Webster Company issues $1,000,000 face value, 6%, 5-year bonds payable on

December 31, 2015. Interest is paid semiannually each June 30 and December 31. The

bonds sell at a price of 97; Webster uses the straight-line method of amortizing bond

discount or premium.

Refer to the information above. The carrying value of this liability in Webster

Company’s December 31, 2016, balance sheet is:

A. $1,000,000.

B. $970,000.

C. $976,000.

D. $967,000.

An activity base is said to be a “driver” of overhead costs when the activity base:

A. Is independent of the amount of overhead cost incurred.

B. Results in an overhead application rate greater than 100%.

C. Is a causal factor in the amount of overhead cost incurred.

D. Is the largest of the various types of expenditures classified as manufacturing

overhead.

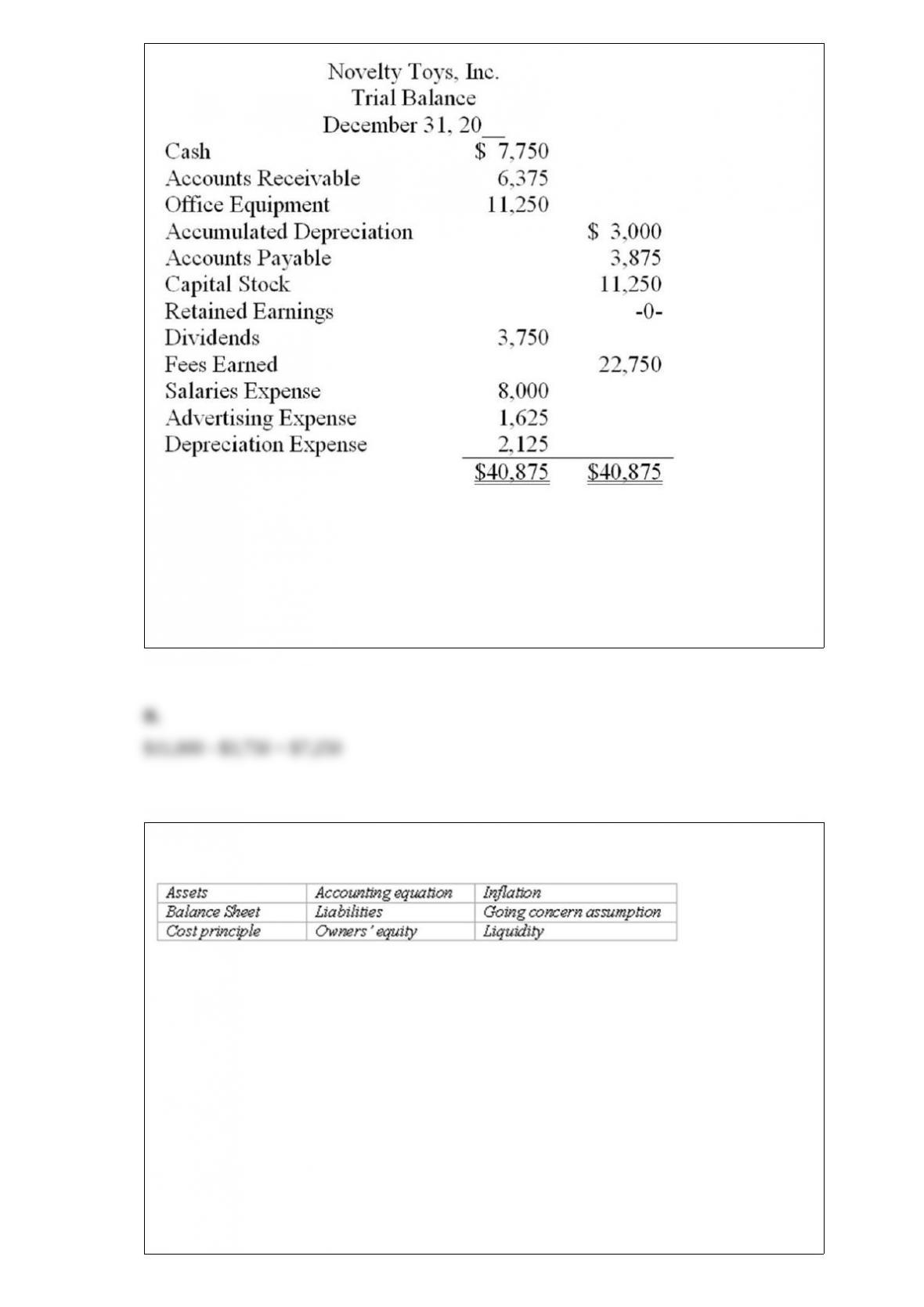

Shown below is a trial balance for Novelty Toys Inc., on December 31, after adjusting

entries:

Refer to the information above. After closing the accounts, Retained Earnings at

December 31 equals:

A. $11,000.

B. $7,250.

C. Zero.

D. $22,250.

Accounting terminology

Listed below are nine technical accounting terms introduced in this chapter:

Each of the following statements may (or may not) describe one of these technical

terms. In the space provided below each statement, indicate the accounting term

described, or answer “None” if the statement does not correctly describe any of the

terms. Do not use a term more than once.

(A.) Having the financial ability to pay debts as they become due.

(B.) An assumption that a business will operate in the foreseeable future.

(C.) Economic resources owned by businesses that are expected to benefit future

operations.

(D.) The debts or obligations of a business organization.

(E.) Assets = Liabilities + Owners’ Equity

(F.) The principle which states that assets are valued in the balance sheet at their

historical cost.

(G.) A residual amount equal to assets minus liabilities.

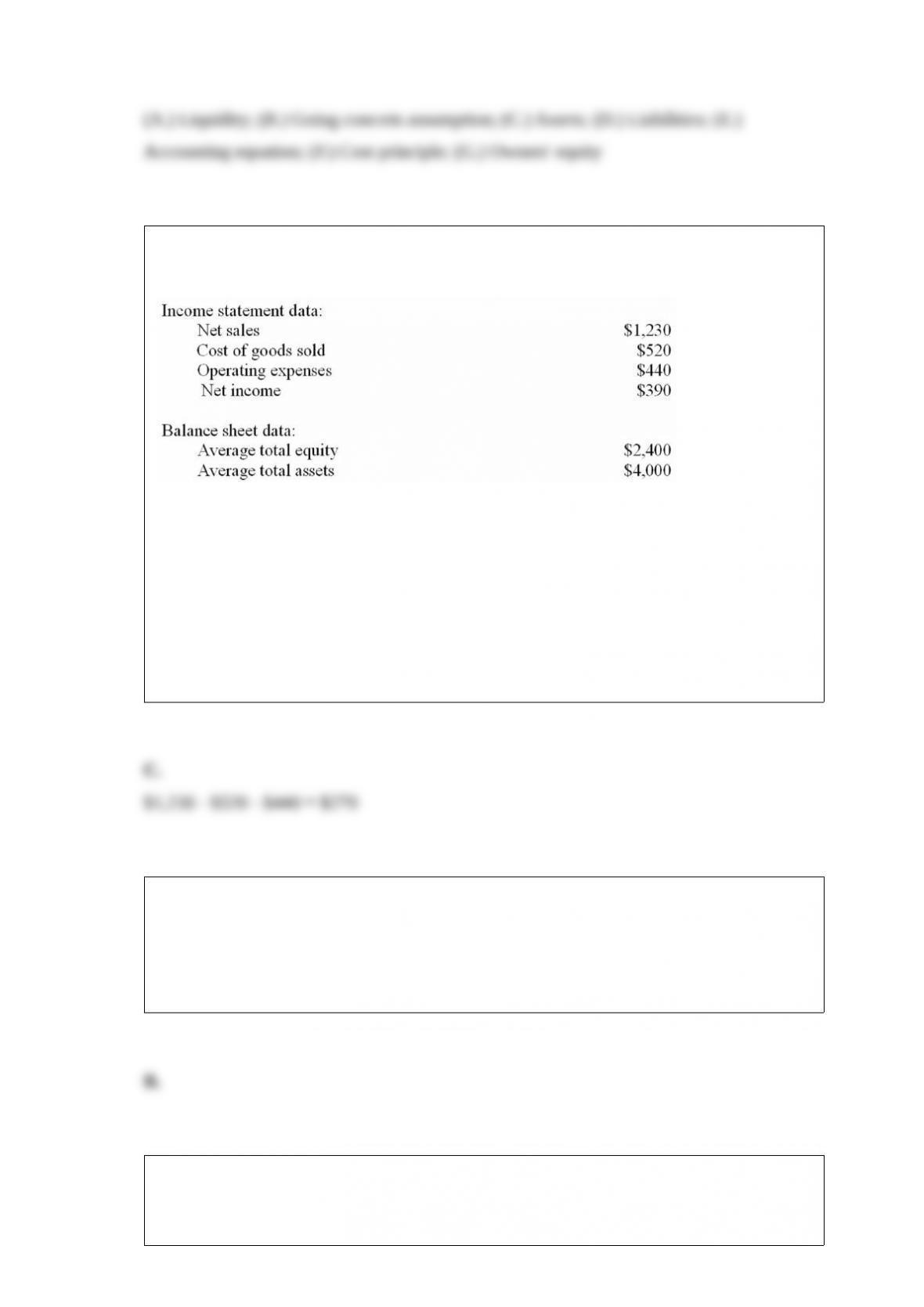

Shown below are selected data from the financial statements of Supreme Co. Dollar

amounts are in millions (except for the per share data).

Supreme reported earnings per share for the year of $4 and paid cash dividends of $1

per share. At year-end, the Wall Street Journal listed Supreme’s capital stock as trading

at $88 per share.

Refer to the information above. What was Supreme’s operating income? (in millions):

A. $710.

B. $390.

C. $270.

D. $520.

A company’s relevant range of production is:

A. The production range from zero to 100% of plant capacity.

B. The production range over which CVP assumptions are valid.

C. The production range beyond the break-even point.

D. The production range that covers fixed but not variable costs.

The principle of consistency states that:

A. Companies are prohibited from ever changing their accounting methods.

B. Every company in the same industry must use the same accounting principle.

C. There must be a consistent blend to the accounting principles.

D. If changes in accounting principles are made, the reasons for the change and the

effects on the company’s net income must be disclosed.

Refer to the information above. What is the return on investment for Brookes, Inc.

(round your answer to the nearest full percentage point)?

A. 70%.

B. 19%.

C. 13%.

D. 9%.

Hamilton Company reported an increase of $370,000 in its accounts receivable during

the year 2015. The company’s statement of cash flows for 2015 reported $1 million of

cash received from customers. What amount of net sales must Hamilton have recorded

in 2015?

A. $630,000.

B. $1,370,000.

C. $1,000,000.

D. $370,000.

Omega Company adjusts its accounts at the end of each month. The following

information has been assembled in order to prepare the required adjusting entries at

December 31:

(1) A one-year bank loan of $720,000 at an annual interest rate of 12% had been

obtained on December 1.

(2) The company pays all employees up-to-date each Friday. Since December 31 fell on

Tuesday, there was a liability to employees at December 31 for two day’s pay

amounting to $6,800.

(3) On December 1, rent on the office building had been paid for four months. The

monthly rent is $6,000.

(4) Depreciation of office equipment is based on an estimated useful life of six years.

The balance in the Office Equipment account is $9,360; no change has occurred in the

account during the year.

(5) Fees of $9,800 were earned during the month for clients who had paid in advance.

Refer to the information above. Failure to make the appropriate adjustment to the

Salary Expense account will:

A. Understate net income for December by $6,800.

B. Understate net income for January by $6,800.

C. Overstate total liabilities at December 31.

D. Overstate the balance in Cash at December 31.

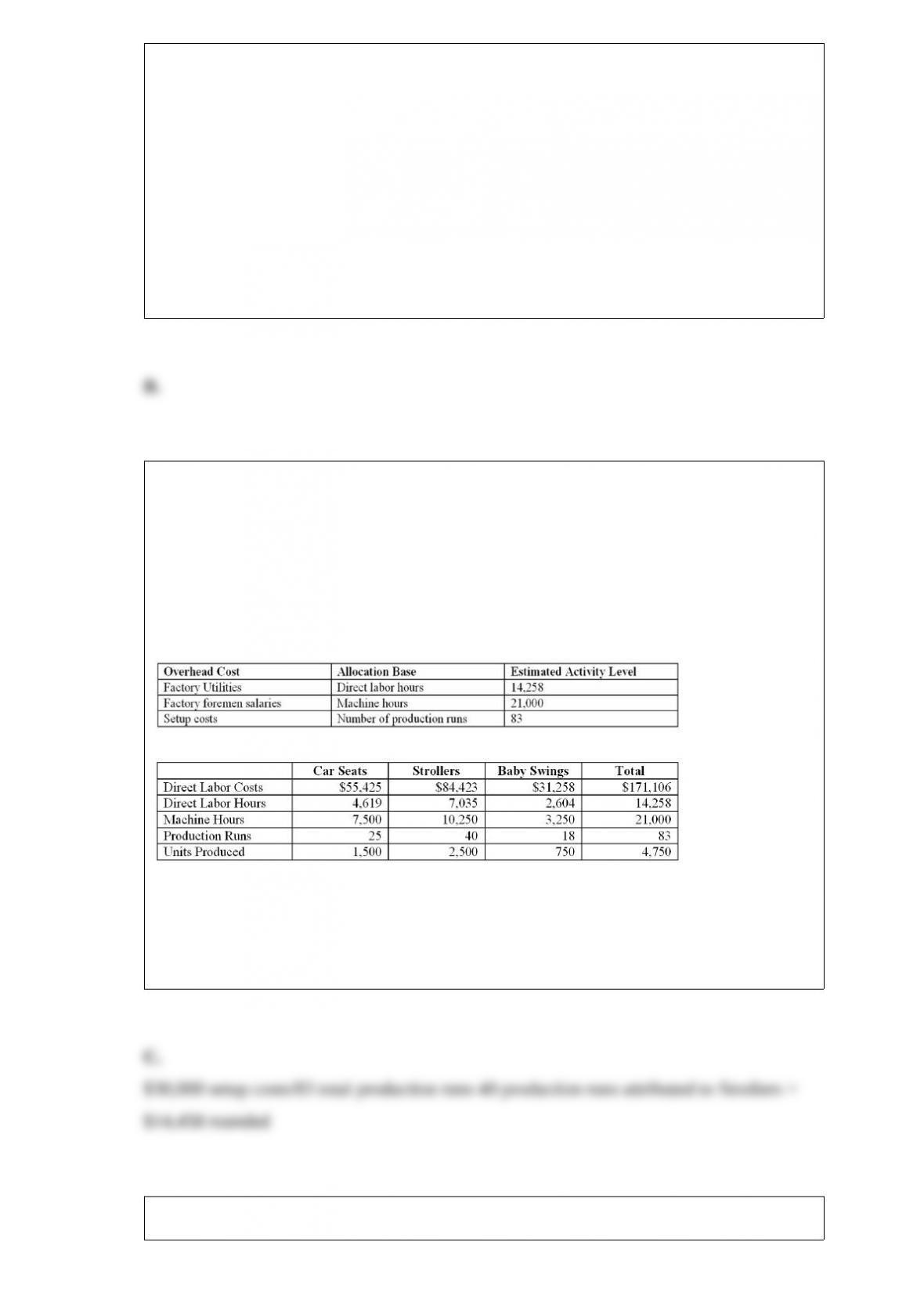

Starbright manufactures children car seats, strollers, and baby swings. Starbright’s

manufacturing costs are budgeted as follows:

Factory utilities $105,000

Factory foremen salaries $75,000

Machinery setup costs $30,000

Total manufacturing overhead $210,000

The company uses activity-based costing to allocate its manufacturing overhead costs to

products based on the following schedule:

During the current month, the following levels of activities were incurred:

What are the setup costs allocated to Strollers during the current month?

A. $9,036.

B. $6,502.

C. $14,458.

D. Cannot be determined.

The primary reason a physical inventory is taken is to:

A. Adjust the perpetual inventory record for unrecorded shrinkage losses.

B. Ensure the periodic inventory record is valued correctly.

C. Both ensure the periodic inventory record is being stored securely and that it is

valued correctly.

D. Ensure the perpetual inventory record is being stored in a secure manner.

At the end of October, Flagship Marina received a bill for fuel used in October.

Payment is not due until November 30. This transaction:

A. Should not be recorded in the accounting records until November.

B. Causes a decrease in assets and in owners’ equity in November, when the bill is paid.

C. Should be recorded as an expense of October, regardless of the payment date.

D. Is recorded as a liability in October, but is not considered an expense until paid.

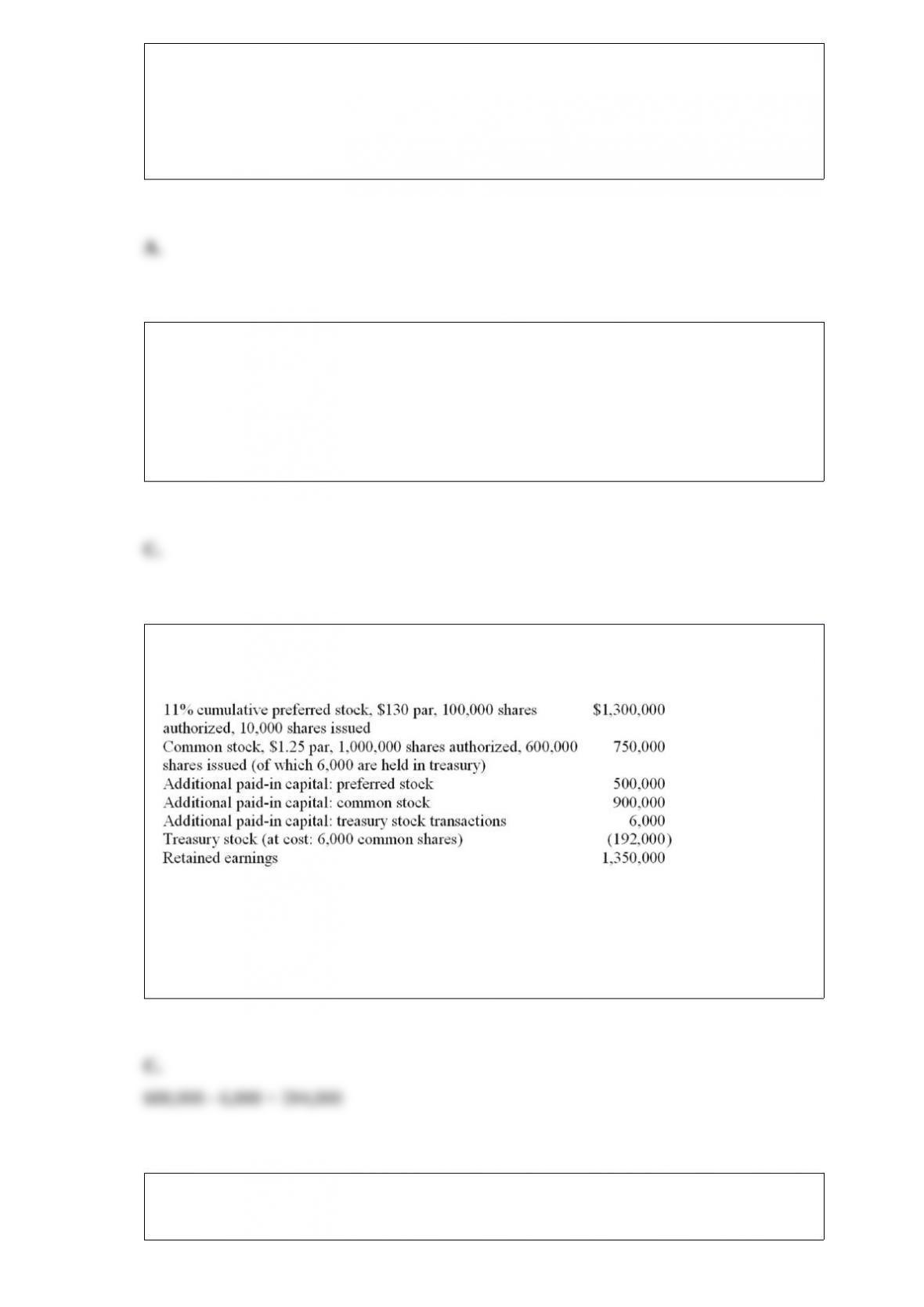

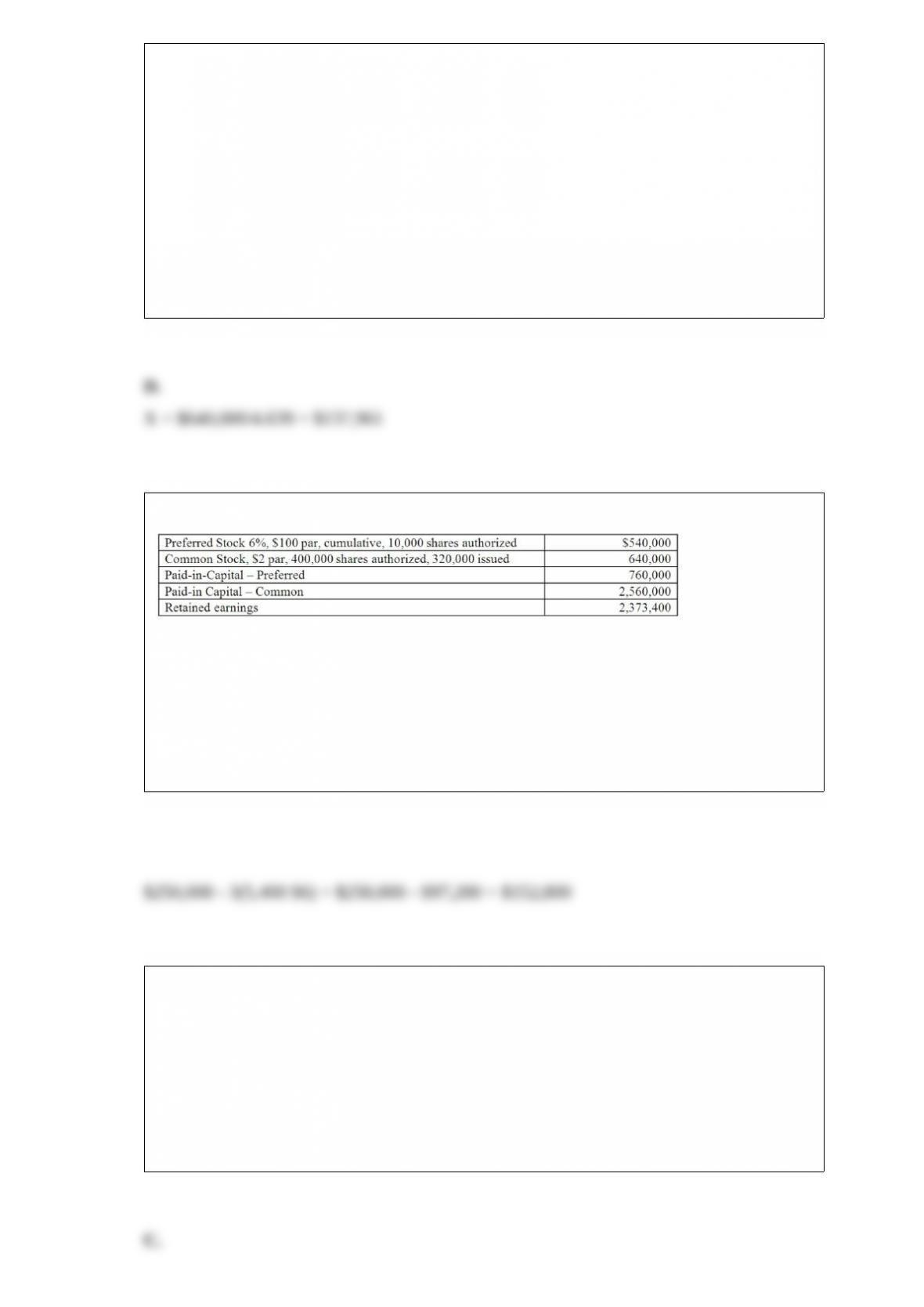

Shown below is information relating to the stockholders’ equity of Brookdale

Corporation at December 31, 2015:

Refer to the information above. How many shares of common stock are outstanding?

A. 600,000 shares.

B. 606,000 shares.

C. 594,000 shares.

D. 1,000,000 shares.

Canfield Construction applies overhead to its projects at a rate of $65 per direct labor

hour. Laborers are paid an average rate of $30 per hour. The Jefferson Apartments

project was charged a total of $1,200,000 in direct materials and $450,000 in direct

labor costs.

Refer to the information above. Overhead applied to the Jefferson Apartments project

amounted to:

A. $450,000.

B. $650,000.

C. $975,000.

D. Some other amount.

A cash dividend paid to shareholders is reported on the:

A. Financing activities section of the statement of cash flows.

B. Balance sheet.

C. Income statement.

D. Operating activities section of the statement of cash flows.

Which of the following costs would not be considered part of the manufacturing

overhead of a chemical plant?

A. The costs of disposing of toxic waste materials.

B. Salaries of factory medical personnel.

C. Salaries of employees who operate distilling equipment used in the production

process.

D. The cost of complying with federal safety regulations concerning plant operations.

Flow of manufacturing costs

The following data are taken from the accounting records of Victoria Mfg. Co.:

Compute the following amounts:

(a) Direct materials purchased during the period: $___________

(b) Total manufacturing costs charged to production (the Work in Process Inventory

account) during the year: $___________

(c) The cost of finished goods manufactured during the year: $___________

(d) The cost of goods sold during the year: $___________

Prepaid expenses are:

A. Assets.

B. Income.

C. Liabilities.

D. Expenses.

A journal entry to recognize an expense must include:

A. A credit to Accounts Payable.

B. A credit to an expense account.

C. A credit to Cash.

D. A debit to an expense account.

The FASB takes on a responsibility to do the following, except:

A. Set the objectives of financial reporting.

B. Describe the elements of financial statements.

C. Judge disputes between management and the CPA.

D. Determine the criteria for deciding what information to include in financial

statements.

A U.S. public corporation’s decision to globalize impacts all of following except:

A. Internal procedures.

B. Who owns stock in the company.

C. Production processes.

D. Accounting outputs.

Which of the following is a period cost?

A. Depreciation on a factory building.

B. The cost of direct materials used.

C. Depreciation on a sales showroom.

D. The cost of disposing of hazardous waste materials from factory operations.

Accounting terminology

Listed below are nine technical accounting terms emphasized in this chapter:

Each of the following statements may (or may not) describe one of these technical

terms. In the space provided below each statement, indicate the accounting term

described, or answer “None” if the statement does not correctly describe any of the

terms.

______ (a.) An account with a credit balance that is an offset against an asset account.

______ (b.) A contra-account.

______ (c.) A liability to customers who have paid in advance.

______ (d.) The estimated current value of an asset.

______ (e.) Entries made to achieve the goals of accrual accounting when revenue or

expense transactions span more than one accounting period.

______ (f.) An asset that will expire shortly.

______ (g.) Revenue that has been earned, but not yet received.

Which of the following assets would most likely be listed last on a statement of

financial position?

A. Land.

B. Cash.

C. Accounts receivable.

D. Equipment.

The most widely used budgeting philosophy is the:

A. Operational approach.

B. Behavioral approach.

C. Strategic approach.

D. Tactical approach.

Rooney, Inc. is considering the purchase of a new machine costing $640,000. The

machine’s useful life is expected to be 8 years with no salvage value. The straight-line

depreciation method will be used. The net increase in annual after tax cash flow is

expected to be $147,000. Rooney estimates its cost of capital to be 14%. (The present

value of a $1 annuity for 8 years at 14% is 4.639, and the present value of $1 to be

received in 8 years is 0.351.)

Refer to the information above. Upper level managers at Rooney, Inc. are concerned

that employee estimates of future cash flows from the new machine may be overly

optimistic. To what dollar amount can the annual after tax cash flow fall before the

investment in the new machine should be rejected?

A. $640,000.

B. $224,640.

C. $168,080.

D. $137,961.

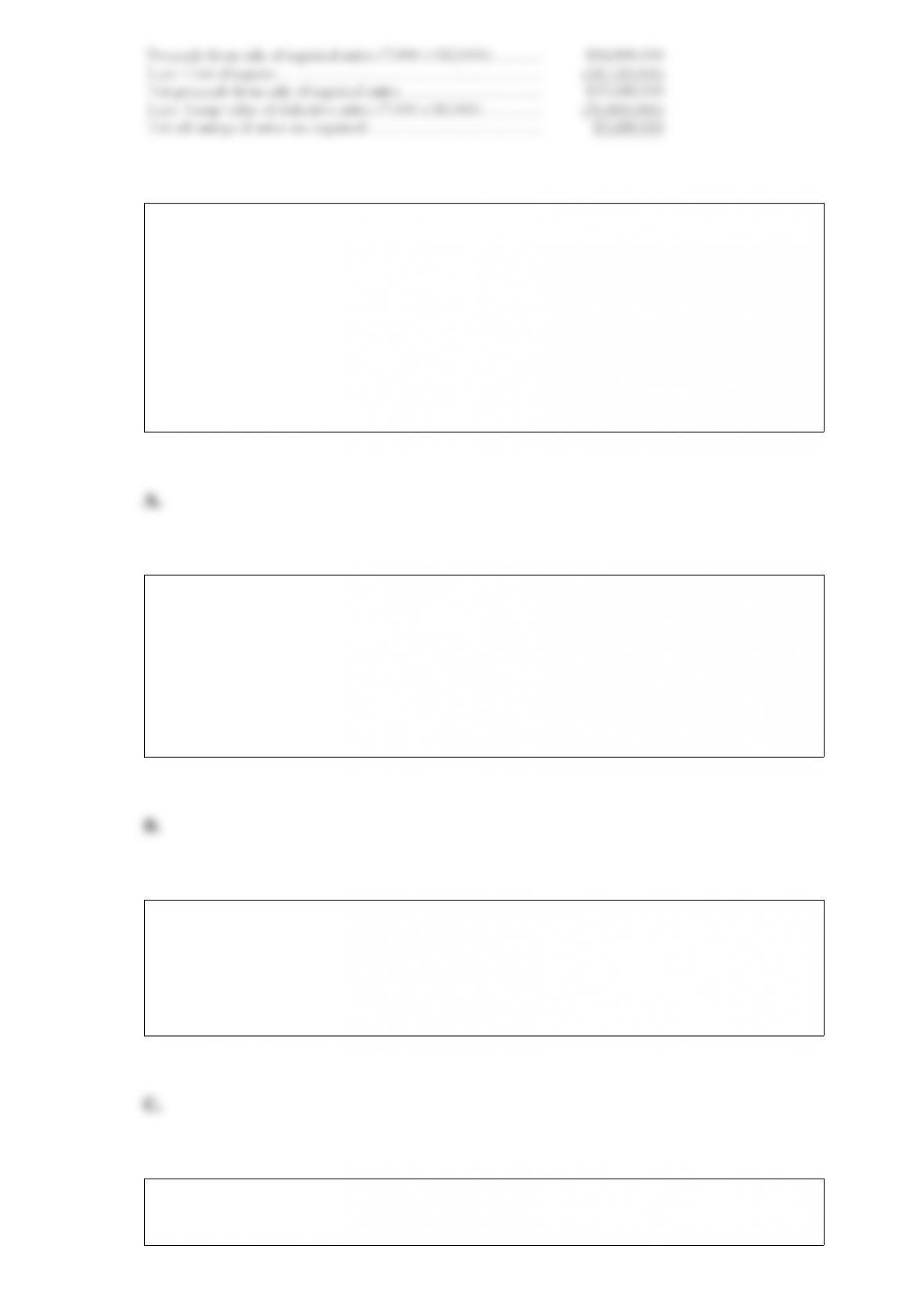

Amelia Corporation has the following information in its financial statement:

Refer to the information above. If Amelia did not pay a dividend for the last two years,

but declared a $250,000 dividend this year, how much will the common stockholders

receive?

A. $152,800.

B. $250,000.

C. $97,200.

D. $217,600.

Legendary Motors has 7,000 defective autos on hand which cost $12,880,000 to

manufacture. Legendary can either sell these defective autos as scrap for $8,000 per

auto, or spend an additional $18,320,000 on repairs and then sell them for $12,000 per

unit. What is the net advantage to repair the autos compared to selling them for scrap?

A. $84,000,000.

B. $18,320,000.

C. $9,680,000.

D. $56,000,000.

Tomassi Company paid $450,000 to acquire a piece of real estate consisting of land and

an office building with a parking lot. In this situation:

A. The purchase price should be apportioned among the Land, Land Improvement, and

Building accounts.

B. The entire purchase price should be debited to the Land account only.

C. Land, Land Improvement, and Building accounts should each be credited for the

respective appraisal value of each item.

D. Allocation of the entire $450,000 to Land results in an understatement of net income

in the current and future accounting periods.

A prior period adjustment appears in the financial statements of the current year when:

A. An error was made in computing the net income of the current period.

B. An error was made in measuring the net income of a previous year or years.

C. An extraordinary loss in a prior year was included among normal results of

operations in the prior year.

D. Earnings per share figures from prior years are restated to reflect the increased

number of shares outstanding due to a stock split or a stock dividend.

Treasury stock:

A. Is an asset.

B. Increases total stockholders’ equity.

C. Decreases total stockholders’ equity.

D. Does not change total stockholders’ equity.

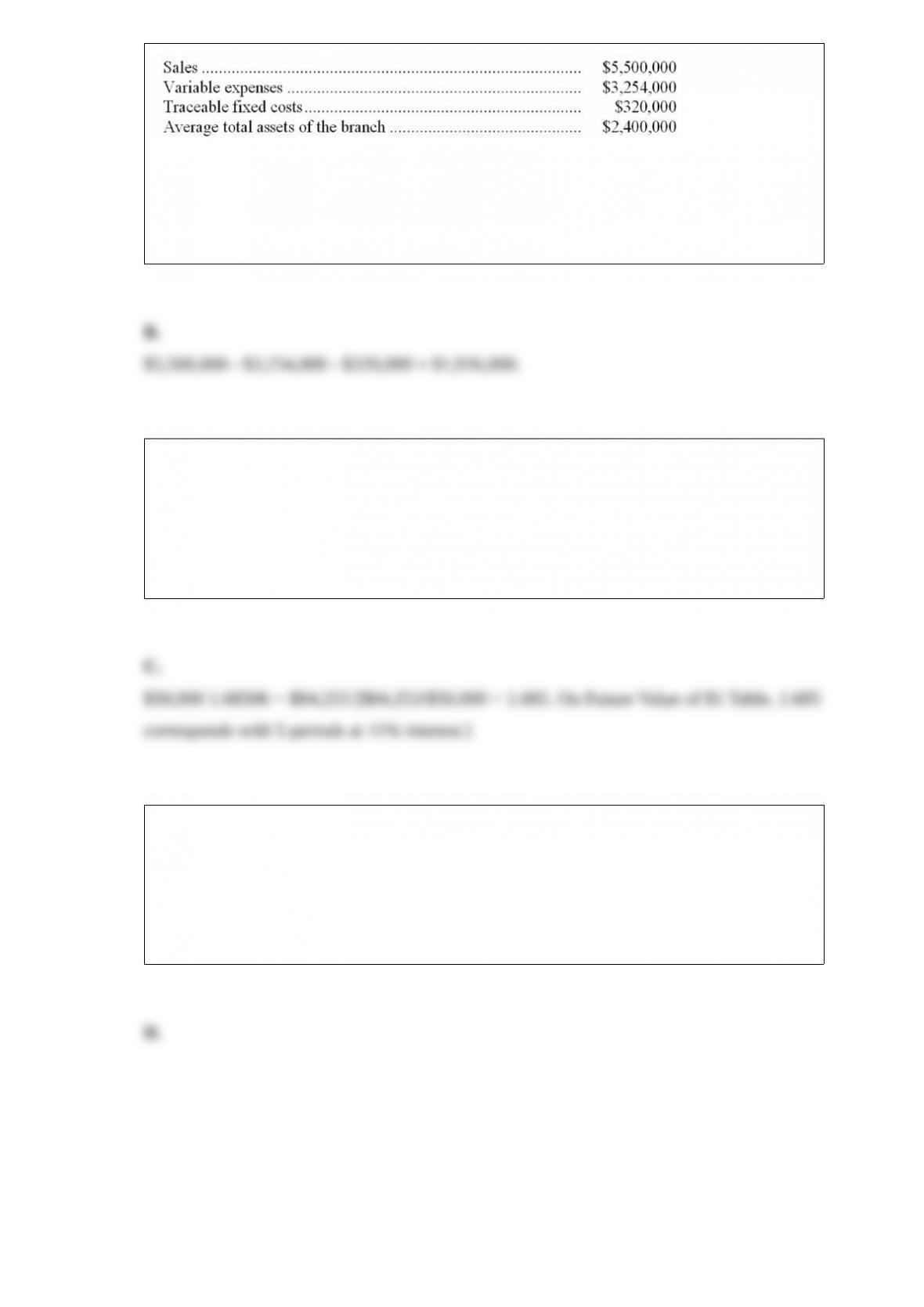

Chic Jewelers views each branch location as an investment center. The local branch

reported the following results for the current year:

Refer to the above information. The responsibility margin of the local branch is:

A. $5,500,000.

B. $1,926,000.

C. $2,246,000.

D. $2,400,000.

If I invest $50,000 today for 5 years and it grows to $84,253, what rate of interest have I

received?

A. 5%.

B. 6%.

C. 11%.

D. 12%.

Refer to the information above. The journal entry to record the transfer of soup out of

the Mixing and Cooking Department during March would include:

A. A debit to Work in Process Inventory, Mixing and Cooking Department of $63,000.

B. A credit to Work in Process Inventory, Canning Department of $72,000.

C. A debit to Finished Goods Inventory of $72,000.

D. A credit to Work in Process Inventory, Mixing and Cooking Department of $63,000.