If a physical count of inventory indicates that the Merchandise Inventory account is

overstated, an adjusting entry is required to record the difference.

Long Company owns a 2% investment in the common stock of Smith Company. The

receipt of a cash dividend from Smith will have no effect on Long’s total equity.

When using management by exception, managers investigate only those variances that

are unfavorable.

A strategic budget will be as detailed as an operational budget.

When using the FIFO inventory costing method, ending merchandise inventory will be

the highest, as compared to LIFO and weighted-average inventory costing methods,

when costs are decreasing.

If a long-term debt is paid in installments, the business will report the current portion of

the note payable as a current liability.

A law firm provides legal services for clients who do not pay immediately. As a result

of this transaction, assets and revenues increase.

Gross profit is the extra amount the company receives from the customer for

merchandise sold over what the company paid to the vendor.

The fixed manufacturing overhead is considered a product cost in variable costing and a

period cost in absorption costing.

An amount that a merchandiser earns by selling its inventory is known as sales revenue

or sales.

Enterprise resource planning systems are software systems that can integrate all of a

company’s functions, departments, and data into a single system.

Under the periodic inventory system, purchases, purchase discounts, and purchase

returns and allowances are recorded in the Merchandise Inventory account as and when

they occur.

Dividends received from available-for-sale investments are recorded with a debit to the

Dividend Revenue account.

As a part of the closing process, revenues and expenses may be closed to a temporary

account called the Net Income (Loss) account.

In a decentralized company, segment managers may not fully understand the big picture

when making decisions.

The gross profit percentage measures the profitability of each sales dollar above the

cost of goods sold.

The primary activity of manufacturing companies is to purchase goods from a

wholesaler and resell them.

The fact that invested cash earns interest over time is called the time value of money.

The three categories of period costs are direct materials, direct labor, and manufacturing

overhead.

When stock is issued for assets other than cash, the transaction is recorded at the market

value of the stock issued or the market value of the assets received, whichever is more

clearly determinable.

The income statement shows whether or not a business can generate enough cash to pay

its liabilities.

A corporation purchased office supplies on account. As a result of this transaction,

expenses and liabilities will increase.

The payback method uses discounted cash flows to make investment decisions.

International Financial Reporting Standards (IFRS) is the main U.S. accounting rule

book and is currently created and governed by the Financial Accounting Standards

Board.

The balance in the Bonds Payable account is a credit of $77,000. The balance in the

Discount on Bonds Payable is a debit of $3,600. The balance sheet will report the bond

balance as $80,600.

Financial reporting is typically much more detailed than managerial accounting.

Weighted average cost per unit is determined by dividing the cost of goods available for

sale by the number of units available.

The operating activities section of the statement of cash flows reflects the cash flows

that affect current assets and current liabilities.

In a manufacturing company, accounting, legal, and administrative costs are typical

examples of product costs.

Managerial accounting can be used to calculate costs for service and merchandising

companies.

Manufacturing overhead includes all manufacturing costs, such as direct labor and

direct materials.

In making product mix decisions under constraining factors, which of the following is

the key to choosing the product type to be maximized?

A) revenue per unit

B) contribution margin per unit of product

C) contribution margin per unit of the constraint

D) gross profit per unit using traditional costing

AAA Metal Bearings produces two sizes of metal bearings (sold by the crate)—

standard and heavy. The standard bearings require $200 of direct materials per unit (per

crate), and the heavy bearings require $245 of direct materials per unit. The operation is

mechanized, and there is no direct labor. Previously AAA used a single plantwide

allocation rate for manufacturing overhead, which was $1.55 per machine hour. Based

on the single rate, gross profit was as follows:

Per unit Standard Heavy

Direct materials cost $200.00 $245.00

Manufacturing overhead cost 124.00 93.00

Total manufacturing cost $324.00 $338.00

Sales price per unit 350.00 370.00

Gross profit per unit $26.00 $32.00

Although the data showed that the heavy bearings were more profitable than the

standard bearings, the plant manager knew that the heavy bearings required much more

processing in the metal fabrication phase than the standard bearings, and that this factor

was not adequately reflected in the single plantwide allocation rate. He suspected that it

was distorting the profit data. He suggested adopting an activity-based costing

approach.

Working together, the engineers and accountants identified the following three

manufacturing activities and broke down the annual overhead costs as shown below:

Activities: Estimated Cost

Metal fabrication $420,000

Machine processing 152,000

Packaging 17,000

Total overhead cost $589,000

Engineers believed that metal fabrication costs should be allocated by weight and

estimated that the plant processed 12,000 kilos of metal per year. Machine processing

costs were correlated to machine hours, and the engineers estimated a total of 380,000

machine hours for the year. Packaging costs were the same for both types of products,

and so they could be allocated simply by the number of units produced. The production

plan provided for 4,000 units of standard and 1,000 units of heavy bearings to be

produced during the year. Additional data on a per unit basis was as given below:

Standard Heavy

Kilos per unit 2.00 4.00

Machine hours per unit 80.00 60.00

Using the data above, calculate the predetermined overhead allocation rates using

activity-based costing. Then, following the ABC methodology, calculate the production

cost and gross profit for one unit of standard bearings. (Round your intermediate

calculations to two decimal places.)

Which of the following is true of source documents in an accounting information

system?

A) All journal entries can be considered as source documents in an accounting

information system.

B) Source documents provide control and reliability in an accounting information

system.

C) A manual document cannot be considered as a source document in an accounting

information system.

D) In a manual accounting information system, source documents refer to financial

statements.

McLeod Fries, Inc. has budgeted sales for June and July at $680,000 and $750,000,

respectively. Sales are 90% credit, of which 70% is collected in the month of sale and

30% is collected in the following month. What is the budgeted Accounts Receivable

balance on July 31?

A) $225,000

B) $202,500

C) $183,600

D) $675,000

Which of the following describes the financing activities section of the statement of

cash flows?

A) It includes increases and decreases in long-term assets.

B) It includes cash inflows and outflows involved in long-term liabilities and equity.

C) It includes interest and dividend income and cash payments for interest expense.

D) It reports on activities that create revenue or expenses for the entity’s business.

Which of the following inventory costing methods results in the lowest value of ending

inventory during a period of rising inventory costs?

A) specific identification

B) weighted-average

C) last-in, first-out

D) first-in, first-out

Bloomington, Inc. is a merchandiser of stone ornaments. The company sold 7,000 units

during the year. The company has provided the following information:

What is the cost of goods sold for the year?

A) $362,000

B) $320,000

C) $318,000

D) $305,000

The ending Merchandise Inventory for the current accounting period is understated by

$2,700. What effect will this error have on Cost of Goods Sold and Net Income for the

current accounting period?

A)

B)

C)

D)

Prepaid Rent in the worksheet’s unadjusted trial balance column is $5,000. Prepaid Rent

in the balance sheet column is $2,000. Which of the following entries would have

caused this difference?

A) a $3,000 debit entry to Prepaid Rent in the worksheet’s adjustments column

B) a $3,000 credit entry to Rent Expense in the worksheet’s adjustments column

C) a $3,000 credit entry to Prepaid Rent in the worksheet’s adjustments column

D) a $3,000 credit entry to Rental Revenue in the worksheet’s adjustments column

A bond is issued at discount when a bond’s stated interest rate is ________.

A) equal to the market interest rate

B) more than the effective interest rate

C) less than the market interest rate

D) more than the market interest rate

Which of the following is true of an effective accounting information system?

A) It has little influence in improving a company’s internal control activities.

B) The cost of using an accounting information system is the same for both small and

large businesses.

C) A compatible accounting information system works smoothly with the business’s

employees and organizational structure.

D) Large private companies prefer a manual accounting information system since their

financial statements are not audited.

The following contains information from the records of the Wellborn Engineers and

Architects.

Wellborn Engineers and Architects

Selected Financial Information

December 31, 2017

Calculate the current ratio. (Round your answer to two decimals.)

A) 1.46

B) 2.28

C) 0.64

D) 3.00

Madison, Inc. had the following balances and transactions during 2017.

The company maintains its records of inventory on a perpetual basis using the last-in,

first-out inventory costing method. Calculate the amount of ending Merchandise Inventory

at December 31, 2017 using the lower-of-cost-or-market rule. (Round any intermediate

calculations two decimal places, and your final answer to the nearest dollar.)

A) $2,880

B) $3,412

C) $3,713

D) $3,572

Which of the following is a plant asset?

A) Equipment

B) Patents

C) Trademark

D) Accounts Receivable

Under the first-in, first-out (FIFO) method, the current period equivalent units of

production for transferred in units in beginning inventory are zero because ________.

A) these units are transferred back to the previous department for further processing in

the current period

B) these units are expected to be sold by the receiving department without subjecting

them to further processing

C) no additional costs for these units were transferred in the current period

D) costs involved in inter-departmental transfers are accounted for only once when

sales are made to customers

On January 1, Alistair Manufacturing had a beginning balance in Work-in-Process

Inventory of $164,000 and a beginning balance in Finished Goods Inventory of

$25,000. During the year, Alistair incurred manufacturing costs of $202,000.

During the year, the following transactions occurred:

Job C-62 was completed for a total cost of $140,000 and was sold for $157,000.

Job C-63 was completed for a total cost of $181,000 and was sold for $212,000.

Job C-64 was completed for a total cost $82,000 but was not sold as of year-end.

The Manufacturing Overhead account had an unadjusted credit balance of $24,000 and

was adjusted to zero at year-end.

What was the amount of gross profit reported by Alistair at the end of the year?

A) $48,000

B) $72,000

C) $17,000

D) $31,000

The tracking of inventory shrinkage due to theft, damage, or errors is done with the help

of a (n) ________ of inventory.

A) authorization

B) sale

C) physical count

D) delivery

Which of the following is not a decision tool based on working capital?

A) cash ratio

B) acid-test ratio

C) current ratio

D) dividend payout ratio

A favorable sales volume variance in variable costs suggests a(n) ________.

A) increase in number of actual units sold when compared to the expected number of

units sold

B) decrease in number of actual units sold when compared to the expected number of

units sold

C) increase in variable cost per unit

D) decrease in fixed costs

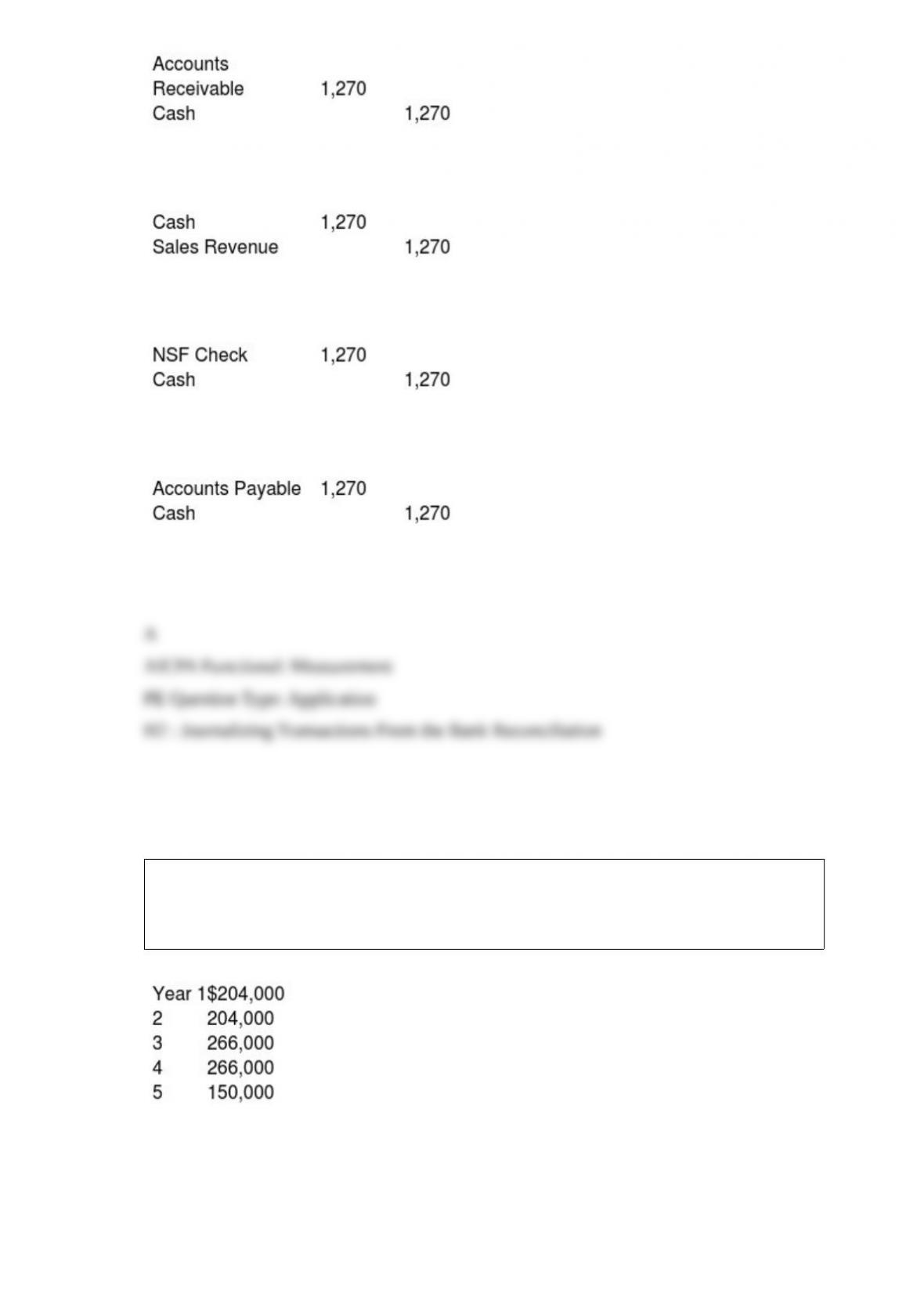

A customer’s check for $1,270 was returned for nonsufficient funds. Which of the

following journal entries is needed to adjust for the NSF check?

A)

B)

C)

D)

Paramount Carpets is considering purchasing new equipment costing $730,000. The

company’s management has estimated that the equipment will generate cash flows as

follows:

Considering the residual value is zero, calculate the payback period. (Round your answer

to two decimal places.)

A) 4.61 years

B) 3.21 years

C) 3.42 years

D) 3.70 years

The journal entry to record indirect labor costs incurred involves a debit to the

________.

A) Manufacturing Overhead account

B) Wages Payable account

C) Finished Goods Inventory account

D) Work-in-Process Inventory account

Mickey Tire Company makes a special kind of racing tire. Variable costs are $225 per

unit, and fixed costs are $30,000 per month. Mickey sells 500 units per month at a sales

price of $310. If the quality of the tire is upgraded, the company believes it can increase

the sales price to $349. If so, the variable cost will increase to $234 per unit, and the

fixed costs will rise by 50%. If Mickey decides to upgrade, how will operating income

be affected?

A) Operating income will decrease by $15,000.

B) Operating income will decrease by $4,500.

C) Operating income will increase by $4,500.

D) Operating income will remain the same.

The ________ method allows managers to increase operating income through

production by producing more products than needed.

A) absorption costing

B) variable costing

C) direct costing

D) marginal costing

Salaries are $6,500 per week for five working days and are paid weekly at the end of

the day Fridays. The end of the month falls on a Thursday. The accountant for Dayton,

Inc. made the appropriate accrual adjustment and posted it to the ledger. The balance of

Salaries Payable, as shown on the adjusted trial balance, will be a ________. (Assume

that there was no beginning balance in the Salaries Payable account.)

A) credit balance of $5,200

B) debit balance of $1,300

C) debit balance of $5,200

D) credit balance of $1,300

Which of the following line items will appear on the income statement of a

merchandiser but not of a service company?

A) Salaries Expense

B) Depreciation Expense

C) Cost of Goods Sold

D) Supplies Inventory

The purchases journal is a special journal that ________.

A) has special columns for credits to merchandise inventory

B) is used to record all purchases of merchandise inventory

C) has a special column for debits to accounts payable

D) is used to record merchandise inventory, office supplies, and other assets purchased

on account

Which of the following is included in the entry to record estimated warranty payable?

A) a credit to Estimated Warranty Payable

B) a credit to Merchandise Inventory

C) a credit to Warranty Expense

D) a debit to Estimated Warranty Payable

The ending merchandise inventory for the current year is overstated by $28,000. What

effect will this error have on the following year’s net income?

A) The net income will be overstated by $56,000.

B) The net income will be overstated by $28,000.

C) The net income will be understated by $28,000.

D) The net income will be understated by $56,000.

Which of the following is affected as a result of an error in performing the physical

count of inventory at the end of the accounting period?

A) sales revenue

B) operating expenses

C) net income

D) net cost of purchases

Common-size statements ________.

A) allow the users to compare numbers in relative terms rather than absolute amounts

B) report dollar amounts and percentages

C) create a dollar value bias

D) show the same percentages that appear in a horizontal analysis

Which of the following internal business perspective key performance indicators (KPIs)

is commonly used to assess the innovation process?

A) number of new products developed

B) number of warranty claims

C) employee turnover rate

D) rate of on-time deliveries

When production is greater than sales, the operating income will be higher under

absorption costing than variable costing. Assume zero beginning and ending

inventories. Which of the following gives the correct reason for the above statement?

A) All costs incurred have been recorded as expenses.

B) A portion of the fixed manufacturing overhead is still in the ending Finished Goods

Inventory account.

C) All selling and administrative expenses have been recorded as period costs.

D) Fixed manufacturing costs have not been considered when calculating the operating

profits.

The current ratio measures a company’s ________.

A) overall ability to pay liabilities

B) ability to pay current liabilities with current assets

C) proportion of assets that are financed by debt

D) rate of cash flow

Which of the following best describes the term capital rationing?

A) a method of determining the period within which the cash invested is recouped

B) a process of ranking and choosing among alternative capital investments based on

the availability of funds

C) a method which shows the effect of an investment on a company’s accrual-based

income

D) a process of controlling operating costs when adequate funds are not available

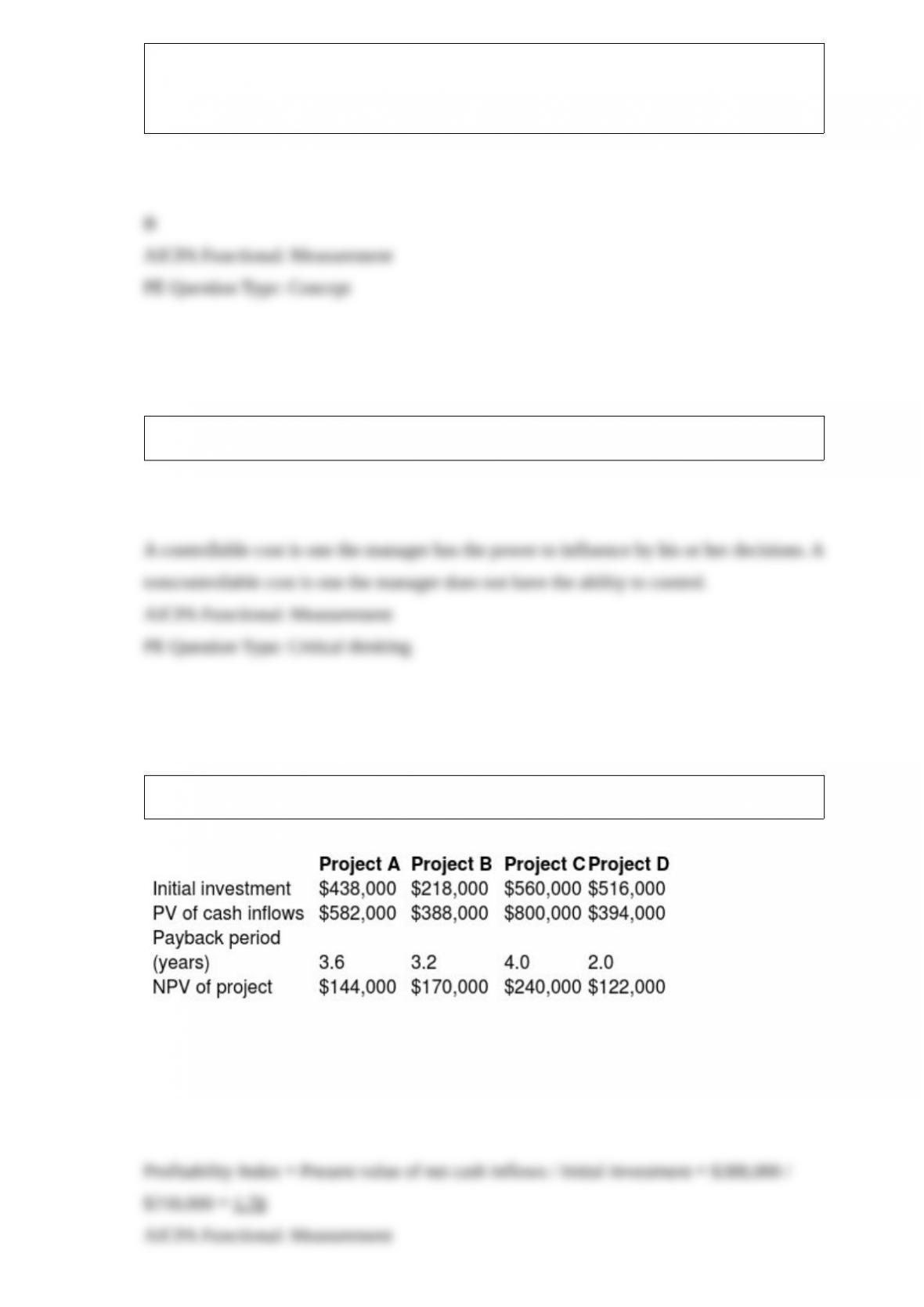

Explain the difference between a controllable and a noncontrollable cost.

The following information is provided by Dinovo Systems:

Calculate the profitability index for Project B. Show your calculations and round to two

decimal places.

Under what circumstances is the investment with the shortest payback the best choice?

How should managers use the payback method?

Redribbon Gallery reported the following assets on its December 31, 2017 balance

sheet:

Dec. 31, 2017 Dec. 31, 2016

Cash $35,000 $28,000

Accounts Receivable 97,000 85,000

Merchandise Inventory 80,000 62,000

Prepaid Expenses 29,000 20,000

Property, plant, and equipment, net 30,000 18,000

If the net sales for the year amounted to $850,000, what is the asset turnover ratio for

2017?

Define joint cost. Should joint costs be considered in the decision to sell or further

process the product? Explain your answer.

On October 1, 2017, Carlos, Inc. borrowed $225,000 by signing a nine-month, 8% note

payable. Interest was accrued on December 31, 2017. Prepare the journal entry July, 1,

2017, the date the note was paid.

For each transaction, identify which account is debited and which account is credited.

Use proper account titles.

On January 1, 2017, Blizzard Manufacturing Corporation purchased a machine for

$40,000,000. The corporation expects to use the machine for 24,000 hours over the next

six years. The estimated residual value of the machine at the end of the sixth year is

$40,000. The corporation used the machine for 3,600 hours in 2017 and 5,000 hours in

2018. What is the depreciation expense for 2017 and 2018 if the corporation uses the

double-declining-balance method of depreciation?

On December 31, 2016, Thompson Hardware Company purchases $300,000 of

property by paying $50,000 in cash and signing a 10-year mortgage note at 13% for the

balance. The amortization schedule shows that the company will pay $46,072 per year.

Journalize the first yearly payment on December 31, 2017.

Provide the formula for (1) To account for and (2) Accounted for.

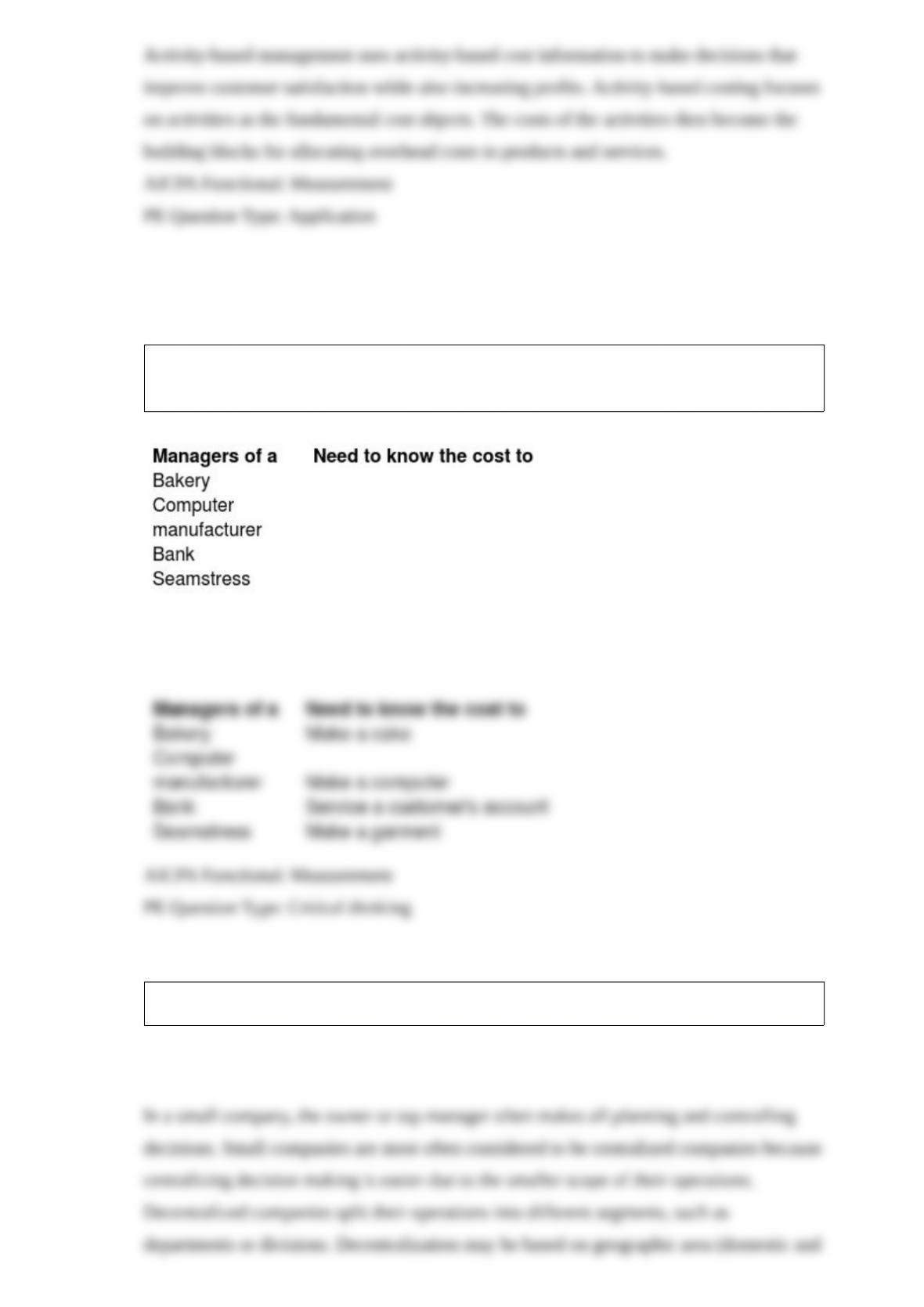

What is activity-based management? How is it different from activity-based costing?

For each of the following types of business, indicate why the manager needs to know

the unit cost information.

Discuss the difference between a centralized company and a decentralized company.

Egerton, Inc. has two processes—Coloring Department and Mixing Department.

Egerton sold 350 gallons on account at $110 per gallon. The total cost of processing

was $385,000 for 5,500 gallons of paint. Throughout the year, the company used a

predetermined overhead allocation rate to allocate $75,000 and $65,000 of indirect

costs to the Coloring Department and Mixing Department, respectively. The actual

overhead cost incurred amounted to $150,000 at the end of the year. Record the

necessary journal entries for the sale of goods and for adjustment of over- or

underallocated manufacturing overhead at the end of the year.

Define treasury stock and provide two reasons why a corporation would purchase

treasury stock.

When computing a bond’s cash flow for interest, which interest rate is used? Why?

Dolby, Inc. issued a $5,000 face value, 10%, five-year bond at 98. What will be the

journal entries at the maturity of the bond? The bonds have semiannual interest, and the

company uses the straight-line method of discount amortization.

List three questions managers should consider when deciding whether to drop a product

or a business segment.