A company purchases software; it has an estimated useful life of three years. The

adjustment to recognize amortization for the use of software would cause which of the

following?

A) An increase in liabilities, an increase in expenses, and a decrease in stockholders’

equity

B) A decrease in assets, a decrease in stockholders’ equity, and an increase in expenses

C) A decrease in assets, an increase in liabilities, and an increase in expenses

D) An increase in assets, an increase in liabilities, and a decrease in expenses

Which of the following would be in the raw materials inventory of a company making

cheese?

A) Milk and cream used to make the cheese

B) Cheese that has been made but is curing before being ready to sell

C) Cured cheese that is waiting to be shipped to retailers

D) Partially processed cheese

Which of the following statements best describes a contingent liability?

A) The amount of a contingent liability is known and will definitely have to be paid in

the future.

B) A contingent liability is a potential liability that has arisen because of a past

transaction or event, but its ultimate outcome will not be known until a future event

occurs or fails to occur.

C) A contingent liability will only be incurred if a particular future event takes place.

D) A contingent liability is a potential liability that will be incurred if a natural disaster

happens.

A company originally issues 180,000 shares of stock at a price of $22; one year later the

stock price is $40 per share, the number of outstanding shares is unchanged, and the

company’s net income for the year is $230,400. The P/E ratio at the end of the recent

year is:

A) 0.0002.

B) 24.22.

C) 31.25.

D) 0.0001.

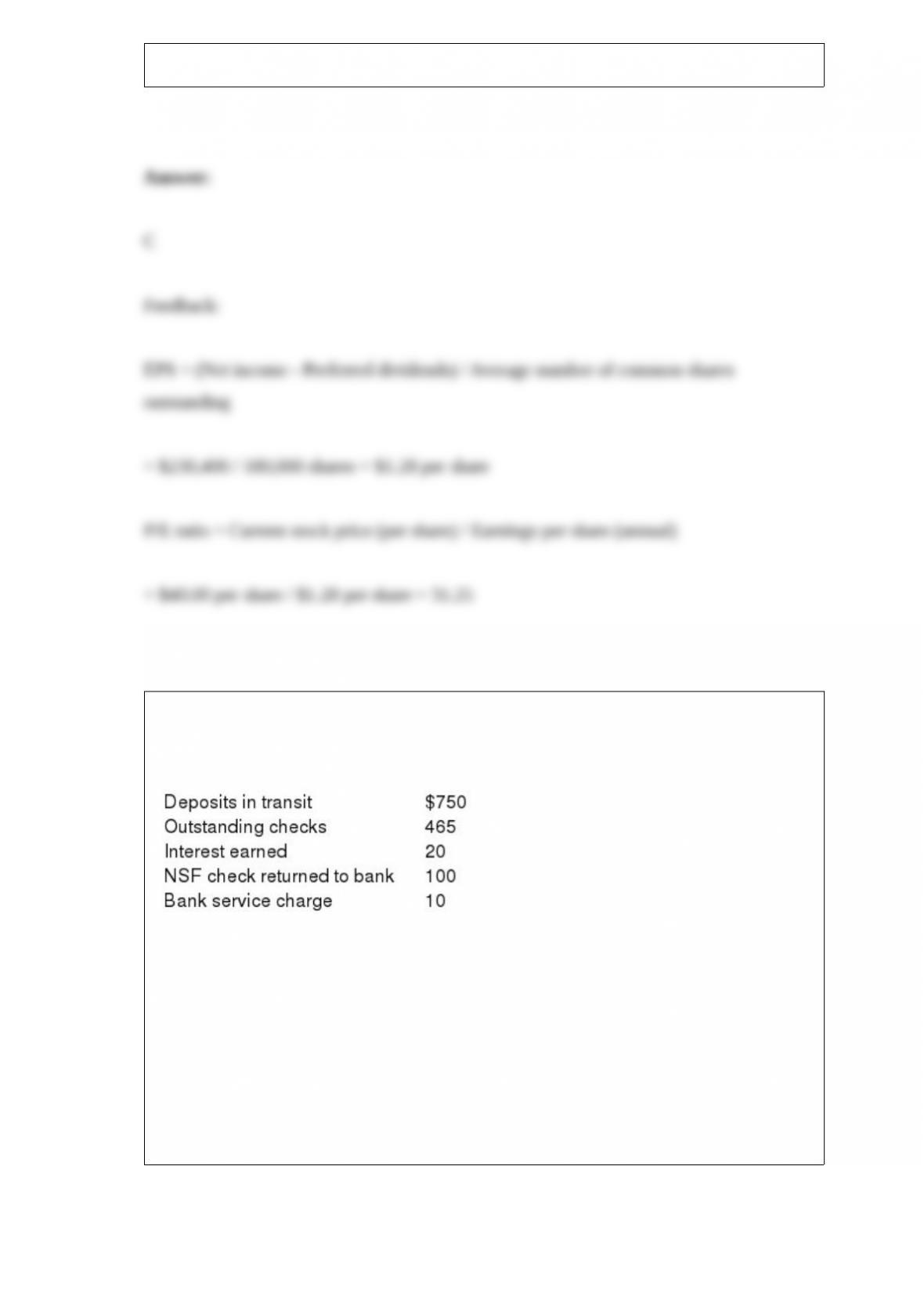

Before reconciling its bank statement, Lauren Cosmetics Corporation’s general ledger

had a month-end balance in the cash account of $5,250. The bank reconciliation for the

month contained the following items:

Given the above information, what up-to-date ending cash balance should Lauren report

at month-end?

A) $4,500

B) $4,820

C) $5,160

D) $5,590

Goodwill

A) is not amortized, but is tested annually for impairment.

B) is amortized using the straight-line method.

C) is amortized using the units-of-production method.

D) is not amortized and is not tested for impairment.

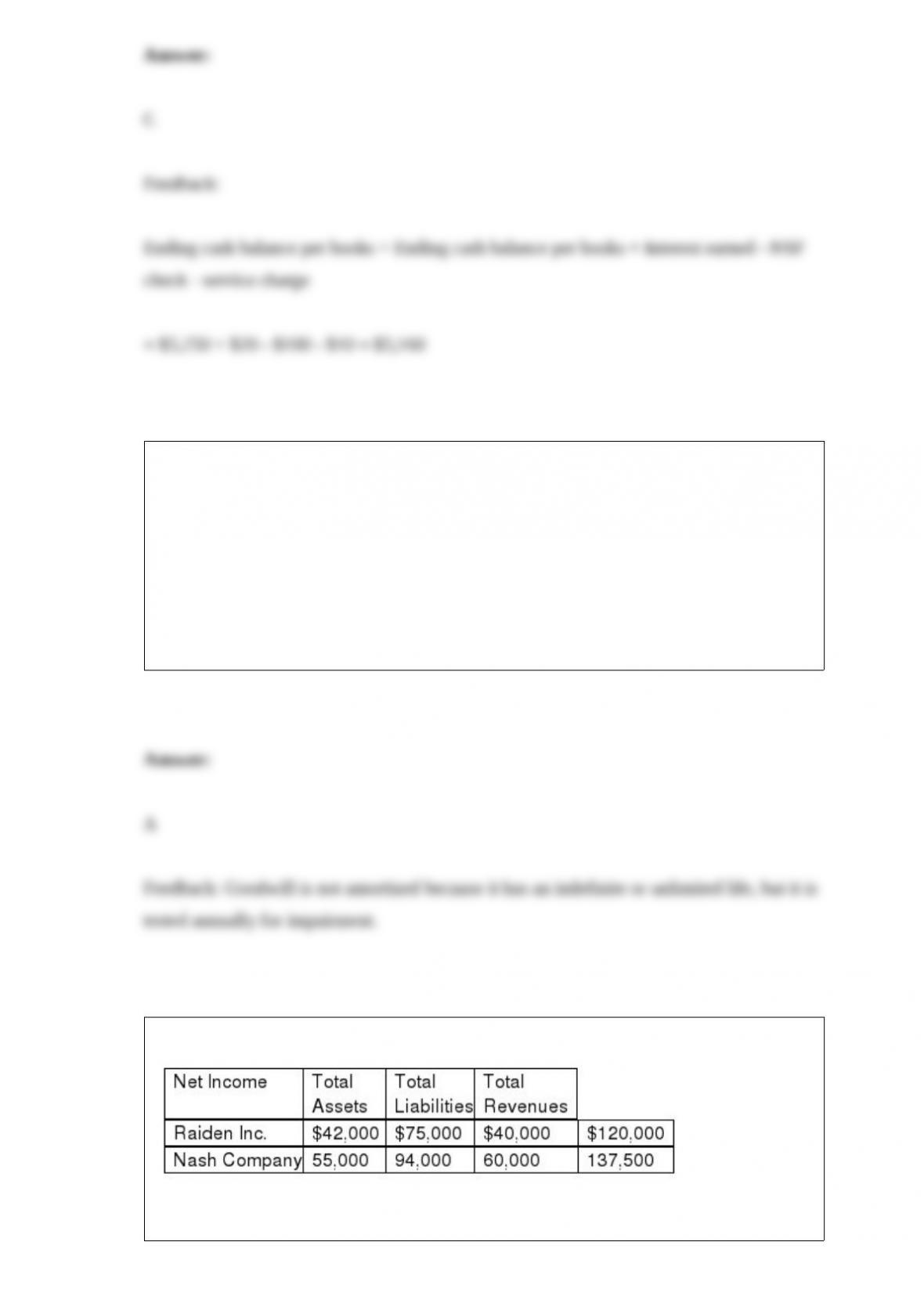

The following amounts were reported by the two companies:

Required:

Part a. Calculate each company’s net profit margin expressed as a percent.

Part b Which company has generated a greater return of profit from each revenue

dollar?

The entry to record a recovery causes:

A) an increase in net accounts receivable.

B) a decrease in net accounts receivable.

C) net accounts receivable to stay the same.

D) an increase in total revenues.

Company X has a P/E ratio of 16 in year 2013 and 16.5 in 2014. In 2015, its P/E ratio is

24. The best way to interpret these data is to conclude that:

A) the stock is overpriced and should be sold.

B) the stock has great growth capacity and should be bought.

C) other financial results and news should be examined to determine the cause of the

P/E ratio change.

D) the stock is underpriced and should be bought.

Langston Company updates its inventory periodically. The company ‘s cost of goods

sold was $2,700 and purchases were $5,600 during the year. The company ‘s ending

inventory count was $5,000. What was the amount of beginning inventory?

A) $3,300

B) $13,300

C) $7,900

D) $2,100

Financial statements are most commonly prepared:

A) daily.

B) monthly, quarterly and annually.

C) as needed.

D) weekly.