A company cannot be increasing its market share if its net sales are declining.

It is not unusual for an entity to report a significant increase in cash from operating

activities, but a decrease in the total amount of cash.

Bonuses may be used to reward employees who meet performance goals.

The two steps required in activity-based costing are identifying separate activity cost

pools and allocating each cost pool to the product using an appropriate cost driver.

Current assets are those assets that are expected to be converted into cash within a

relatively short period of time.

A high interest coverage ratio is a sign of creditworthiness.

Sunk costs are relevant costs when considering a special order.

Assuming that the MR Corporation has an inventory of 200 defective motors costing

$450,000 to produce and $150,000 to repair, the repaired units can be sold for

$425,000. The company receives an offer to purchase these motors for $325,000 before

repairing them. The company’s decision should be to sell the motors at the offered price.

When cost-volume-profit analysis is used, the need for a cost accounting system is

eliminated.

Stock dividends and stock splits do not cause a change in the total amount of

stockholders’ equity.

If a piece of equipment is dropped and damaged during installation, the cost of

repairing the damage should be added to the cost of the equipment.

The systematic write-off of intangible assets to expense is called depletion.

In most process costing systems, the number of units “in process” at any one time is

usually significant relative to the total production output of the period.

The difference between the present value and future value depends on the rate of

interest and the length of time that interest accumulates.

Generally accepted accounting principles were established by the American Accounting

Association in 1934 and are updated annually by Congress.

The average gross profit margin is a measure of relative profitability.

The formula for the double-declining balance method of computing depreciation

expense is: Remaining book value times the straight line rate.

Extraordinary items and the results of discontinued operations are shown in the income

statement net of any related income tax effects.

Vertical analysis compares the results of financial information with a business in the

same industry for a number of consecutive periods of time.

A stockholders’ subsidiary ledger will have entries made for each stockholder showing

the number of shares held.

Sunk costs have already been incurred and cannot be changed by future actions.

In the early years of an asset’s life, an accelerated depreciation method results in a more

conservative balance sheet amount for the asset and a more conservative net income

amount.

The annual net cash flow of an investment refers to the excess revenue it generates over

its related expenses.

“Six Sigma” describes the length of time it takes a product to pass through the 6 stages

of manufacturing, from processing through inspection.

Stockholders of an S corporation pay taxes on their share of the corporate net income

whether they receive it or not.

Investors are individuals and other enterprises that have provided equity to the reporting

enterprise.

To convert a dollar amount into a foreign currency divide the dollar amount by the

exchange rate.

A just-in-time inventory system is dependent on reliability of equipment and production

workers are often trained in how to make routine repairs.

Interest paid belongs in the operating activities section of the statement of cash flows.

Instead of paying for merchandise purchased on account, Olympic Corp. returned this

merchandise to the supplier. Olympic should record this transaction by debiting

Accounts Payable and crediting Sales Returns and Allowances.

Comprehensive income is a component of net income.

Materiality is determined by the Financial Accounting Standards Board.

The adjusted trial balance contains income statement accounts and balance sheet

accounts, while the after-closing trial balance will only have balance sheet accounts.

Metalworks Incorporated purchased $54,500 worth of direct materials to be used in Job

#222. During the accounting period, Job #222 used $45,600 of direct materials. The

amount of direct materials that would be shown in Job #222 Job Cost Sheet at the end

of the accounting period should be $54,500, since this is the amount of direct materials

the company had purchased for this particular job.

In cost-volume-profit analysis, the number of units sold is assumed to be equal to the

number of units produced.

An accounting system designed to measure the performance of each center within a

business is referred to as a profitability accounting system.

The recognition of depreciation expense often causes the annual net income of an

investment to be less than the amount of its annual net cash flows.

The balance in the Retained Earnings account that appears on the adjusted trial balance

is the same as the balance of the Retained Earnings account that is reported on the

balance sheet.

Under the indirect method, depreciation, increase in inventories, and “non-operating”

losses are added to net income to arrive at net cash flow from operating activities.

When direct materials are applied to the production process, materials inventory is

debited and work in process is credited.

A product cost is deducted from revenue in the period in which:

A. The related finished goods are sold.

B. The expenditure is made.

C. The production of the product begins.

D. The production process is completed.

For the last several years Conway Corporation has operated with a gross profit rate of

40%. On January 1 of the current year, the company had on hand inventory with a cost

of $600,000. Purchases of merchandise during January amounted to $150,000, and sales

for the month were $360,000. Using the gross profit method, what is the estimated

inventory at January 31?

A. $144,000.

B. $216,000.

C. $360,000.

D. $534,000.

Goods in transit between the buyer and the seller belong to:

A. The seller.

B. The buyer.

C. The freight company.

D. The answer depends upon whether the goods were shipped F.O.B. shipping point or

F.O.B. destination.

Soriano Company had net sales of $300,000 for the month (after returns and allowances

of $1,500 and sales discounts of $3,250). Beginning inventory for the month was

$60,000; purchases for the month were $175,000; and gross profit was 43%.

Refer to the information above. What were the gross sales for the month?

A. $129,000.

B. $171,000.

C. $300,000.

D. $304,750.

The purpose of adjusting entries is to:

A. Prepare the revenue and expense accounts for recording the revenue and expenses of

the next accounting period.

B. Record certain revenue and expenses that are not properly measured in the course of

recording daily routine transactions.

C. Correct errors made during the accounting period.

D. Update the owners’ equity account for the changes in owners’ equity that had been

recorded in revenue and expense accounts throughout the period.

Transactions are recorded in the general journal in:

A. Numerical order.

B. Chronological order.

C. Account number order.

D. Financial statement order.

In a manufacturing company, the cost of goods sold is equal to:

A. The beginning inventory of finished goods, plus net purchases, less the ending

inventory of finished goods.

B. The sum of the manufacturing costs charged (debited) to the Work in Process

Inventory account during the period.

C. The costs of direct materials, direct labor, and manufacturing overhead incurred in

manufacturing the goods sold during the period.

D. The beginning inventory of Work in Process, plus total manufacturing costs for the

period, less the ending inventory of Work in Process.

Refer to the information above. A statement of cash flows for August, would report an

increase in cash of:

A. $26,000.

B. $32,400.

C. $40,000.

D. $46,400.

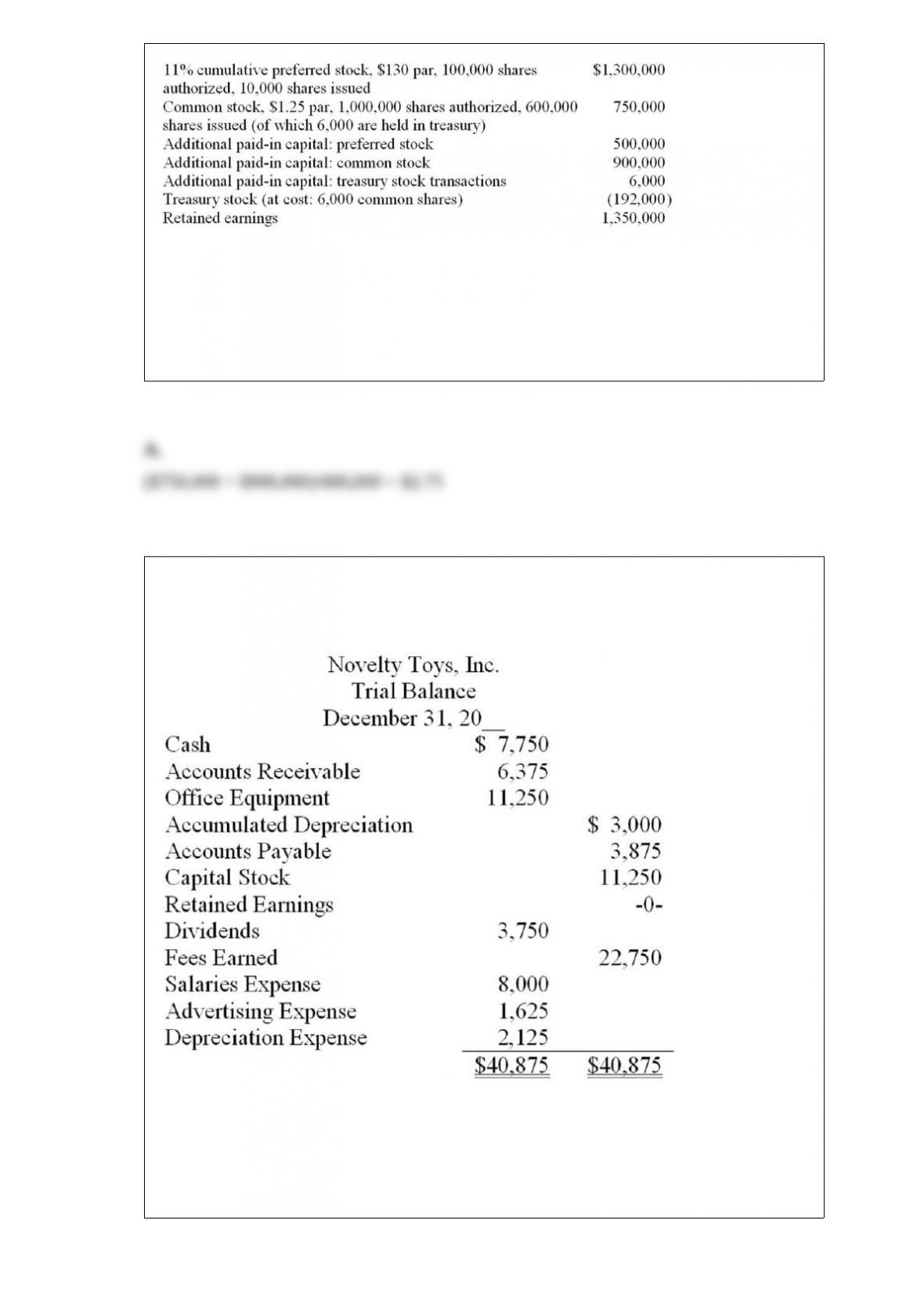

Shown below is information relating to the stockholders’ equity of Brookdale

Corporation at December 31, 2015:

Refer to the information above. What was the average issue price per share of common

stock?

A. $2.75 per share

B. $1.25 per share

C. $1.50 per share

D. $3.75 per share

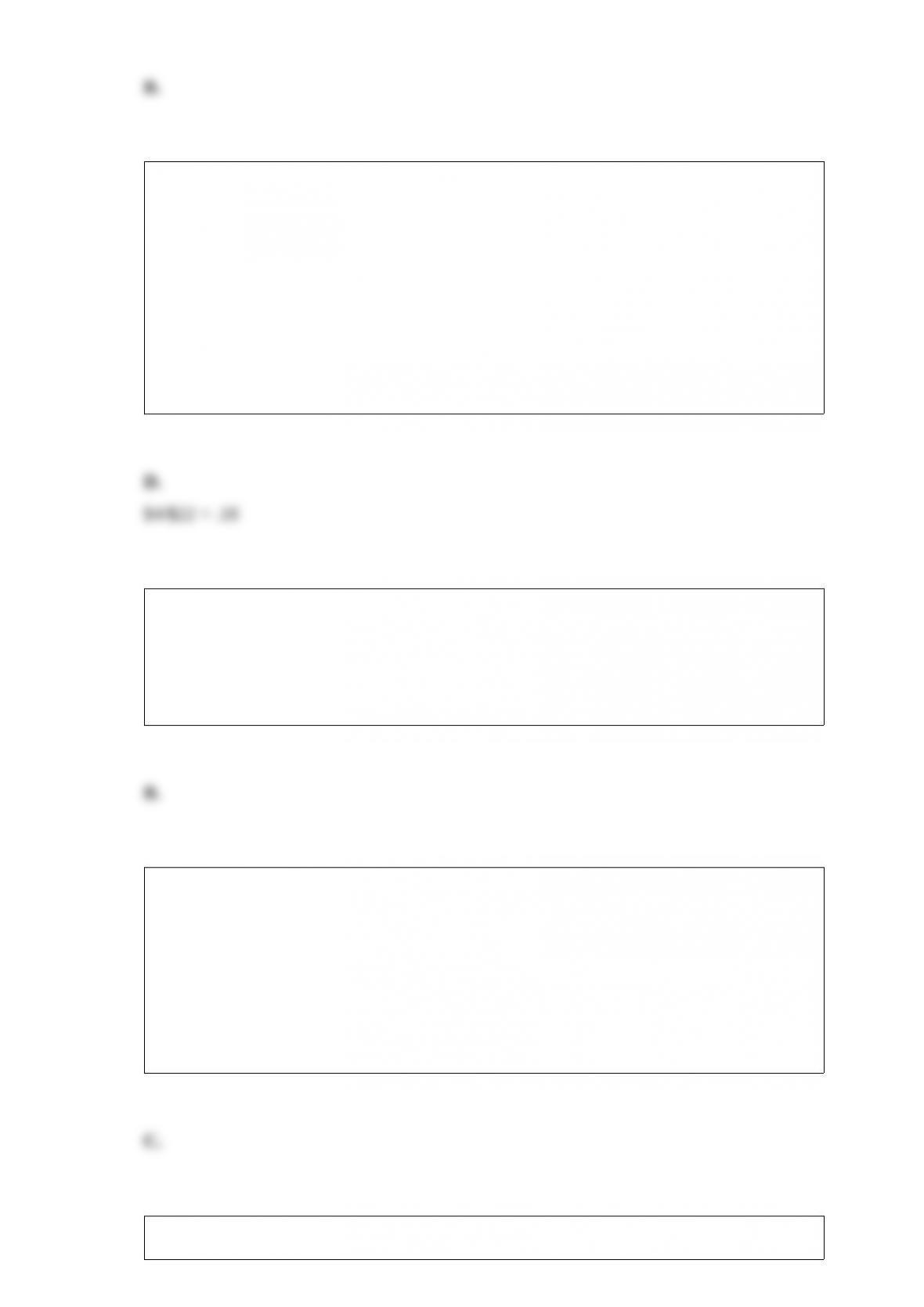

Shown below is a trial balance for Novelty Toys Inc., on December 31, after adjusting

entries:

Refer to the information above. The entry to close Salaries Expense account will:

A. Transfer the total of Salaries Expense directly to Retained Earnings.

B. Include a debit to Income Summary.

C. Include a debit to Salaries Expense.

D. Include a credit to Capital Stock.

The current balance sheet of Apex reports total assets of $20 million, total liabilities of

$2 million, and owners’ equity of $18 million. Apex is considering several financing

possibilities in order to expand operations. Each question based on this data is

independent of any others.

Refer to the information above. Assume Apex borrows $2 million to finance its

expansion. Apex’s debt ratio immediately after the borrowing will be:

A. .10.

B. .20.

C. .33 (rounded).

D. .18 (rounded).

Which account will appear on an After-Closing Trial Balance?

A. Dividends.

B. Prepaid Expenses.

C. Retained Earnings, at the beginning of the period.

D. Sales.

An accounting principle must receive substantial authoritative support to qualify as

generally accepted. Among the organizations and agencies that have been influential in

the development of generally accepted accounting principles, which of the following

has provided the most influential leadership?

A. Internal Revenue Service.

B. Institute of Management Accountants.

C. Financial Accounting Standards Board.

D. New York Stock Exchange.

During the current year, Jules Company incurred the following product costs:

Direct materials used in production $250,000

Direct labor $185,000

Manufacturing overhead $245,500

Jules Company’s beginning Work in Process Inventory was $20,000 and its ending

Work in Process Inventory amounted to $30,000. What is the company’s cost of

finished goods manufactured for the year?

A. $700,500.

B. $690,500.

C. $670,500.

D. $430,500.

During the month of June, $352,150 of costs were transferred from Department A to

Department B. The journal entry to summarize the transfer of these costs includes:

A. A debit to department A for $352,150.

B. A credit to department B for $352,150.

C. A credit to department A for $352,150.

D. No entry is required when costs are transferred between departments.

In either a job order or a process costing system, credits to the Materials Inventory

account represent:

A. The cost of materials purchased during the period.

B. The cost of materials relating to finished goods.

C. The cost of unused materials returned to the inventory.

D. The cost of materials placed into production.

Which of the following will not cause a change in the owners’ equity of a business?

A. Purchase of land with cash.

B. Withdrawal of cash by the owner.

C. Sale of land at a profit.

D. Losses from unprofitable operations.

Total owners’ equity = $360,000 (capital stock issued)

-The following transactions occurred during May, the first month of operations for

Hunter Products, Inc.:

* Issued 50,000 shares of capital stock to the owners of the corporation in exchange for

$600,000 cash.

* Purchased a piece of land for $400,000, making a $150,000 cash down payment and

signing a note payable for the balance.

* Made a $60,000 cash payment on the note payable from the purchase of land.

* Purchased equipment on credit from BBW, Inc. for $63,000.

Refer to the information above. What is the total of Hunter Products’ liabilities at the

end of May?

A. $253,000.

B. $190,000.

C. $63,000.

D. $313,000.

A strong internal control structure:

A. Contributes to the accuracy and verifiability of the accounting records.

B. Will prevent a business from operating at a loss.

C. Assures that a business will remain solvent.

D. Will prevent fraud, theft, and embezzlement.

Depreciation on the factory would be an example of a:

A. Controllable fixed cost.

B. Period cost.

C. Responsibility cost.

D. Committed fixed cost.

Until the related goods are sold, product costs are viewed as:

A. Assets.

B. Liabilities.

C. Operating expenses.

D. Manufacturing overhead.

If manufacturing overhead is materially over-applied, it is best to close it to:

A. Work-in-process inventory.

B. Finished goods inventory.

C. Cost of goods sold.

D. Apportioned among work-in-process, finished goods, and cost of goods sold.

Generally accepted accounting principles are the “ground rules” used in the preparation

of:

A. Income tax returns.

B. All accounting reports.

C. Reports to federal and state regulatory agencies.

D. Financial statements.

Which of the following inventory approaches is not in accord with the physical flow of

merchandise in most businesses?

A. LIFO.

B. FIFO.

C. Specific identification.

D. Average cost.

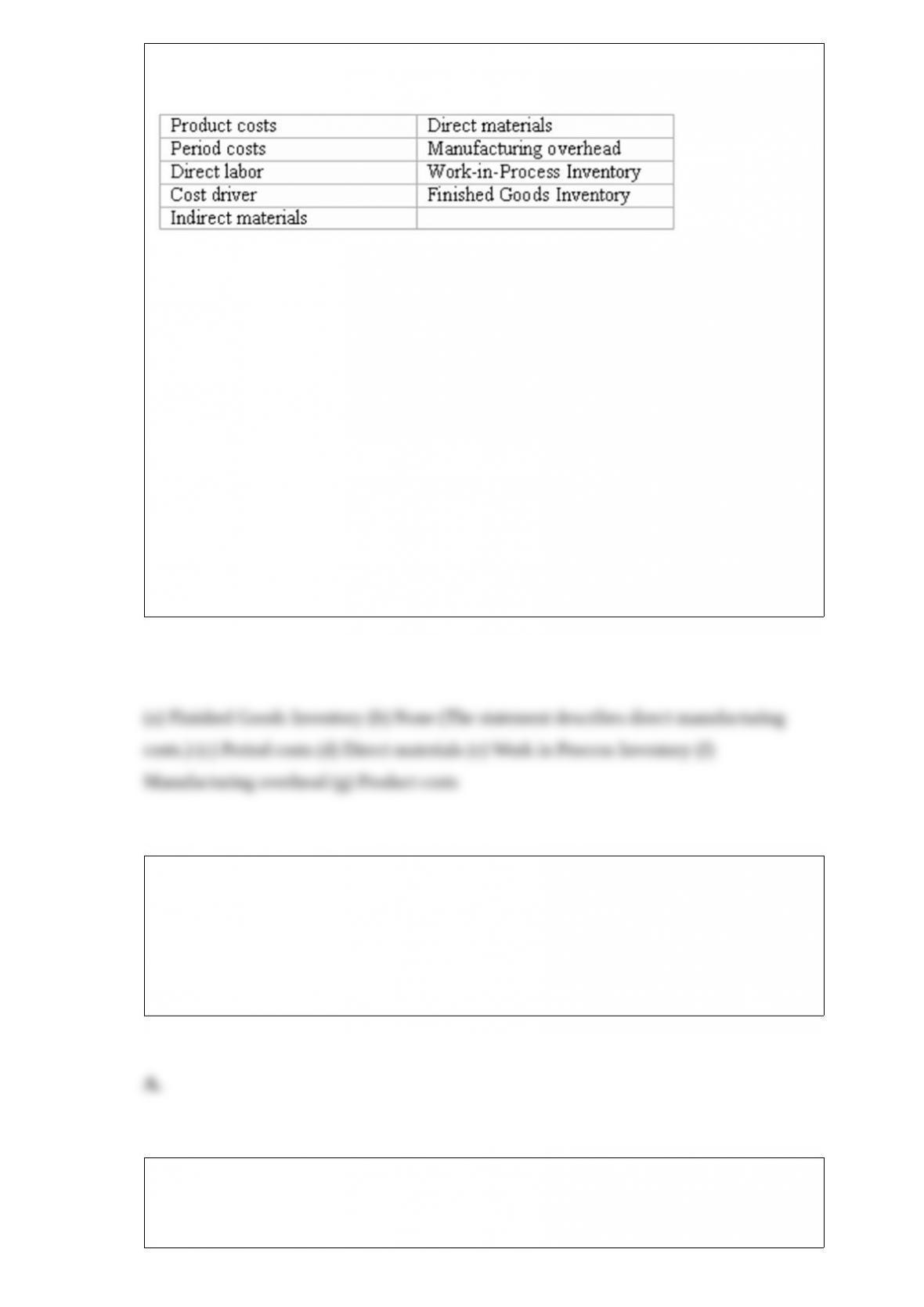

Accounting terminology

Listed below are nine technical accounting terms introduced or emphasized in this

chapter:

Each of the following statements may (or may not) describe one of these technical

terms. In the space provided, indicate the accounting term described, or answer “None”

if the statement does not correctly describe any of the terms.

____ (a) The account that is debited when the Work in Process Inventory account is

credited.

____ (b) A term describing any manufacturing cost that can be traced conveniently and

directly to the various types of products being manufactured.

____ (c) Costs that are charged directly to expense accounts at the time that the costs

are incurred.

____ (d) The category of manufacturing cost that would include the cost of tires used in

the manufacture of automobiles.

____ (e) An account which has a balance that is increased by manufacturing costs

incurred during the period and decreased by the cost of finished goods manufactured.

____ (f) The category of manufacturing cost that includes the salaries of plant guards,

supervisors, and maintenance personnel.

____ (g) A term describing all three categories of manufacturing costs.

The measures most often used in evaluating solvency—the current ratio, quick ratio,

and amount of working capital—are developed from amounts appearing in the:

A. Balance sheet.

B. Income statement.

C. Statement of retained earnings.

D. Statement of cash flows.

Amounts credited to the Work in Process inventory account may best be described as:

A. The cost of finished goods manufactured.

B. Total manufacturing costs charged to production.

C. The cost of goods sold.

D. Direct materials purchased, direct labor costs paid, and payments for items classified

as manufacturing overhead.

Treasury stock represents:

A. Shares of ownership in the United States Treasury Department.

B. A current asset.

C. Authorized shares that have never been issued.

D. Previously outstanding shares that have been repurchased by the issuing company.

The president of Nash Company is considering a proposal by the factory manager for

the purchase of a machine for $72,500. The useful life would be eight years, with no

residual scrap value. The use of the machine will produce a positive annual cash flow of

$14,000 a year for eight years. An annuity table shows that the present value of $1

received annually for eight years and discounted at 10% is 5.335. The net present value

of the proposal, discounted at 10%, is:

A. $2,190.

B. Zero.

C. ($3,868).

D. $3,868.

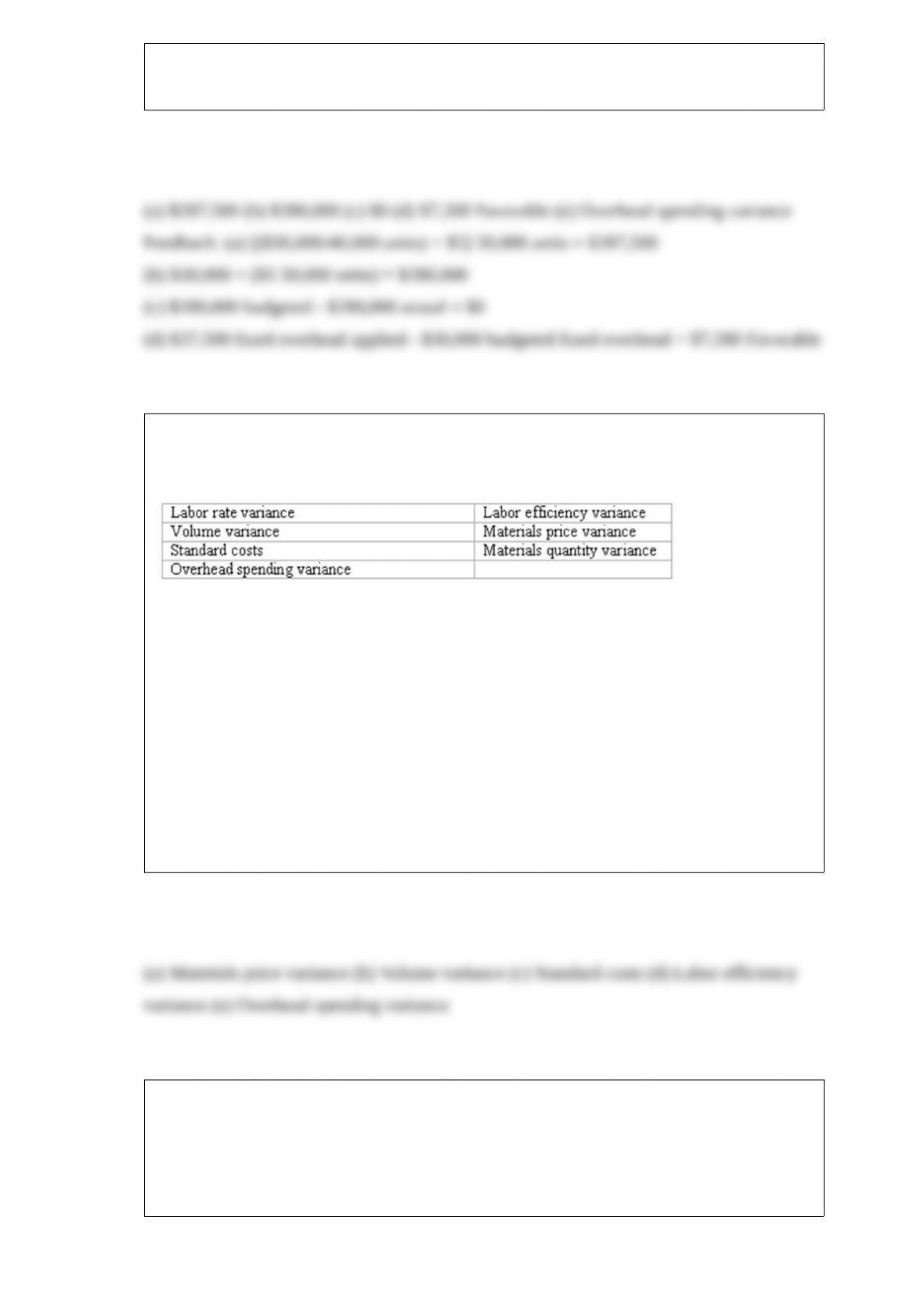

Standard cost system overhead variances

Rogers Manufacturing produces a component part used throughout the computer

industry. Variable overhead is allocated to production at a rate of $5 per unit. The

company’s monthly fixed overhead costs average $30,000. Normal output levels

average 40,000 units per month. During April, Rogers produced 50,000 units and

incurred actual overhead costs of $280,000.

(a) Total overhead applied to production in April amounted to $__________.

(b) Total overhead budgeted in April for the level of output achieved amounted to

$__________.

(c) April’s overhead spending variance was $__________ (favorable/unfavorable).

(d) April’s overhead volume variance was $__________ (favorable/unfavorable).

(e) For which of Rogers’ two overhead variances is the production manager held

responsible?

Accounting terminology

Listed below are seven technical accounting terms introduced or emphasized in this

chapter:

Each of the following statements may (or may not) describe one of these technical

terms. In the space provided beside each statement, indicate the accounting term

described, or answer “None” if the statement does not correctly describe any of the

terms.

____ (a) A materials variance which is the responsibility of the Purchasing Department.

____ (b) The variance which exists whenever actual production levels differ from

normal levels.

____ (c) Unit costs expected to be incurred under normal conditions.

____ (d) A labor variance caused by a difference between standard and actual hours

required to complete a task.

____ (e) The variance caused by incurring more overhead costs than allowed for at a

given level of production.

Generally Accepted Accounting Principles

The accounting department of Burke Manufacturing prepares numerous reports at the

request of, and for exclusive use by, the management of the company. Is it necessary

that these managerial accounting reports be developed in accordance with generally

accepted accounting principles (GAAP)?

Net sales and gross profit

Mayflower Supply House had gross sales revenue of $1,700,000, cost of goods sold of

$950,000, sales returns and allowances of $52,500, and allowed sales discounts of

$30,000.

Compute for the year:

Redman Company is considering an investment in new machinery. The details of the

investment are as follows:

The company uses straight-line depreciation for its machinery and requires a 12% rate

of return. The present value of $1 for 4 years at 12% is 0.636. The present value of an

ordinary annuity for $1 for 4 years at 12% is 3.037.

(1) What is the payback period? (Round your answer to one decimal place.)

(2) What is the rate of return on average investment? (Round your percentage to one

decimal place.)

(3) What is the net present value?

(4) Would you advise the company to invest in this machinery?

The common stock of Securetech Corporation consistently sells at a market price of 20

times earnings (i.e., at a p/e ratio of 20). What would be the most likely effect of a 10

cent increase in Securetech’s basic EPS?