A disclosure note is required for all material loss contingencies for which the

probability of loss is reasonably possible.

The FASB is currently the public-sector organization responsible for setting accounting

standards in the United States.

If a company chooses the option to report its bonds at fair value, then it reports changes

in fair value in its income statement unless the changes are attributable to changes in

credit risk.

The receivables turnover ratio provides a way for an analyst to assess the effectiveness

of a company in managing its investment in receivables.

Error corrections require restatement of all the affected prior year financial statements

reported in comparative financial statements.

Under IFRS, firms typically use the cost recovery method if they conclude that the

percentage-of-completion method is not appropriate to account for a long-term

construction contract.

All investments in debt securities whose fair values are not readily determinable are

carried at historical cost.

Under IFRS, an overdraft in a cash account at one bank can be offset against a positive

balance in the account at another bank for purposes of reporting cash on the company’s

balance sheet.

The fair value of the asset, debt, or equity securities given in a noncash acquisition

should determine the value of the consideration received.

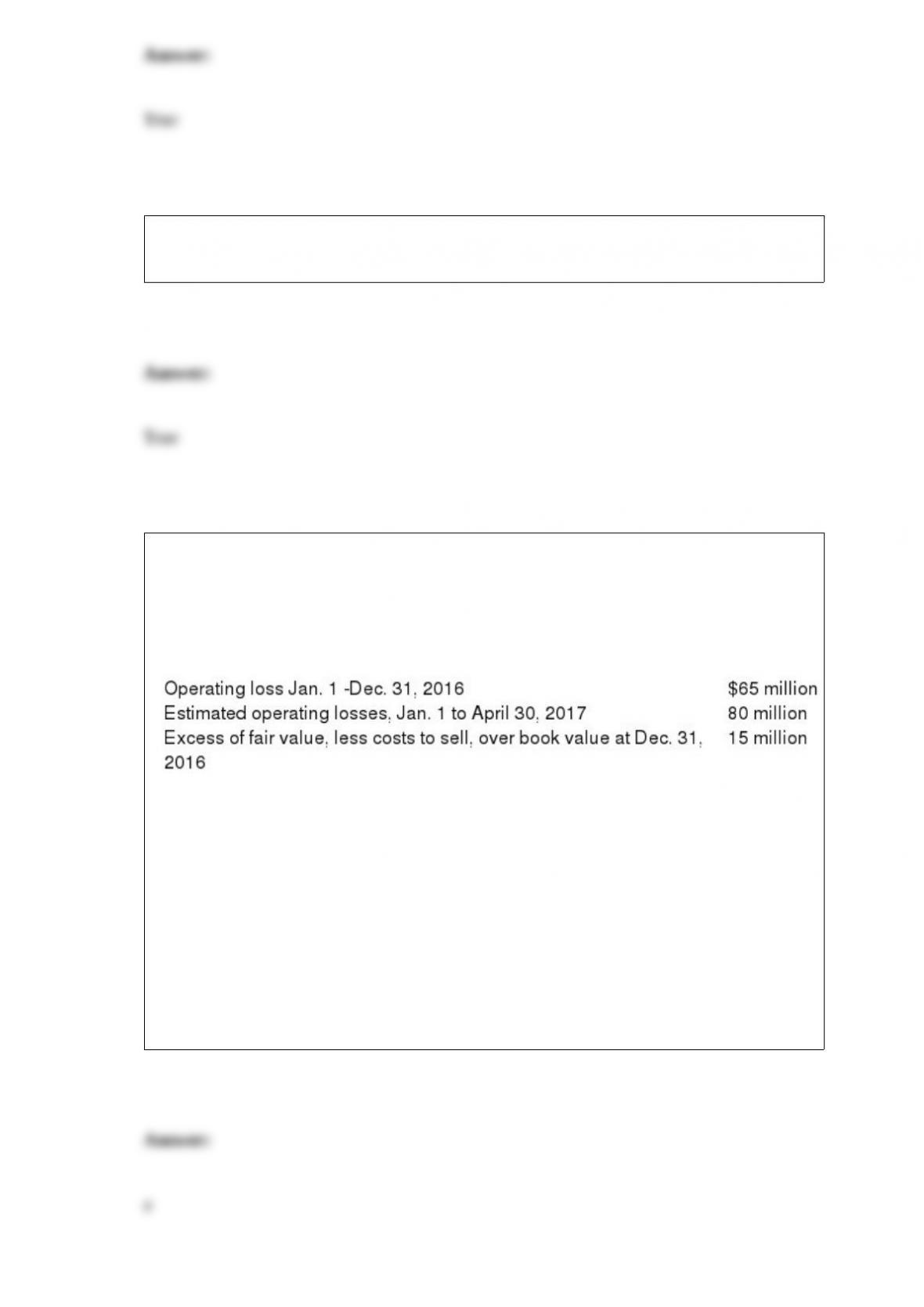

On November 1, 2016, Jamison Inc. adopted a plan to discontinue its barge division,

which qualifies as a separate component of the business according to GAAP regarding

discontinued operations. The disposal of the division was expected to be concluded by

April 30, 2017. On December 31, 2016, the company’s year-end, the following

information relative to the discontinued division was accumulated:

In its income statement for the year ended December 31, 2016, Jamison would report a

before-tax loss on discontinued operations of:

a. $ 65 million.

b. $ 50 million.

c. $130 million.

d. $145 million.

Mary Parker Co. invested $15,000 in ABC Corporation and received capital stock in

exchange. Mary Parker Co.’s journal entry to record this transaction would include a:

a. Debit to investments.

b. Credit to retained earnings.

c. Credit to capital stock.

d. Debit to expense.

The final paragraph of the audit report:

a. Provides the auditors’ opinion on the fairness of the financial statements.

b. Provides the auditor’s opinion on the effectiveness of internal control.

c. Describes the scope of the audit.

d. States management’s responsibility for the financial statements.

In which investment category are fair values and subsequent growth of an investee not

relevant for reporting?

a. Securities reported under the equity method.

b. Trading securities.

c. Held-to-maturity securities.

d. Securities available for sale.

In reconciling net income to taxable income, interest earned on municipal bonds is:

a. Ignored.

b. A temporary difference.

c. A reversing difference.

d. A permanent difference.

If a change is made from straight-line to SYD depreciation, one should record the

effects by a journal entry including:

a. A credit to deferred tax liability.

b. A credit to accumulated depreciation.

c. A debit to depreciation expense.

d. No journal entry is required.

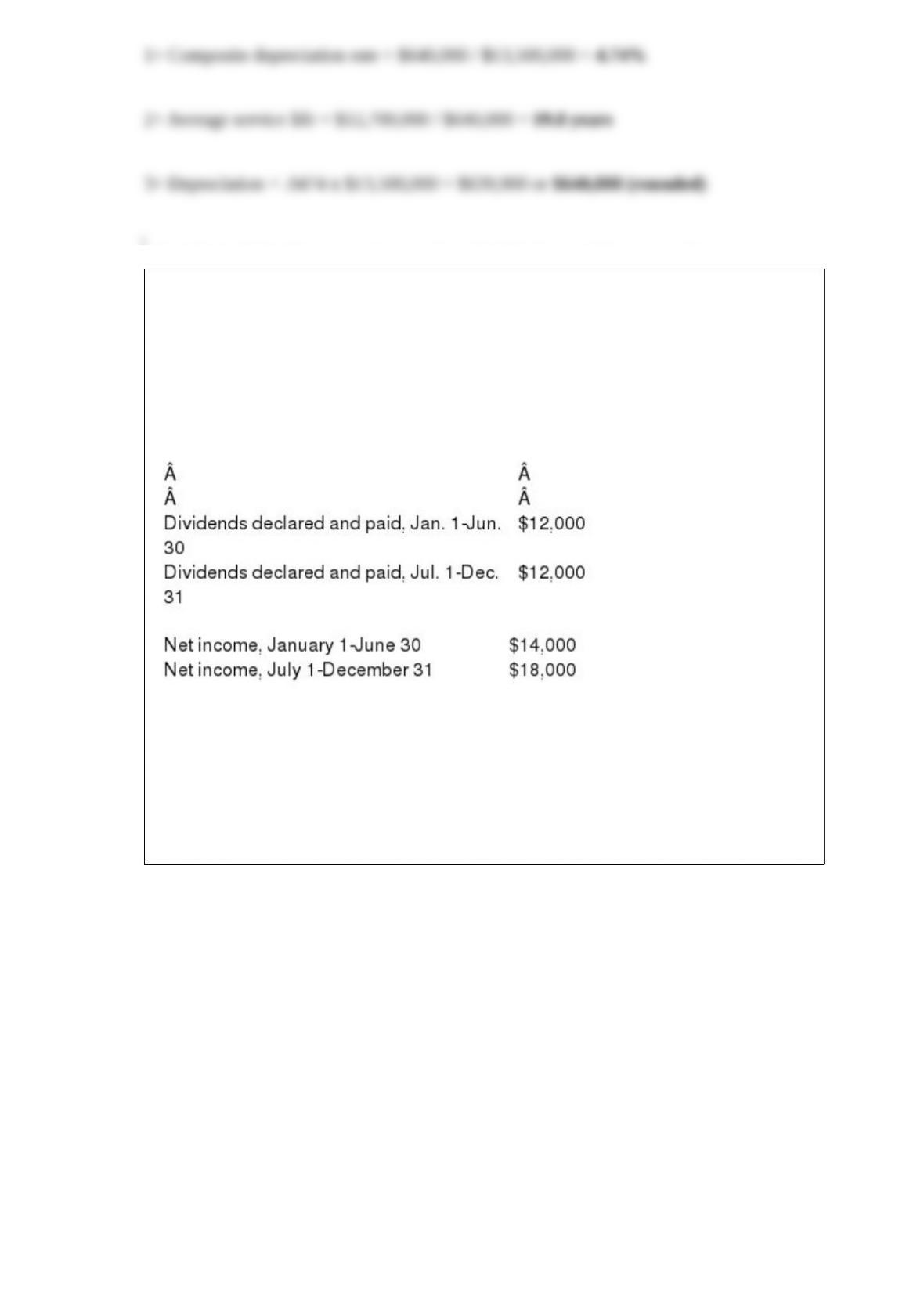

When dividends are declared in one fiscal year and paid in the next fiscal year, the

liability for the dividend should be recorded as of the:

a. Date the dividend is declared.

b. Last day of the fiscal year.

c. Date of record.

d. Date of payment.

On January 1, 2016, Tiny Tim Industries had outstanding $1,000,000 of 12% bonds

with a book amount of $966,130. The indenture specified a call price of $981,000. The

bonds were issued previously at a price to yield 14%. Tiny Tim called the bonds (retired

them) on July 1, 2016. What is the amount of the loss on early extinguishment?

a. $0.

b. $6,932.

c. $7,241.

d. $7,629

Granite Enterprises acquired a patent from Southern Research Corporation on January

1, 2016, for $4 million. The patent will be used for 5 years, even though its legal life is

20 years. Rocky Corporation has made a commitment to purchase the patent from

Granite for $200,000 at the end of five years. Compute Granite’s patent amortization for

2016, assuming the straight-line method is used.

a. $380,000.

b. $400,000.

c. $760,000.

d. $800,000.

The compensation associated with restricted stock units (RSUs) under a stock award

plan is the number of shares represented by the RSUs multiplied by:

A. The market price of a share of similar fixed income securities.

B. The market price of an unrestricted share of the same stock.

C. The book value of an unrestricted share of the same stock.

D. The book value of a share of similar stock.

What are the key provisions of the Public Company Accounting Reform and Investor

Protection (Sarbanes-Oxley) Act of 2002?

Listed below are five terms followed by a list of phrases that describe or characterize

each of the terms. Match each phrase with the number for the correct term.

Concept 1 Office Products sells office electronics that carry a 60-day manufacturer’s

warranty. At the time of purchase, customers are offered the opportunity to also buy a

1-year or 2-year extended warranty for an additional charge.

Required:

1> Does the sale of the extended warranty represent a loss contingency?

2> Provide journal entries for the extended warranty sales and revenue recognition.

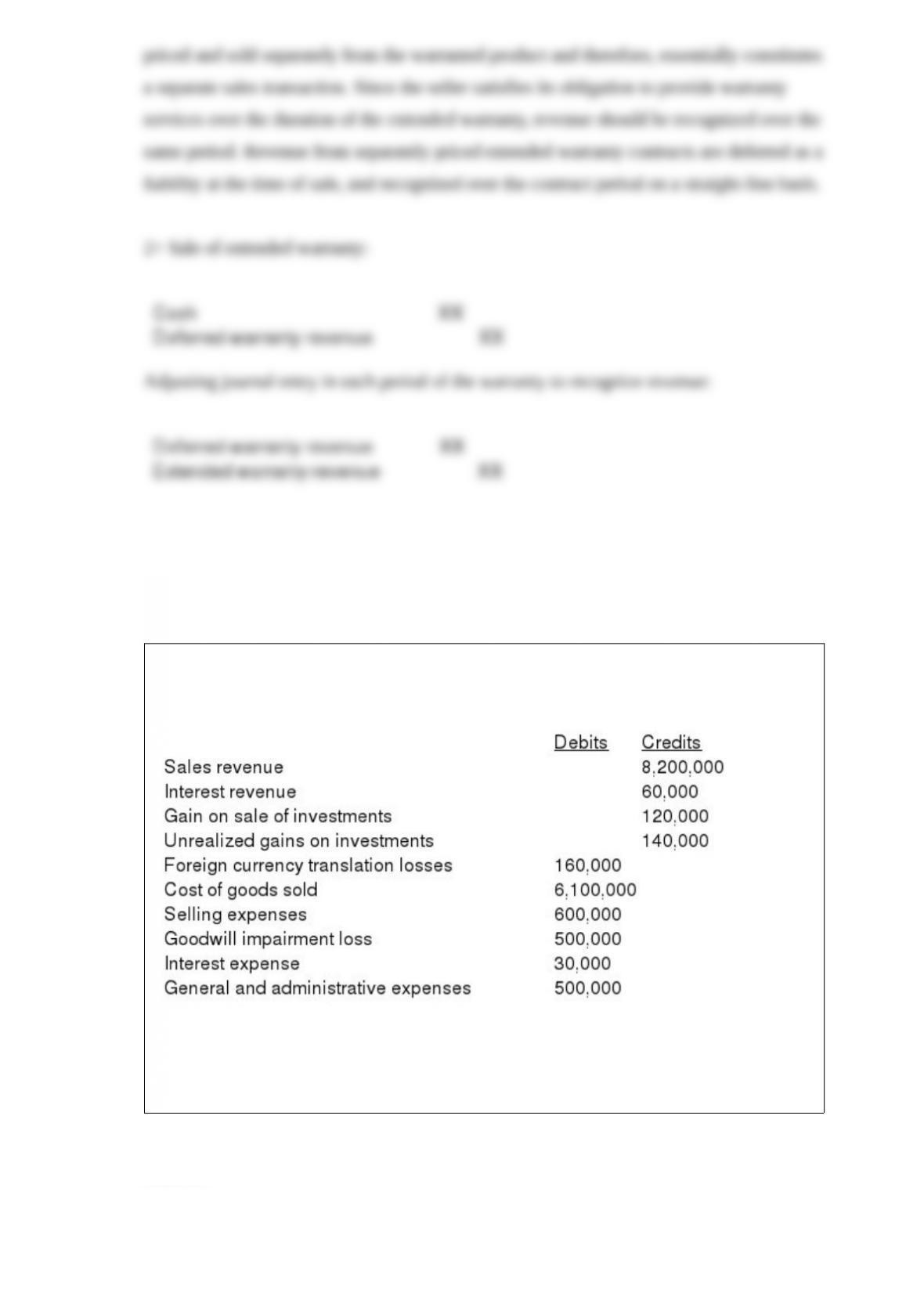

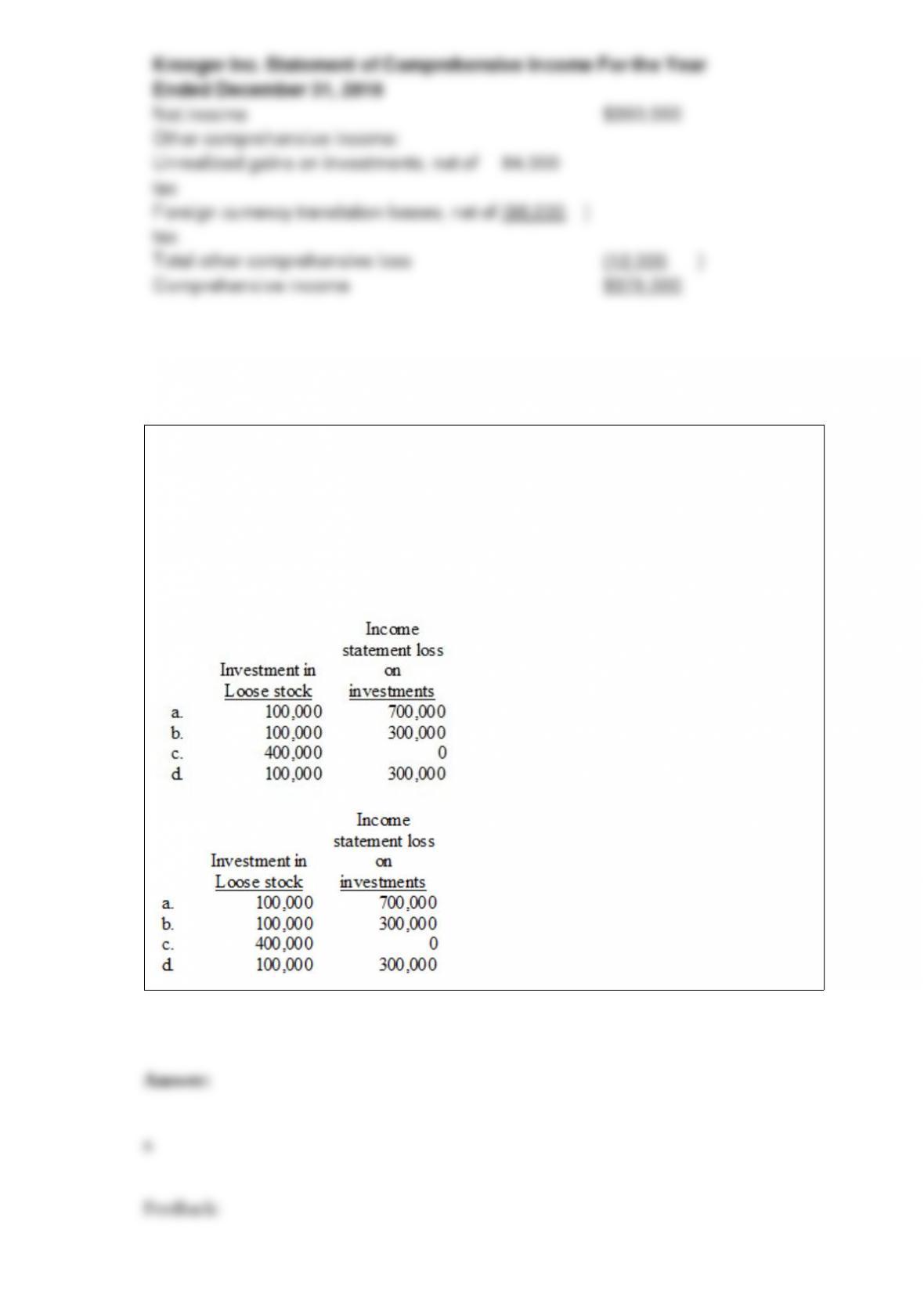

The trial balance of Kroeger Inc. included the following accounts as of December 31,

2016:

Kroeger had 300,000 shares of stock outstanding throughout the year. Income tax

expense has not yet been accrued. The effective tax rate is 40%.

Required: Prepare a 2016 separate statement of comprehensive income for Kroeger

Inc.

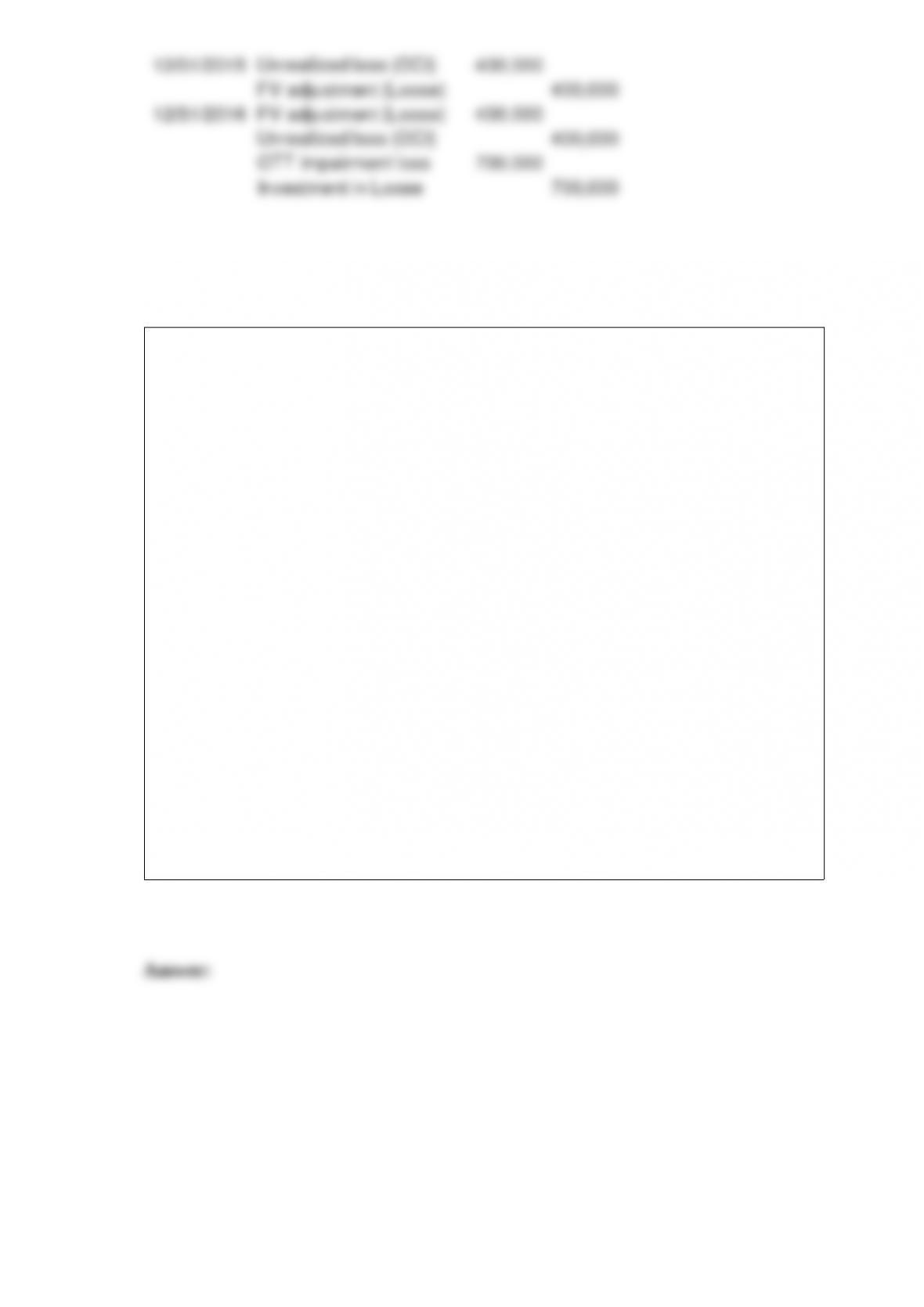

Dicker Furriers purchased 1,000 shares of Loose Corporation stock on January 10,

2015, for $800 per share and classified the investment as securities available for sale.

Loose’s market value was $400 per share on December 31, 2015, and the decline in

value was viewed as temporary. As of December 31, 2016, Dicker still owned the Loose

stock whose market value had declined to $100 per share. The decline is due to a reason

that’s judged to be other than temporary. Dicker’s December 31, 2016, balance sheet and

the 2016 income statement would show the following:

On January 1, 2016, Cobbler Corporation awarded restricted stock units (RSUs)

representing 30 million of its $1 par common shares to key personnel, subject to

forfeiture if employment is terminated within three years. After the recipients of the

RSUs satisfy the vesting requirement, the company will distribute the shares. On the

grant date, the shares had a market price of $3 per share.

Required:

(1) Determine the total compensation cost pertaining to the RSUs.

(2) Prepare the appropriate journal entry to record the award of RSUs on January 1,

2016.

(3) Prepare the appropriate journal entry to record compensation expense on December

31, 2016.

(4) Prepare the appropriate journal entry to record compensation expense on December

31, 2017.

(5) Prepare the appropriate journal entry to record compensation expense on December

31, 2018.

(6) Prepare the appropriate journal entry to record the lifting of restrictions on the RSUs

and issuing shares at December 31, 2018.

Rodeo Corporation amended its defined benefit pension plan on January 31, 2016, to

increase retirement benefits earned with each service year. The actuary estimated the

prior service cost to be $216,000. Rodeo’s 80 present employees are expected to retire

at the rate of about 10 each year at the end of each of the next eight years beginning on

December 31, 2016.

Required:

Using the service method, calculate the amount of prior service cost to be amortized to

pension expense in each of the next eight years.

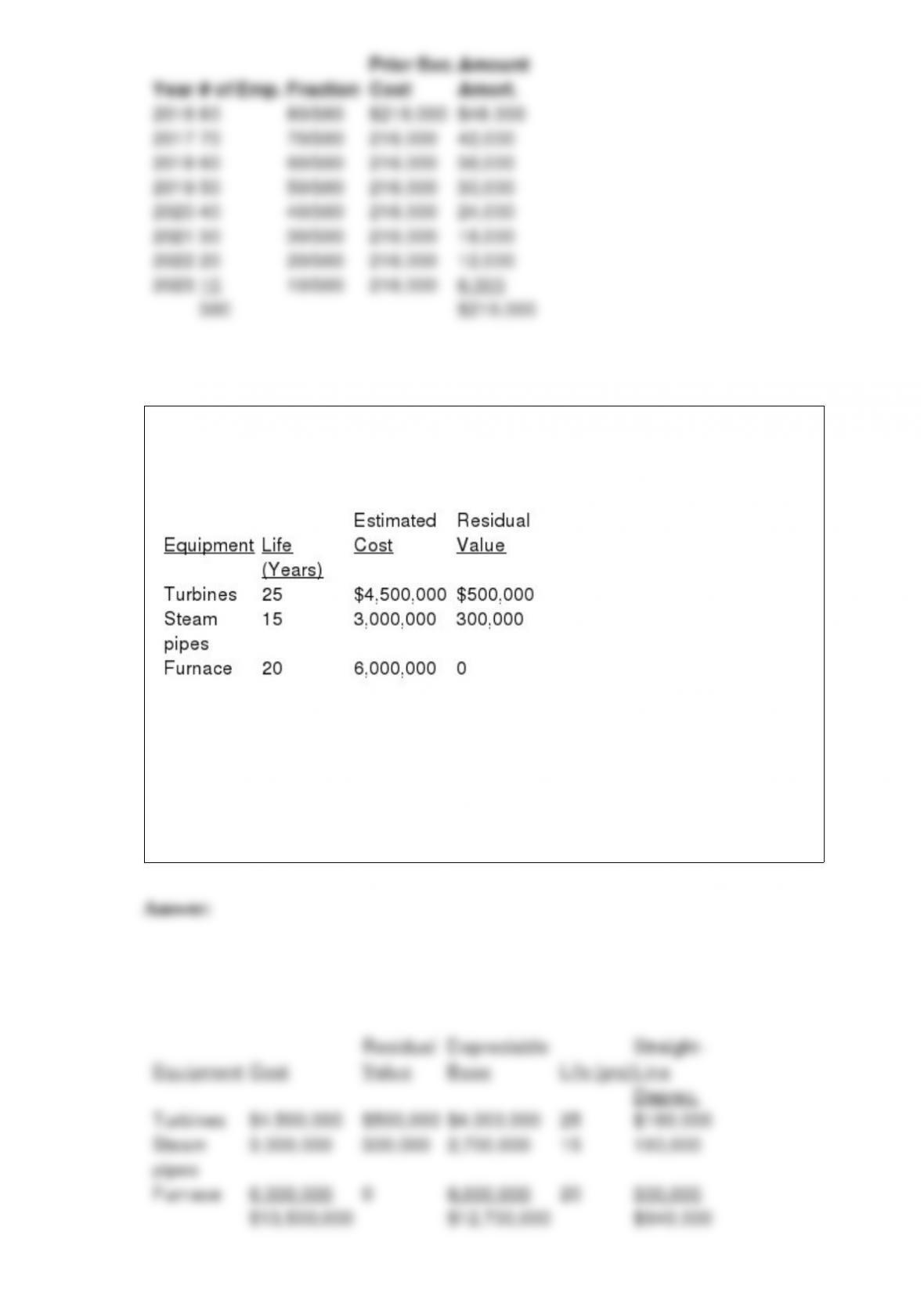

Nature Power Company uses the composite method and straight-line depreciation for its

power plant equipment. Its Apple River plant, which began generating electricity

January 1, 2016, had the following equipment:

Required:

1> Compute the composite depreciation rate.

2> Compute the average service life.

3> Compute 2016 depreciation.

On July 1, 2016, Clearwater Inc. purchased 6,000 shares of the outstanding common

stock of Mountain Corporation at a cost of $140,000. Mountain had 30,000 shares of

outstanding common stock. The total book value and total fair value of Mountain’s

individual net assets on July 1, 2016, are both $700,000. The total fair value of the

30,000 shares of Mountain’s common stock on December 31, 2016, is $760,000. Both

companies have a January through December fiscal year. The following data pertains to

Mountain Corporation during 2016:

Required:

1) Prepare the necessary entries for 2016 under the equity method (other than for the

purchase.

2) Prepare any necessary entries for 2016 (other than for the purchase) that would be

required if the securities are classified as available for sale.

•

In the following questions, inventory errors are noted for 2016. Assume that the errors

are not discovered until 2017, and that the company uses a periodic inventory system.

Indicate the effect of the error, if any, on the accounts noted in the columns, using the

following code:

U = Understated; O = Overstated; NE = No effect