Average accumulated expenditures:

a. Is an approximation of the average debt a firm would have outstanding if it financed

all construction through debt.

b. Is computed as a simple average if all construction expenditures are made at the end

of the period.

c. Are irrelevant if the company’s total outstanding debt is less than total costs of

construction.

d. All of these answer choices are true statements.

On January 1, 2016, an investor paid $291,000 for bonds with a face amount of

$300,000. The contract rate of interest is 8% while the current market rate of interest is

10%. Using the effective interest method, how much interest income is recognized by

the investor in 2017 (assume annual interest payments and amortization)?

a. $23,280.

b. $25,140.

c. $29,100.

d. $29,610.

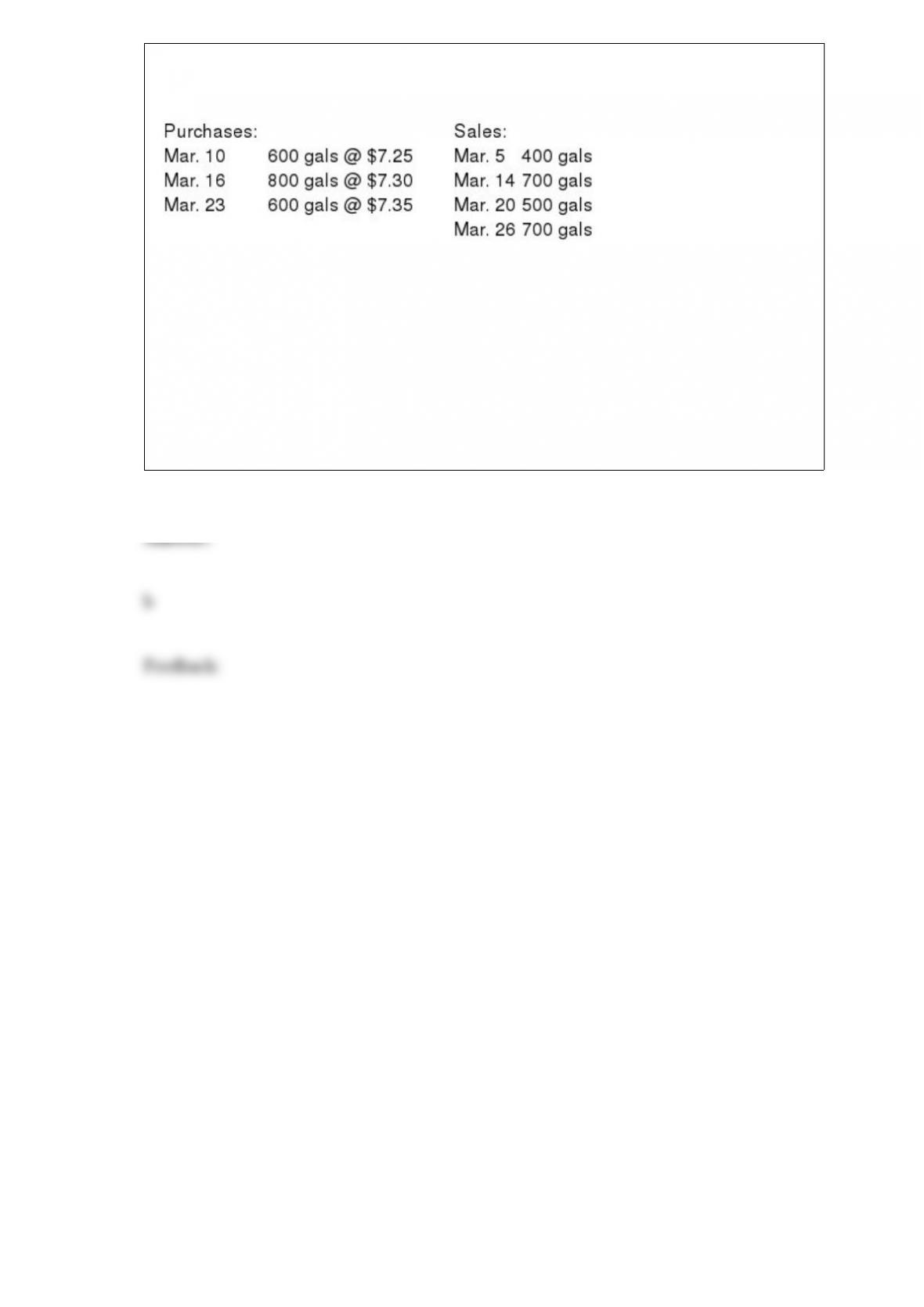

Inventory records for Herb’s Chemicals revealed the following: March 1, 2016,

inventory: 1,000 gallons @ $7.20 = $7,200

Ending inventory assuming LIFO in a perpetual inventory system would be:

a. $4,960.

b. $5,060.

c. $5,080.

d. $5,140.

Stock options do not affect the calculation of:

a. Diluted EPS.

b. Weighted-average common shares.

c. The denominator in the diluted EPS fraction.

d. Basic EPS.

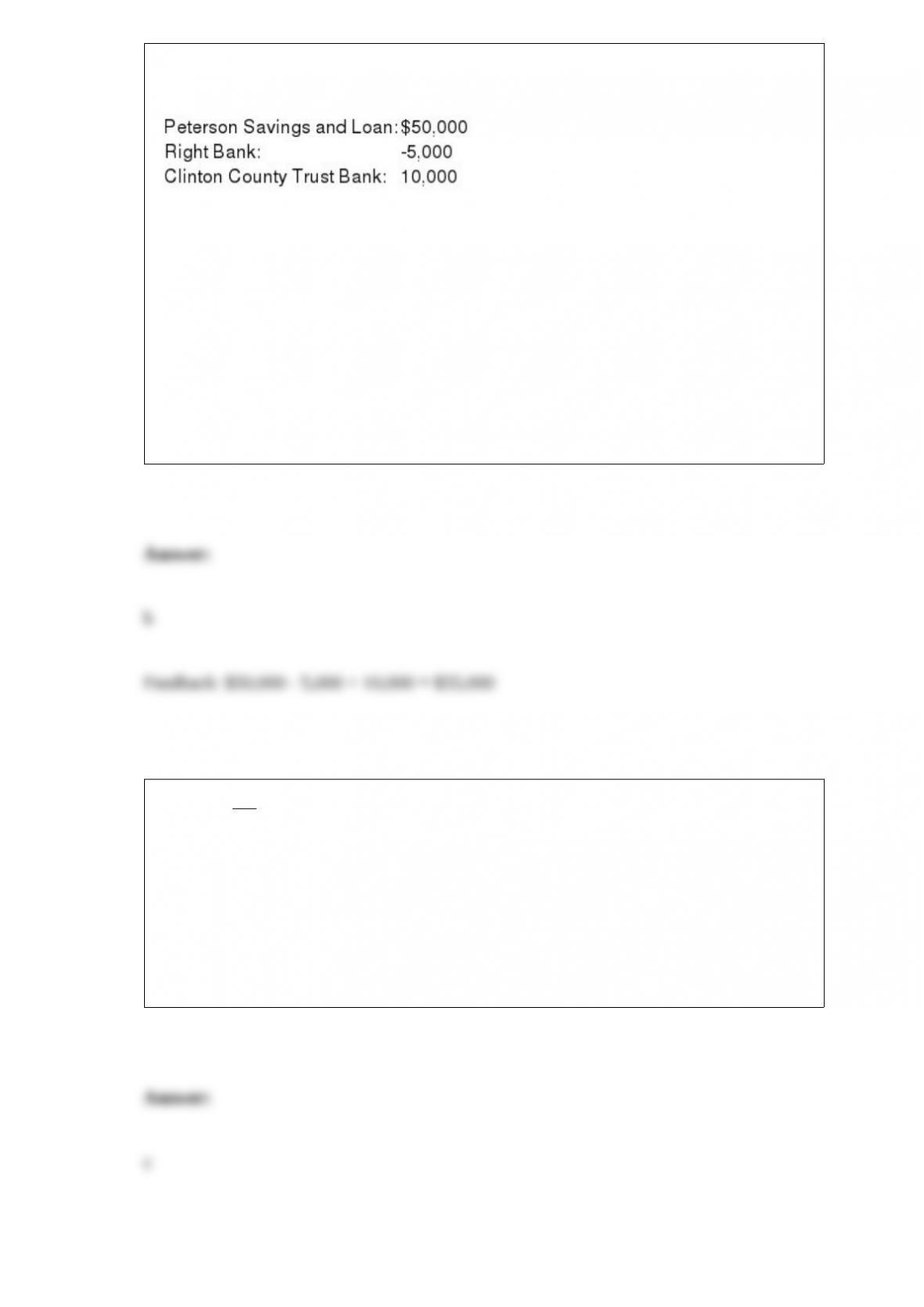

Wilson Company had the following cash balance items listed in its trial balance at

12/31/2016:

If Wilson reports under IFRS, its 12/31/2016 balance sheet would show what cash

balance?

a. ($5,000).

b. $55,000.

c. $60,000.

d. None of these answer choices are correct.

Interest is not capitalized for:

a. Assets that are constructed as discrete projects for sale or lease.

b. Assets constructed for a company’s own use.

c. Inventories routinely and repetitively produced in large quantities.

d. Interest is capitalized for all of these items.

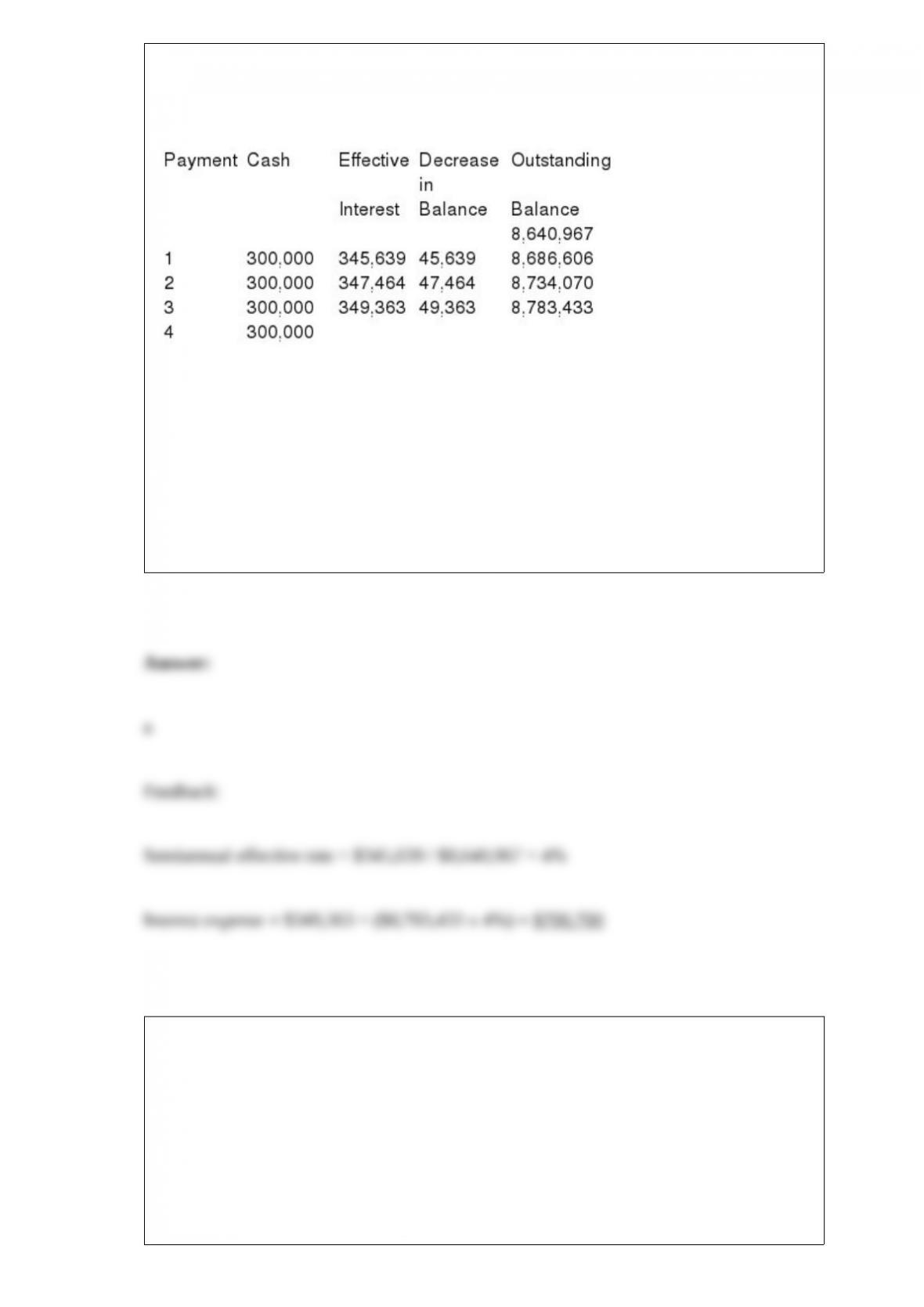

Discount-Mart issued ten thousand $1,000 bonds on January 1, 2016. The bonds have a

10-year term and pay interest semiannually. This is the partial bond amortization

schedule for the bonds.

What is the interest expense on the bonds in 2017?

a. $700,700.

b. $600,000.

c. $347,464.

d. $100,700.

Oklahoma Oil Corp. paid interest of $785,000 during 2016, and the interest payable

account decreased by $125,000. What was interest expense for the year?

a. $910,000.

b. $660,000.

c. $555,000.

d. $785,000.

Which of the following statements is true regarding share appreciation rights (SAR)

payable in cash?

a. Any change in estimated total compensation is recorded as a prior adjustment.

b. The total amount of compensation is not known for certain until the date the SAR is

exercised.

c. The liability is adjusted only to reflect each additional year of service.

d. None of these answer choices is correct.

Archie Co. purchased a framing machine for $45,000 on January 1, 2016. The machine

is expected to have a four-year life, with a residual value of $5,000 at the end of four

years. Using the straight-line method, depreciation for 2016 and book value at

December 31, 2016, would be:

a. $10,000 and $30,000.

b. $11,250 and $28,750.

c. $10,000 and $35,000.

d. $11,250 and $33,750.

The key elements of a defined benefit pension plan include all of the following except:

a. The pension expense.

b. The plan assets.

c. Amortized future benefits.

d. The employer’s obligation.

Which of the following is a change in estimate?

a. A change from the full costing method in the extractive industries.

b. A change from LIFO to FIFO inventory costing.

c. Consolidating a subsidiary for the first time.

d. A change in the termination rate of employees under a pension plan.

A change in the residual value of equipment is accounted for:

a. As a prior period adjustment.

b. Prospectively.

c. Retrospectively.

d. None of these answer choices is correct.

When there is agreement between a measure or description and the phenomenon it

purports to represent, information possesses which characteristic?

a. Verifiability.

b. Predictive value.

c. Faithful representation.

d. Timeliness.

Cutter Enterprises purchased equipment for $72,000 on January 1, 2016. The equipment

is expected to have a five-year life and a residual value of $6,000. Using the

double-declining balance method, depreciation for 2016 and the book value at

December 31, 2016, would be:

a. $26,400 and $45,600.

b. $28,800 and $43,200.

c. $28,800 and $37,200.

d. $26,400 and $36,600.

In a perpetual average cost system:

a. A new weighted-average unit cost is calculated each time additional units are

purchased.

b. The cost allocated to ending inventory is generally the same as it would be in a

periodic inventory system.

c. The moving-average unit cost is determined following each sale.

d. The average is determined by dividing the total number of units sold by the cost of

units purchased during the period.

When a change in accounting principle is reported, what is sometimes sacrificed?

a. Relevance.

b. Consistency.

c. Conservatism.

d. Representational faithfulness.

Slotnick Chemical received customer deposits on returnable containers in the amount of

$300,000 during 2016. Fifteen percent of the containers were not returned. The deposits

are based on the container cost marked up 20%. How much profit did Slotnick realize

on the forfeited deposits?

a. $0.

b. $7,500.

c. $9,000.

d. $45,000.

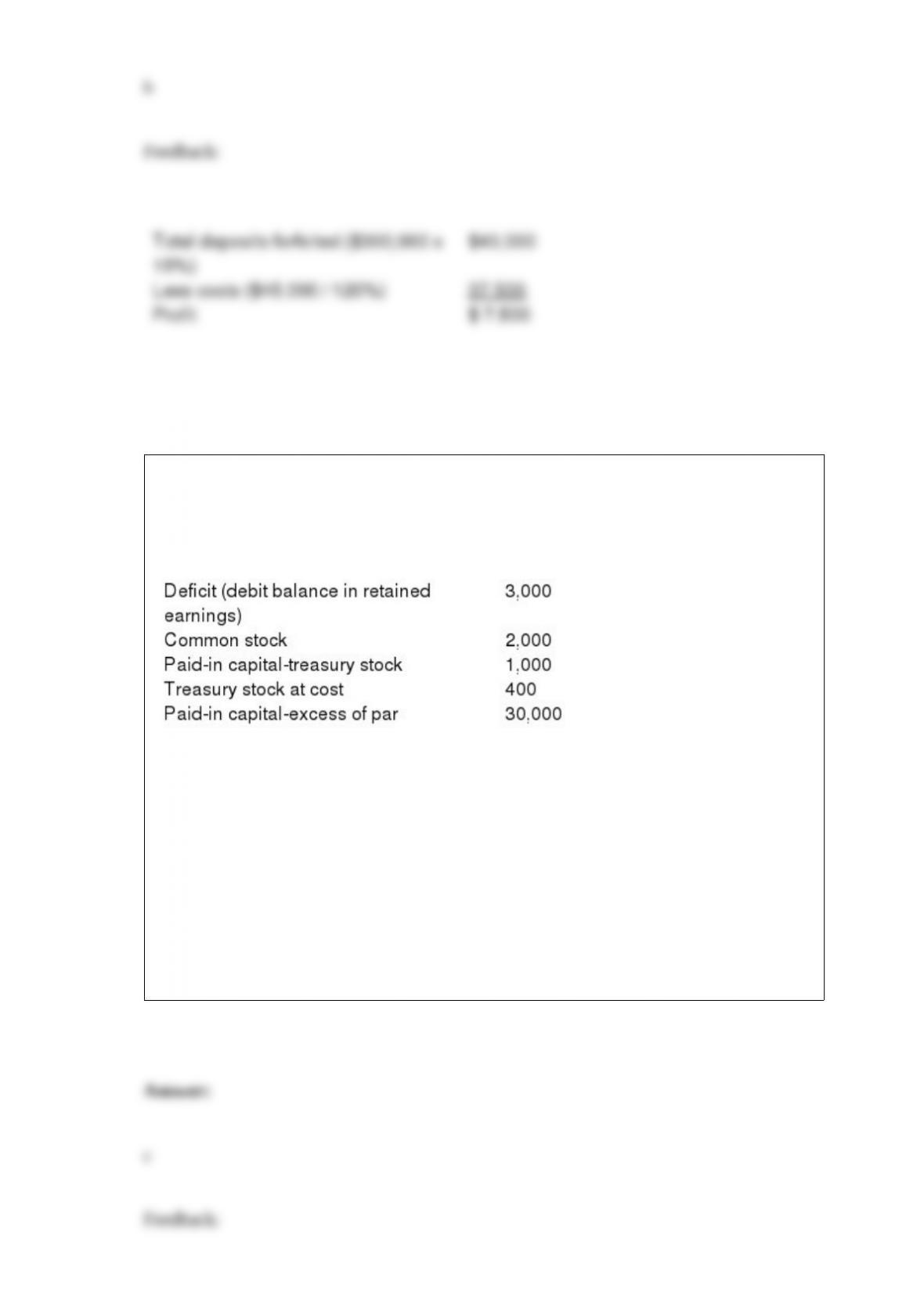

What ($ in 000s) was shareholders’ equity as of December 31, 2017?

Yellow Enterprises reported the following ($ in 000s) as of December 31, 2016. All

accounts have normal balances.

During 2017 ($ in 000s), net income was $9,000; 25% of the treasury stock was resold

for $450; cash dividends declared were $600; cash dividends paid were $500.

a. $38,100.

b. $37,450.

c. $38,450.

d. $38,350.

Auerbach Inc. issued 4% bonds on October 1, 2016. The bonds have a maturity date of

September 30, 2026 and a face value of $300 million. The bonds pay interest each

March 31 and September 30, beginning March 31, 2017. The effective interest rate

established by the market was 6%. Assuming that Auerbach issued the bonds for

$255,369,000, what would the company report for its net bond liability balance after its

first interest payment on March 31, 2017, rounded up to the nearest thousand?

a. $252,369,000.

b. $256,369,000.

c. $256,300,000.

d. $257,030,000.

How do U.S. GAAP and International Financial Reporting Standards (IFRS)differ with

respect to accounting for convertible debt?

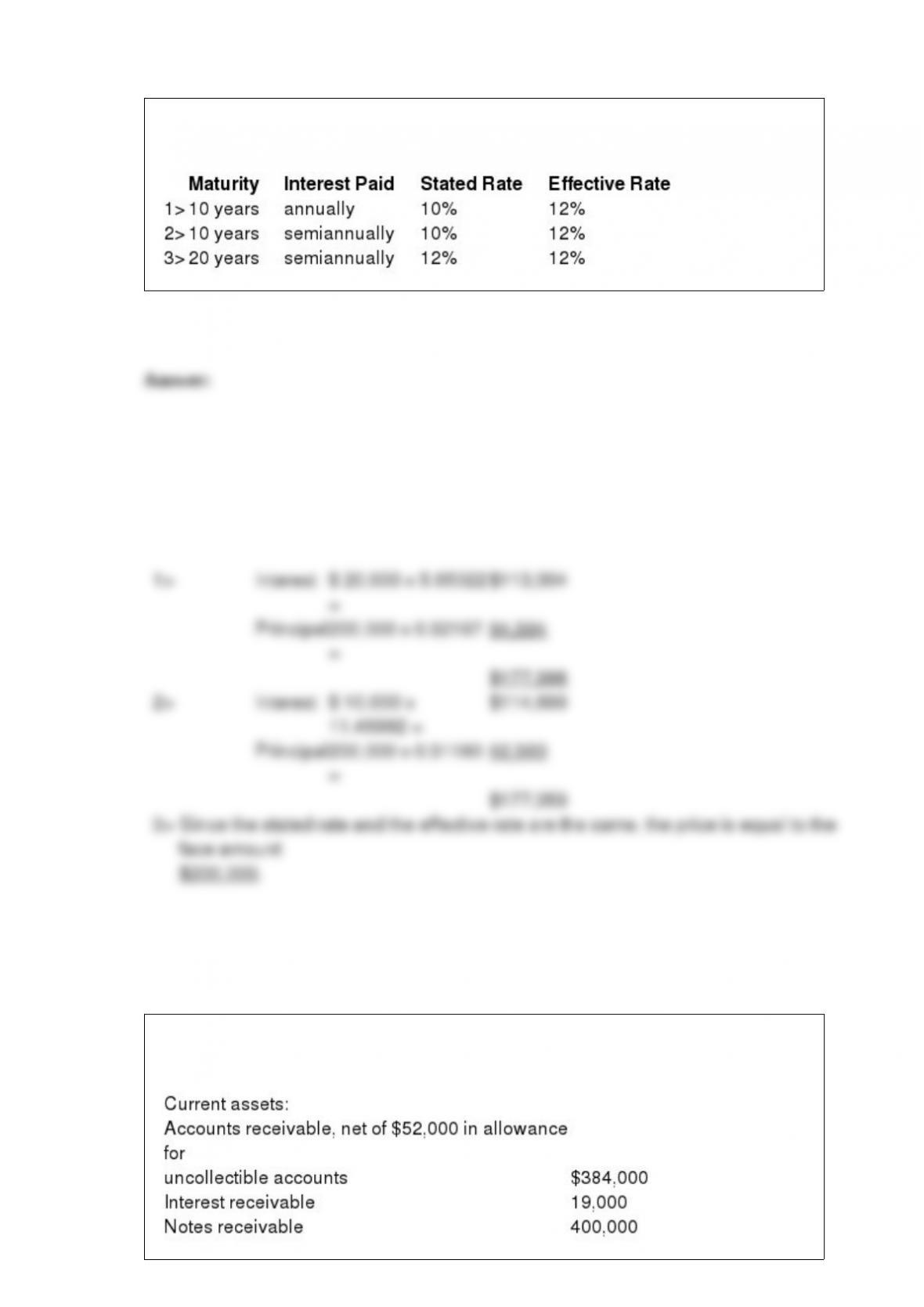

Determine the price of a $200,000 bond issue under each of the following independent

assumptions:

Cordova, Inc., reported the following receivables in its December 31, 2015, year-end

balance sheet:

Additional information:

1> The notes receivable account consists of two notes, a $100,000 note and a $300,000

note. The $100,000 note is dated October 31, 2015, with principal and interest payable

on October 31, 2016. The $300,000 note is dated March 31, 2015, with principal and

8% interest payable on March 31, 2016.

2> During 2016, sales revenue totaled $2,120,000, $1,980,000 cash was collected from

customers, and $41,000 in accounts receivable were written off. All sales are made on a

credit basis. Bad debt expense is recorded at year-end by adjusting the allowance

account to an amount equal to 8% of year-end accounts receivable. Required:

1> In addition to sales revenue, what revenue and expense amounts related to

receivables will appear in Cordova’s 2016 income statement?

2> Calculate the receivables turnover ratio for 2016.

Tokyo Imports sold merchandise to Tall-Mart, receiving a six-month,

noninterest-bearing note for $100,000. The implied discount rate on the note is 10% per

annum. Tokyo uses a periodic inventory system.

Required:

1> Prepare the journal entry to record the sale.

2> Compute the effective rate of interest.

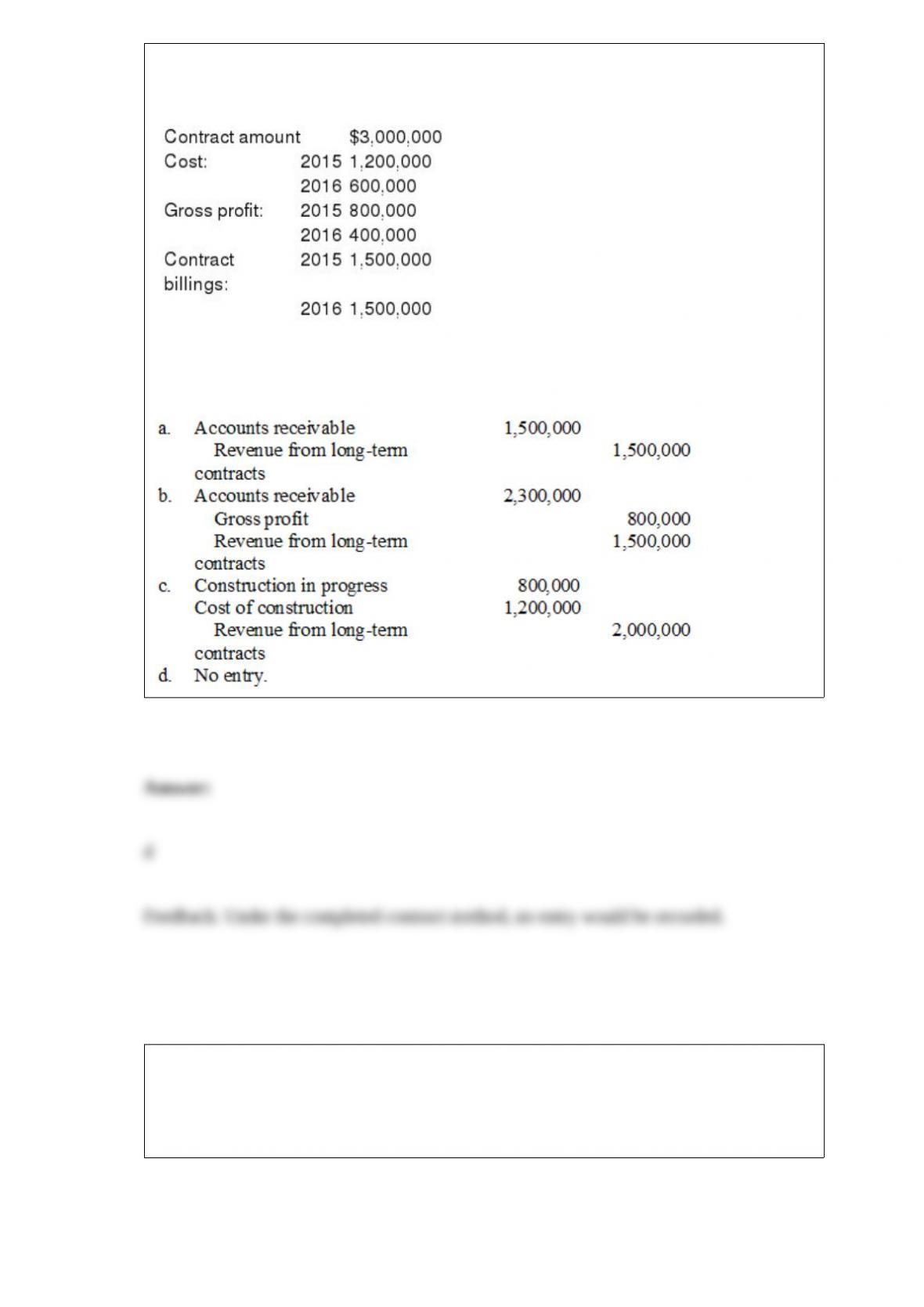

Arizona Desert Homes (ADH) constructed a new subdivision during 2015 and 2016

under contract with Cactus Development Co. Relevant data are summarized below:

ADH recognizes revenue upon completion of the contract.

For 2015, what is the journal entry to record revenue?

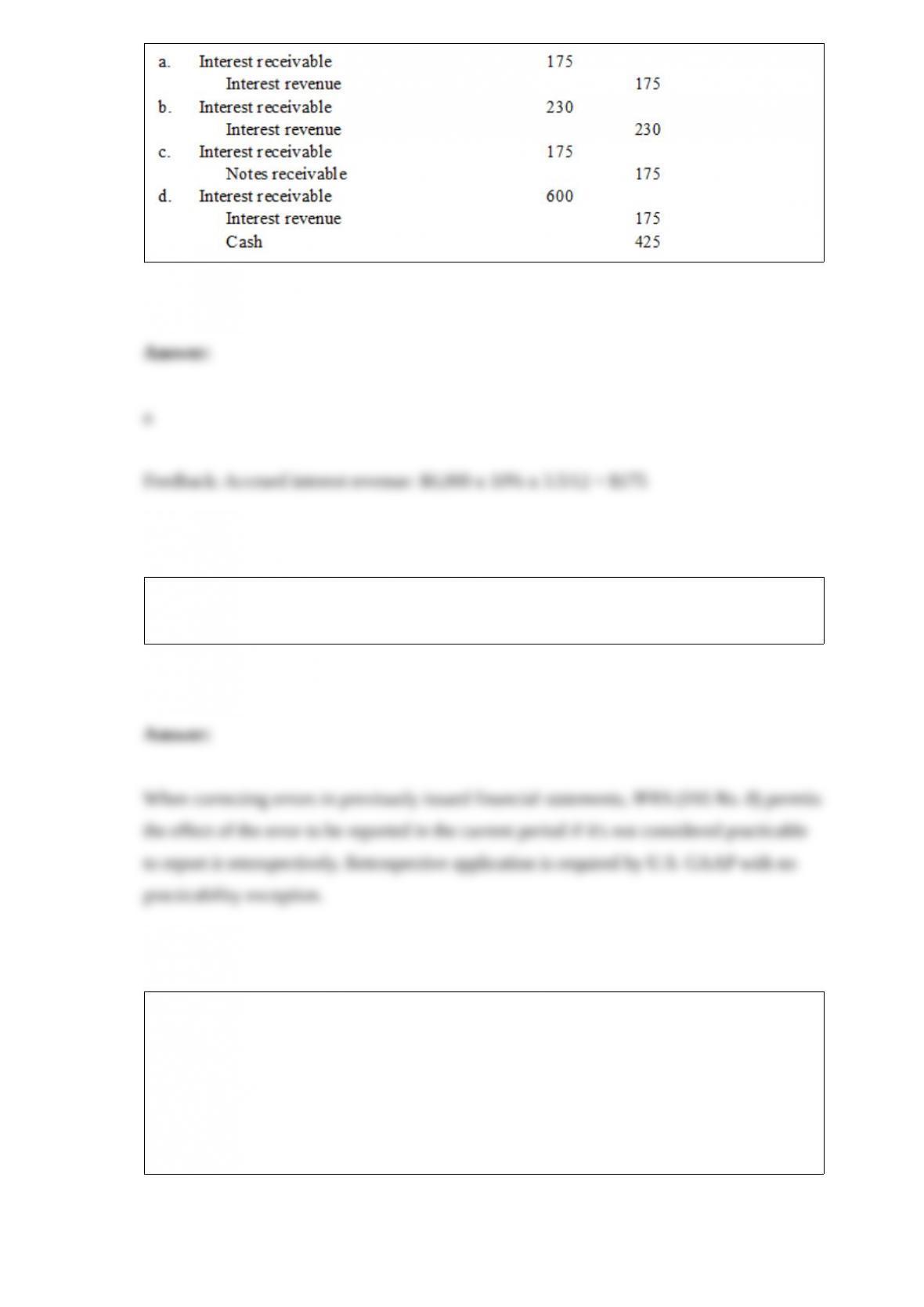

On September 15, 2016, Oliver’s Mortuary received a $6,000, nine-month note bearing

interest at an annual rate of 10% from the estate of Jay Hendrix for services rendered.

Oliver’s has a December 31 year-end. What adjusting entry will the company record on

December 31, 2016?

What is the difference between U.S. GAAP and IFRS with regard to the correction of

accounting errors?

The shareholders’ ‘equity of Tru Corporation includes $600,000 of $1 par common

stock and $1,200,000 par value of 6% cumulative preferred stock. The board of

directors of Tru declared cash dividends of $150,000 in 2016 after paying $60,000 cash

dividends in each of 2015 and 2014.

Required:

What is the amount of dividends common shareholders will receive in 2016?

What is an antidilutive security?