Return on shareholders’ equity is increased if a firm can maintain its return on assets but

increase its leverage.

Revenue should be recognized over time for the construction of an annex to a building

that the customer owns, even if the seller will not receive payment until the annex is

completed.

Under IFRS, accounts receivable can be accounted for as “available for sale” if that

approach is elected upon initial recognition of the receivable.

Both trading securities and securities available for sale are reported at their fair values.

The adjusted market assessment approach can be used to estimate the stand-alone

selling price of a good or service.

Deferred tax assets and liabilities typically are classified as current or long term

according to when the underlying temporary difference is expected to reverse.

The interest capitalization period for a self-constructed asset ends either when the asset

is substantially complete and ready for use or when interest costs no longer are being

incurred.

Expense for a quality-assurance warranty is recorded along with the related liability in

the reporting period in which the product under warranty is sold.

Selecting the fair value option for an available-for-sale investment is equivalent to

reclassifying that investment as a trading security.

Cash dividends become a binding liability as of the record date.

LIFO liquidation profits occur when inventory quantity declines and costs are rising.

Under IFRS, transfer of risks and rewards of ownership, rather than transfer of control,

is the primary factor determining whether a factored receivable can be treated as sold

rather than as part of a secured borrowing.

The FASB’s required accounting treatment for research and development costs often

understates both net income and assets.

Horizontal analysis involves expressing each item in the financial statements as a

percentage of an appropriate total, or base amount, within the same year.

The following facts relate to gift cards sold by Sunbru Coffee Company during 2016.

Sunbru’s fiscal year ends on December 31.

(a.) In October 2016, sold $3,000 of gift cards, and redeemed $500 of those gift cards.

(b.) In November 2016, sold $4,000 of gift cards, and redeemed $1,400 of October gift

cards and $700 of November gift cards.

(c.) In December 2016, sold $3,000 of gift cards, and redeemed $200 of October gift

cards, $2,000 of November gift cards, and $400 of December gift cards.

(d.) Sunbru views a gift card to be “broken” (with a remote probability of redemption)

two months after the end of the month in which it is sold. Thus, an unredeemed gift

card sold at any time during July would be viewed as broken as of September 30.

Required:

1> Prepare all journal entries appropriate to be recorded only during the month of

December 2016 relevant to gift card sales, gift card redemptions, and gift card

breakage.

2> Determine the balance of the deferred revenue liability to be reported in the

December 31, 2016, balance sheet. Show the relevant T-account information to support

your answer.

For contracts that include more than one separate performance obligation:

a. Revenue is recorded over time at the fair value of each performance obligation.

b. Revenue is recognized in the amount of the contract price on the date the last

separate performance obligation is satisfied.

c. The contract price is allocated to each performance obligation in proportion to the

obligations’ stand-alone selling prices.

d. Revenue is recognized in the amount of the contract price on the date the contract is

signed.

Lake Power Sports sells jet skis and other powered recreational equipment. Customers

pay one-third of the sales price of a jet ski when they initially purchase the ski, and then

pay another one-third each year for the next two years. Because Lake has little

information about the ability to collect these receivables, it uses the installment sales

method for revenue recognition. In 2015, Lake began operations and sold jet skis with a

total price of $900,000 that cost Lake $450,000. Lake collected $300,000 in 2015,

$300,000 in 2016, and $300,000 in 2017 associated with those sales. In 2016, Lake sold

jet skis with a total price of $1,500,000 that cost Lake $900,000. Lake collected

$500,000 in 2016, $400,000 in 2017, and $400,000 in 2018 associated with those sales.

In 2018, Lake also repossessed $200,000 of jet skis that were sold in 2016. Those jet

skis had a fair value of $75,000 at the time they were repossessed.

In 2017, Lake would recognize realized gross profit of:

a. $0.

b. $450,000.

c. $310,000.

d. $700,000.

Using International Financial Reporting Standards (IFRS), which of the following

statements is true regarding correcting errors in previously issued financial statements?

a. Retrospective application is required with no exception.

b. The error can be reported in the current period if it’s not considered practicable to

report it prospectively.

c. The error can be reported prospectively if it’s not considered practicable to report it

retrospectively.

d. The error can be reported in the current period if it’s not considered practicable to

report it retrospectively.

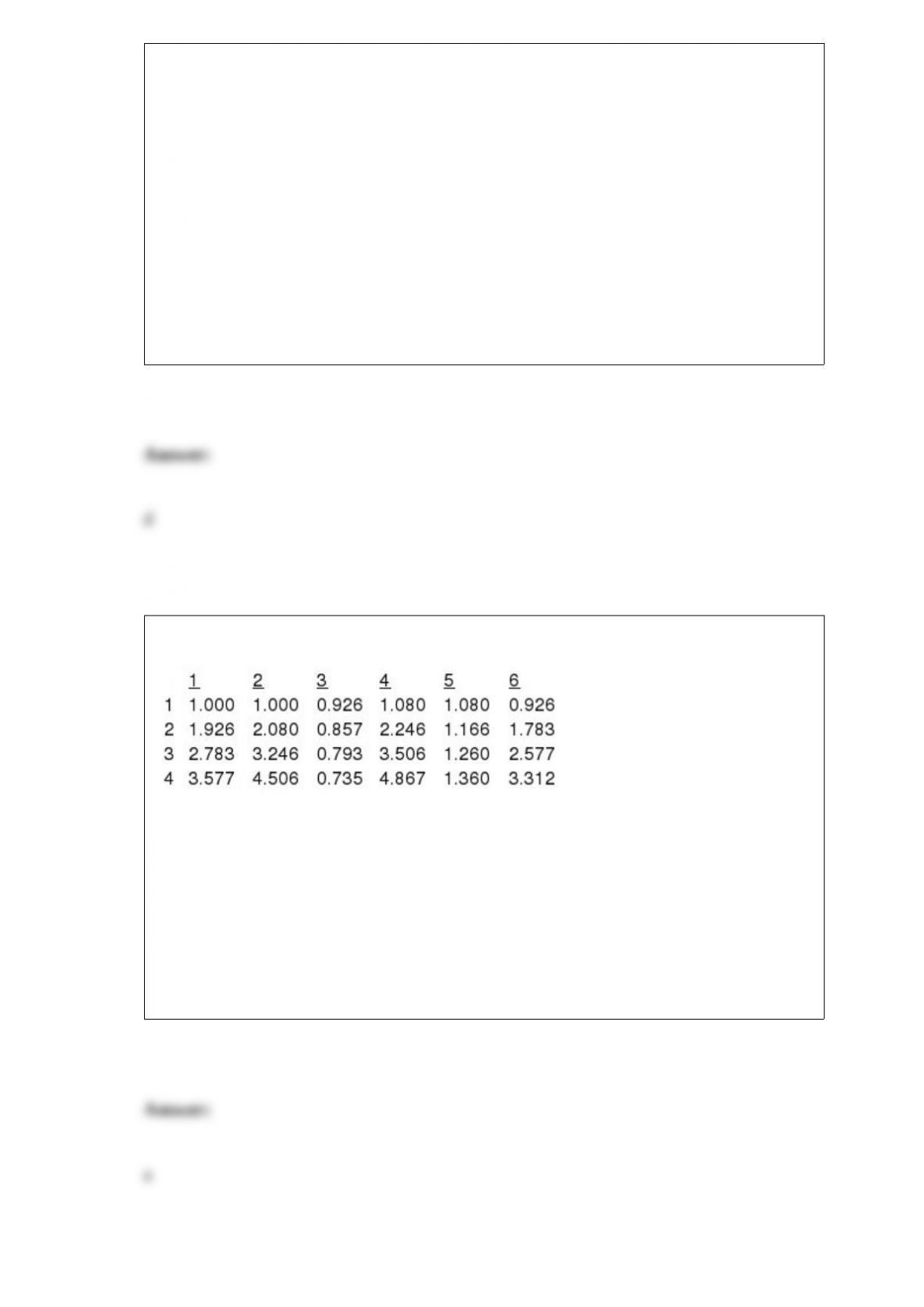

Below are excerpts from time value of money tables for the 8% rate.

Column 6 is an interest table for the:

a. Present value of an ordinary annuity of 1.

b. Future value of an ordinary annuity of 1.

c. Present value of an annuity due of 1.

d. Future value of an annuity due of 1.

Under current tax law, generally a net operating loss may be carried back:

a. 2 years.

b. 5 years.

c. 15 years.

d. 20 years.

Montgomery & Co., a well-established law firm, provided 500 hours of its time to Fink

Corporation in exchange for 1,000 shares of Fink’s $5 par common stock.

Montgomery”s usual billing rate is $700 per hour, and Fink’s stock has a book value of

$250 per share. By what amount will Fink’s paid-in capital’”-excess of par increase for

this transaction?

a. $345,000.

b. $295,000.

c. $350,000.

d. $300,000.

On January 1, 2016, Ozark Minerals issued $10 million of 9%, 10-year convertible

bonds at 101. The bonds pay interest on June 30 and December 31. Each $1,000 bond is

convertible into 40 shares of Ozark’s no par common stock. Bonds that are similar in all

respects, except that they are nonconvertible, currently are selling at 99. Upon issuance,

Ozark should:

a. Debit discount on bonds payable $100,000.

b. Credit premium on bonds payable $100,000.

c. Credit equity $100,000.

d. Credit bonds payable $10,100,000.

The market price of a bond issued at a discount is the present value of its principal

amount at the market (effective) rate of interest:

a. Less the present value of all future interest payments at the rate of interest stated on

the bond.

b. Plus the present value of all future interest payments at the rate of interest stated on

the bond.

c. Plus the present value of all future interest payments at the market (effective) rate of

interest.

d. Less the present value of all future interest payments at the market (effective) rate of

interest.

Under the NBA deferred compensation plan, payments made at the end of each year

accumulate up to retirement and then retirees are given two options. Option 1 allows the

retiree to select the amount of the annual payment to be received, and option 2 allows

the retiree to specify over how many years payments are to be received. Assume

Rodman has had $6,000 deposited at the end of each year for 30 years, and that the

long-term interest rate has been 8%.

Required:

a. How much has accumulated in Rodman’s deferred compensation account?

b. How much will Rodman be able to withdraw at the beginning of each year if he

elects to receive payments for 15 years?

c. How many years will Rodman be able to receive payments if he chooses to receive

$65,000 per year at the beginning of each year?

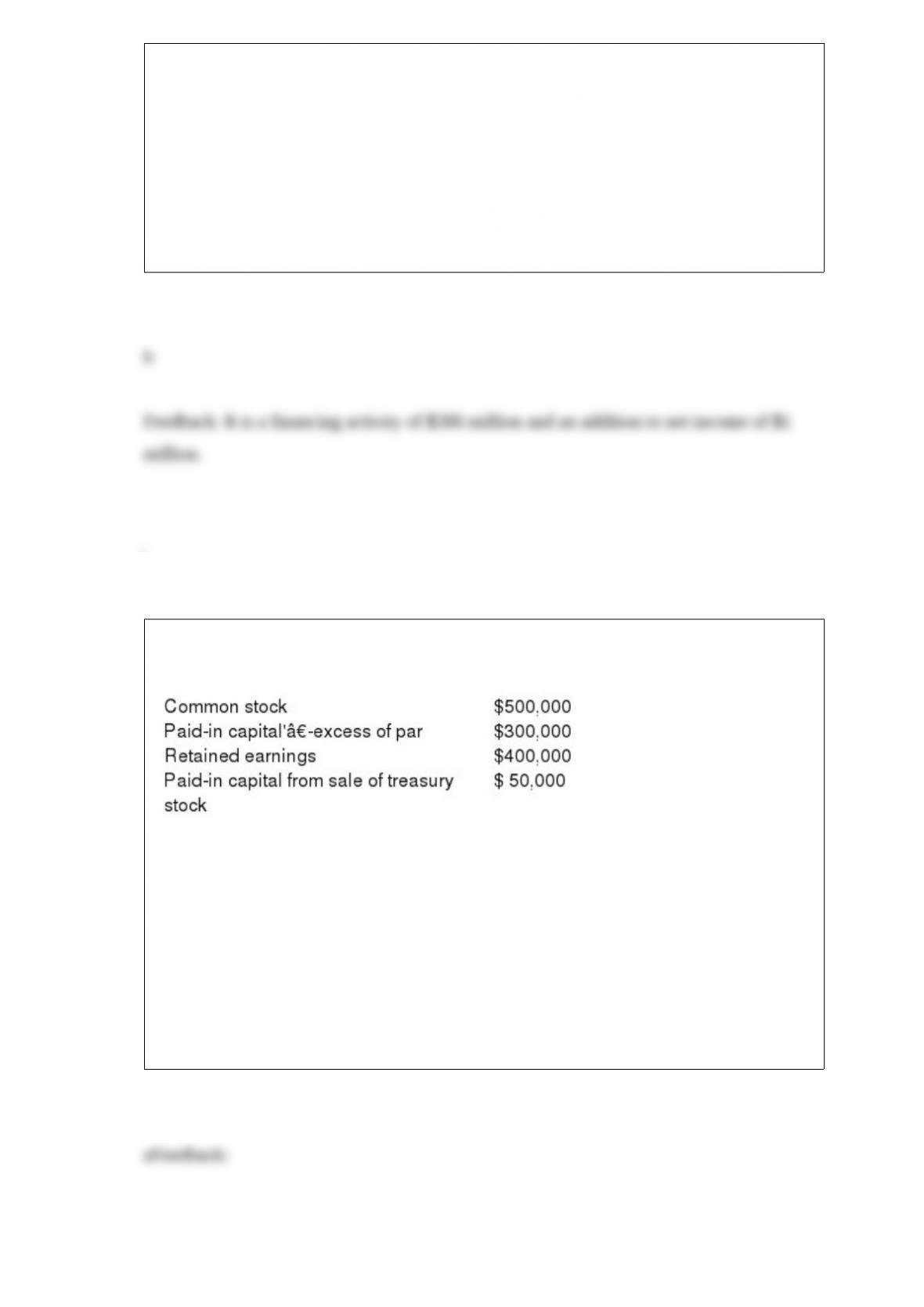

On June 4, White Corporation issued $400 million of bonds for $386 million. During

the same year, $1 million of the bond discount was amortized. In a statement of cash

flows prepared by the indirect method, White Corporation should report:

a. A financing activity of $400 million.

b. An addition to net income of $1 million.

c. An investing activity of $386 million.

d. A deduction from net income of $1 million.

On January 1, 2016, the board of directors of Goby Inc. declared a $540,000 dividend.

The following data is from the balance sheet of Goby on that date:

How much is the liquidating dividend?

a. $140,000.

b. $240,000.

c. $290,000.

d. None of these answer choices is correct.

Which category completely excludes equity securities?

a. Securities available for sale.

b. Consolidating securities.

c. Held-to-maturity securities.

d. Trading securities.

Under the retail inventory method:

a. A company measures inventory on its balance sheet by converting retail prices to

cost.

b. A company measures inventory on its balance sheet at current selling prices.

c. A company measures inventory on its balance sheet on a LIFO basis.

d. None of these answer choices are correct.

Loan A has the same original principal, interest rate, and payment amount as Loan B.

However, Loan A is structured as an annuity due, while Loan B is structured as an

ordinary annuity. The maturity date of Loan A will be:

a. Earlier than Loan B.

b. Later than Loan B.

c. The same as Loan B.

d. Indeterminate with respect to loan B.

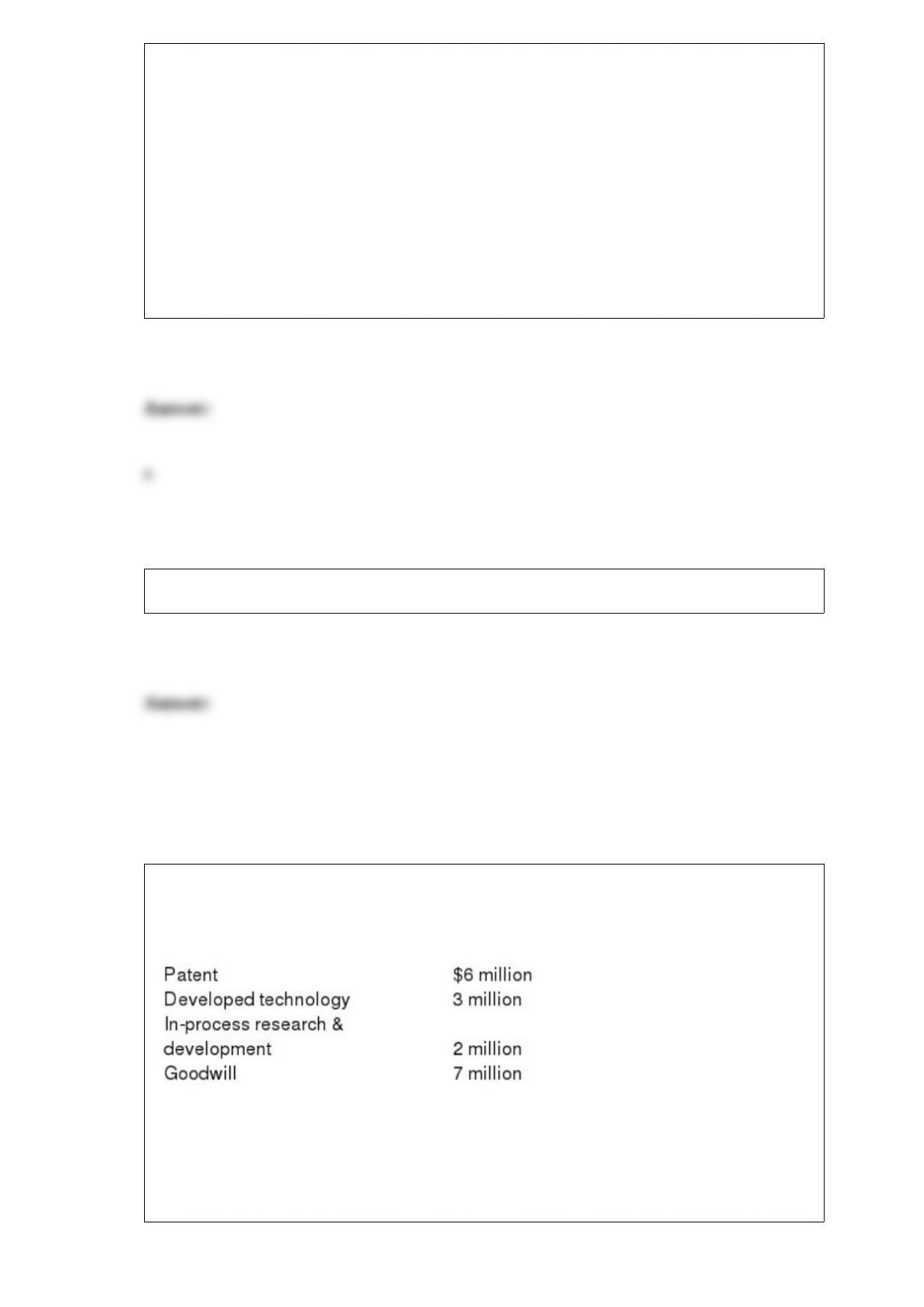

On September 30, 2016, Morgan, Inc. acquired all of the outstanding common stock of

Pathways, Inc., for $100 million. In addition to tangible assets, Morgan recorded the

following assets as a result of the acquisition:

Morgan’s policy is to amortize intangible assets using the straight-line method, no

residual value, and a six-year useful life. Required:

What is the total amount of expenses that would appear in Morgan’s income statement

for the year ended December 31, 2016, related to these items?

In 2015, Dooling Corporation acquired Oxford Inc. for $250 million, of which $50

million was attributed to goodwill. At the end of 2016, Dooling’s accountants derive the

following information for a required goodwill impairment test:

Assume the same facts as above, except that the fairvalue of Oxford (the reporting unit)

is $225 million.

Required: Determine the amount, if any, of the goodwill impairment loss that Dooling

must recognize on these assets.

Listed below are 5 terms followed by a list of phrases that describe or characterize each

of the terms. Match each phrase with the number for the correct term.

Answer

Symington and Cribbs (S&C) is a sporting goods distributor. S&C uses the FIFO

inventory method to determine the cost of its ending inventory. Ending inventory

quantities are determined by a physical count. For the fiscal year-end December 31,

2016, ending inventory was originally determined to be $67 million. However, in early

January of 2017, the company’s controller, Amy Grant, discovered that an error was

made in the inventory count. The correct amount of ending inventory should be $87

million. The auditors did not discover the error and the financial statements are

scheduled to be issued on February 26, 2017. S&C is a public company.

Amy’s first reaction was to communicate her finding to the auditors and to revise the

financial statements before they are issued. However, she knows that this was a very

good year for the company with profits far exceeding analysts’ expectations. If the error

is not corrected this year, it will self-correct next year as long as 2017 ending inventory

is correctly stated. This will help future 2017 profits. On the other hand, her fellow

workers’ profit sharing plans are based on annual pretax earnings and if she revises the

statements, everyone’s profit sharing bonus will be higher this year. Required:

1> Is Amy correct by stating that the error will self-correct next year as long as 2017

ending inventory is correctly stated? If the error is not corrected in the current year,

what will be the effect on 2016 and 2017 income before tax?

2> Discuss the ethical dilemma Amy faces.

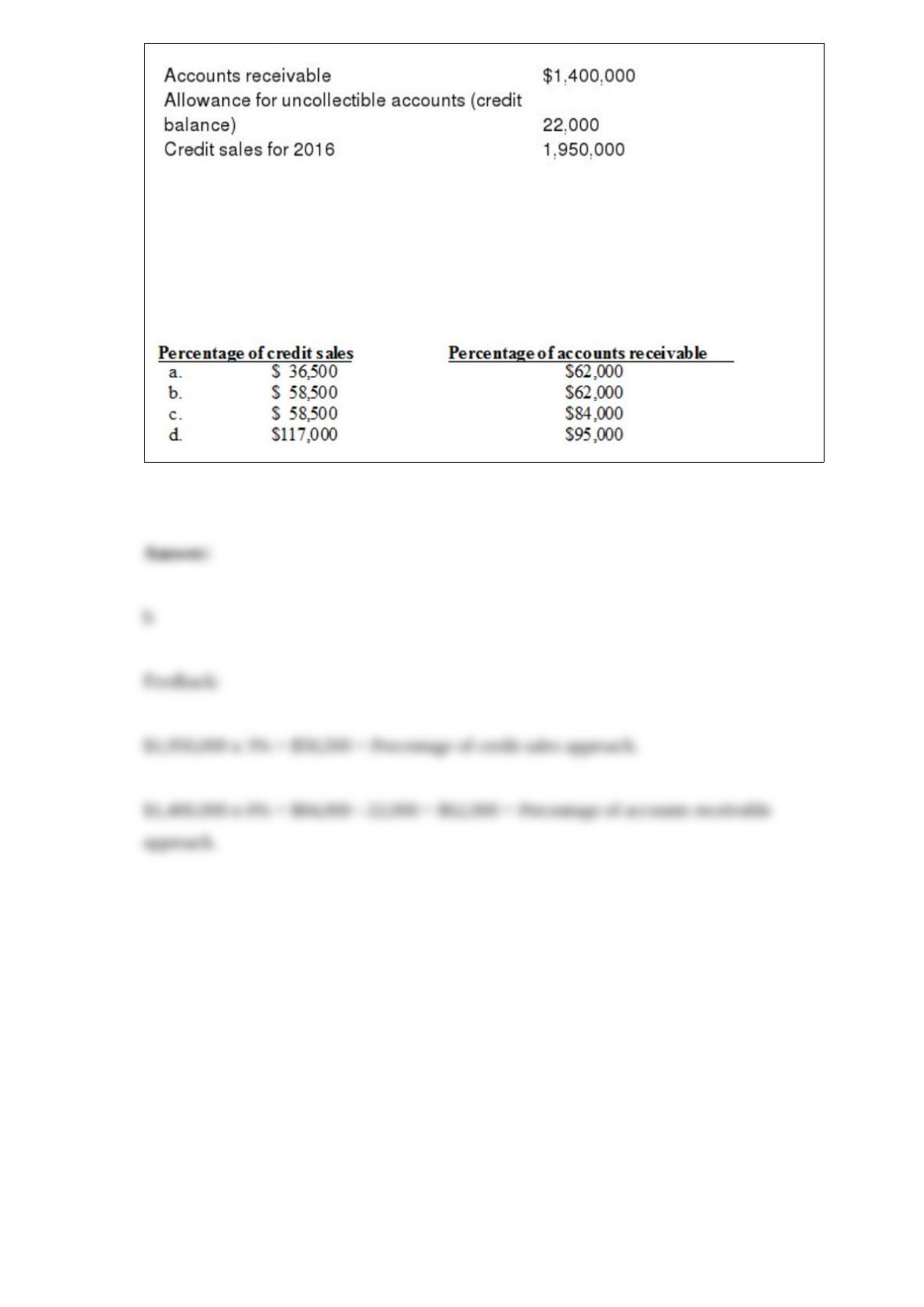

San Mateo Company had the following account balances at December 31, 2016, before

recording bad debt expense for the year:

San Mateo is considering the following approaches for estimating bad debts for 2016:

– Based on 3% of credit sales

– Based on 6% of year-end accounts receivable What amount should San Mateo charge

to bad debt expense at the end of 2016 under each method?