1) An example of a service department is the human resources department.

2) Operating leases are long-term or noncancelable leases in which the lessor transfers

substantially all the risks and rewards of ownership to the lessee.

3) A properly designed internal control system is a key part of systems design, analysis,

and performance.

4) When merchandise is needed, a department manager must inform the purchasing

department of its needs by preparing and signing a purchase requisition which lists the

merchandise needed and requests that it be purchased.

5) Return on equity increases when the expected rate of return from the acquired assets

is higher than the interest rate on the debt issued to finance the acquired assets.

6) The cost of an inventory item includes its invoice cost minus any discount, and plus

any added or incidental costs necessary to put it in a place and condition for sale.

7) Future value can be found if the interest rate (i), the number of periods (n), and the

present value (p) are known.

8) To be classified as a cash equivalent, the only criterion an item must meet is that it

must be readily convertible to a known amount of cash.

9) A premium on bonds occurs when bonds carry a contract rate greater than the market

rate at issuance and the premium reduces the interest expense of the bond over its life.

10) Managerial accounting information can be forwarded to the managers of a company

quickly since external auditors do not have to review it, and estimates and projections

are acceptable.

11) Internal control in technologically advanced accounting systems depends more on

the design and operation of the information system and less on the analysis of its

resulting documents.

12) A discount on bonds payable occurs when a company issues bonds with an issue

price less than par value.

13) A company pays each of its two office employees each Friday at the rate of $100

per day for a five-day week that begins on Monday. If the monthly accounting period

ends on Tuesday and the employees worked on both Monday and Tuesday, the

month-end adjusting entry to record the salaries earned but unpaid is:

A.Debit Unpaid Salaries $600 and credit Salaries Payable $600

B.Debit Salaries Expense $400 and credit Salaries Payable $400

C.Debit Salaries Expense $600 and credit Salaries Payable $600

D.Debit Salaries Payable $400 and credit Salaries Expense $400

E.Debit Salaries Expense $400 and credit Cash $400

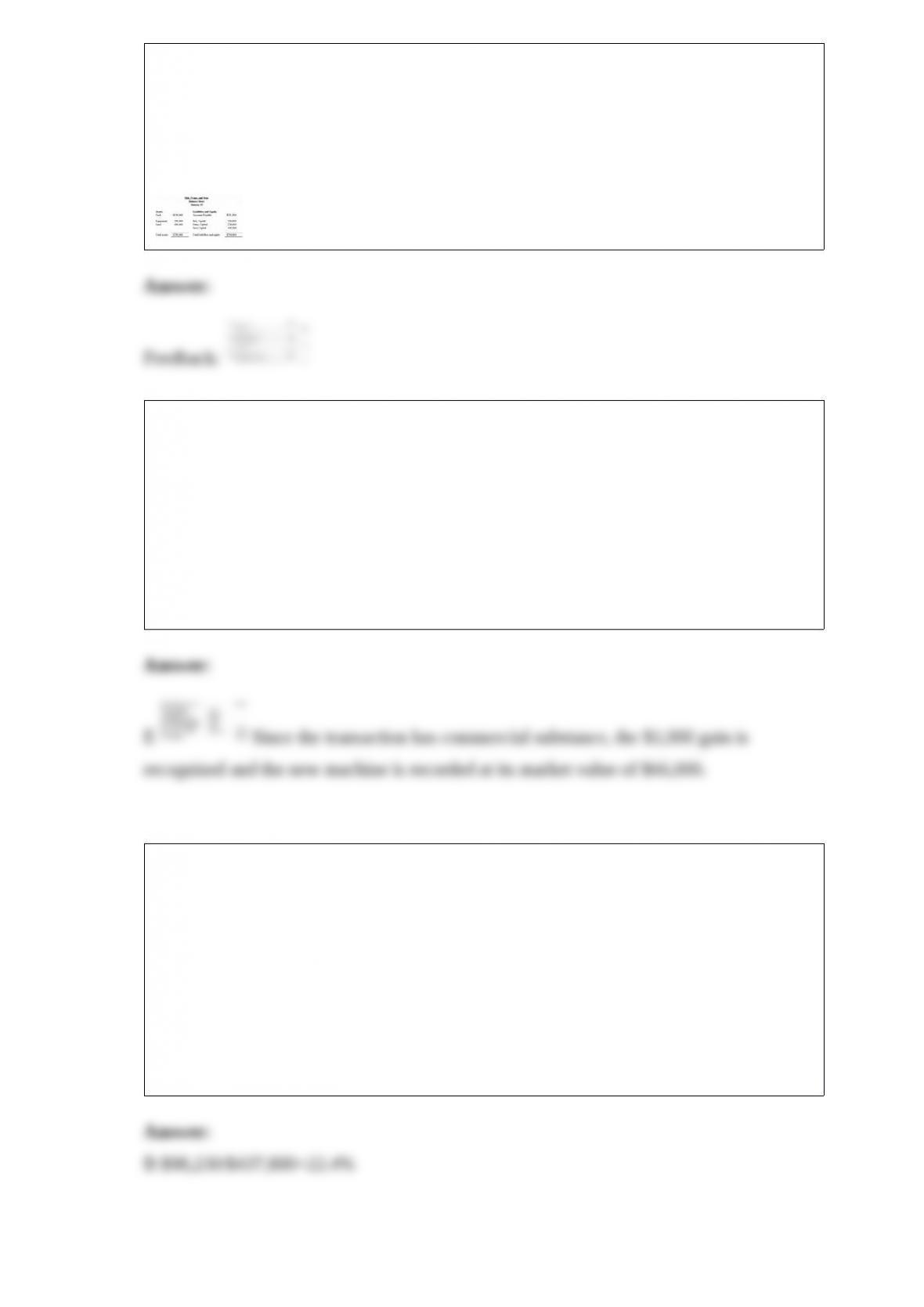

14) The following year-end adjusted trial balance is for Tom Janes Co. at the end of

December 31. The credit balance in Tom Janes, Capital at the beginning of the year,

January 1, was $320,000. The owner, Tom Janes, invested an additional $300,000

during the current year. The land held for future expansion was also purchased during

the current year.

Required: 1. Prepare a classified year-end balance sheet. (Note: A $22,000 installment

on the long-term note payable is due within one year.)

2. Using the information presented:

(a) Calculate the current ratio. Comment on the ability of Tom Janes Co. to meets its

short-term debts.

(b) Calculate the debt ratio and comment on the financial position and risk analysis of

Tom Janes Co.

(c) Using the account balances to analyze the financial position of Tom Janes Co., why

would the owner need to invest an additional $300,000 in the business when the

business is already profitable and the owner had an existing capital balance of

$320,000?

15) A company’s net sales are $775,420, its costs of goods sold are $413,890, and its net

income is $117,220. Its gross margin ratio equals:

A.46.6%.

B.53.4%.

C.28.3%.

D.31.5%.

E.40.5%.

16) The costs of bringing a corporation into existence, including legal fees, promoter

fees, and amounts paid to obtain a charter are called:

A.Minimum legal capital

B.Stock subscriptions

C.Organization expenses

D.Selling expenses

E.Prepaid fees

17) Calco accepts all major bank credit cards, including First Bank’s, which assesses a

3.5% charge on sales for using its card. On May 25, Calco had $4,800 in First Bank

Card credit sales. What entry should Calco make on May 25 to record the deposit?

A.Debit Accounts Receivable $4,800; credit Sales $4,800

B.Debit Cash $4,632; debit Credit Card Expense $168; credit Sales $4,800

C.Debit Cash $4,800; credit Sales $4,800

D.Debit Cash $4,968; credit Credit Card Expense $168; credit Sales $4,800

E.Debit Accounts Receivable $4,632; debit Credit Card Expense $168; credit Sales

$4,800

18) Cost accounting systems used by manufacturing companies are based on the:

A.Periodic inventory system

B.Perpetual inventory system

C.Finished goods inventories

D.Weighted average inventories

E.LIFO inventory system

19) The flexibility principle of accounting information systems prescribes that the:

A.Benefits from an activity outweigh the costs of the activity

B.System report useful, understandable, timely, and pertinent information for effective

decision making

C.System aid managers in controlling and monitoring business activities

D.System be able to adapt to changes in the company, business environment, and needs

of decision makers

E.System conforms to a company’s activities, personnel, and structure

20) A company has net income of $250,000, net sales of $2,000,000, and average total

assets of $1,500,000. Its return on total assets equals:

A.12.5%

B.13.3%

C.16.7%

D.75.0%

E.600.0%

21) The credit purchase of a delivery truck for $4,700 was posted to Delivery Trucks as

a $4,700 debit and to Accounts Payable as a $4,700 debit. What effect would this error

have on the trial balance?

A.The total of the Debit column of the trial balance will exceed the total of the Credit

column by $4,700

B.The total of the Credit column of the trial balance will exceed the total of the Debit

column by $4,700

C.The total of the Debit column of the trial balance will exceed the total of the Credit

column by $9,400

D.The total of the Credit column of the trial balance will exceed the total of the Debit

column by $9,400

E.The total of the Debit column of the trial balance will equal the total of the Credit

column

22) Parker Plumbing has received a special one-time order for 1,500 faucets (units) at

$5 per unit. Parker currently produces and sells 7,500 units at $6.00 each. This level

represents 75% of its capacity. Production costs for these units are $4.50 per unit, which

includes $3.00 variable cost and $1.50 fixed cost. To produce the special order, a new

machine needs to be purchased at a cost of $1,000 with a zero salvage value.

Management expects no other changes in costs as a result of the additional production.

Should the company accept the special order?

A.No, because additional production would exceed capacity

B.No, because incremental costs exceed incremental revenue

C.Yes, because incremental revenue exceeds incremental costs

D.Yes, because incremental costs exceed incremental revenues

E.No, because the incremental revenue is too low

23) Identify the risk and the return in each of the following examples.

a. Investing $500 in a CD at 4.5% interest.

b. Placing a $100 bet on an NBA game.

c. Investing $10,000 in Microsoft stock.

d. Borrowing $20,000 in student loans.

24) In business decision-making, managers typically examine the two fundamental

factors of:

A.Risk and capital investment

B.Risk and rate of return

C.Capital investment and rate of return

D.Risk and payback

E.Payback and rate of return

25) Brit, Franc, and Scot who share income and loss in a 2:2:1 ratio, plan to liquidate

their partnership. At liquidation, their balance sheet appears as follows. Prepare journal

entries for (a) the sale of land and equipment sold as a package for $500,000, (b) the

allocation of the gain or loss, (c) the payment of the liabilities, and (d) the distribution

of cash to the individual partners.

26) A company purchased a machine valued at $66,000. It traded in an old machine for

a $9,000 trade-in allowance and the company paid $57,000 cash with the trade-in. The

old machine cost $44,000 and had accumulated depreciation of $36,000. This

transaction has commercial substance. What is the recorded value of the new machine?

A.$8,000

B.$9,000

C.$57,000

D.$65,000

E.$66,000

27) A company had average total assets of $982,450 and net income of $190,700, and

reports various segment information. Segment A had average total assets of $437,800

and segment operating income of $98,230. Segment B had average assets of $151,200

and segment operating income of $16,190. Calculate the segment return on assets for

Segment A.

A.19.4%

B.22.4%

C.26.1%

D.10.7%

E.20.2%

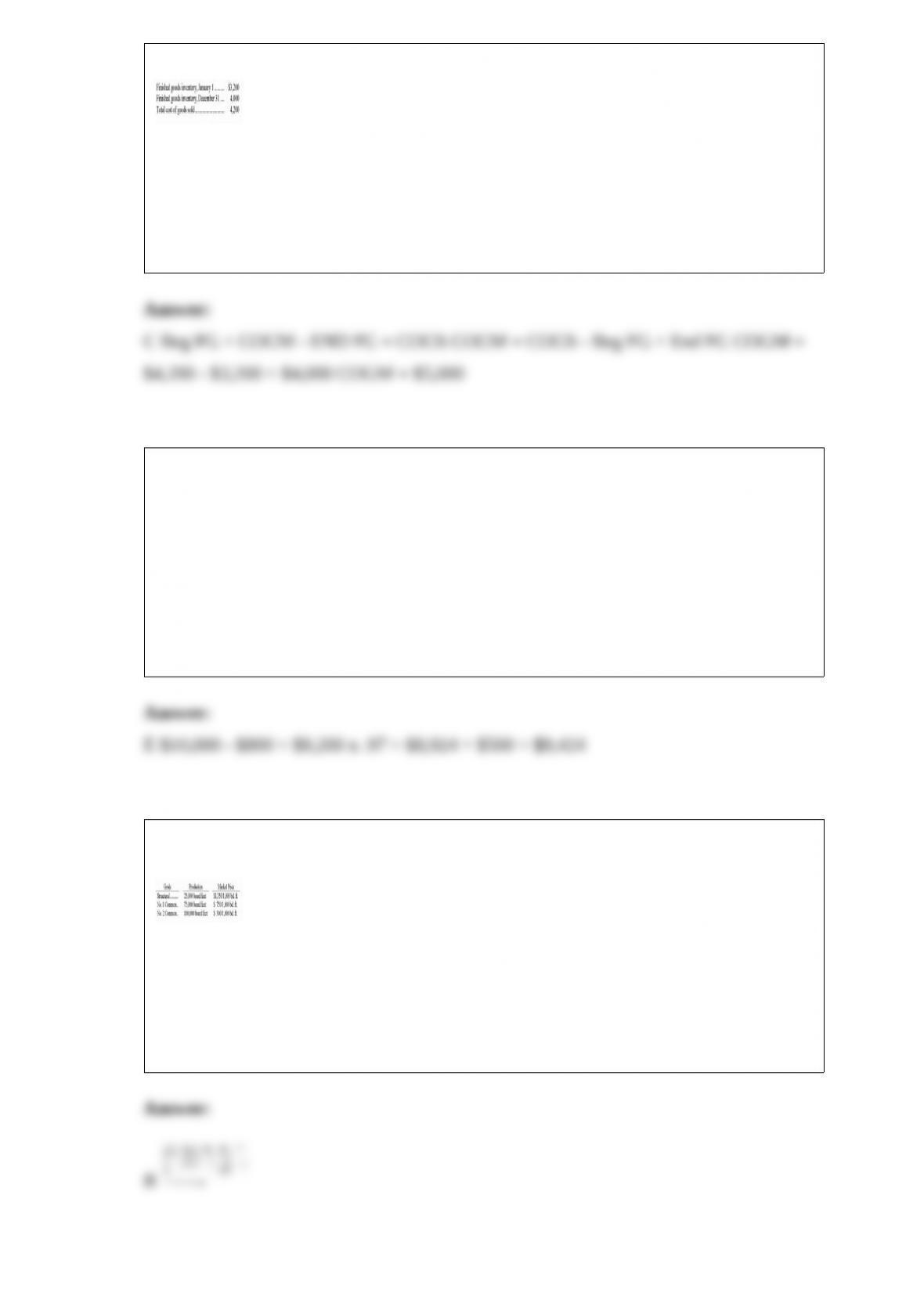

28) Juliet Corporation has accumulated the following accounting data for the year:

The cost of goods manufactured for the year is:

A.$200

B.$1,000

C.$5,000

D.$6,400

E.$8,200

29) A company purchased $10,000 of merchandise on June 15 with terms of 3/10, n/45,

and FOB shipping point. The freight charge was $500. On June 20, it returned $800 of

that merchandise. On June 24, it paid the balance owed for the merchandise taking any

discount it is entitled to. The cash paid on June 24 equals:

A.$9,224.

B.$10,200.

C.$10,500.

D.$10,300.

E.$9,424.

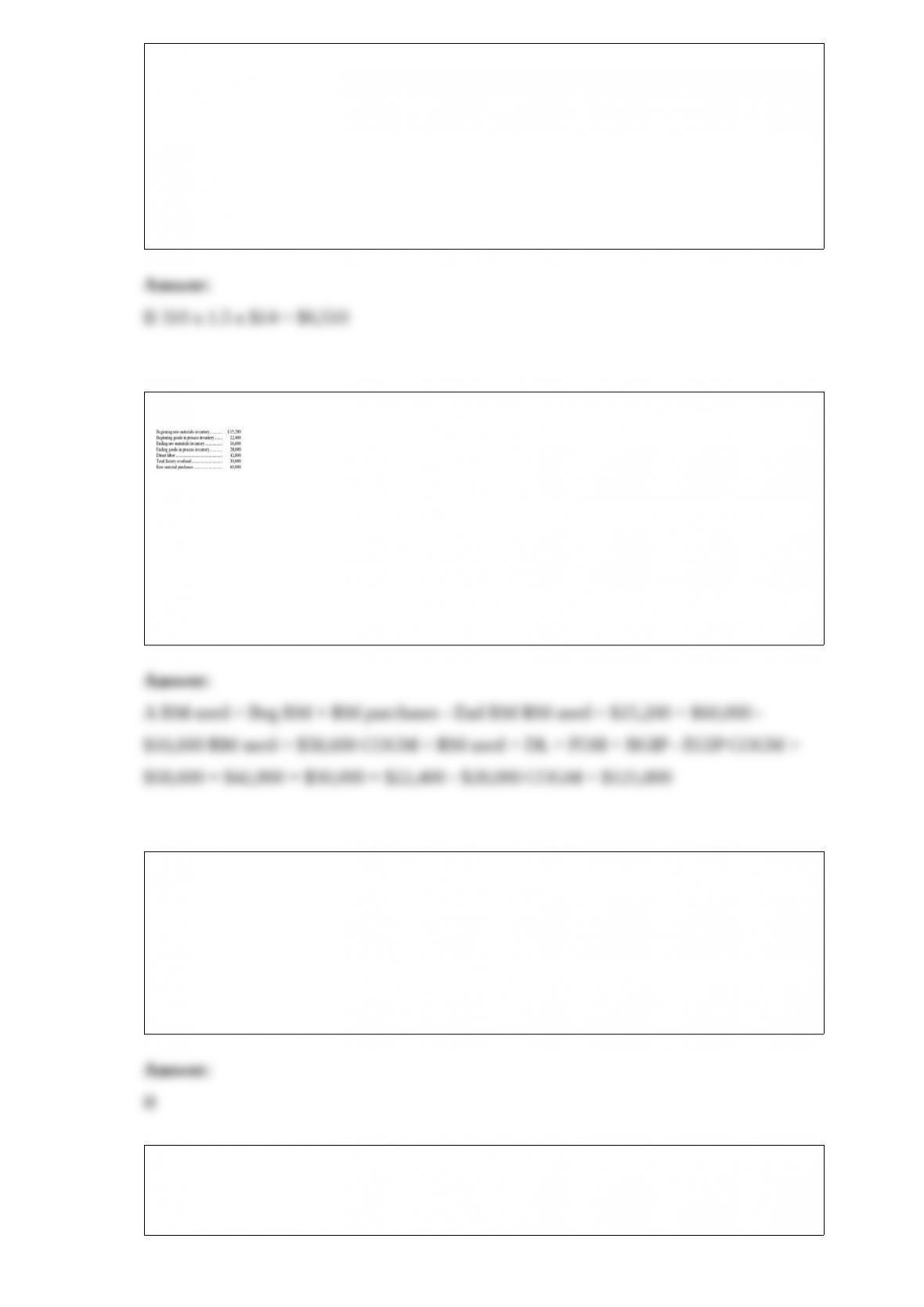

30) A sawmill paid $70,000 for logs that produced 200,000 board feet of lumber in 3

different grades and amounts as follows:

Compute the portion of the $70,000 joint cost to be allocated to No. 2 Common.

A.$0

B.$17,500

C.$23,333

D.$35,000

E.$70,000

31) Grafton budgets production of 300 units in June and 310 units in July. Each unit

requires 1.5 hours of direct labor. The direct labor rate if $14 per hour. The indirect

labor rate is $21.00 per hour. Compute the budgeted direct labor cost for July.

A.$6,300

B.$6,510

C.$9,450

D.$9,765

E.$16,275

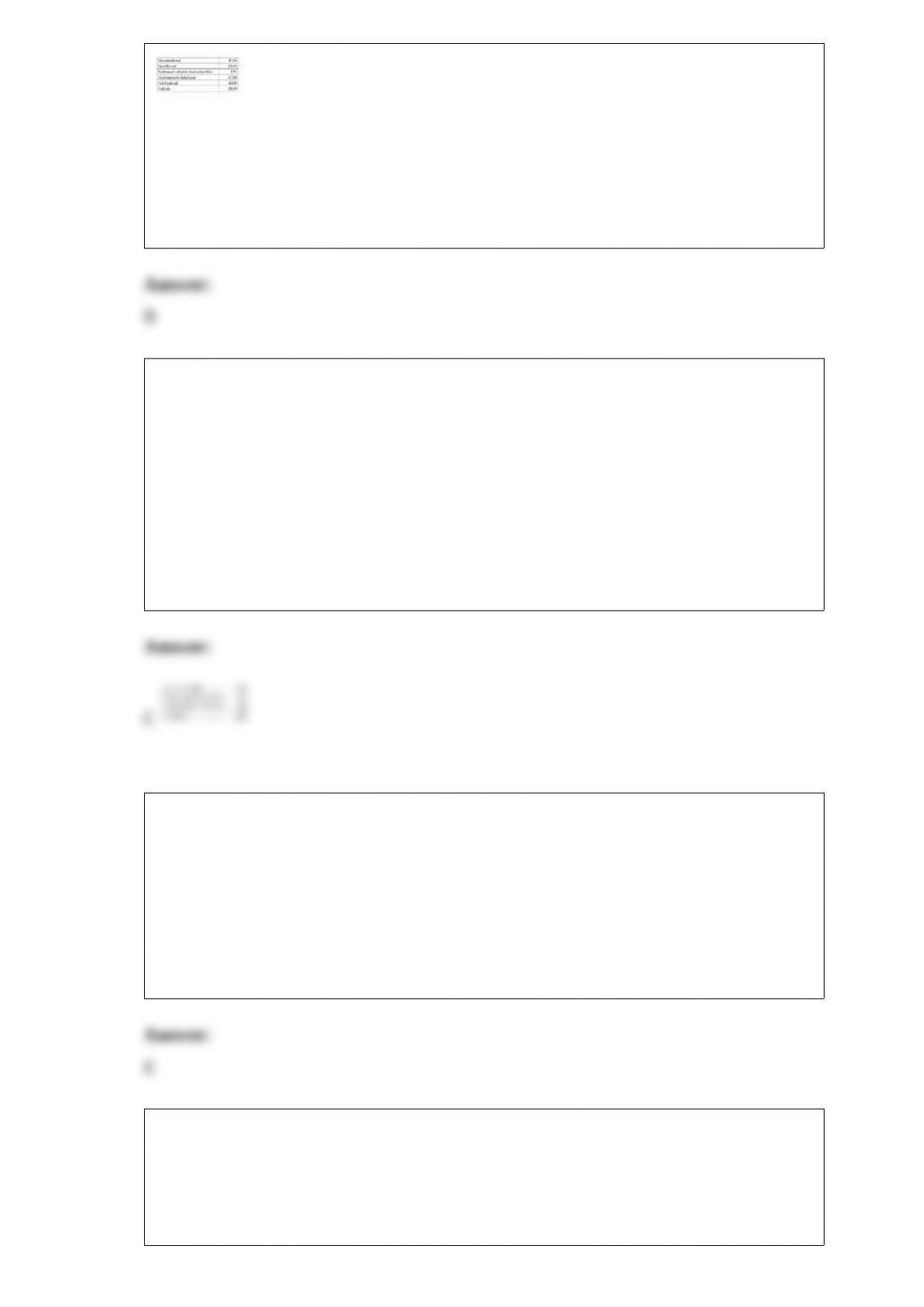

32) Current information for the Austin Company follows:

All raw materials used were traceable to specific batches of product. Austin Company’s

cost of goods manufactured for the year is:

A.$125,800

B.$128,600

C.$131,400

D.$137,000

E.$139,000

33) The appropriate section in the statement of cash flows for reporting the issuance of

common stock for cash is:

A.Operating activities

B.Financing activities

C.Investing activities

D.Schedule of noncash investing or financing activity

E.None of these. This is not reported on the statement of cash flows

34) Embark produces mulch for landscaping use. The following information

summarizes production operations for June. The journal entry to record June production

activities for direct labor usage is:

A.Debit Factory Payroll $160,000; credit Cash $160,000

B.Debit Goods in Process Inventory $160,000; credit Factory Payroll $160,000

C.Debit Cost of Goods Sold $160,000; credit Factory Payroll $160,000

D.Debit Goods in Process Inventory $160,000; credit Raw Materials Inventory

$160,000

E.Debit Goods in Process Inventory $160,000; credit Cash $160,000

35) Kent Company anticipates total sales for April, May, and June of $800,000,

$900,000, and $950,000 respectively. Cash sales are normally 25% of total sales. Of the

credit sales, 30% are collected in the same month as the sale, 65% are collected during

the first month after the sale, and the remaining 5% are not collected. Compute the

amount of cash received from total sales for May.

A.$561,500

B.$652,500

C.$817,500

D.$592,500

E.$890,000

36) An analytical technique used by management to focus on the most significant

variances and give less attention to the areas where performance is satisfactory is

known as:

A.Controllable management

B.Management by variance

C.Performance management

D.Management by objectives

E.Management by exception

37) Kent Company anticipates total sales for April, May, and June of $800,000,

$900,000, and $950,000 respectively. Cash sales are normally 25% of total sales. Of the

credit sales, 30% are collected in the same month as the sale, 65% are collected during

the first month after the sale, and the remaining 5% are collected in the second month.

Compute the amount of accounts receivable reported on the company’s budgeted

balance sheet for June 30.

A.$561,500

B.$712,500

C.$463,125

D.$496,875

E.$617,500

38) The conservatism constraint:

A.Prescribes that when multiple estimates of amounts to be received or paid in the

future are equally likely, then the least optimistic amount should be used

B.Prescribes that a company use the same accounting methods period after period

C.Prescribes that revenues and expenses be reported in the period in which they are

earned or incurred

D.Prescribes that all items of a material nature be included in financial statements

E.Prescribes that all inventory items be reported at full cost

39) Zion Company has assets of $600,000, liabilities of $250,000, and equity of

$350,000. It buys office equipment on credit for $75,000. What would be the effects of

this transaction on the accounting equation?

A.Assets increase by $75,000 and expenses increase by $75,000

B.Assets increase by $75,000 and expenses decrease by $75,000

C.Liabilities increase by $75,000 and expenses decrease by $75,000

D.Assets decrease by $75,000 and expenses decrease by $75,000

E.Assets increase by $75,000 and liabilities increase by $75,000

40) Match the following terms with the appropriate definition.

1>Accounting cycle A. Analyses and other informal reports prepared by accountants

when organizing the information presented in reports and financial statements.

2>Temporary accounts B. The time span from when cash is used to acquire goods and

services until cash is received from the sale of those goods and services.

3>Operating cycle of a business C. A temporary account used only in the closing

process and to where the balances of revenue and expense accounts are transferred.

4>Post-closing trial balance D. A spreadsheet used to draft an unadjusted trial balance,

adjusting entries, adjusted trial balance, and financial statements.

5>Work sheet E. A list of permanent accounts and their balances from the ledger after

all closing entries and are journalized and posted.

6>Pro forma statements F. Recurring steps performed each accounting period, starting

with analyzing and recording of transactions in the journal and continuing through the

post-closing trial balance (or reversing entries).

7>Income summary G. Entries recorded at the end of each accounting period to transfer

end-of-period balances and in revenue, expense, and withdrawals accounts to the

permanent owner’s capital account.

8>Permanent accounts H. Statements that show the effects of proposed transactions as

if the transactions had already occurred.

9>Working papers I. Accounts that reflect on activities related to one or more future

periods; they include all balance sheet accounts.

10>Closing entries J. Accounts that are used to record transactions and events for one

accounting period only; they include revenues, expenses, and withdrawals.

41) The following information is available to reconcile Cloy Company’s book balance

of cash with its bank statement cash balance as of June 30. The June 30 cash balance

according to the accounting records is $58,542, and the bank statement cash balance for

that date is $68,047.

a. The bank erroneously cleared a $395 check against the account in June that was not

issued by Cloy. The check documentation included with the bank statement indicates

the check was actually issued by Clare Co.

b. On June 30, the bank issued a credit memorandum for $35 interest earned on Cloy’s

account.

c. When the June checks are compared with entries in the accounting records, it is

found that Check No. 1727 had been correctly drawn for $1,450 to pay for advertising

but was erroneously entered in the accounting records as $1,540.

d. A credit memorandum indicates that the bank collected $9,000 cash on a note

receivable for Cloy, deducted a $30 collection fee, and credited the balance to the

company’s Cash account. Cloy did not record this transaction before receiving the

statement.

e. A debit memorandum of $895 is enclosed with the bank statement for an NSF check

for $870 received from a customer. The bank assessed a $25 fee for processing it.

f. Cloy’s June 30 daily cash receipts of $6,325 were placed in the bank’s night

depository on that date, but do not appear on the June 30 bank statement.

g. Cloy’s June 30 cash disbursements journal indicates that Check No. 1737 for $4,830

and Check No. 1740 for $3,280 were both written and entered in the accounting

records, but are not among the canceled checks.

h. A debit memorandum for $85.00 indicates the bank deducted the annual lock box fee

for the company.

1> Prepare the bank reconciliation for this company as of June 30.

2> Prepare the journal entries necessary to bring the company’s book balance of cash

into conformity with the reconciled cash balance as of June 30.

42) On December 31, a company needed to estimate its ending inventory to prepare its

fourth quarter financial statements. The following information is currently available:

Inventory as of October 1: $12,500

Net sales for fourth quarter: $40,000

Net purchases for fourth quarter: $27,500

This company typically achieves a gross profit ratio of 15%. Ending Inventory under

the gross profit method would be:

A.$4,000

B.$6,000

C.$10,000

D.$16,000

E.$34,000

43) Sales less sales discounts less sales returns and allowances equals:

A.Net purchases.

B.Cost of goods sold.

C.Net sales.

D.Gross profit.

E.Net income.

44) Managerial accounting is different from financial accounting in that

A.Managerial accounting is more focused on the organization as a whole and financial

accounting is more focused on subdivisions of the organization

B.Managerial accounting never includes nonmonetary information

C.Managerial accounting includes many projections and estimates whereas financial

accounting has a minimum of predictions

D.Managerial accounting is used extensively by investors, whereas financial accounting

is used only by creditors

E.Managerial accounting is mainly used to set stock prices

45) On April 30, Holden Company had an Accounts Receivable balance of $18,000.

During the month of May, total credits to Accounts Receivable were $52,000 from

customer payments. The May 31 Accounts Receivable balance was $13,000. What was

the amount of credit sales during May?

A.$5,000

B.$47,000

C.$52,000

D.$57,000

E.$32,000

46) Standards for comparisons in financial statement analysis include:

A.Intracompany standards

B.Competitors’ standards

C.Industry standards

D.Guidelines (rules of thumb)

E.All of these

47) If a company borrows money from a bank, the interest paid on this loan should be

reported on the statement of cash flows as a(n):

A.Operating activity

B.Investing activity

C.Financing activity

D.Noncash investing and financing activity

E.None of these. This is not reported in the statement of cash flows

48) All of the following regarding current ratio are true except:

A.Current ratio is calculated by dividing current assets by current liabilities

B.Current ratio helps to assess a company’s ability to pay its debts in the near future

C.Current ratio does not affect a creditor’s decision on when to allow a company to buy

on credit

D.Current ratio can affect a creditor’s decision about whether to lend money to a

company

E.Current ratio can reveal problems in a company if it is less than 1

49) A corporation reported average total assets in Year 1 of $397,350 and $440,800 in

Year 2. Its net operating cash flow for Year 1 was $35,667 and $35,790 for Year 2.

Calculate the cash flow on total assets ratio for both years. Comment on the results.

50) Differences between actual costs and standard costs are known as

__________________. These differences may be subdivided into _________________

and ________________.

51) On January 2, Froxel Company purchased 10,000 shares of Sandia Corp. common

stock at $19 per share plus a $3,000 commission. This represents 30% of Sandia Corp.’s

outstanding stock. On August 6, Sandia Corp. declared and paid cash dividends of

$1.75 per share, and on December 31 it reported net income of $150,000. Prepare the

necessary entries for Froxel to account for these transactions and events.

52) Durango and Verde formed a partnership with capital contributions of $150,000 and

$190,000, respectively. Their partnership agreement called for Durango to receive a

$50,000 annual salary allowance. They also agreed to allow each partner a share of

income equal to 10% of their initial capital investments. The remaining income or loss

is to be divided equally. If the net income for the current year is $120,000, what are

Durango’s and Verde’s respective shares?

53) A company uses the periodic inventory system, and the following information is

available. All purchases and sales are on credit.

1> Prepare the general journal entries to record:

The October 6 purchase.

The October 12 sale.

2> Assuming the periodic inventory system is used, determine both the cost of the

ending inventory and the cost of goods sold using the LIFO method for October.

54) Explain the impact, if any, on depreciation when estimates that determine

depreciation change.

55) ______________________ are nonoperating activities that include interest expense,

losses from asset disposals, and casualty losses.

56) Prepare journal entries to record the following merchandise transactions of Geo

Company, which applies the perpetual inventory system.