The adjusting entry to accrue Interest Expense results in:

A. an increase in Interest Expense.

B. a decrease in Interest Expense.

C. a decrease in Cash.

D. a decrease in Interest Payable.

Income from operations is:

A. sometimes called the “bottom line.”

B. sometimes used in the ROI calculation.

C. usually used in the ROE calculation.

D. usually calculated after income tax expense.

If the net present value of the investment is $8,510, then:

A. the rate of return is less than the cost of capital.

B. the present value of the cash flows is greater than the required investment.

C. the cost of capital is higher than the internal rate of return.

D. the present value of the cash flows is $8,510 less than the investment.

Another term frequently used to describe stockholders’ equity is:

A. net assets.

B. gross assets.

C. paid-in capital.

D. capital stock.

Selling price per unit $100 Variable expenses per unit $40 Fixed expenses per month

$60,000

Operating income at a volume of 4,000 units per month is:

A. $240,000.

B. $200,000.

C. $180,000.

D. $120,000.

One inventory cost flow assumption will result in different cost of goods sold from

another inventory cost flow assumption only if:

A. inventory quantities change from the beginning to end of the year.

B. a new product is added to inventory during the year.

C. the cost of inventory items changes during the year.

D. price levels do not change during the year.

Which of the following is NOT an inventory account for a manufacturing company?

A. Cost of goods sold.

B. Work-in-process.

C. Raw materials.

D. Finished goods.

Which of the following is(are) true regarding cost flow assumptions?

A. Manufacturing firms are required to use FIFO.

B. Service firms are required to use LIFO.

C. If a firm uses FIFO for tax purposes, then FIFO must be used for financial reporting

purposes.

D. If a firm uses LIFO for tax purposes, then LIFO must be used for financial reporting

purposes.

E. All of the above.

How is performance evaluated for a cost center?

A. Actual costs incurred compared to budgeted costs.

B. Actual segment margin compared to budgeted segment margin.

C. Comparison of actual and budgeted return on investment (ROI) based on segment

margin and assets controlled by the segment.

D. None of the above.

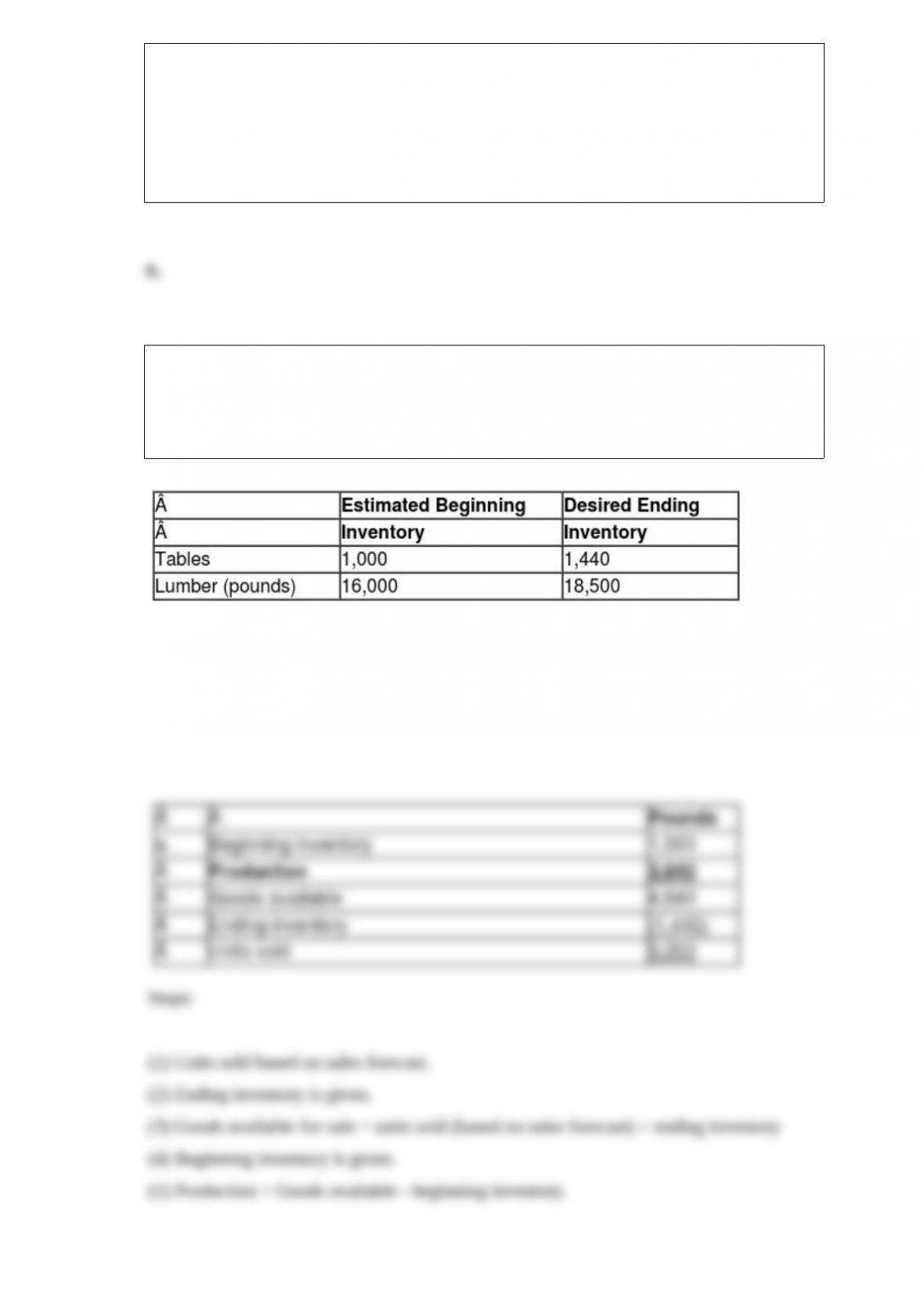

Pinedale, Inc. makes wooden tables. Each table requires 25 pounds of lumber to

produce. The sales forecast for May is 3,200 tables. Estimated beginning and desired

ending inventories for May are the following:

(a.) Calculate the number of tables to be produced in May.

(b.) Calculate the number of pounds of lumber to be purchased in May.

Prepare a bank reconciliation for Grace, Inc., as of January 31, from the following

information:

a.) The January 31 cash balance in the general ledger is $5,088.

(b.) The January 31 balance shown on the bank statement is $4,544.

(c.) Checks issued but not returned with the bank statement were No. 435 for $452 and

No. 448 for $182.

(d.) A deposit made on January 31 for $1,280 was included in the general ledger

balance but not in the bank statement balance.

(e.) Interest credited to the account during January but not recorded on the company’s

books amounted to $72.

(f.) A bank charge of $24 for printing new checks was made to the account during

January. Although the company was expecting a charge, the amount was not Known

until the bank statement arrived.

(g.) In the process of reviewing canceled checks, it was determined that a check issued

to a supplier in payment of an account payable of $139 was recorded as a $193 cash

disbursement.

Which of the following items would be reported on the Statement of Cost of Goods

Manufactured?

A. cost of goods sold.

B. beginning finished goods inventory.

C. ending work in process inventory.

D. contribution margin.

Cost accounting is concerned with:

A. accumulation and determination of product, process or service cost.

B. income measurement and inventory valuation.

C. generally accepted accounting principles.

D. all of the above.

Revenue may be recognized:

A. from the sale of a company’s own common stock.

B. if a company trades inventory at its usual selling price for newspaper advertising.

C. if management believes the market value of land held for future development has

increased during the year.

D. in 2016 from the sale of subscriptions of a magazine to be published in 2017.

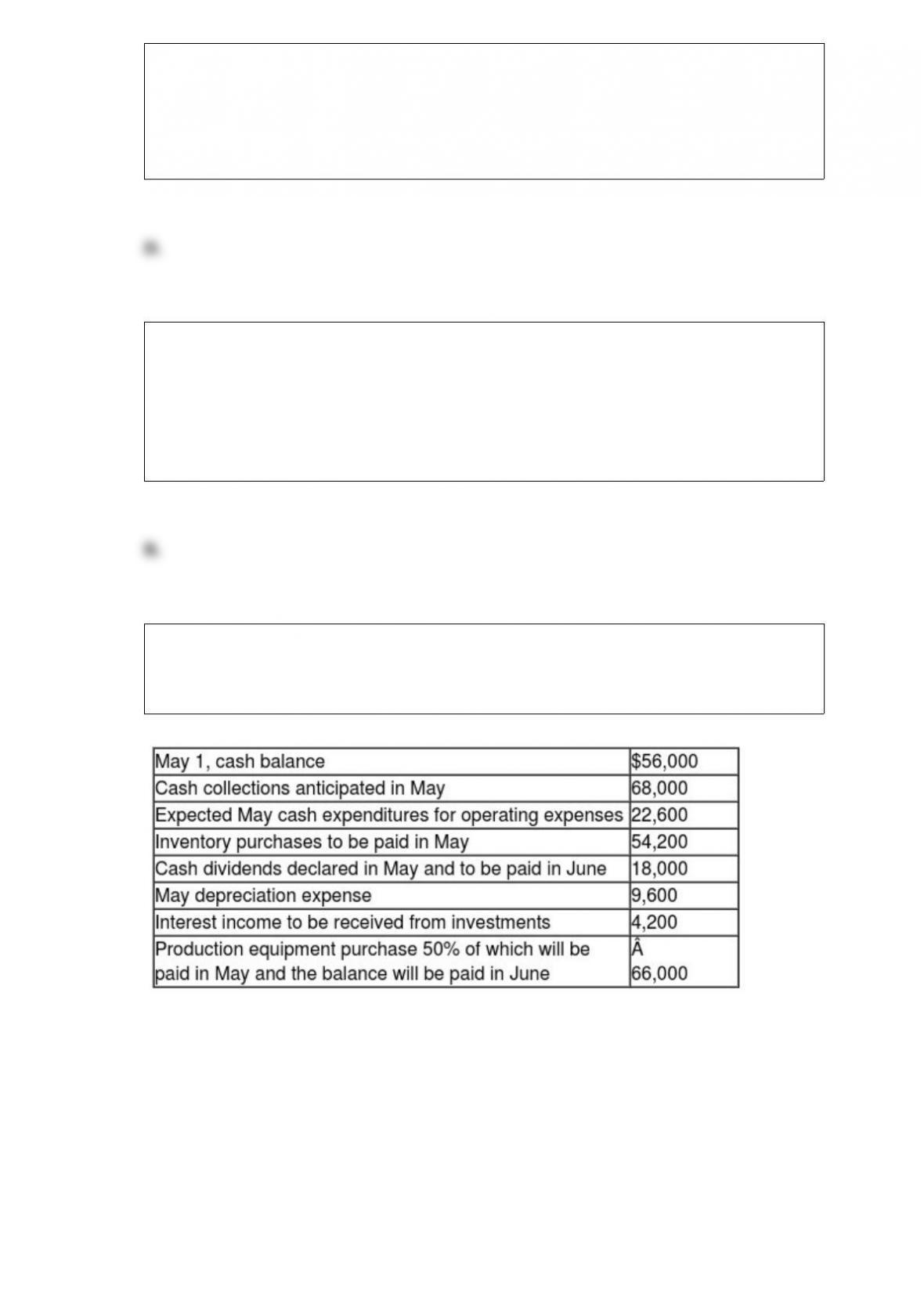

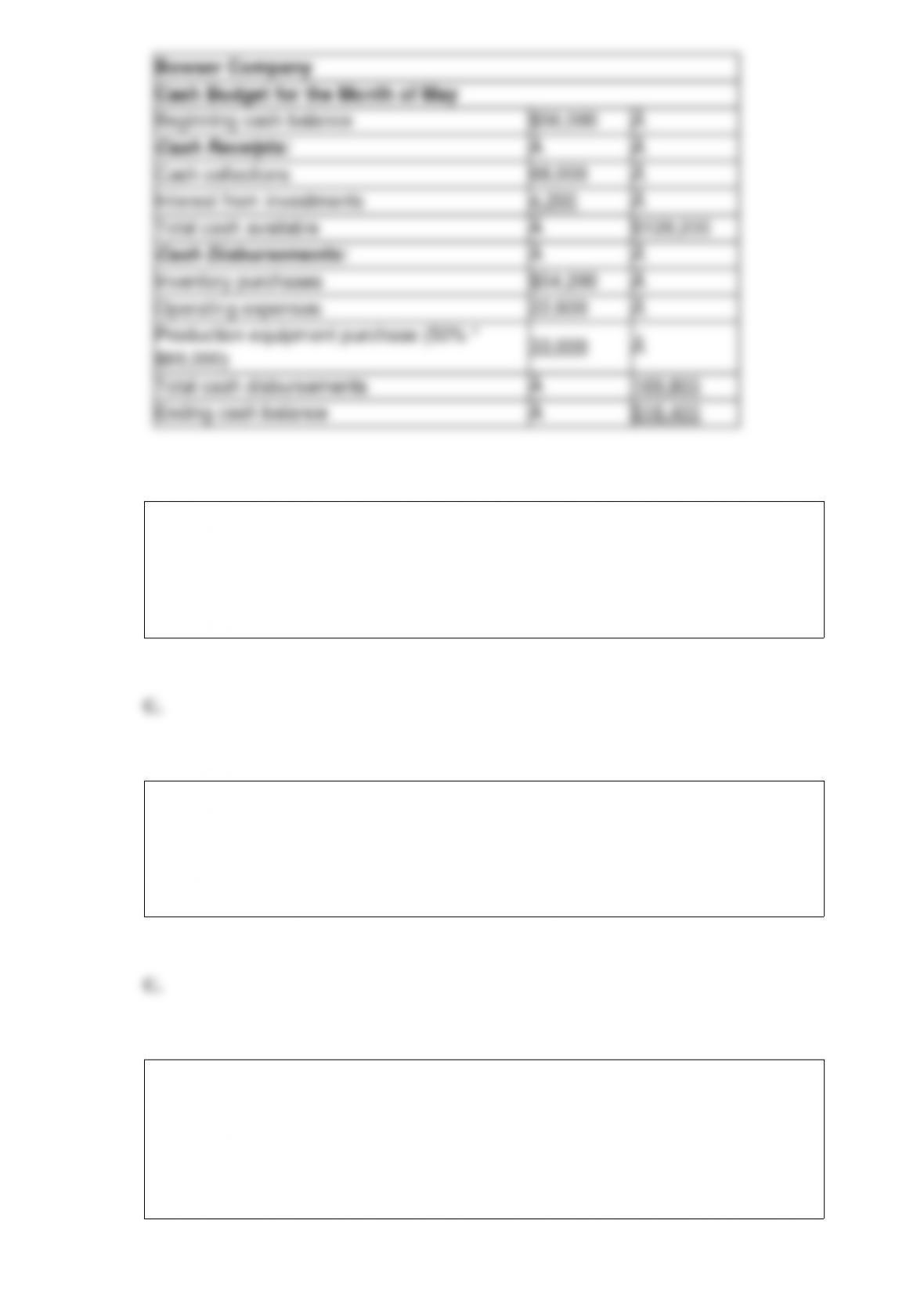

The following information for the month of May has been provided for Bowser

Company:

(a.) Prepare a cash budget for May.

A current ratio of 6.0 is usually an indication that the firm:

A. has a low degree of liquidity.

B. has a reasonable degree of liquidity.

C. has not made the most productive use of its assets.

D. has made the most productive use of its assets.

A cost is considered relevant if:

A. it is positive.

B. it is sunk.

C. it makes a difference.

D. if it can’t be changed.

The principal reason for converting a customer’s account receivable to a note receivable

is:

A. the note receivable earns interest and the account receivable does not.

B. the receivable is less likely to have to be written off as uncollectible.

C. working capital is immediately increased.

D. the customer is more likely to continue purchasing the company’s products.

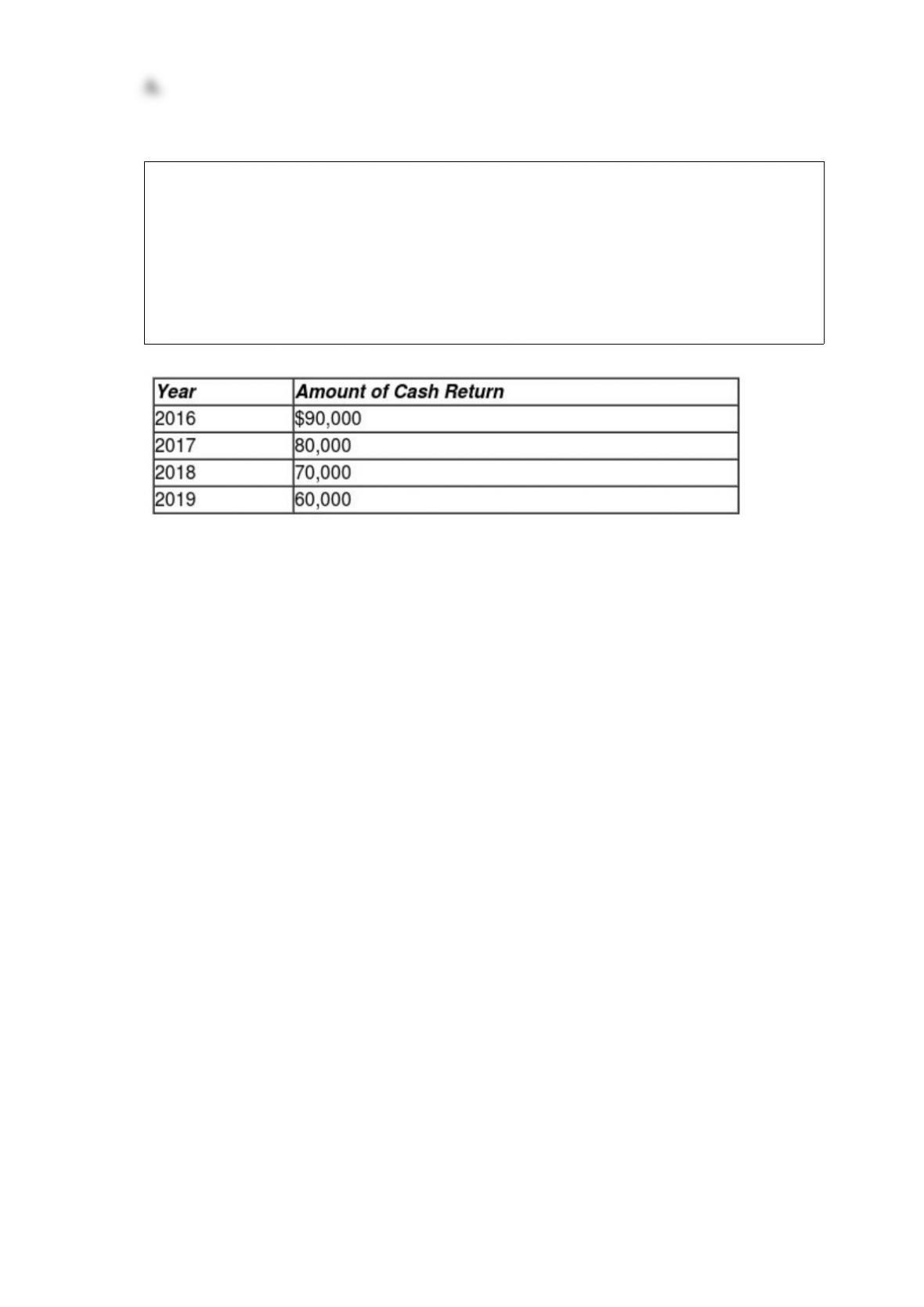

The following data have been collected by capital budgeting analysts at Halda, Inc.

concerning an investment in an expansion of the company’s product line. Analysts

estimate that an investment of $210,000 will be required to initiate the project at the

beginning of 2016. Estimated cash returns from the new product line are summarized in

the following table; assume that the returns will be received in lump sum at the end of

each year.

The new product line will also require an investment in working capital of $30,000; this

investment will become available for other purposes at the end of the project. Salvage

value of machinery and equipment at the end of the product line’s life is expected to be

$20,000. The cost of capital used in Hilda, Inc.’s capital budgeting analysis is 10%.

(a.) Calculate the net present value of the proposed investment. Ignore income taxes, and

round all answers to the nearest $1.

(b.) Calculate the present value ratio of the investment.

(c.) What will the internal rate of return on this investment be relative to the cost of

capital? Explain your answer.

(d.) Calculate the payback period of the investment. .

Which of the following qualitative factors favors the buy option in the make or buy

decision?

A. production scheduling.

B. utilization of idle capacity.

C. ability to control quality.

D. technical expertise of supplier.

When a firm purchases its own shares as treasury stock:

A. total stockholders’ equity is decreased.

B. total stockholders’ equity is increased.

C. retained earnings is decreased.

D. paid-in capital is decreased.

The authoritative financial accounting standards-setting body in the United States is

presently the:

A. Securities and Exchange Commission (SEC)

B. International Accounting Standards Board (IASB)

C. Public Company Accounting Oversights Board (PCAOB)

D. Financial Accounting Standards Board (FASB)

E. Accounting Principles Board (APB)

A firm has used LIFO for several years during which costs have trended higher. The

effect on 2017 net income using LIFO, relative to FIFO, will be:

A. net income for 2017 will be greater under LIFO than FIFO.

B. net income for 2017 will be less under LIFO than FIFO.

C. net income for 2017 will be the same under LIFO as under FIFO.

D. can’t tell from the information given.

A principal difference between operational budgeting and capital budgeting is the time

frame of the budget. Because of this difference, capital budgeting:

A. is an activity that involves only the financial staff.

B. is done on a rolling budget period basis.

C. focuses on the present value of cash flows from investments.

D. is concerned with a long-term net income forecast.

Management accounting is:

A. a highly technical subject that people in personnel or engineering should not be

expected to understand.

B. performed by individuals who seldom work with people in other functional areas of

the organization.

C. the principal activity involved in determining the goals and objectives of the entity.

D. an activity that gets involved with virtually all of the other functional areas of the

organization.

The cost formula for monthly customer order processing cost has been established as

$100 + $0.15 per order. It is expected that 5,600 orders will be processed in May and

6,400 in June. Total order processing costs for May and June combined will be

estimated to be:

A. $940.

B. $1,060.

C. $2,000.

D. $2,500.

A debit balance in the manufacturing overhead account at the end of the period

indicates that:

A. manufacturing overhead is overapplied.

B. manufacturing overhead is underapplied.

C. manufacturing overhead has been accurately applied.

D. None of the above.

On July 1, 2016, $8 million face amount of 6%, 10-year bonds were issued. The bonds

pay interest on an annual basis on June 30 each year. The market interest rates were

slightly lower than 6% when the bonds were sold.

Required:

(a.) How much interest will be paid annually on these bonds?

(b.) Were the bonds issued at a premium or discount? Explain.

(c.) Will the annual interest expense on these bonds be more than, equal to, or less than

the amount of interest paid each year? Explain your answer.

(a.) Annual interest payment = $8 million * 6% = $480,000

(b.) The bonds were issued at a premium because market interest rates were less than

the stated rate when the bonds were issued. The lower the discount rate (i.e., the market

interest rate), the higher the present value of cash flows for interest payments and

principal (i.e., the higher the bond’s selling price).

Bad debt expense is recognized in the same accounting period as the revenue that is

related to the receivable because:

A. the accounts receivable asset should be stated at original cost.

B. the exact amount of the losses from bad debts is known.

C. revenues should be stated at realizable value.

D. all costs incurred in the current period should be subtracted from current period

revenues.

Which of the following is not an important factor to consider when preparing a sales

forecast?

A. the state of the economy.

B. seasonal demand variations.

C. a change in the management team.

D. competitors’ actions.

When a cost formula is used to describe a mixed (semi-variable) cost behavior pattern,

total costs are expected to increase and per unit variable costs are expected to:

A. increase as the level of activity increases.

B. decrease as the level of activity decreases.

C. decrease as the level of activity increases.

D. remain constant as the level of activity increases.

An accounts receivable results from the sale of:

A. property, plant, and equipment for cash.

B. goods and services to customers on account.

C. goods and services to customers for cash.

D. the firm’s common stock.

When costs are rising over time:

A. LIFO results in higher profits that FIFO.

B. Cost of goods sold using the weighted average method will be greater than LIFO

cost of goods sold.

C. ending inventory balances will be greater under LIFO.

D. FIFO results in higher profits than LIFO.

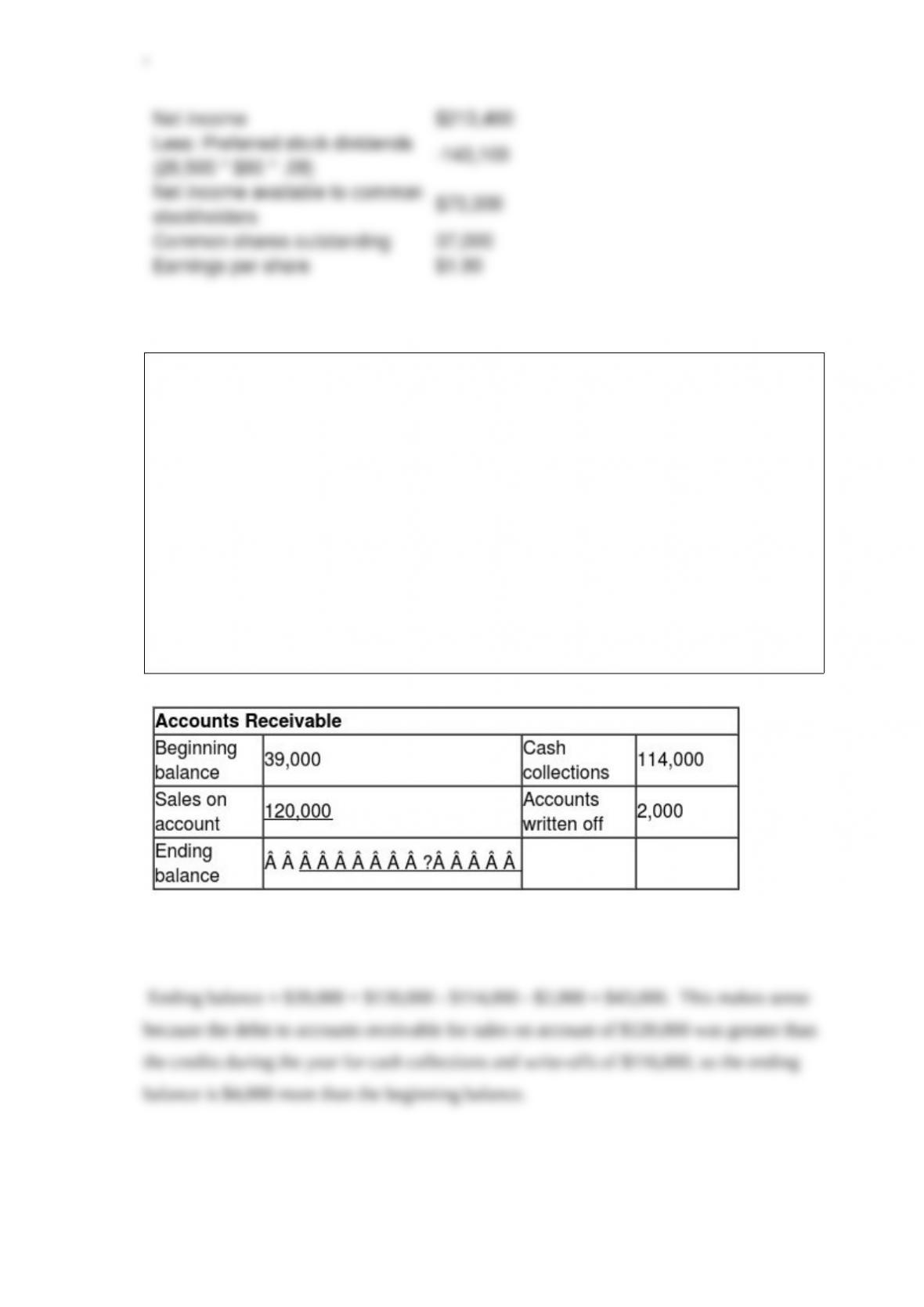

Norman’s Cabinet, Inc., had net income of $213,400 for its fiscal year ended October

31, 2017. During the year, the company had outstanding 26,500 shares of 9%, $60 par

value preferred stock, and 37,000 shares of common stock. Calculate the basic earnings

per share of common stock for the 2017 fiscal year.

At the beginning of the year, accounts receivable were $39,000 and the allowance for

bad debts was $2,400. During the year, sales (all on account) were $120,000, cash

collections were $114,000, bad debts expense totaled $1,700, and $2,000 of accounts

receivable were written off as bad debts.

Required:

Calculate the balances at the end of the year for the Accounts Receivable and

Allowance for Bad Debts accounts. (Hint: Use T-accounts to analyze each of these

accounts, plug in the amounts that you know, and solve for the ending balances.)

The Allowance for Bad Debts account had a balance of $20,400 at the beginning of the

year and $24,500 at the end of the year. During the year (including the year-end

adjustment), bad debts expense of $33,600 was recognized.

Required:

Calculate the total amount of past-due accounts receivable that were written off as

uncollectible during the year. (Hint: Make a T-account for the Allowance for Bad Debts

account, plug in the amounts that you know, and solve for the missing amount.)

Firm Z had net assets at the end of the year of $320,000.The only transactions affecting

stockholders’ equity during the year were net income of $51,000 and dividends of

$11,000.

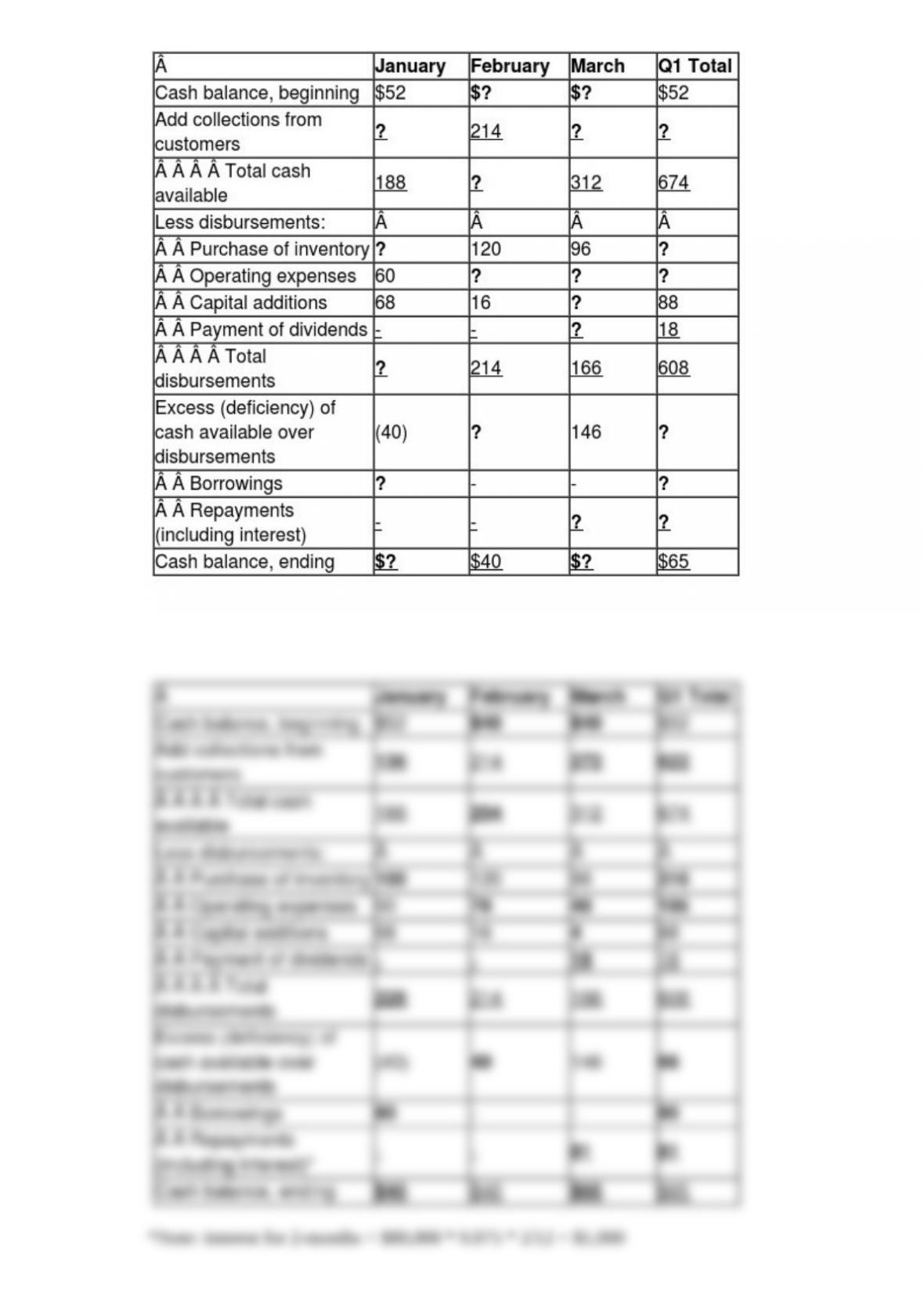

The monthly cash budgets for the first quarter of 2016 are shown below ($000 omitted)

for XYZ Company. A minimum cash balance of $40,000 is required. A line of credit has

been established with ABC’s bank at a 7.5% interest rate. Calculate the missing

amounts: