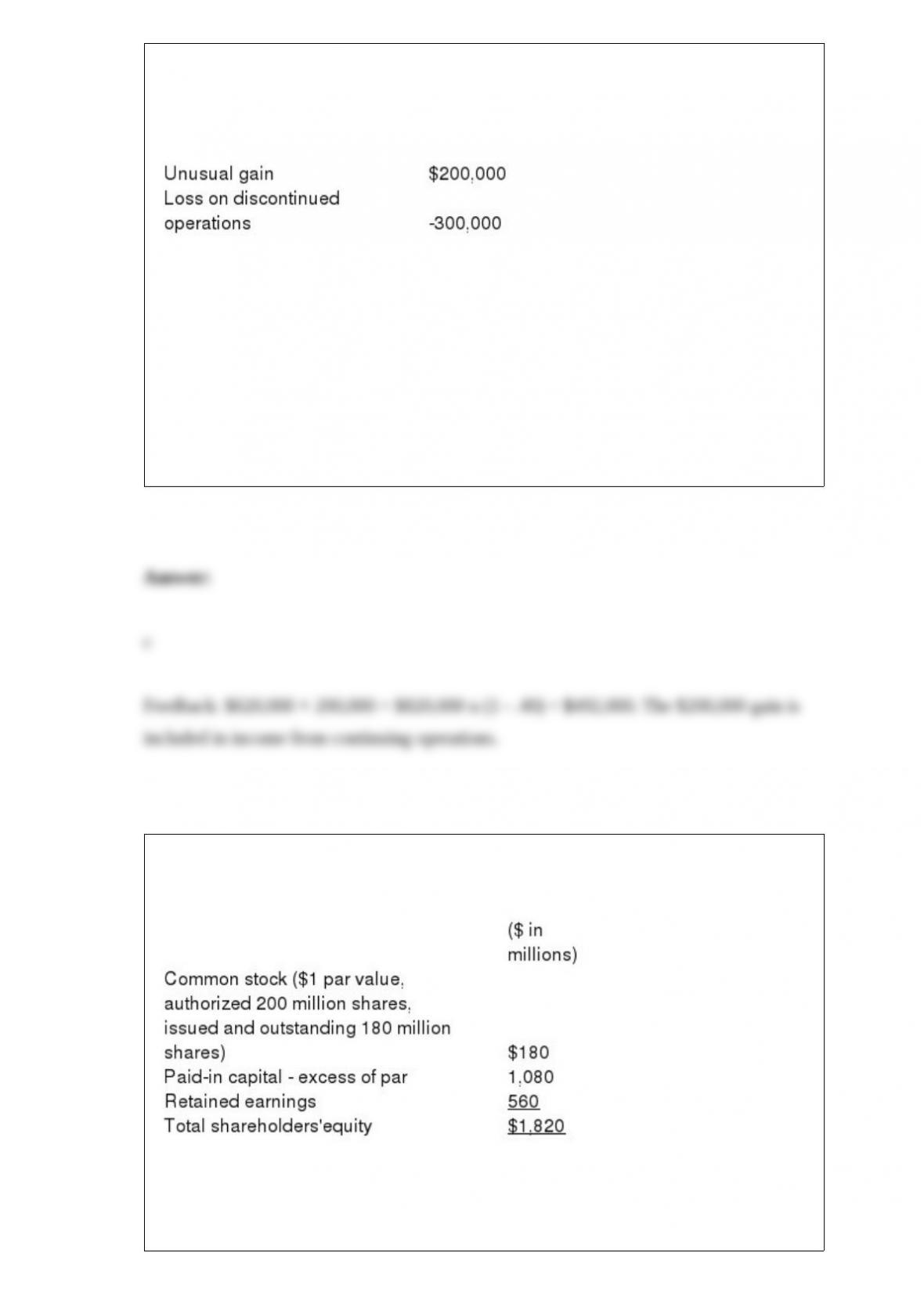

Jacobsen Corporation prepares its financial statement applying International Financial

Reporting Standards. During its 2016 fiscal year, the company reported before-tax

income of $620,000. This amount does not include the following two items, both of

which are considered to be material in amount:

The company’s income tax rate is 40%. In its 2016 income statement, Jacobsen would

report income from continuing operations of:

a. $312,000.

b. $372,000.

c. $492,000.

d. $620,000.

The balance sheet of FIFA Cup Company included the following shareholders’ ‘equity

section at December 31, 2016:

($ in millions)

Common stock ($1 par value,

authorized 200 million shares,

issued and outstanding 180 million shares) $ 180

Paid-in capital ‘“ excess of par 1,080

Retained earnings 560

Total shareholders’ equity $1,820

On January 5, 2017, FIFA purchased and retired 2 million shares for $9 million.

Immediately after retirement of the shares, the balances in the paid-in capital ‘“- excess

of par and retained earnings accounts are:

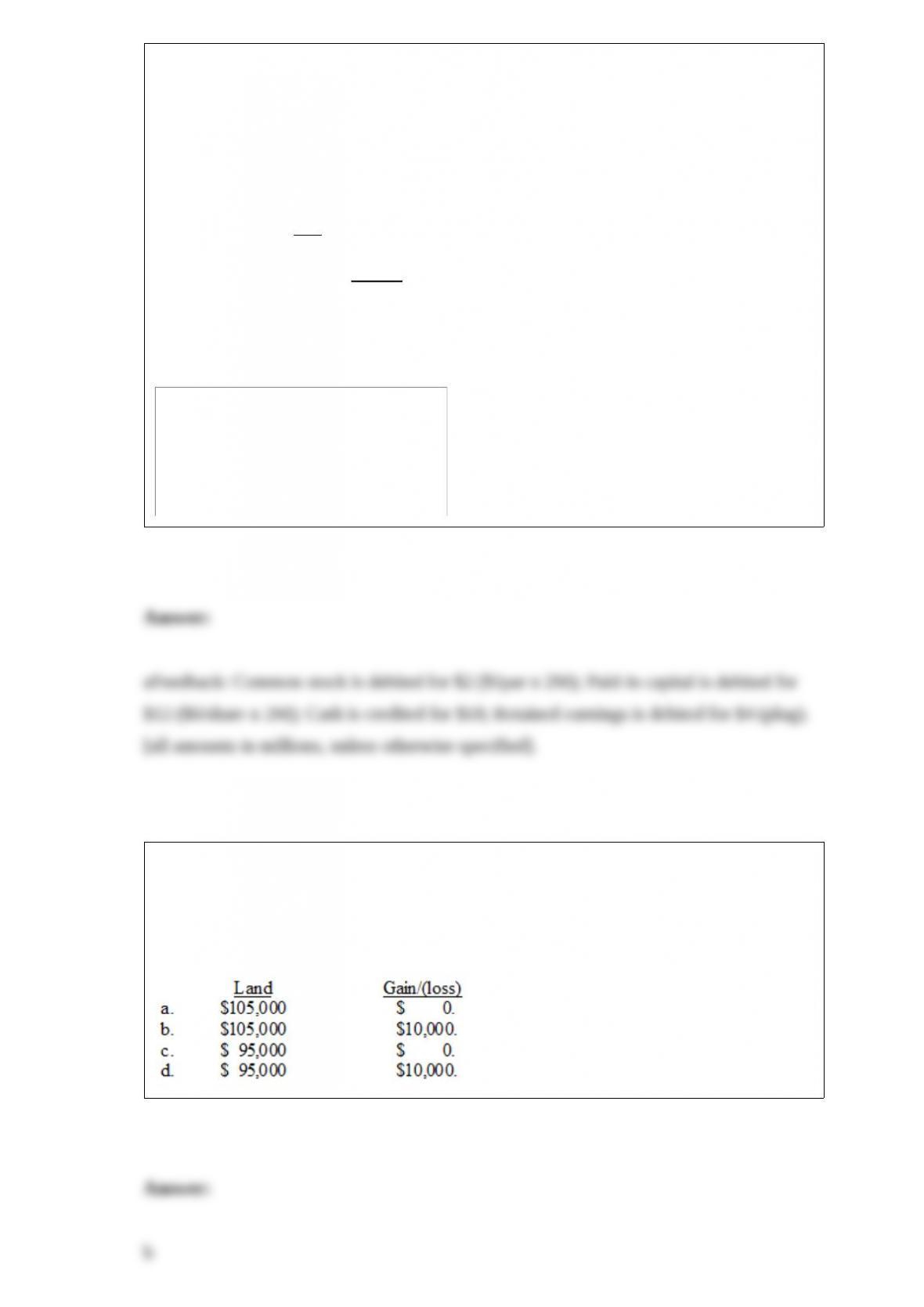

Horton Stores exchanged land and cash of $5,000 for similar land. The book value and

the fair value of the land were $90,000 and $100,000, respectively.

Assuming that the exchange has commercial substance, Horton would record land-new

and a gain/(loss) of:

Montana Mining Co. (MMC) paid $200 million for the right to explore and extract rare

metals from land owned by the state of Montana. To obtain the rights, MMC agreed to

restore the land to a suitable condition for other uses after its exploration and extraction

activities. MMC incurred exploration and development costs of $60 million on the

project. MMC has a credit-adjusted risk free interest rate is 7%. It estimates the possible

cash flows for restoring the land, three years after its extraction activities begin, as

follows:

The asset retirement obligation (rounded) that should be reported on MMC’s balance

sheet one year after the extraction activities begin is:

a. $0.

b. $14.7 million.

c. $15.7 million.

d. $19.3 million.

Which of the following is a correct statement concerning the reporting of the pension

plan on the face of the employer’s balance sheet?

a. Only the plan assets are separately reported.

b. Only the PBO is separately reported.

c. Both the PBO and the plan assets are separately reported.

d. Neither the PBO nor the plan assets is separately reported.

Lake Power Sports sells jet skis and other powered recreational equipment. Customers

pay one-third of the sales price of a jet ski when they initially purchase the ski, and then

pay another one-third each year for the next two years. Because Lake has little

information about the ability to collect these receivables, it uses the installment sales

method for revenue recognition. In 2015, Lake began operations and sold jet skis with a

total price of $900,000 that cost Lake $450,000. Lake collected $300,000 in 2015,

$300,000 in 2016, and $300,000 in 2017 associated with those sales. In 2016, Lake sold

jet skis with a total price of $1,500,000 that cost Lake $900,000. Lake collected

$500,000 in 2016, $400,000 in 2017, and $400,000 in 2018 associated with those sales.

In 2018, Lake also repossessed $200,000 of jet skis that were sold in 2016. Those jet

skis had a fair value of $75,000 at the time they were repossessed.

In its December 31, 2016, balance sheet, Lake would report:

a. Deferred gross profit of $700,000.

b. Deferred gross profit of $1,050,000.

c. Installment receivables (net) of $750,000.

d. Installment receivables (net) of $900,000.

The primary professional organization for those accountants working in industry is the:

a. AAA.

b. AICPA.

c. IIA.

d. IMA.

Jacobsen Corporation prepares its financial statements applying U.S. GAAP. During its

2016 fiscal year, the company reported before-tax income of $620,000. This amount

does not include the following two items, both of which are considered to be material in

amount:

The company’s income tax rate is 40%. In its 2016 income statement, Jacobsen would

report income from continuing operations of:

a. $312,000.

b. $372,000.

c. $492,000.

d. $620,000.

Flyaway Travel Company reported net income for 2016 in the amount of $90,000.

During 2016, Flyaway declared and paid $2,125 in cash dividends on its nonconvertible

preferred stock. Flyaway also paid $10,000 cash dividends on its common stock.

Flyaway had 40,000 common shares outstanding from January 1 until 10,000 new

shares were sold for cash on April 1, 2016. What is 2016 basic earnings per share?

a. $1.85.

b. $1.64.

c. $1.76.

d. None of these answer choices is correct.

A firm’s comprehensive income always:

a. Is the same as its net income.

b. Is greater than its net income.

c. Is less than its net income.

d. Could be greater than or less than net income.

If Pop Company exercises significant influence over Son Company and owns 40% of

its common stock, then Pop Company:

a. Would record dividends received from Son Company as investment revenue.

b. Would increase its investment account when Son Company declares dividends.

c. Would record 40% of the net income of Son Company as investment income each

year.

d. All of the above are correct.

Revenue on a long-term contract should not be recognized according to the proportion

of the performance obligation that has been completed if:

a. Completion rates are certain.

b. Profits are low.

c. Projects are more than five years to completion.

d. The arrangement does not qualify for revenue recognition over time.

Louie Company has a defined benefit pension plan. On December 31 (the end of the

fiscal year), the company received the PBO report from the actuary. The following

information was included in the report: ending PBO, $110,000; benefits paid to retirees,

$10,000; interest cost, $8,000. The discount rate applied by the actuary was 8%. What

was the service cost for the year?

a. $ 2,000.

b. $12,000.

c. $18,000.

d. $92,000.

Accounting for impairment losses:

a. Involves a two-step process for recoverability and measurement.

b. Applies only to depreciable assets.

c. Applies only to assets with finite lives.

d. All of these answer choices are correct.

The following information pertains to J Company’s outstanding stock for 2016:

What is the number of shares J should use to calculate 2016 basic earnings per share?

a. 20,000.

b. 22,500.

c. 25,000.

d. 27,000.

Reliable Enterprises sells distressed merchandise on extended credit terms. Collections

on these sales are not reasonably assured, and bad debt losses cannot be reasonably

predicted. It is unlikely that repossessed merchandise is in condition to be re-sold.

Therefore, Reliable uses the cost recovery method. Merchandise costing $30,000 was

sold for $55,000 in 2015. Collections on this sale were $20,000 in 2015, $15,000 in

2016, and $20,000 in 2017.

In 2016, Reliable would recognize gross profit of:

a. $0.

b. $ 6,000.

c. $ 5,000.

d. $10,000.

Payments to acquire bonds of other corporations should be classified on a statement of

cash flows as:

a. A lending activity.

b. An operating activity.

c. A financing activity.

d. An investing activity.

A net gain or loss affects the pension expense only if it exceeds an amount equal to

what percentage of the PBO or plan assets, whichever is higher?

a. 5%.

b. 10%.

c. 15%.

d. 20%.

Revenue for gift card breakage should be recognized:

a. When the gift card is sold.

b. No later than the last day of the operating period in which the gift card is delivered to

the customer.

c. When the probability of gift card redemption is viewed as remote.

d. Under no circumstances, as gift cards are not themselves a delivered product, but

rather a selling technique.

Briefly explain why the direct write-off of uncollectible accounts is not permitted by

GAAP if bad debts are material.

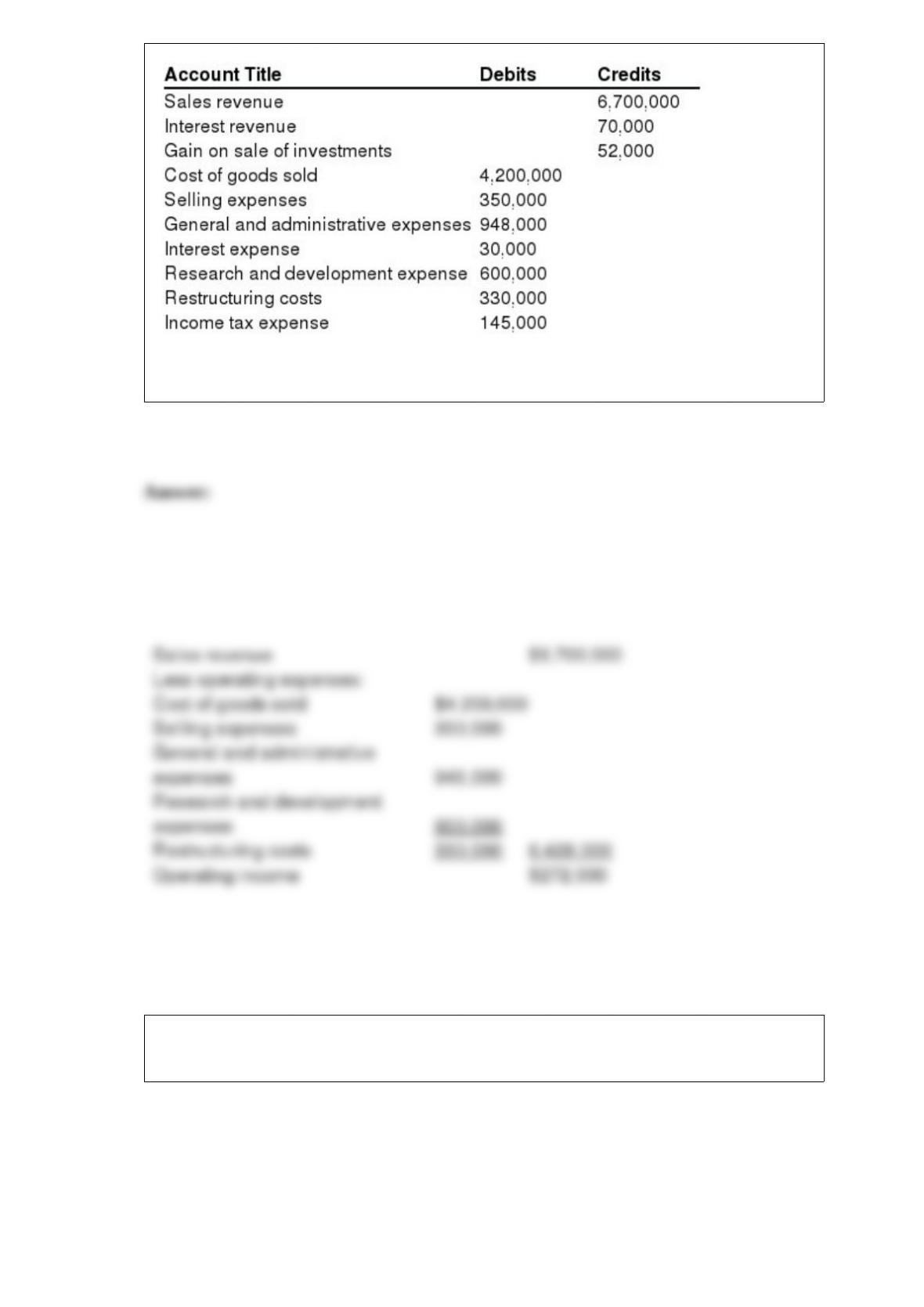

The Filzinger Corporation’s December 31, 2016 year-end trial balance contained the

following income statement items:

Required: Calculate the company’s operating income for the year using a single-step

income statement format.

Listed below are five terms followed by a list of phrases that describe or characterize

each of the terms. Match each phrase with the number for the correct term.

Briefly discuss the factors that determine the service life of a depreciable asset.

Listed below are five terms followed by a list of phrases that describe or characterize

each of the terms with respect to accounting for investments under IFRS. Match each

phrase with the correct term by placing the number designating the best term in the

space provided by the phrase.

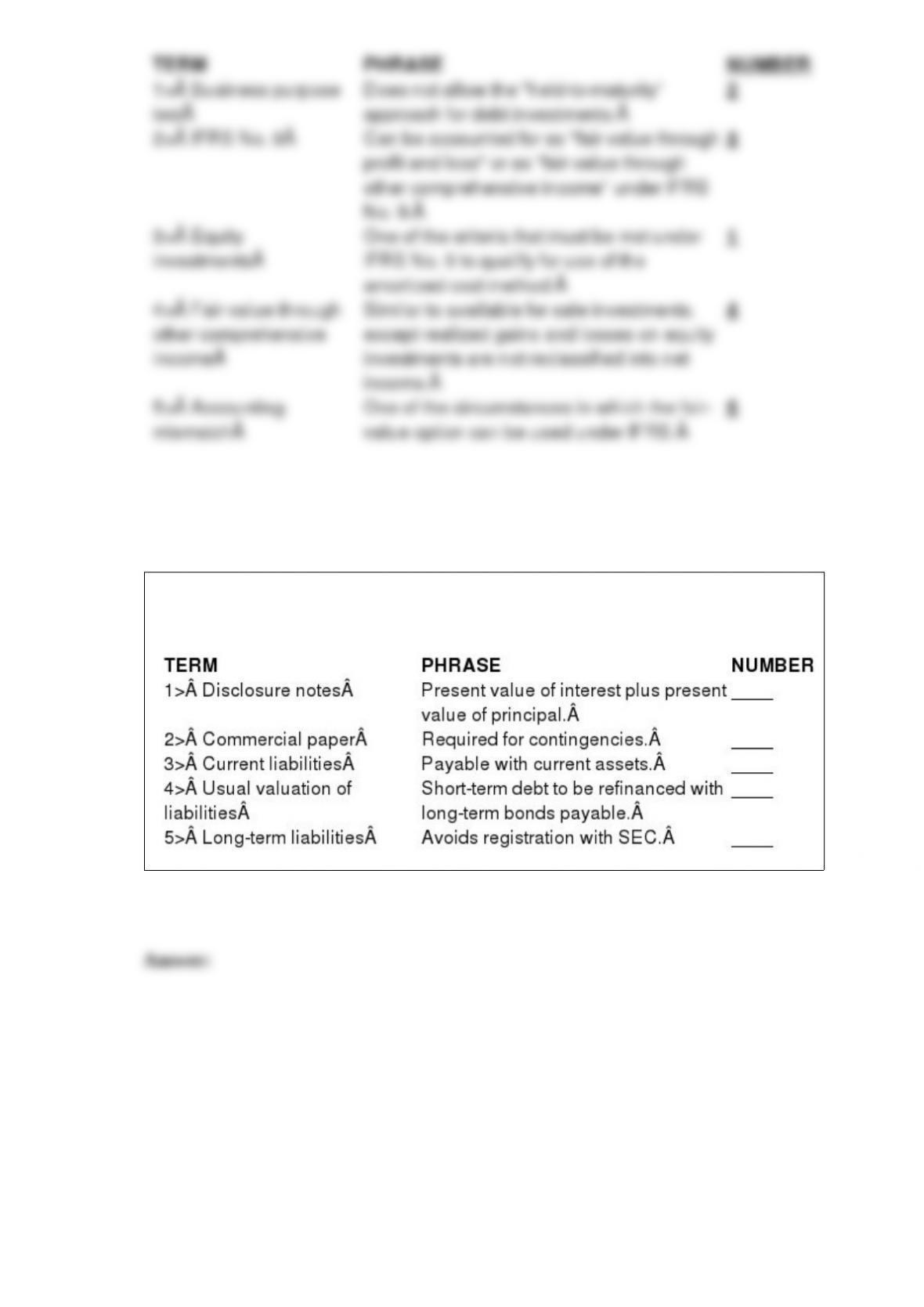

Listed below are five terms followed by a list of phrases that describe or characterize

each of the terms. Match each phrase with the number for the correct term.