1) the management of haigler corporation would like to investigate the possibility of

basing its predetermined overhead rate on activity at capacity. the company’s controller

has provided an example to illustrate how this new system would work. in this example,

the allocation base is machine-hours and the estimated amount of the allocation base for

the upcoming year is 64,000 machine-hours. in addition, capacity is 80,000

machine-hours and the actual level of activity for the year is 66,300 machine-hours. all

of the manufacturing overhead is fixed and is $3,788,800 per year. for simplicity, it is

assumed that this is the estimated manufacturing overhead for the year as well as the

manufacturing overhead at capacity. it is further assumed that this is also the actual

amount of manufacturing overhead for the year.

if the company bases its predetermined overhead rate on capacity, by how much was

manufacturing overhead underapplied or overapplied?

a.$648,832 underapplied

b.$136,160 underapplied

c.$648,832 overapplied

d.$136,160 overapplied

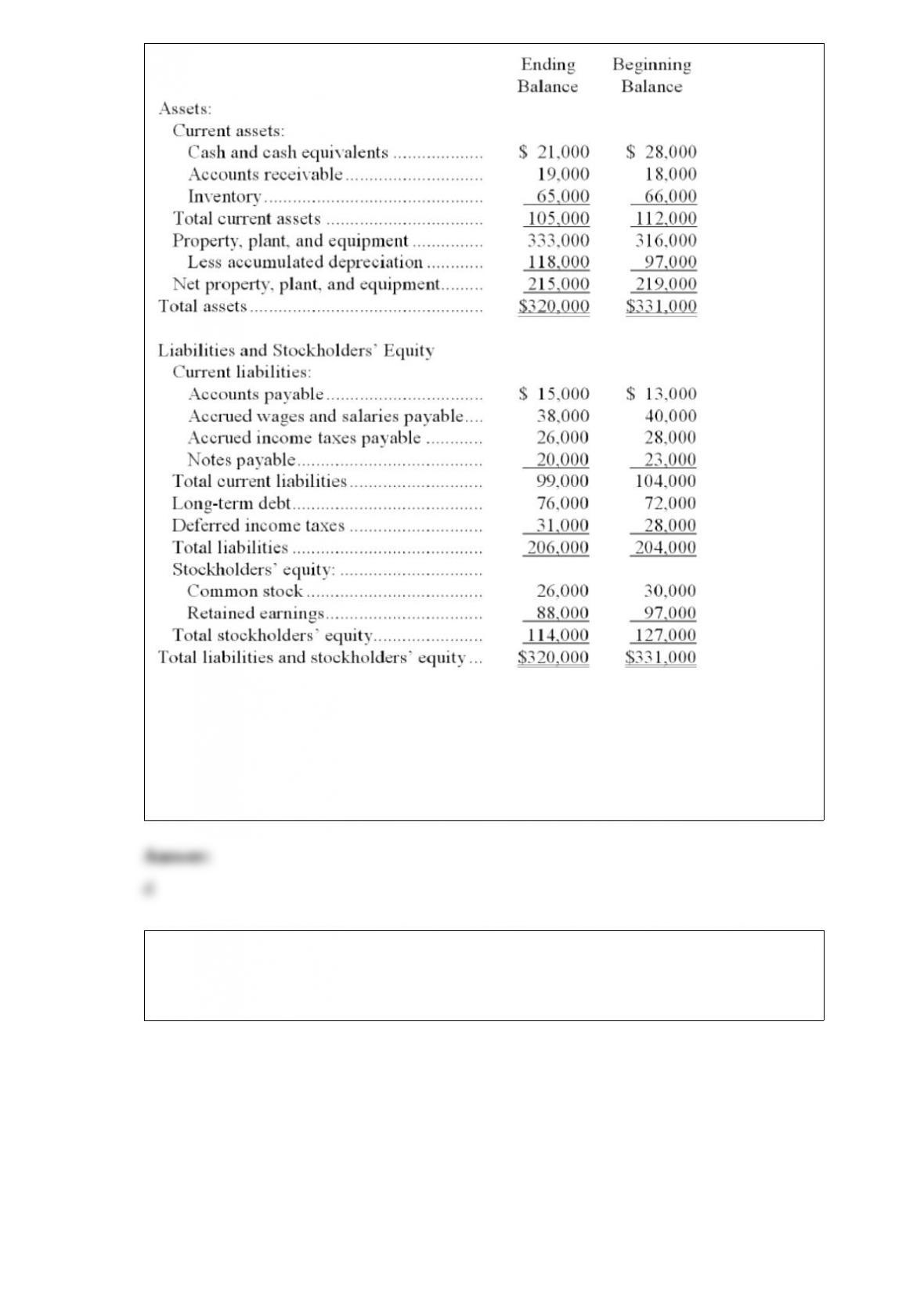

2) the most recent comparative balance sheet of benefield corporation appears below:

which of the following classifications of changes in balance sheet accounts as sources

and uses is correct?

a.the change in accounts receivable is a source; the change in inventory is a use

b.the change in accounts receivable is a source; the change in inventory is a source

c.the change in accounts receivable is a use; the change in inventory is a use

d.the change in accounts receivable is a use; the change in inventory is a source

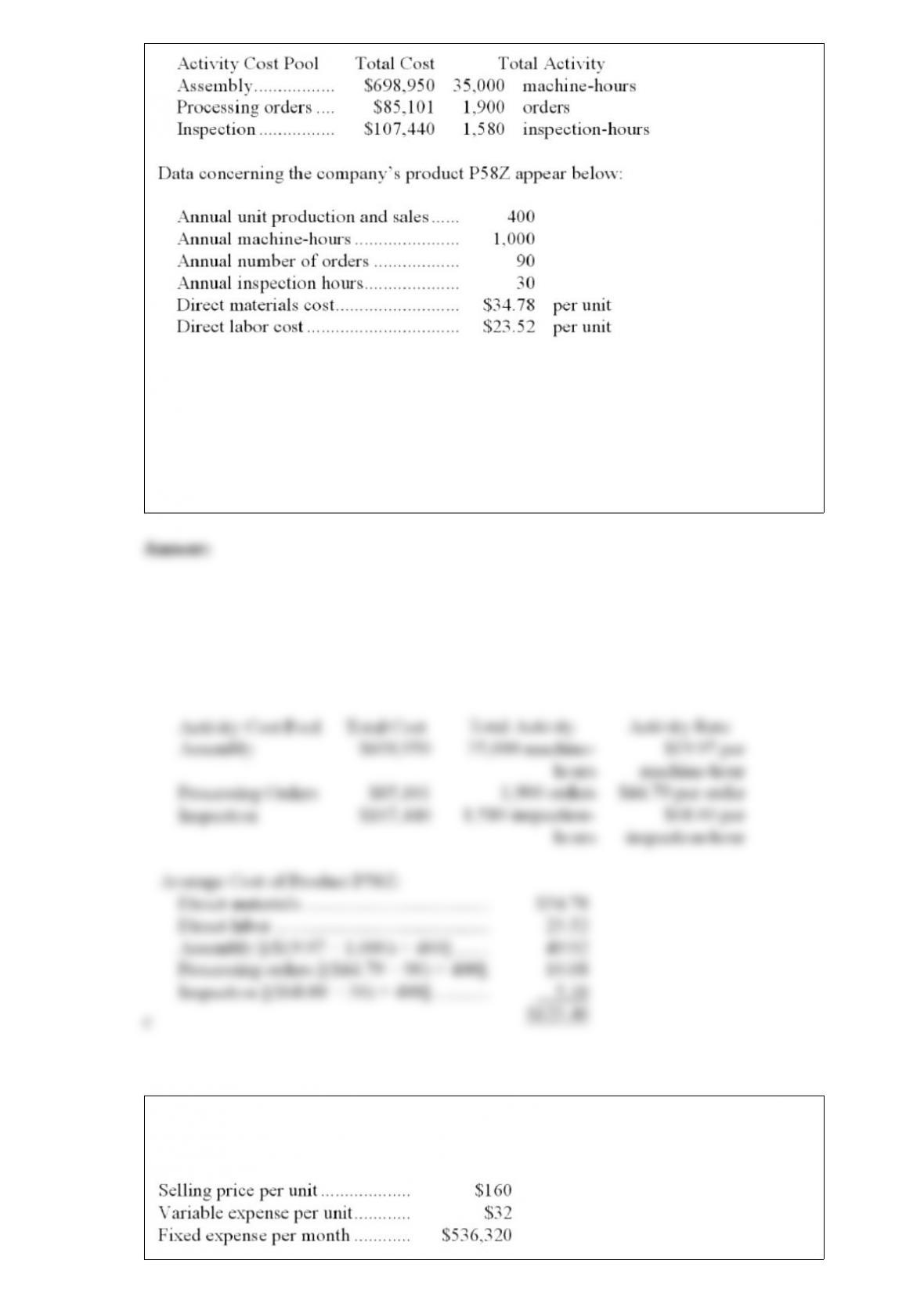

3) vodopich corporation has provided the following data from its activity-based costing

system:

according to the activity-based costing system, the average cost of product p58z is

closest to:

a.$113.33 per unit

b.$58.30 per unit

c.$123.40 per unit

d.$118.30 per unit

4) vandinter corporation produces and sells a single product. data concerning that

product appear below:

the break-even in monthly unit sales is closest to:

a.8,101

b.3,352

c.4,190

d.16,760

5) nichnols corporation’s marketing manager believes that every 6% decrease in the

selling price of one of the company’s products would lead to a 18% increase in the

product’s total unit sales. the product’s absorption costing unit product cost is $10.10.

the variable production cost is $1.70 per unit and the variable selling and administrative

cost is $1.60.

required:

a. compute the product’s price elasticity of demand as defined in the text.

b. compute the product’s profit-maximizing price according to the formula in the text.

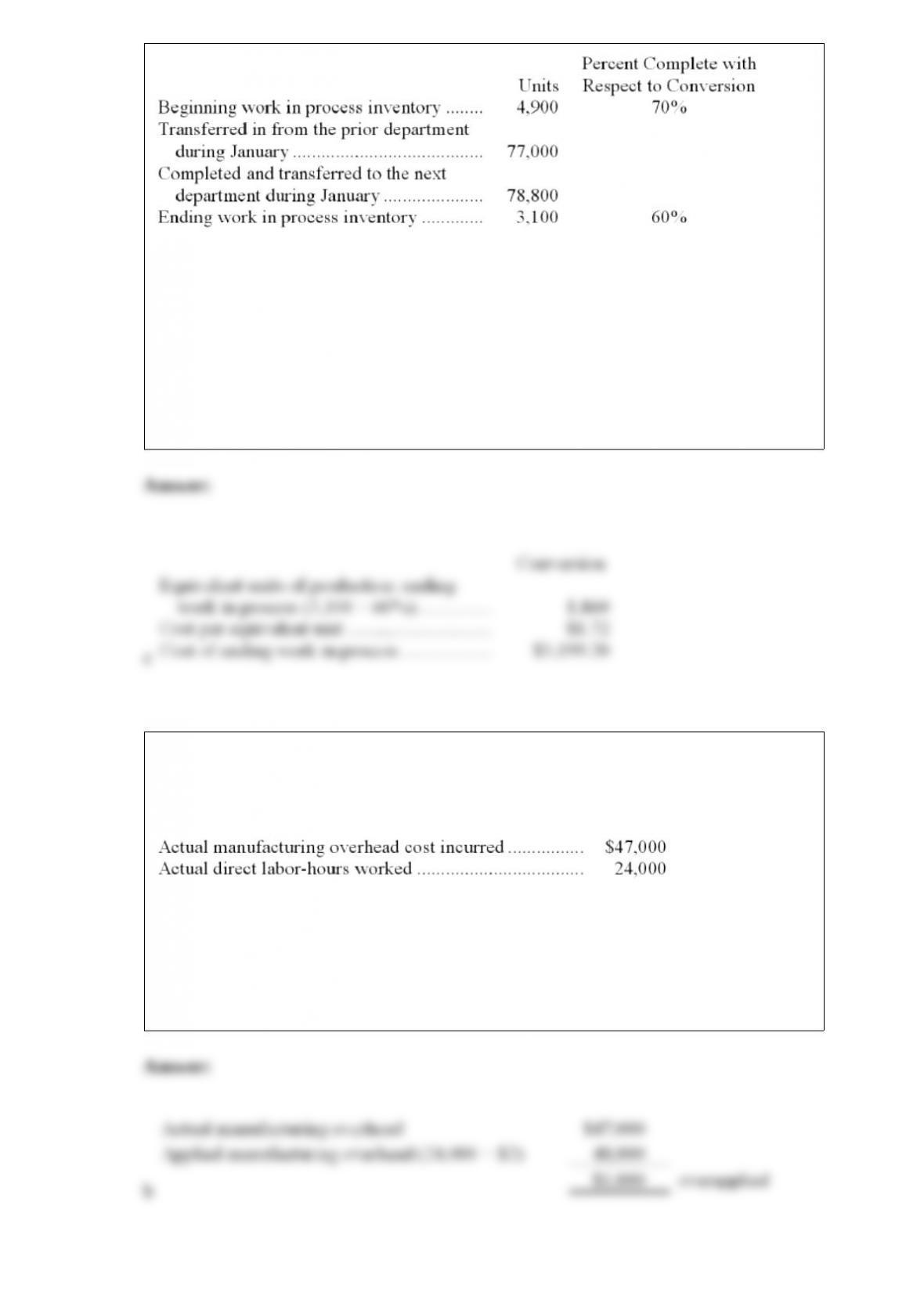

6) park company uses the weighted-average method in its process costing system. the

molding department is the second department in its production process. the data below

summarize the department’s operations in january.

the accounting records indicate that the conversion cost that had been assigned to

beginning work in process inventory was $40,484 and a total of $213,890 in conversion

costs were incurred in the department during january.

the cost per equivalent unit for conversion costs for january in the molding department

is closest to:

a.$4.823

b.$4.186

c.$4.650

d.$4.590

7) raulot corporation uses the weighted-average method in its process costing system.

the molding department is the second department in its production process. the data

below summarize the department’s operations in january.

the molding department’s cost per equivalent unit for conversion cost for january was

$1.72.

how much conversion cost was assigned to the ending work in process inventory in the

molding department for january?

a.$5,332.00

b.$2,540

c.$3,199.20

d.$2,132.80

8) beaver company used a predetermined overhead rate last year of $2 per direct

labor-hour, based on an estimate of 25,000 direct labor-hours to be worked during the

year. actual costs and activity during the year were:

the underapplied or overapplied overhead last year was:

a.$1,000 underapplied

b.$1,000 overapplied

c.$3,000 overapplied

d.$2,000 underapplied

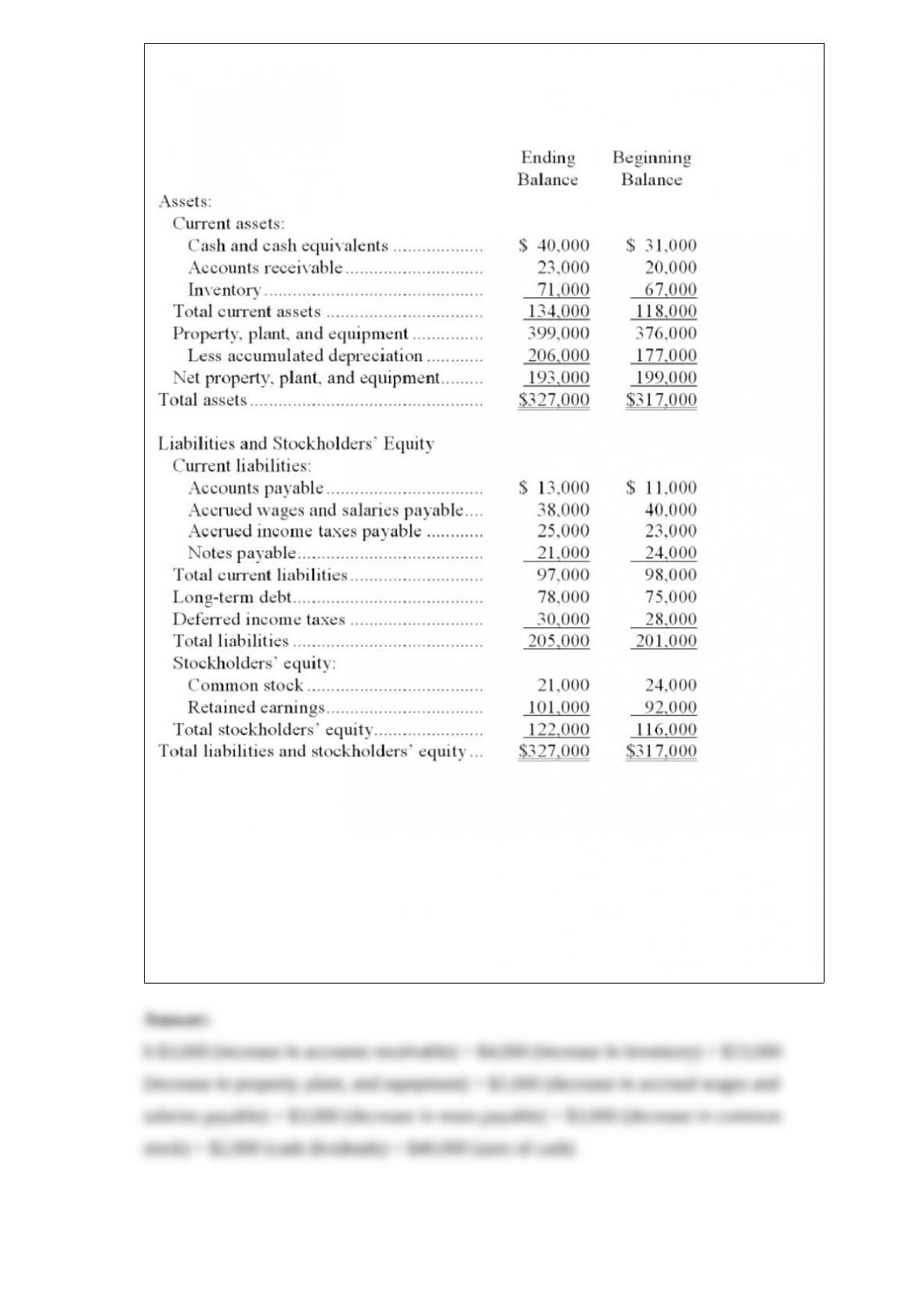

9) spettel corporation’s comparative balance sheet appears below:

the company’s net income (loss) for the year was $11,000 and its cash dividends were

$2,000.

the total dollar amount of all of the items that would be classified as uses when

compiling a simplified statement of cash flows is:

a.$38,000

b.$40,000

c.$9,000

d.$49,000

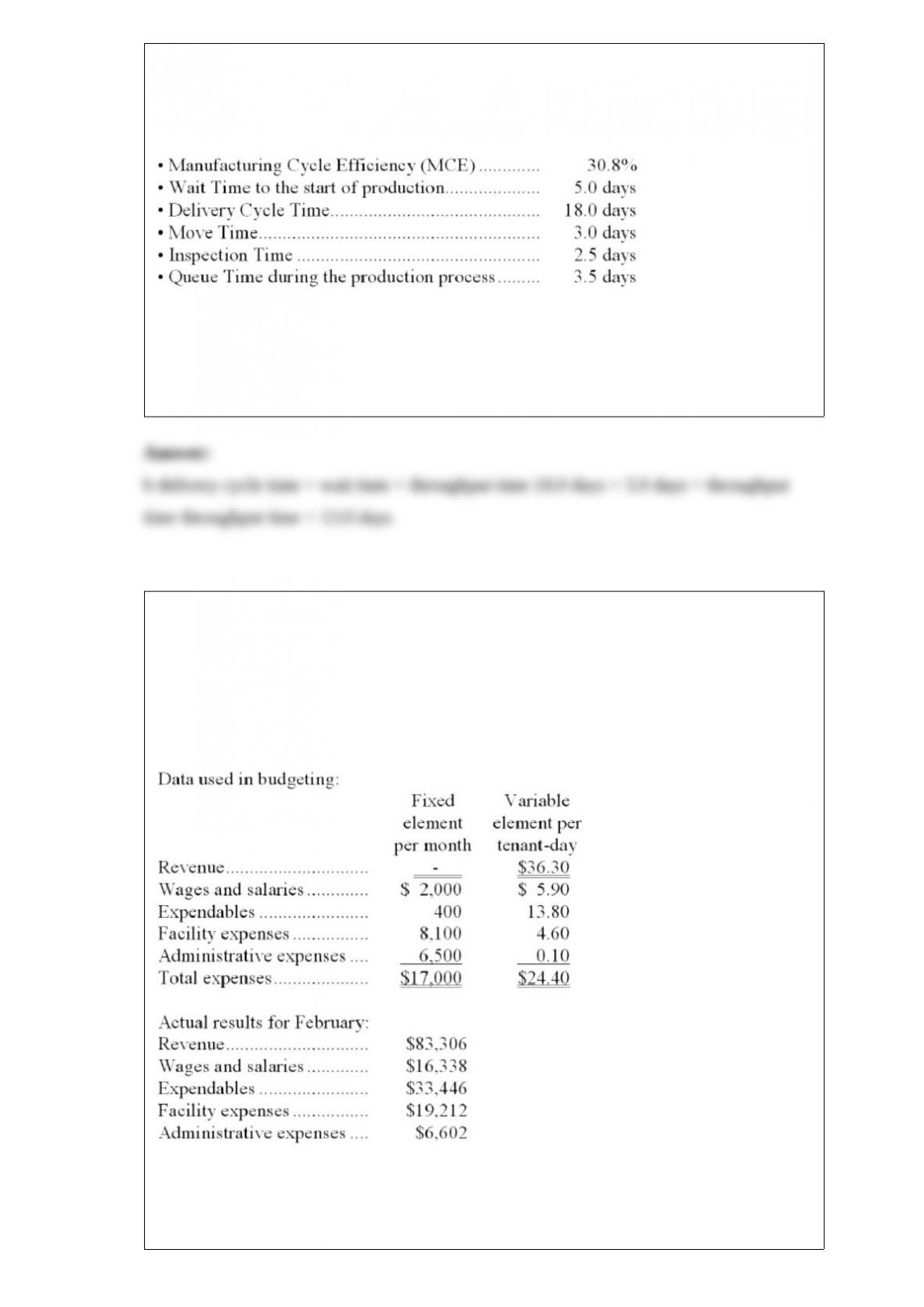

10) the management of granger sports equipment has been maintaining delivery

performance data in order to improve the company’s customer service. data for the most

recent month follows:

what is the throughput (manufacturing cycle) time?

a.6 days

b.13 days

c.18 days

d.23 days

11) kalinowski kennel uses tenant-days as its measure of activity; an animal housed in

the kennel for one day is counted as one tenant-day. during february, the kennel

budgeted for 2,300 tenant-days, but its actual level of activity was 2,320 tenant-days.

the kennel has provided the following data concerning the formulas used in its

budgeting and its actual results for february:

the net operating income in the flexible budget for february would be closest to:

a.$10,370

b.$10,608

c.$7,642

d.$7,775

12) last year, variable expenses were 60% of total sales and fixed expenses were 10% of

total sales. if the company increases its selling prices by 10%, but if fixed expenses,

variable costs per unit, and unit sales remain unchanged, the effect of the increase in

selling price on the company’s total contribution margin would be:

a.a decrease of 2%

b.an increase of 5%

c.an increase of 10%

d.an increase of 25%

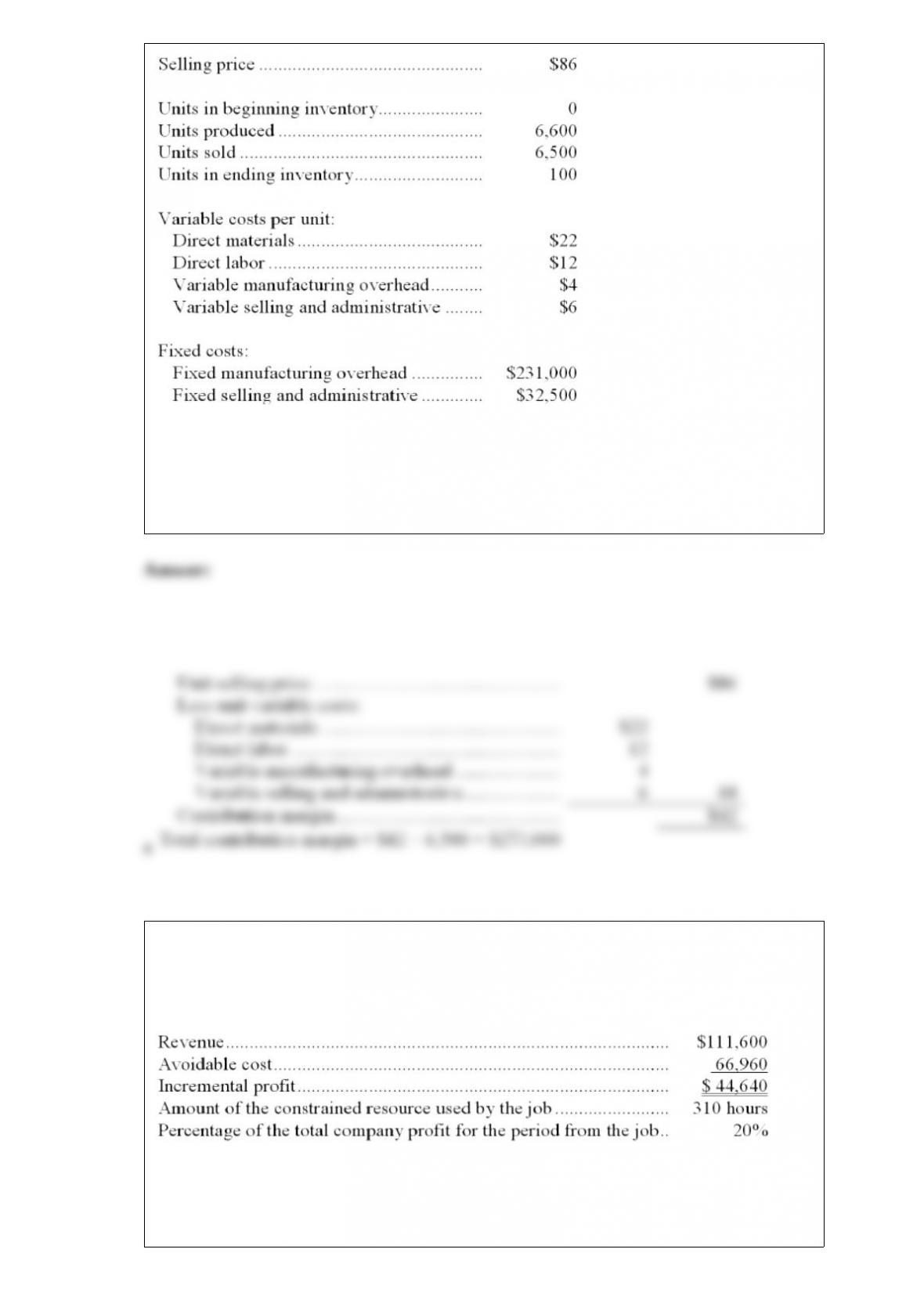

13) abdol company, which has only one product, has provided the following data

concerning its most recent month of operations:

the total contribution margin for the month under the variable costing approach is:

a.$273,000

b.$42,000

c.$84,500

d.$312,000

14) rognstad corporation would like to determine the relative profitability of a number

of jobs. for illustration purposes, the company has provided the following data for job

m38s:

what is the profitability index for job m38s?

a.$360 per hour

b.0.20

c.0.40

d.$144 per hour

15) crose inc. is working on its cash budget for november. the budgeted beginning cash

balance is $22,000. budgeted cash receipts total $118,000 and budgeted cash

disbursements total $116,000. the desired ending cash balance is $40,000.

to attain its desired ending cash balance for november, the company needs to borrow:

a.$16,000

b.$40,000

c.$0

d.$64,000

16) last year, perry company reported profits of $4,200. its variable expenses totaled

$66,000 or $6 per unit. the unit contribution margin was $3.00. the break-even point in

unit sales for perry company is:

a.11,000

b.9,600

c.22,000

d.12,400

17) an increase in appraisal costs will usually result in an increase in:

a.prevention costs

b.internal failure costs

c.external failure costs

d.opportunity costs

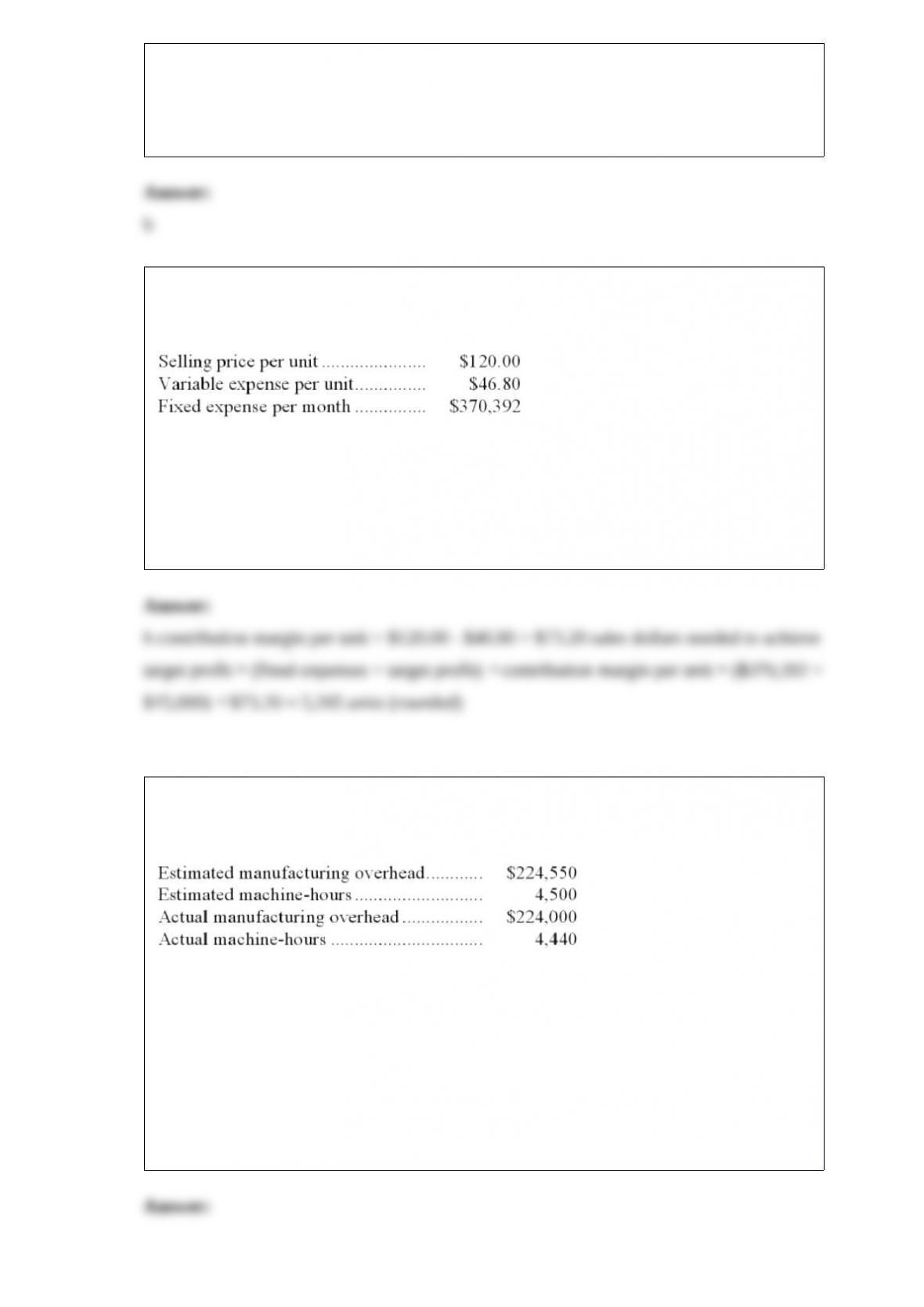

18) pedaci corporation produces and sells a single product. data concerning that product

appear below:

assume the company’s monthly target profit is $15,000. the unit sales to attain that

target profit is closest to:

a.3,212

b.5,265

c.8,235

d.5,571

19) acer corporation, which applies manufacturing overhead on the basis of

machine-hours, has provided the following data for its most recent year of operations.

the estimates of the manufacturing overhead and of machine-hours were made at the

beginning of the year for the purpose of computing the company’s predetermined

overhead rate for the year.

the overhead for the year was:

a.$2,994 underapplied

b.$2,444 overapplied

c.$2,444 underapplied

d.$2,994 overapplied