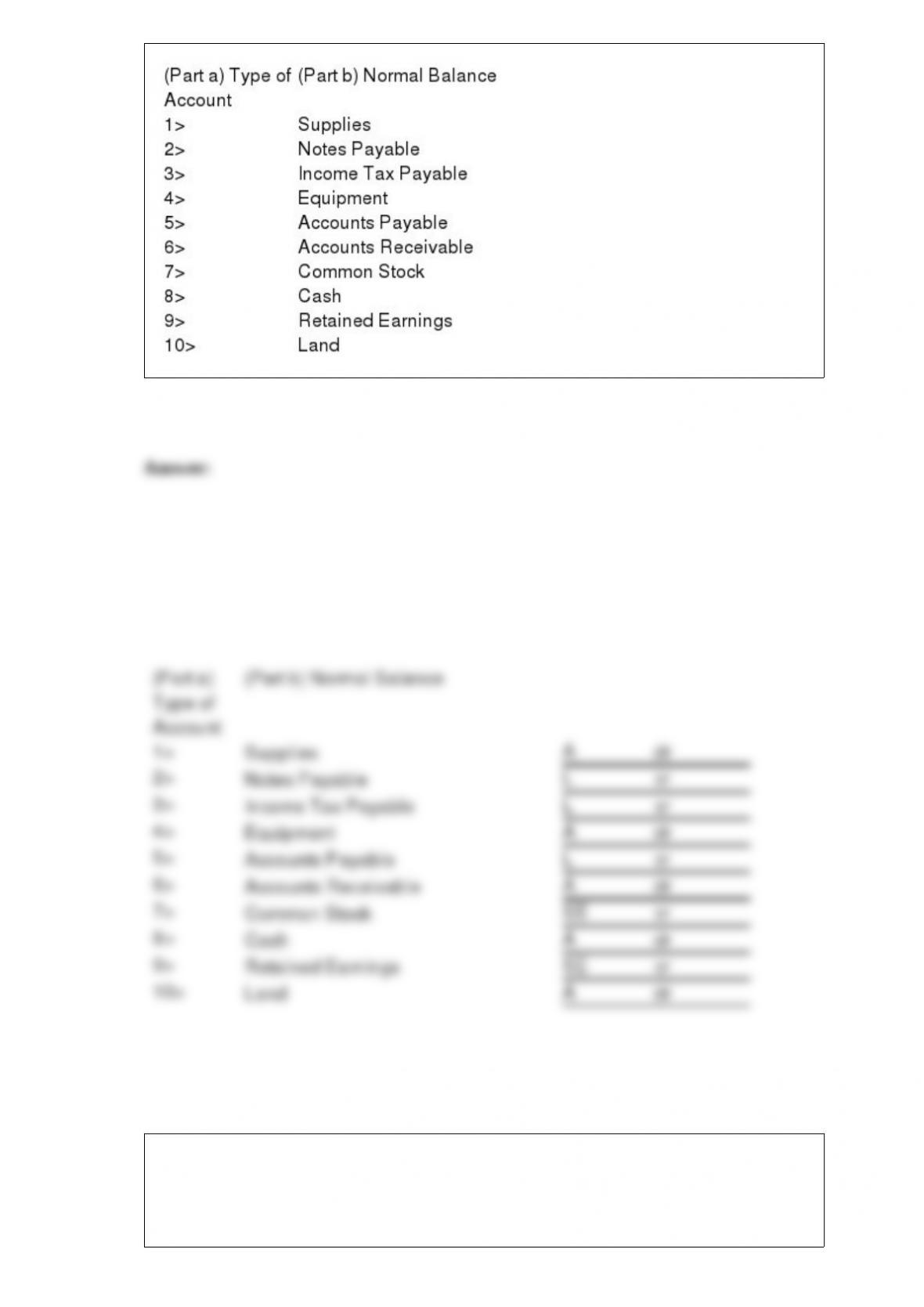

Selected accounts for Moonbills Corporation appear below.

Required:

For each account, indicate the following:

Part a. In the first column at the right, indicate the nature of each account, using the

following abbreviations: Asset – A, Liability – L, Stockholders’ Equity – SE.

Part b. In the second column, indicate the normal balance by inserting dr (for debit) or

cr (for credit).

Which of the following is performed last at the end of the year?

A) Prepare adjusting entries.

B) Prepare an adjusted trial balance.

C) Prepare closing journal entries.

D) Prepare a post-closing trial balance.

Free cash flow is a positive cash flow from operating activities:

A) beyond what is needed to replace current property, plant, and equipment and pay

cash dividends.

B) across all three activity components of the statement of cash flows.

C) beyond what has been allotted for future property, plant, and equipment replacement

and expansion.

D) across both financing and investing activities.

Equipment with a cost of $80,000 and accumulated depreciation of $75,000 is sold for

$12,000 cash.

Required:

Part a. Prepare the journal entry to record this transaction.

Part b. Explain how this transaction would be reported on the statement of cash flows

prepared using the indirect method.

Two different companies, Ripper and Berners, entered into the following inventory

transactions during December. Both companies use a perpetual inventory system.

December 3 – Ripper Corporation sold inventory on account to Berners Corp. for

$480,000, terms 2/10, n/30. This inventory originally cost Ripper $320,000.

December 8 – Berners Corp. returned inventory to Ripper Corporation for a credit of

$30,000. Ripper returned this inventory to inventory at its original cost of $20,000.

December 12 – Berners Corp. paid Ripper Corporation for the amount owed.

Required:

Part a. Prepare the journal entries to record these transactions on the books of Ripper

Corporation.

Part b. What is the amount of net sales to be reported on Ripper Corporation’s income

statement?

Part c. What is the Ripper Corporation’s gross profit percentage?

During the month, a company uses up $4,000 of supplies. At the end of the month, the

related adjusting journal entry would result in a(n):

A) decrease in an asset and an equal decrease in expenses.

B) increase in an asset and an equal increase in expenses.

C) decrease in an asset and an equal increase in expenses.

D) increase in an asset and a decrease in expenses.

Which of the following statements regarding debits and credits is always correct?

A) Debits decrease accounts while credits increase them.

B) The total value of all debits recorded in the ledger must equal the total value of all

credits recorded in the ledger.

C) The total value of all debits to a particular account must equal the total value of all

credits to that account.

D) The normal balance for an account is the side on which it decreases.

On December 1, 2015, Newco borrowed $200,000 from First National Bank, and

signed a 9% note payable due in one year. Interest on the note is due at maturity.

Required:

Part a. Prepare the journal entry to record the borrowing transaction.

Part b. Prepare the required adjusting entry on December 31, 2015.

Part c. Prepare the journal entry to record the payment of the interest on December 1,

2016.

Part d. Prepare the journal entry to record the payment of the note on December 1,

2016.

Which of the following statements about extending credit is notcorrect?

A) It is common for companies to sell on account to other companies.

B) Some companies extend credit to individual consumers.

C) Bad debts arise from credit sales to individual consumers, but not from credit sales

to other companies.

D) When credit is available, customers often buy more products and services.

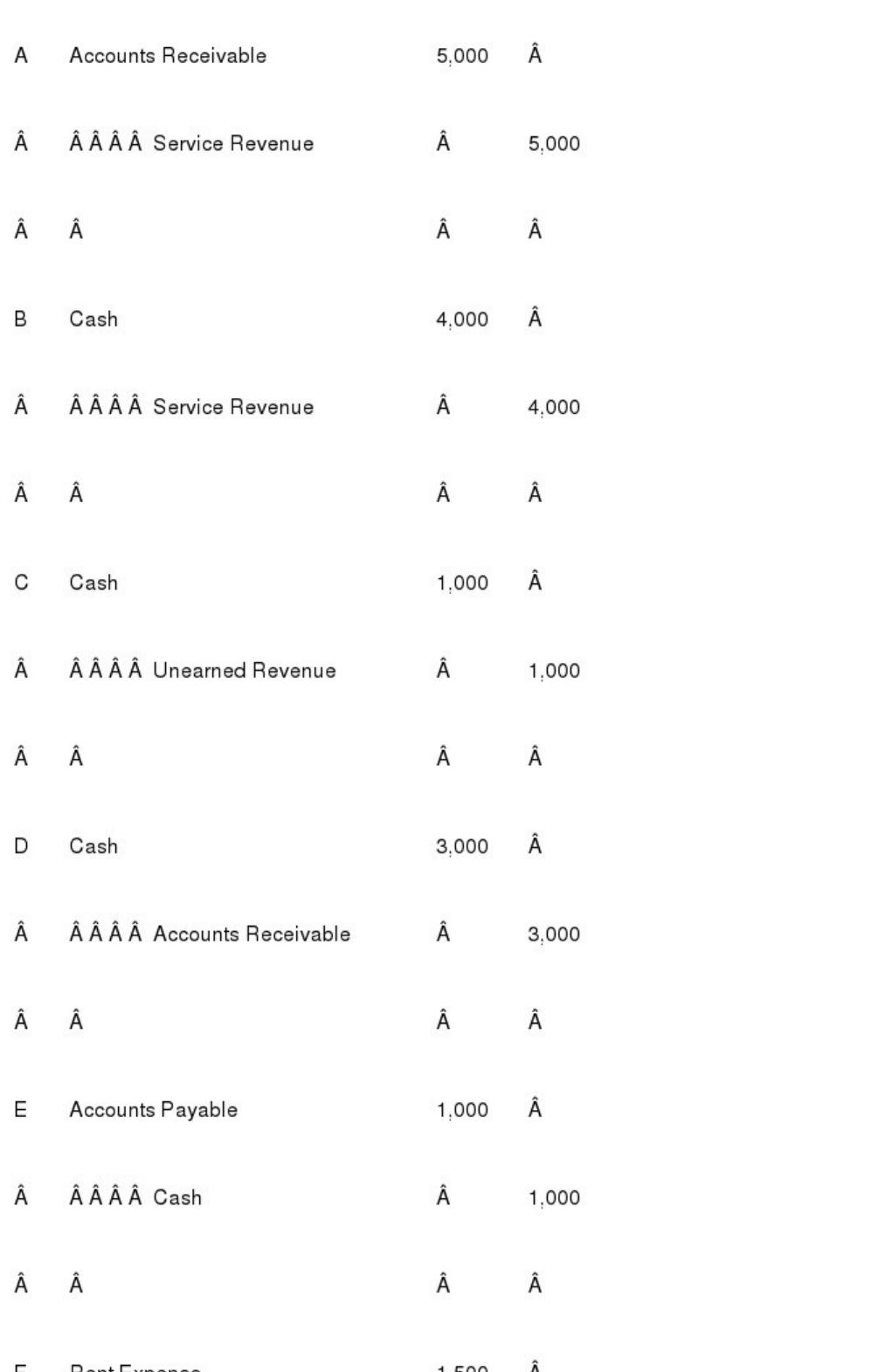

Jim’s Gymnastics Training’s operations for the month of October are summarized as

follows:

A. Provided $5,000 of training to students on account.

B. Received $4,000 cash from students for training provided in October.

C. Received $1,000 cash for training to be provided in November.

D. Received $3,000 cash from students on account for training provided in September.

E. Paid September’s gym rental bill on account in the amount of $1,000.

F. Received October’s rental bill of $1,500; set it aside.

Required:

Prepare journal entries to record the transactions identified among activities (A) through

(F).

Stock dividends and stock splits are similar in all of the following ways except:

A) they both involve a pro rata distribution of shares to existing stockholders.

B) they both reduce the stock price.

C) they both decrease Retained Earnings.

D) have no effect on cash.

A machine with a cost of $130,000 and accumulated depreciation of $85,000 is sold for

$35,000 cash.

Required:

Part a. Prepare the journal entry to record this transaction.

Part b. Explain how this transaction would be reported on the statement of cash flows

prepared using the indirect method.

A company sells a long-lived asset that originally cost $200,000 for $50,000 on

December 31, 2016. The Accumulated Depreciation account had a balance of $110,000

after the current year’s depreciation of $45,000 had been recorded. The company should

recognize a:

A) $100,000 loss on sale.

B) $40,000 gain on sale.

C) $40,000 loss on sale.

D) $25,000 loss on sale.