1) During a “flight to quality”

A) the spread between Treasury bonds and Baa bonds increases

B) the spread between Treasury bonds and Baa bonds decreases

C) the spread between Treasury bonds and Baa bonds is not affected

D) the change in the spread between Treasury bonds and Baa bonds cannot be predicted

2) When a city enters into a capital lease for a fixed asset for the general government,

A) government-wide statements will report an Encumbrance for the leased asset.

B) government-wide statements will report the liability, Capital Lease Obligation.

C) governmental fund statements will report a fixed asset.

D) governmental fund statements will report a liability, Capital Lease Obligation.

3) Panini Corporation owns 85% of the outstanding voting stock of Strathmore

Company and Malone Corporation owns the remaining 15% of Strathmore’s voting

stock. On the consolidated financial statements of Panini Corporation and Strathmore,

Malone is

A) an affiliate

B) a noncontrolling interest

C) an equity investee

D) a related party

4) A single creditor

A) can never file a petition for bankruptcy

B) with a $12,300 or more secured claim may file a petition for bankruptcy

C) with a $12,300 or more unsecured claim may file a petition for bankruptcy, if there

are fewer than 12 unsecured creditors

D) with a $12,300 or more unsecured claim may file a petition for bankruptcy if there

are more than 12 unsecured creditors

5) Under the modified accrual basis of accounting, revenues are recognized in the

period

A) when the relevant service is done

B) when they are collected

C) when the paying entity is billed

D) when they become both measurable and available

6) Internal Service Funds differ from Enterprise Funds because Internal Service Funds

A) are a proprietary fund

B) are intended to show a profit

C) charge for their services

D) provide goods and services primarily to other government agencies

7) When a capital lease is used to lease fixed assets for the general government, the

governmental fund acquiring the fixed assets debits ________ at the ________.

A) expenditures; future value of the minimum lease payments

B) fixed assets; future value of the minimum lease payments

C) expenditures, present value of the minimum lease payments

D) fixed assets; present value of the minimum lease payments

8) The material sale of inventory items by a parent company to an affiliated company

A) enters the consolidated revenue computation only if the transfer was the result of

arm’s length bargaining

B) affects consolidated net income under a periodic inventory system but not under a

perpetual inventory system

C) does not result in consolidated income until the merchandise is sold to outside

parties

D) does not require a working paper adjustment if the merchandise was transferred at

cost

9) Durer Inc. acquired Sea Corporation in a business combination and Sea Corp went

out of existence. Sea Corp developed a patent listed as an asset on Sea Corp’s books at

the patent office filing cost. In recording the combination,

A) fair value is not assigned to the patent because the research and development costs

have been expensed by Sea Corp

B) Sea Corp’s prior expenses to develop the patent are recorded as an asset by Durer at

purchase

C) the patent is recorded as an asset at fair market value

D) the patent’s market value increases goodwill

10) In partnership liquidations, what are safe payments?

A) The amounts of distributions that can be made to the partners, after all creditors have

been paid in full

B) The amounts of distributions that can be made to the partners with assurance that

such amounts will not have to be returned to the partnership

C) The amounts of distributions that can be made to the partners, after all non-cash

assets have been adjusted to fair market value

D) The amounts of distributions that can be made to the partners during the liquidation

based on the partner’s contributed capital return

11) Push-down accounting

A) requires a subsidiary to use the same accounting principles as its parent company

B) is required when the parent company uses the equity method to account for its

investment in a subsidiary

C) is required when the parent company uses the cost method to account for its

investment in a subsidiary

D) requires the subsidiary to record the subsidiary’s assets and liabilities at fair value at

the acquisition date

12) A direct quote for the U.S. dollar is given at $1.45 per 1 foreign currency unit (fcu).

The respective indirect quote for the U.S. dollar would be reported as

A) 1.45 fcu = $1.00

B) 1.45 fcu = $.6897

C) .6897 fcu = $1.00

D) 1.00 fcu = $1.45

13) Plenty Corporation issued six thousand, $1,000 par, 6% bonds on January 1, 2010,

at par. Interest is paid on January 1 and July 1 of each year; the bonds mature on

January 1, 2015 . On January 2, 2012, Scrawn Corporation, a 75%-owned subsidiary of

Plenty, purchased 3,000 of the bonds on the open market at 102.50 . Plenty’s separate

net income for 2012 included the annual interest expense for all 3,000 bonds. Scrawn’s

separate net income for 2012 was $400,000, which included the bond interest received

on July 1 as well as the accrual of bond interest revenue earned on December 31 . Both

companies use straight-line amortization of bond discounts/premiums.

If the bonds were originally issued at 106, and 80% of them were purchased by Scrawn

on January 2, 2013 at 98, the gain or (loss) from the intercompany purchase was

A) $(384,000)

B) $(211,200)

C) $ 211,200

D) $ 384,000

14) Match the following definitions to the appropriate government accounting terms

(numbered below).

A.Legally separate organization for which primary government is financially

accountable

B.The use of governmental fund working capital

C.Appropriation for a specific time period

D.Governmental and Proprietary fund revenues and expenses presented using full

accrual accounting

E.Approved or authorized expenditures

F.Revenues recognized when available to meet current obligations

G.Self-balancing set of accounts

H.Each state government and each general-purpose local government

I.The responsibility to demonstrate compliance with public decisions with regard to the

use of financial resources

J.Governmental and Internal Service Funds assets and liabilities presented together

_____1>Modified Accrual Basis

_____2>Fund

_____3>Primary Government

_____4>Appropriation

_____5>Statement of Net Assets

_____6>Fiscal Accountability

_____7>Allotment

_____8>Component Unit

_____9>Statement of Activities

_____10>Expenditures

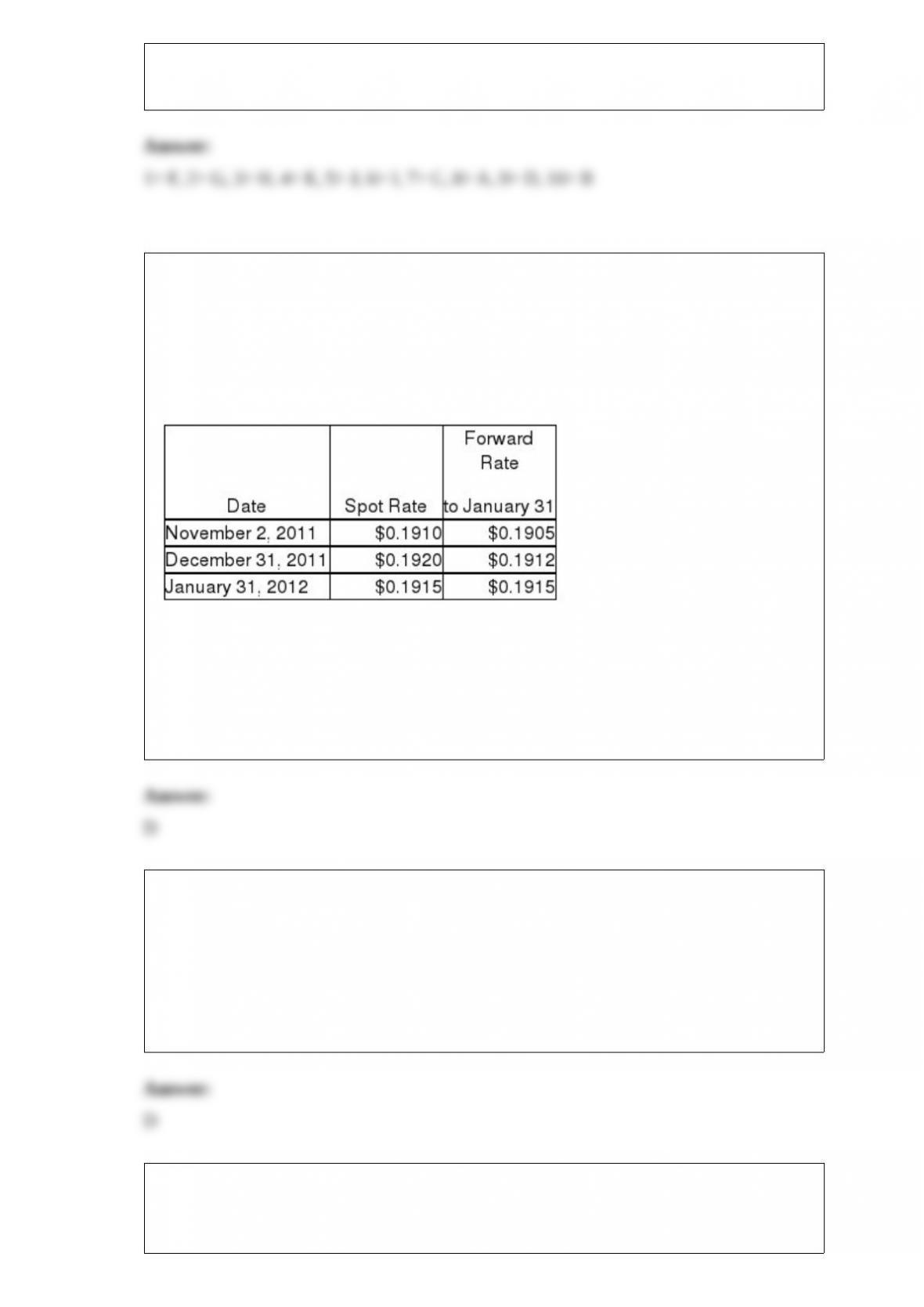

15) On November 2, 2011, Bellamy Corporation sells product to their Danish customer.

At the same time, Bellamy signed a forward contract to sell 200,000 Danish krone in

ninety days to hedge the account receivable at $0.1905, the 90-day forward rate. The

receivable is expected to be collected in ninety days. Assume the forward contract will

be settled net and this is a fair value hedge. The related exchange rates are shown

below:

Assuming a present value factor of 1 for simplicity, what is the fair value of this

forward contract on December 31?

A) $160 asset

B) $160 liability

C) $140 asset

D) $140 liability

16) When the billing for a U.S. company’s sale to a company in a foreign country is

denominated in U.S. dollars, ________ is required when preparing journal entries for

the sale.

A) translation to a foreign currency

B) conversion to a foreign currency

C) translation to U.S. dollars

D) no translation

17) On January 1, 2011, Pinnead Incorporated paid $300,000 for an 80% interest in

Shalle Company. At that time, Shalle’s total book value was $300,000. Patents were

undervalued in the amount of $10,000. Patents had a 5-year remaining useful life, and

any remaining excess value was attributed to goodwill. The income statements for the

year ended December 31, 2011 of Pinnead and Shalle are summarized below:

PinneadShalle

Sales$800,000$300,000

Income from Shalle 78,400

Cost of sales (100,000)(100,000)

Depreciation (70,000)(30,000)

Other Expenses (130,000)(70,000)

Net Income $578,400$100,000

Requirements:

1>Calculate the goodwill that will appear in the consolidated balance sheet of Pinnead

and Subsidiary at December 31, 2011 .

2>Calculate consolidated net income for 2011 .

3>Calculate the noncontrolling interest share for 2011 .

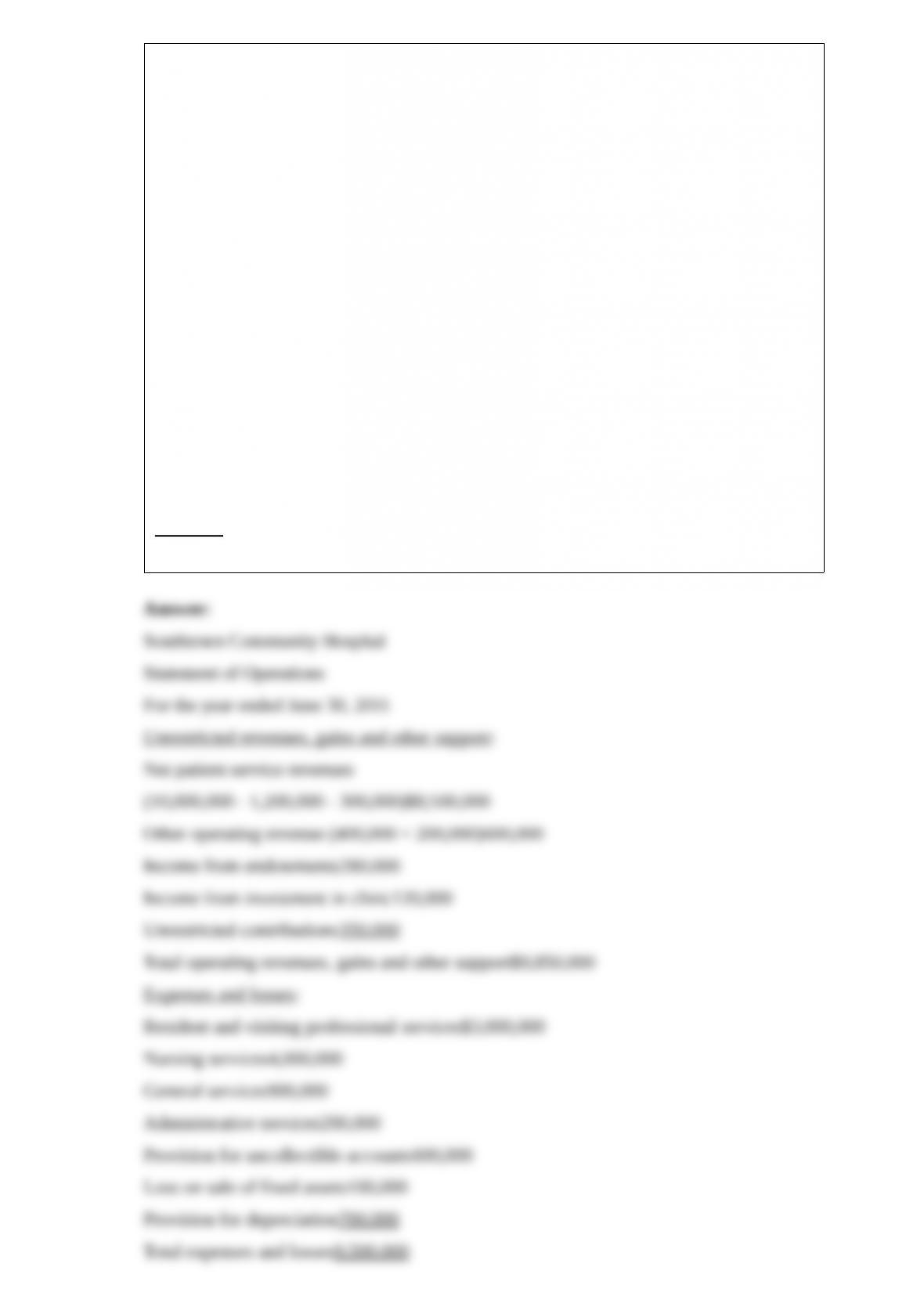

18) Southtown Community Hospital (SCH) shows the following balances on its trial

balance at June 30, 2011, their fiscal year end. SCH is a not-for-profit,

nongovernmental hospital. $260,000 cash was spent on equipment from donations

restricted for that purpose.

Debits:

Administrative services expense200,000

Contractual allowances1,200,000

Depreciation expense700,000

Employee discounts300,000

General services expense900,000

Loss on sale of fixed assets100,000

Nursing services expense4,000,000

Resident and visiting professional services expense3,000,000

Provision for bad debts600,000

Credits:

Income from investment in clinic120,000

Patient service revenues10,000,000

Pharmacy400,000

Cafeteria services200,000

Unrestricted contributions350,000

Unrestricted income from endowment funds280,000

Restricted donations for equipment purchases500,000

Required:

Prepare a statement of operations for Southtown Community Hospital at June 30, 2011 .

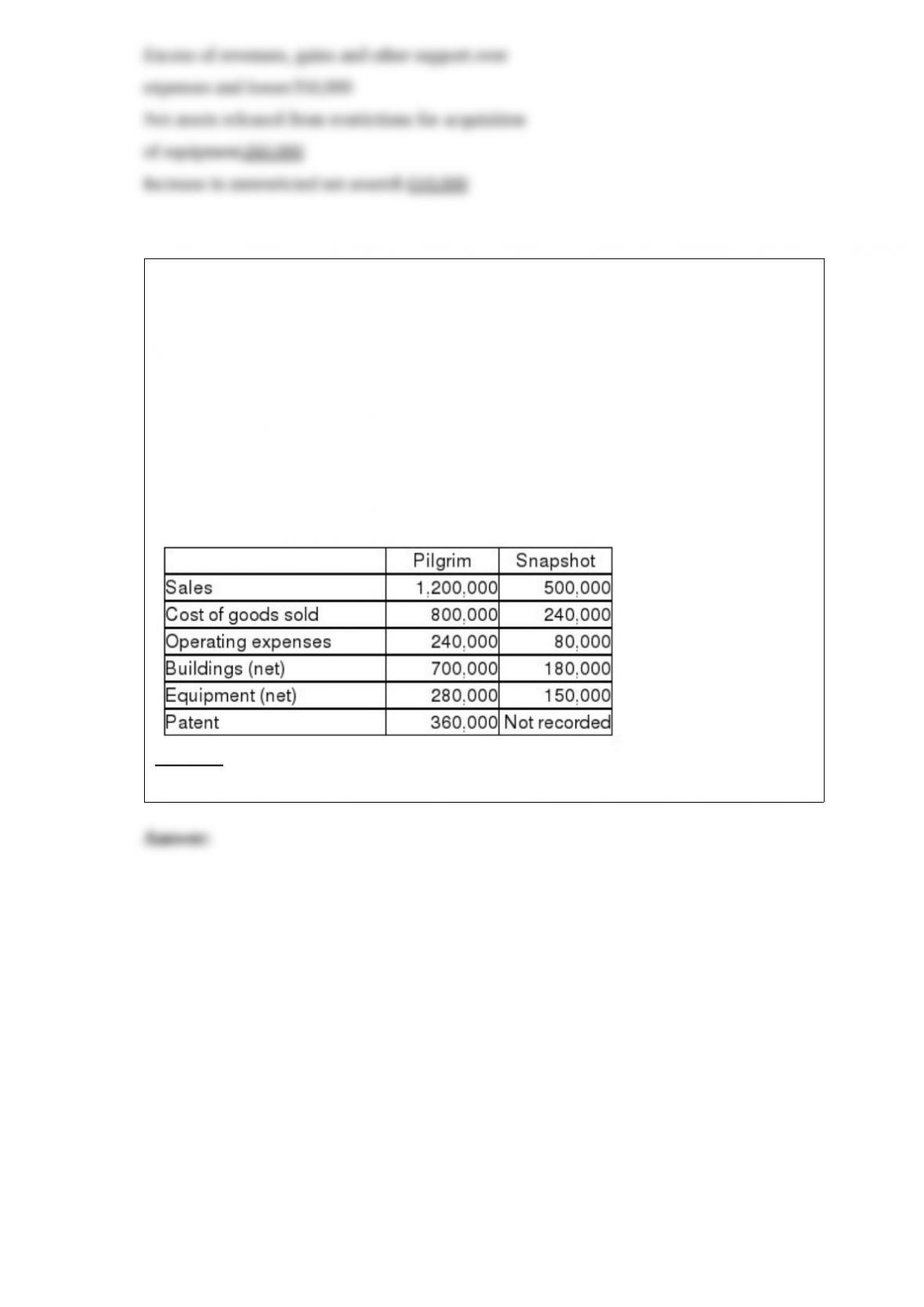

19) On January 1, 2011, Pilgrim Imaging purchased 90% of the outstanding common

stock of Snapshot Productions for $585,000 cash. The remaining 10% of Snapshot had

an assessed fair value of $65,000 at that time. Snapshot had equipment that was

undervalued on their books by $50,000, and an unrecorded patent with a fair value of

$15,000. The equipment had five years remaining to its useful life, and the patent had

10 years remaining to its useful life.

On January 1, 2012, Pilgrim sold Snapshot a building for $100,000 that had originally

cost $140,000. The book value was $60,000 at the date of transfer, and had a five-year

remaining life at the date of transfer. Straight-line depreciation is used with no salvage

value. Several line items from the companies’ separate December 31, 2012 trial

balances are shown below.

Required: Determine consolidated balances for each of the accounts listed as of

December 31, 2012 .

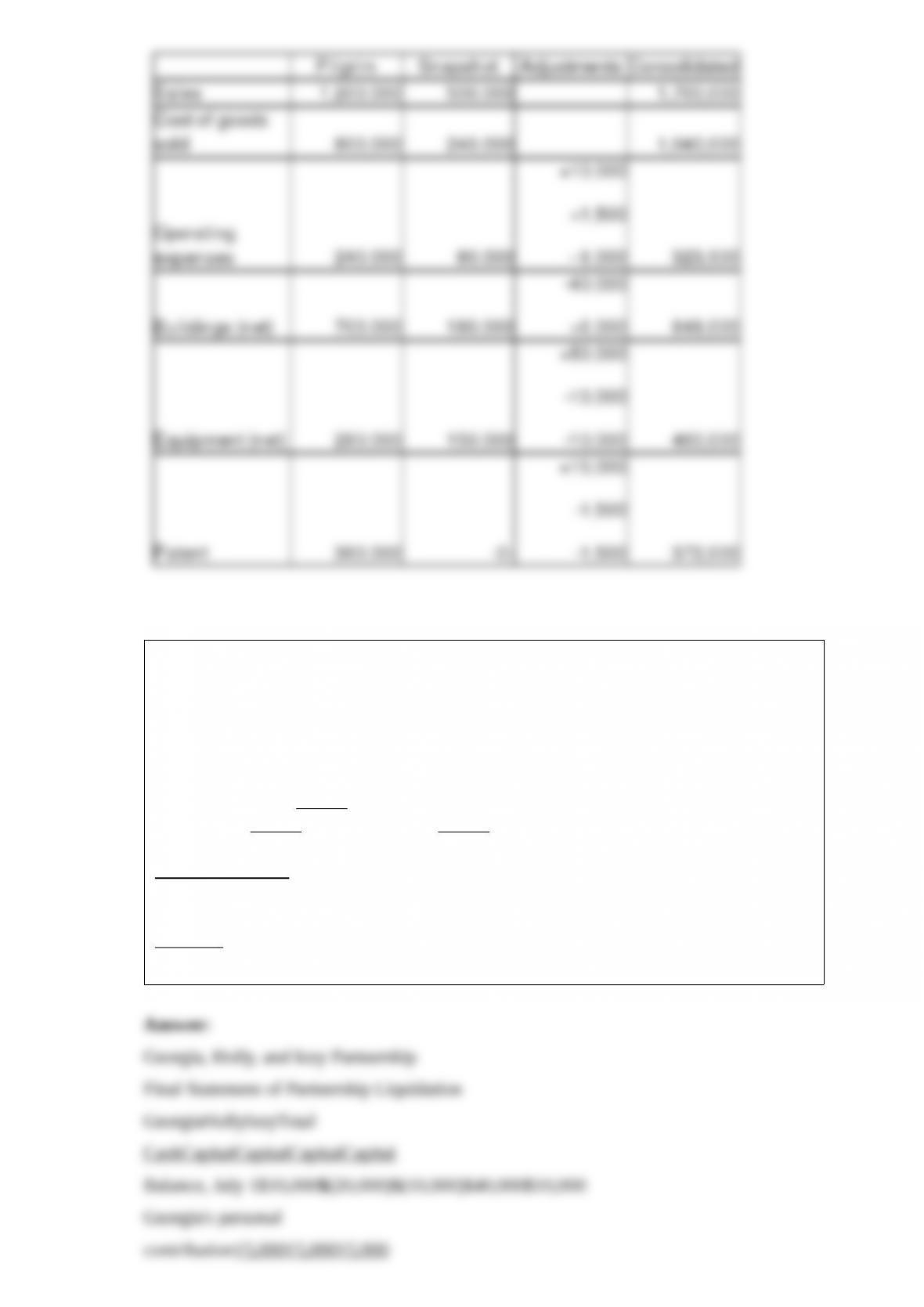

20) The partnership of Georgia, Holly, and Izzy was dissolved, and by July 1, 2011, all

assets had been converted into cash and all partnership liabilities were paid. The

partnership balance sheet on July 1, 2011 (with partner residual profit and loss sharing

percentages) was as follows:

Cash$10,000Georgia, capital (40%)$(20,000)

Holly, capital (30%)(10,000)

Izzy, capital (30%)40,000

Total assets$10,000Total liab./equity$10,000

The value of the partners’ personal assets and liabilities on July 1, 2011 were as follows:

GeorgiaHollyIzzy

Personal assets$45,000$30,000$25,000

Personal liabilities30,00020,00010,000

Required:

Prepare the final statement of partnership liquidation.

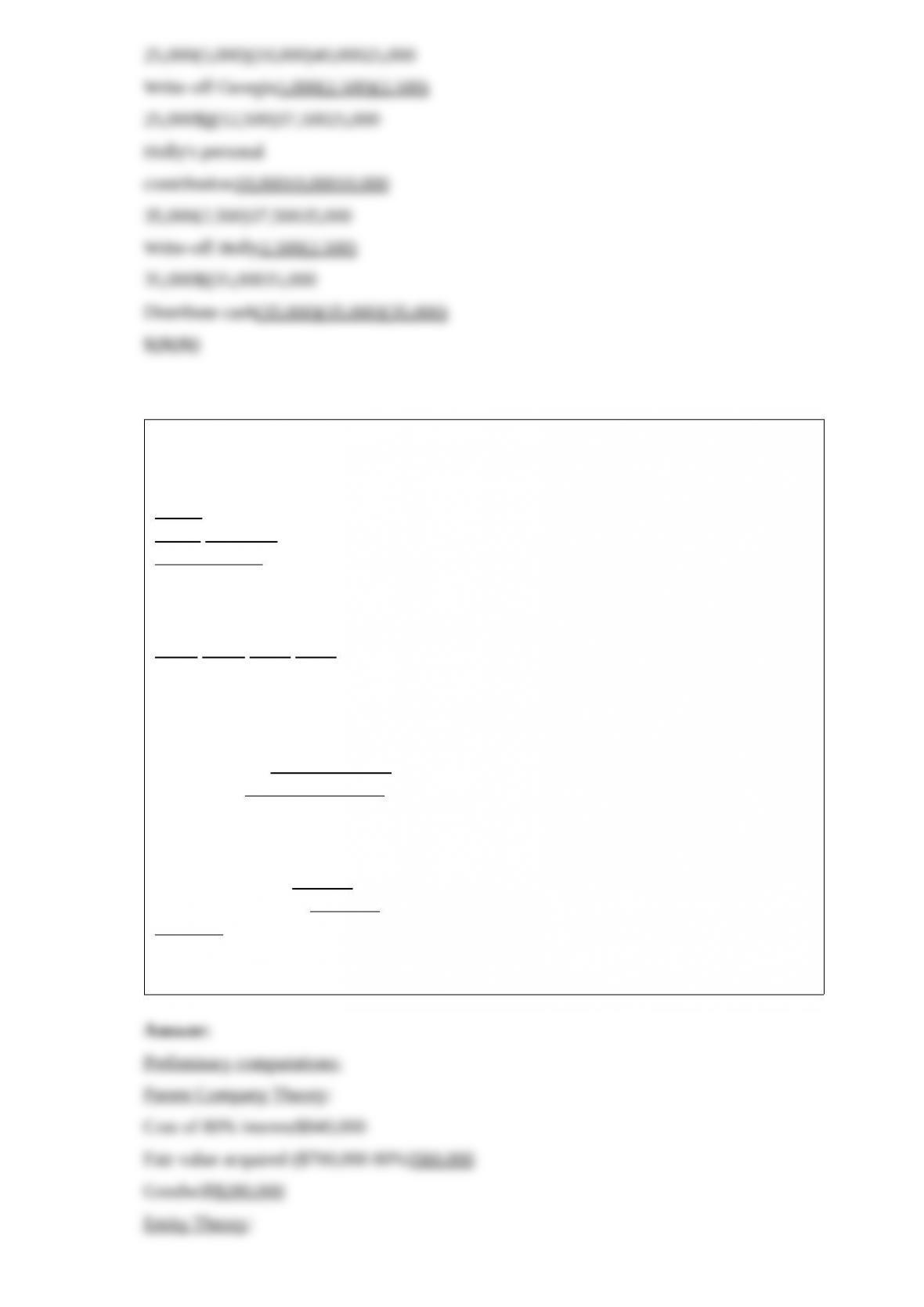

21) Partridge Corporation purchased an 80% interest in Sandy Corporation for

$840,000 on January 1, 2011 . Sandy’s balance sheet book values and accompanying

fair values on this date are shown below.

Parent

Entity Company

TheoryTheory

Push-Push-

Down Down

BookFairBalanceBalance

Value Value Sheet Sheet

Cash$30,000$30,000________________

Receivables200,000200,000________________

Inventory300,000360,000________________

Land50,00090,000________________

Plant assets-net250,000300,000________________

Total Assets$830,000$980,000________________

Current liabilities$180,000$180,000________________

Other liabilities120,000100,000________________

Common Stock400,000________________

Retained Earnings130,000________________________

Total Liab. & Equity$830,000________________________

Required:

Complete the push-down columns of Sandy Corporation’s restructured balance sheet

using entity theory and parent company theory.

22) The trial balance for the General Fund for Golden City held the following balances

at June 30, 2011, just before closing entries were made:

Due from other funds$2,700

Fund balance – unassigned51,000

Estimated revenues208,000

Revenues198,900

Appropriations196,500

Expenditures – current year193,800

Expenditures – prior year4,500

Other Financing Sources – Transfer from Debt Service Fund6,000

Required:

Prepare the necessary closing entries.

23) On December 31, 2011, Dixie Corporation has the following information available:

Common stock, $10 par$200,000

Additional paid-in capital60,000

Retained earnings40,000

Total stockholders’ equity$300,000

On December 31, 2011, Grimsled Corporation buys an 80% interest in Dixie

Corporation for $240,000. On December 31, 2011, the fair value of Dixie’s assets and

liabilities are equal to the respective book values.

Required:

1> On January 1, 2012, Dixie Corporation sells 5,000 additional shares of common

stock to noncontrolling stockholders at $20 per share. Prepare the journal entry for

Grimsled Corporation on January 1, 2012 .

2> On January 1, 2012, Dixie Corporation sells 5,000 additional shares of common

stock to noncontrolling stockholders at $35 per share. Prepare the journal entry for

Grimsled Corporation on January 1, 2012 .

3> On January 1, 2012, Dixie Corporation sells 5,000 additional shares of common

stock to noncontrolling stockholders at $10 per share. Prepare the journal entry for

Grimsled Corporation on January 1, 2012 .

24) Pelami Corporation owns a 90% interest in Sunbird Corporation. At December 31,

2010, Sunbird had $3,000,000 of par value 6% bonds outstanding with an unamortized

premium of $30,000. The bonds have interest payment dates of January 1 and July 1

and mature on January 1, 2015 .

On January 2, 2011, Pelami purchased $1,200,000 par value of Sunbird’s outstanding

bonds for $1,210,000. Assume straight-line amortization.

Required:

Prepare the necessary consolidation working paper entries with respect to the

intercompany bonds for the year ending December 31, 2011 .

25) Stilt Corporation purchased a 40% interest in the common stock of Shallow

Company for $2,660,000 on January 1, 2011, when the book value of Shallow’s net

equity was $6,000,000. Shallow’s book values equaled their fair values except for the

following items:

BookFair

ValueValueDifference

Inventories$450,000$500,000$ 50,000

Land100,000450,000350,000

Building-net400,000200,000(200,000)

Equipment-net350,000400,00050,000

Required:

Prepare a schedule to allocate any excess purchase cost to identifiable assets and

goodwill.