A cheque involves three parties: the maker, who signs the cheque, the payee, who is the

recipient, and the bank, on which the cheque is drawn.

A compound journal entry usually affects three or more accounts.

Credit terms are the listing of the amounts and timing of payments between a buyer and

a seller.

If the total balance of the Accounts Receivable Ledger equals the total of the controlling

Accounts Receivable account, then the individual accounts are presumed to be correct.

Harley Ravidson’s current ratio is .9 to 1. The industry average current ratio is 1.2.

Harley Davidson does not have a problem in covering its current liabilities because of

its strong sales and position in its industry.

The retail inventory method estimates the cost of ending inventory by applying the

gross profit ratio to net sales.

Internal control policies and procedures are standard across companies.

Errors in inventory valuation only affect the current period’s records and financial

statements.

Equity is increased by owner investments, net income and withdrawals.

The purpose of an audit is to add credibility to the financial statements.

Reversing entries are optional.

A transaction that increases an asset account and decreases a liability account must also

affect another account.

On April 1, Gallery Corp. entered into a two-month contract for $50,000. Gallery Corp.

earned $25,000 of the contract in April and billed the customer. Gallery Corp. should

recognize the revenue when it receives the customer’s cheque.

Accounts unique to merchandising companies include Merchandise Inventory, Sales,

Sales Discounts, Sales Returns and Allowances, and Cost of Goods Sold.

An internal control system is comprised of the policies and procedures companies use

to protect assets, ensure reliable accounting, and promote efficient operations.

Individuals and organizations who own the right to receive payments from a business

are called its debtors.

Goods in transit are automatically included in inventory.

As prepaid assets are used up, the costs of the assets become expenses.

Debits increase asset and expense accounts.

Preventing unauthorized access to company resources is one of the most difficult and

time-consuming tasks for internal control experts.

Ethics and social responsibility are incidental to the primary functions of accounting.

Business transactions are exchanges of economic consideration between two parties.

A Sales Journal is used to record cash sales.

Most transactions for merchandising businesses fall into four groups: sales on credit,

purchases on credit, cash receipts, and cash disbursements.

The gross profit ratio measures how much of each dollar of gross sales is gross profit.

Trekking Company’s cost of goods sold was $15,550. Its average merchandise

inventory was $4,575. Its merchandise turnover was 3.4.

When a company sells services for which cash will not be received until some future

date, the company should credit an unearned revenues account for the amount charged

to the customer.

Basic services provided by banks such as bank accounts, deposit slips and cheques

contribute to the control and safeguarding of cash.

A transaction that decreases an asset account and increases a liability account must also

affect another account.

The days’ sales uncollected ratio is calculated by dividing accounts receivable by net

sales and multiplying the answer by 365.

The principle of faithful representation requires that information be complete, neutral

and free from error so that assets and income are not overstated and liabilities and

expenses are not understated.

To make it easier for the bookkeeper, the cost of land is separated from the cost of

buildings located on the land.

The direct write-off method is used because it is simpler than the allowance method.

The third closing entry is to close Withdrawals to Income Summary.

The normal balance of an account refers to the debit or credit side where increases are

recorded.

The first step in the accounting cycle is to analyze and record transactions during the

accounting period.

Trekking Company’s inventory in its River Oaks store was destroyed by a flood. Its

gross profit ratio was 65% and net sales were $30,000. The estimated cost of goods

available for sale was $32,500. The estimated value of the lost inventory was $18,000.

The direct write-off method does not use an allowance for doubtful accounts account.

Cash sales total $705 and the amount of cash in the register is $685. The shortage of

$20 represents an expense.

Bonding does not discourage loss from theft because employees know that bonding is

an insurance policy against loss from theft.

Which of the following accounting principles would require that all goods and services

purchased be recorded at cost?

A. Going concern principle.

B. Monetary unit principle.

C. Cost principle.

D. Business entity principle.

E. Revenue recognition principle.

The special account used only in the closing process to temporarily hold the amounts of

revenues and expenses before the net difference is added to (or subtracted from) the

owner’s capital account is the:

A. Income Summary account.

B. Closing account.

C. Balance column account.

D. Contra account.

E. Nominal account.

The ledger that contains the financial statement accounts of a business is the:

A. Columnar journal.

B. Accounts payable ledger.

C. General journal.

D. General ledger.

E. Subsidiary ledger.

In reconciling the bank balance, the amount of an unrecorded bank service charge

should be:

A. Added to the book balance of cash.

B. Deducted from the book balance of cash.

C. Added to the bank balance of cash.

D. Deducted from the bank balance of cash.

E. Noted as a memo.

The accounting principle that states that revenue is recorded at the time that it is earned

regardless of whether cash or another asset has been exchanged is the:

A. Monetary unit principle.

B. Business entity principle.

C. Going concern principle.

D. Revenue recognition principle.

E. Cost principle.

Social responsibility:

A. Is a code that helps accountants when dealing with confidential information.

B. Is a concern for the impact of our actions on society as a whole.

C. Allows Canada Revenue Agency to regulate businesses.

D. Requires that all businesses conduct social audits.

E. Requires analysts to report information favourable to their companies.

Martock Company uses the periodic inventory system. The following information is

available for the period ending December 31:

(1) Sales: $30,000

(2) Beginning inventory: $17,500

(3) Ending inventory: $8,000

(4) Purchases: $10,000

The cost of goods sold for the period is:

A. $19,500.

B. $21,500.

C. $24,500.

D. $25,100.

E. $26,000.

From the following information taken from the records of Peach Company at December

31 of this year, calculate equity.

A. $1,500.

B. $2,500.

C. $7,500.

D. $3,500.

E. $6,000.

If, in preparing a work sheet, an adjusted trial balance amount is sorted to the wrong

work sheet column, the Balance Sheet columns will balance on completing the work

sheet, but with the wrong net income, if the amount sorted in error is:

A. An expense amount entered in the Balance Sheet Credit column.

B. A revenue amount entered in the Balance Sheet Debit column.

C. A liability amount entered in the Income Statement Credit column.

D. An asset amount entered in the Balance Sheet Credit column.

E. A liability amount entered in the Balance Sheet Debit column.

Laurey’s Pet Emporium purchased equipment on January 1 for $35,000. The equipment

will be used for five years, after which the estimated residual value will be $2,000.

Using straight-line depreciation, what is the depreciation expense for the first year of

the asset’s life?

A. $4,000

B. $5,600

C. $6,600

D. $7,000

E. $7,400

Video Buster had $62 in extra cash at the end of the day. The correct procedure is:

A. Credit Cash for $62.

B. Debit Cash for $62.

C. Credit Cash Over and Short for $62.

D. Debit Cash Over and Short for $62.

E. Debit Petty Cash for $62.

The General Journal is used for:

A. Recording adjusting entries.

B. Posting transactions to special journals.

C. Accumulating debits and credits.

D. Collecting detailed listings of amounts.

E. Recording both adjusting entries and posting transactions to special journals.

Prepaid expenses are:

A. Payments made for economic benefits that never expire.

B. Classified as liabilities on the balance sheet.

C. Generally all combined into one account called “Miscellaneous Expenses”.

D. Assets created by payments for economic benefits that are not used up until later.

E. Always debited to an expense account.

A contingent liability:

A. Is another name for a long term liability.

B. Only arise when accounts receivable are factored.

C. Arise when a note receivable is discounted without recourse.

D. Is an obligation to make a future payment if a certain future event occurs.

E. Is an obligation to make a future payment if an uncertain future event occurs.

If accrued salaries were recorded on December 31 with a credit to Salaries Payable, the

entry to record payment of these wages on January 5 would include:

A. A debit to Cash and a credit to Salaries Payable.

B. A debit to Cash and a credit to Prepaid Salaries.

C. A debit to Salaries Payable and a credit to Cash.

D. A debit to Salaries Payable and a credit to Salaries Expense.

E. No entry would be necessary on January 5.

DVDs usually sell for $14 per unit, and have a profit margin of 25%. However, the

expected selling price has fallen to $7 per unit. The Movie Company’s current inventory

includes 200 units purchased at $10 per unit. Calculate the value of the inventory at the

lower of cost and net realizable value.

A. $1,350.

B. $1,400.

C. $1,500.

D. $1,800.

E. $2,000.

External users of accounting information include:

A. Shareholders.

B. Customers.

C. Creditors.

D. The press.

E. All of these answers are correct.

The assets of a business total $20,000; the liabilities, $8,000. The claims of the owners

are:

A. $0.

B. $8,000.

C. $12,000.

D. $20,000.

E. $28,000.

On September 30, Stark Company needed to estimate its ending inventory in order to

prepare its third-quarter financial statements. The following information is available:

(1) Inventory, July 1: $12,500

(2) Third quarter net sales: $40,000

(3) Third quarter net purchases: $17,500

Stark’s gross profit ratio is 15%. Estimated cost of goods sold would be:

A. $6,000.

B. $34,000.

C. $36,000.

D. $40,000.

E. $57,500.

For a merchandising company using the perpetual inventory system, the second closing

entry closes debit balances in:

A. Sales Discounts.

B. Sales Returns and Allowances.

C. Cost of Goods Sold.

D. Operating Expenses.

E. All of these answers are correct.

Which of the following is an example of a source document?

A. Invoice.

B. Cheque.

C. Bank statement.

D. Employee earnings records.

E. All of these answers are correct.

The sale of inventory may:

A. decrease inventory.

B. impact the Sales Journal.

C. create accounts receivable.

D. initiate billing.

E. All of these answers are correct.

Which statement is incorrect?

A. Revenue accounts are closed to Income Summary.

B. Expense accounts are closed to Income Summary.

C. Income Summary is closed to Capital.

D. Withdrawals are closed to Income Summary.

E. Withdrawals are closed to Capital.

A credit memorandum from the bank may be used as:

A. An explanation for a payment by cheque.

B. A bank statement.

C. A voucher.

D. An EFT.

E. A cancelled cheque.

A 90-day note issued on July 10 matures on:

A. October 7.

B. October 8.

C. October 9.

D. October 10.

E. October 11.

A trial balance prepared after the adjusting and closing entries have been posted, and

which is the final step in the accounting cycle, is a(n):

A. Unadjusted trial balance.

B. Post-closing trial balance.

C. Book of final entry.

D. Adjusted trial balance.

E. Work sheet.

Select the appropriate financial statement for each of the following items.

(a) Income statement

(b) Statement of changes in equity

(c) Balance sheet

(d) Statement of cash flows

______ (1) Supplies

______ (2) Net income

______ (3) Ahmad Khan, Capital

______ (4) Advertising Expense

______ (5) Purchased equipment for cash

______ (6) Withdrawals

______ (7) Fees earned

______ (8) Proceeds received from a loan

Accounts receivable accounts for specific customers are important because they show:

A. How much each customer purchases.

B. How much each customer has paid.

C. How much each customer still owes.

D. The basis for sending bills to customers.

E. All of these answers are correct.

Of the following accounts, the one that normally has a debit balance is:

A. Accounts Payable.

B. Accounts Receivable.

C. Ted Neal, Capital.

D. Sales Revenue.

E. Unearned Revenue.

If an accountant forgot to record depreciation on office equipment at the end of an

accounting period, what is the effect on the statements prepared at that time?

A. Assets are overstated and equity is understated.

B. Assets and equity are both understated.

C. Assets are overstated, net income is understated, and equity is overstated.

D. Assets, net income, and equity are understated.

E. Assets, net income, and equity are overstated.

A business pays each of its two office employees each Friday at the rate of $60 per day

for a five-day week that begins on Monday. If the accounting period ends on Tuesday

and the employees worked on both Monday and Tuesday, the adjusting entry to record

the salaries earned but unpaid is:

A. Debit Unpaid Salaries $120 and credit Salaries Payable $120.

B. Debit Salaries Payable $240 and credit Office Salaries Expense $240.

C. Debit Office Salaries Expense $120 and credit Salaries Payable $120.

D. Debit Office Salaries Expense $240 and credit Salaries Payable $240.

E. Debit Salaries Expense $240 and credit Cash $240.

Understatement of ending inventory causes:

A. Cost of goods sold to be overstated and net income to be understated.

B. Cost of goods sold to be overstated and net income to be overstated.

C. Cost of goods sold to be understated and net income to be understated.

D. Cost of goods sold to be understated and net income to be overstated.

E. Cost of goods sold to be overstated and net income to be accurate.

If the accountant failed to make the end-of-period adjustment to reduce the Unearned

Management Fees account by the amount of management fees earned, the omission

would cause:

A. An overstatement of net income.

B. An overstatement of assets.

C. An overstatement of liabilities.

D. An overstatement of equity.

E. An understatement of expenses.

The full disclosure principle:

A. Requires that when a change in inventory cost flow assumption is made, the notes to

the statements report the type of change.

B. Requires that when a change in inventory cost flow assumption is made, the notes to

the statements report the justification for the change.

C. Requires that any change in net income due to changes in the inventory cost

assumption be disclosed.

D. Does not require a company to use one cost flow assumption exclusively.

E. All of these answers are correct.

The chief accountant was reviewing the financial statements that you had prepared for

the current year with comparative results from last year. She asked you the following

questions.

1. Why is Trucking Expense so high?

2. Why is Supplies Expense so low?

3. Why is Unearned Revenue so high?

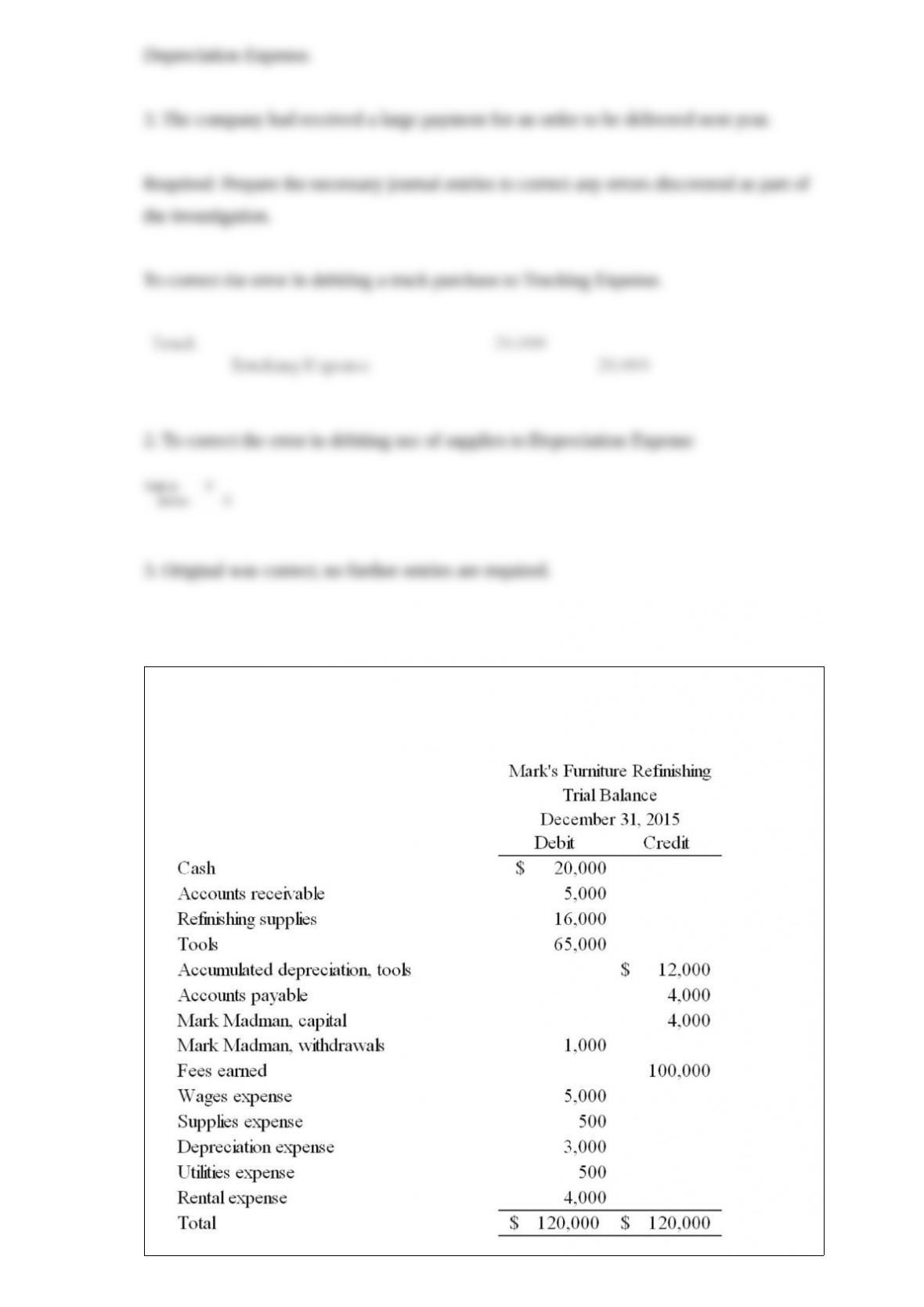

The following are selected accounts and their balances after adjustments at May 31,

2015, the end of Mark’s Furniture Refinishing’s fiscal year.

1. Prepare the necessary closing entries at December 31.

2. What is the balance of Mark’s capital account after the bookkeeper posts the closing

entries?

Accrued revenues at the end of one accounting period often result in cash

_______________________ in the next period.

The expected sales price of an item minus the cost of making the sale is called:

______________.

Shrinkage can be calculated by comparing _______________ of the inventory with

recorded quantities.

Describe the accounting aspects of a periodic inventory system.

Match the following definitions and terms by placing the letter that identifies the best

definition in the blank space next to the term.