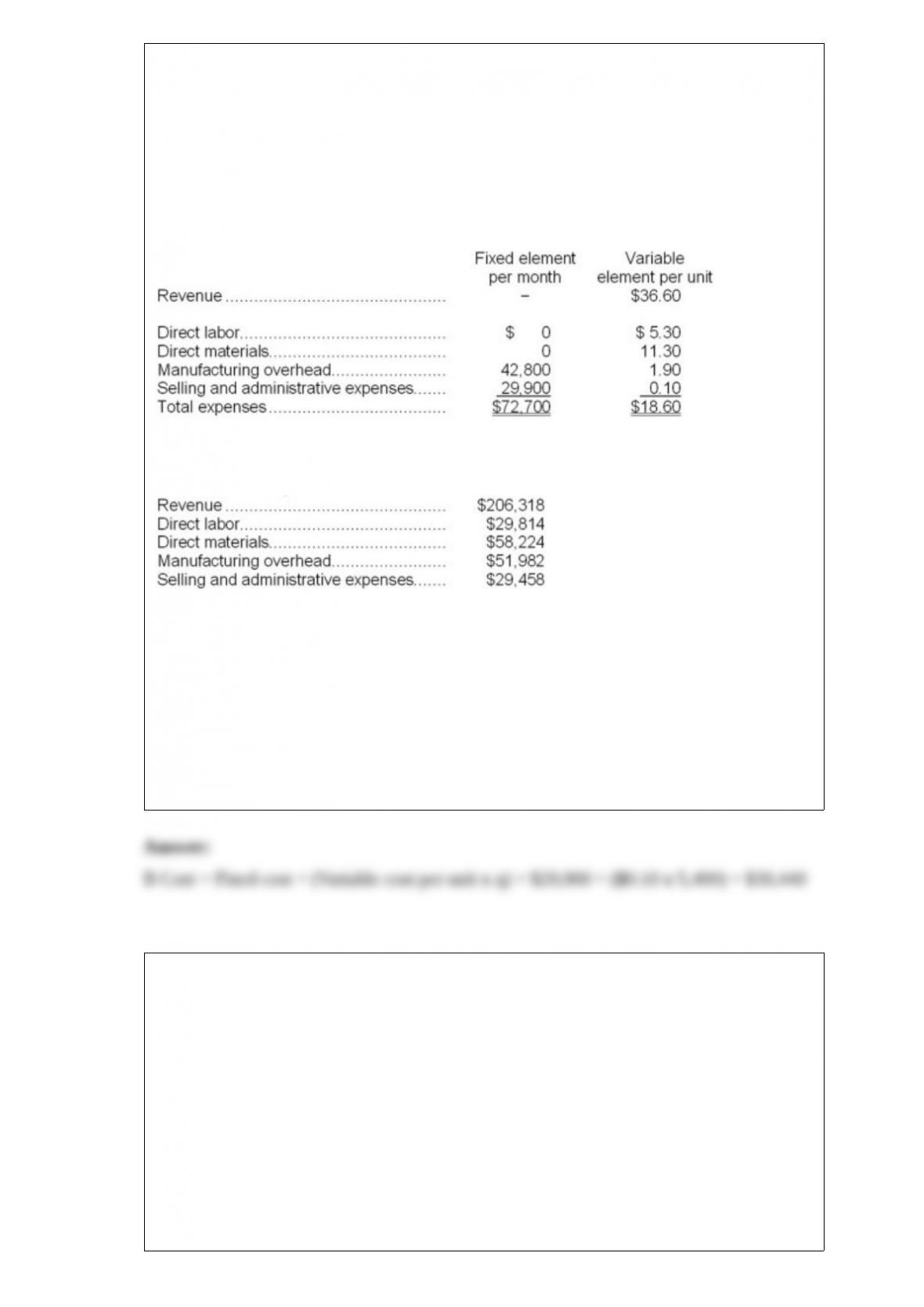

1) Linscott Corporation manufactures and sells a single product. The company uses

units as the measure of activity in its budgets and performance reports. During July, the

company budgeted for 5,400 units, but its actual level of activity was 5,380 units. The

company has provided the following data concerning the formulas used in its budgeting

and its actual results for July:

Data used in budgeting:

Actual results for July:

The selling and administrative expenses in the planning budget for July would be

closest to:

A.$30,438

B.$30,440

C.$29,458

D.$29,568

2) Division A makes watzits. The company has sufficient capacity to make 70,000

watzits per year. The company expects to sell 65,000 watzits this year. Division B uses

watzits in their production and has total needs of 20,000 watzits this year. Division B is

presently buying watzits from an outside supplier for $11.25 each. The cost to Division

A to make the watzits are $5.00 for direct materials, $2.00 for direct labor, $2.50 for

variable manufacturing overhead, and $1.50 for fixed manufacturing overhead. Direct

labor is a variable cost. Division A sells watzits on the outside market for $11.50 each.

Required:

a. Assuming that Division B buys its entire 20,000 requirement of watzits from Division

A, is it possible for Division A and Division B to agree to a mutually acceptable transfer

price and if so, within what range would that transfer price be?

b. Assuming that Division B buys only 5,000 watzits from Division A, is it possible for

Division A and Division B to agree to a mutually acceptable transfer price and if so,

within what range would that transfer price be?

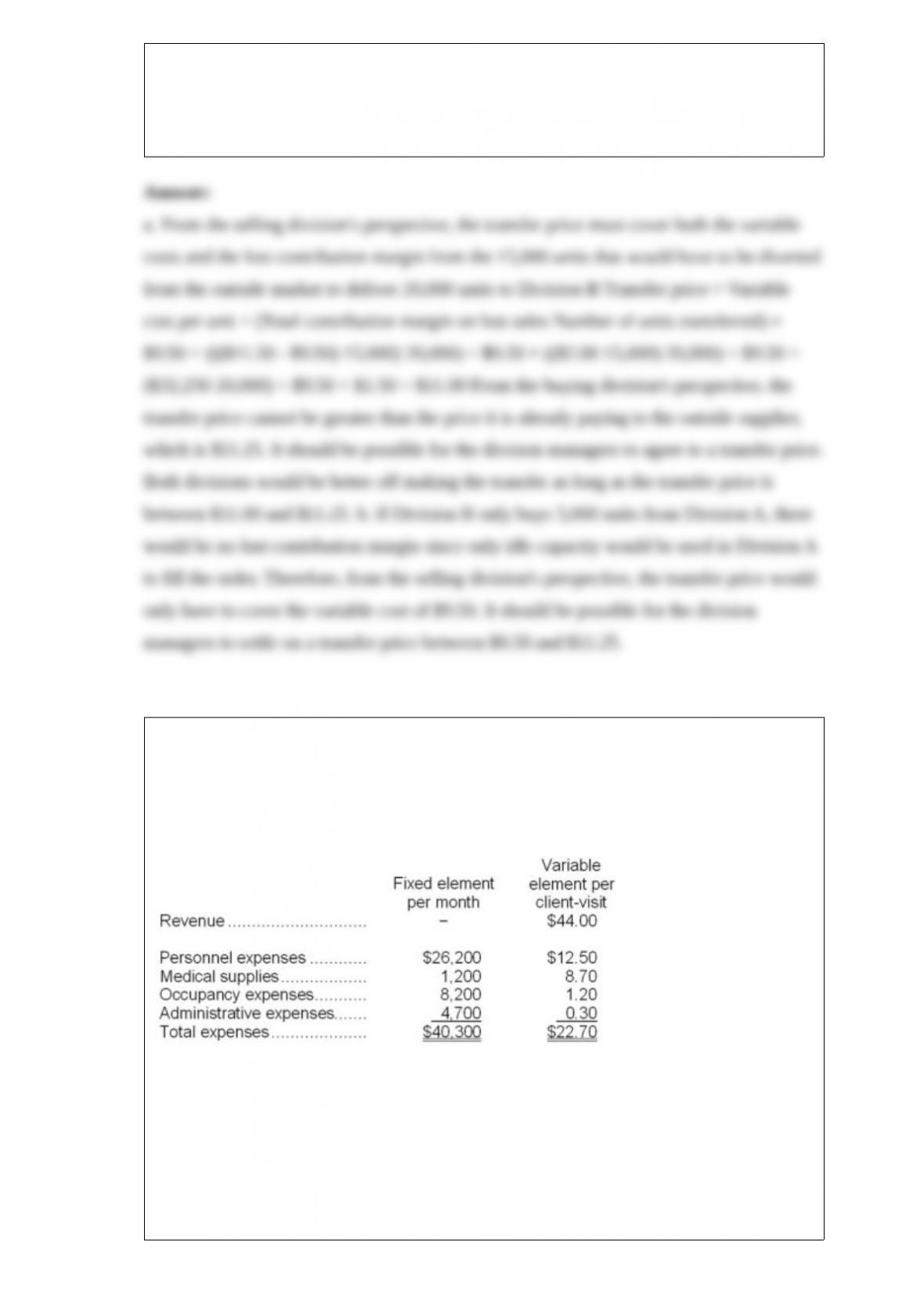

3) Ruetz Clinic uses client-visits as its measure of activity. During November, the clinic

budgeted for 2,500 client-visits, but its actual level of activity was 2,520 client-visits.

The clinic has provided the following data concerning the formulas to be used in its

budgeting:

The occupancy expenses in the flexible budget for November would be closest to:

A.$11,016

B.$11,224

C.$11,200

D.$11,193

4) What is the maximum contribution margin the company can earn per month?

A.$35,155

B.$46,404

C.$34,852

D.$35,460

5) How much of the unit product cost of $59.90 is relevant in the decision of whether to

make or buy the part?

A) $38.00 per unit

B) $59.90 per unit

C) $35.20 per unit

D) $22.70 per unit

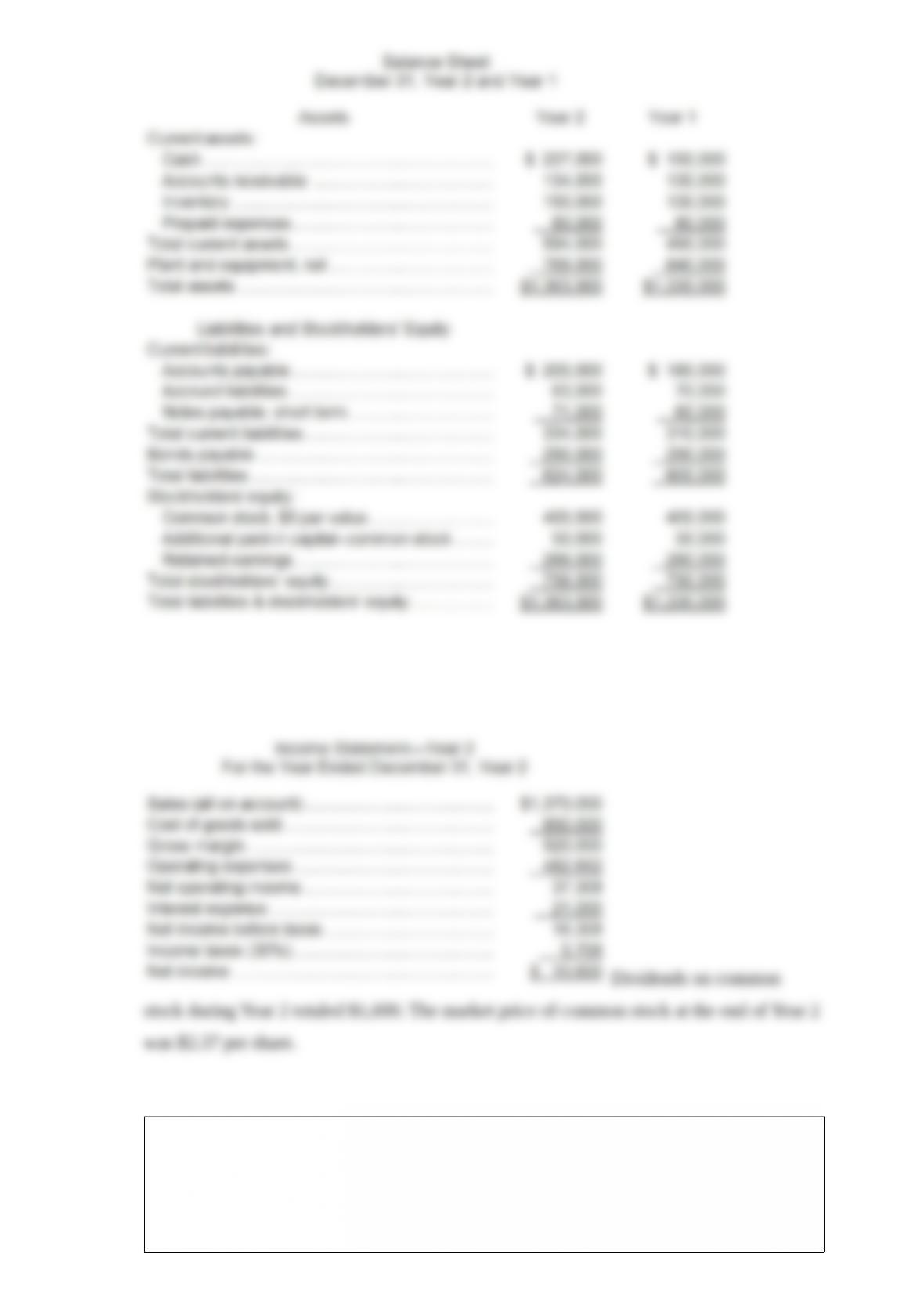

6) The company’s total asset turnover for Year 2 is closest to:

A.5.29

B.0.19

C.1.04

D.0.96

7) Contribution margin is the amount remaining after:

A.variable expenses have been deducted from sales revenue.

B.fixed expenses have been deducted from sales revenue.

C.fixed expenses have been deducted from variable expenses.

D.cost of goods sold has been deducted from sales revenues.

8) Lartey Corporation’s cost formula for its selling and administrative expense is

$22,200 per month plus $27 per unit. For the month of December, the company planned

for activity of 5,300 units, but the actual level of activity was 5,270 units. The actual

selling and administrative expense for the month was $168,150.

The spending variance for selling and administrative expense in December would be

closest to:

A.$3,660 F

B.$3,660 U

C.$2,850 F

D.$2,850 U

9) Maraby Corporation’s acid-test ratio at the end of Year 2 was closest to:

A.0.51

B.0.47

C.1.14

D.1.95

10) Palinkas Cane Products, Inc., processes sugar cane in batches. The company buys a

batch of sugar cane from farmers for $80 which is then crushed in the company’s plant

at a cost of $11. Two intermediate products, cane fiber and cane juice, emerge from the

crushing process. The cane fiber can be sold as is for $22 or processed further for $10 to

make the end product industrial fiber that is sold for $30. The cane juice can be sold as

is for $41 or processed further for $27 to make the end product molasses that is sold for

$101. How much more profit (loss) does the company make by processing one batch of

sugar cane into the end products industrial fiber and molasses?

A.$(128)

B.$3

C.$(28)

D.$31

11) The Breiden Corporation sells rodaks for $6.00 per unit. Fixed expenses total

$37,500 per month and variable expenses are $2.00 per unit. The number of units that

must be sold each month to realize a profit of 15% of sales is closest to:

A.9,375 units

B.11,029 units

C.12,097 units

D.9,740 units