Of the following, the most important objective for financial reporting is to provide

information useful for:

a. Making decisions.

b. Determining taxable income.

c. Providing accountability.

d. Increasing future profits.

A firm reported salary expense of $239,000 for the current year. The beginning and

ending balances in salaries payable were $40,000 and $15,000, respectively. What was

the amount of cash paid for salaries?

a. $214,000.

b. $289,000.

c. $264,000.

d. $239,000.

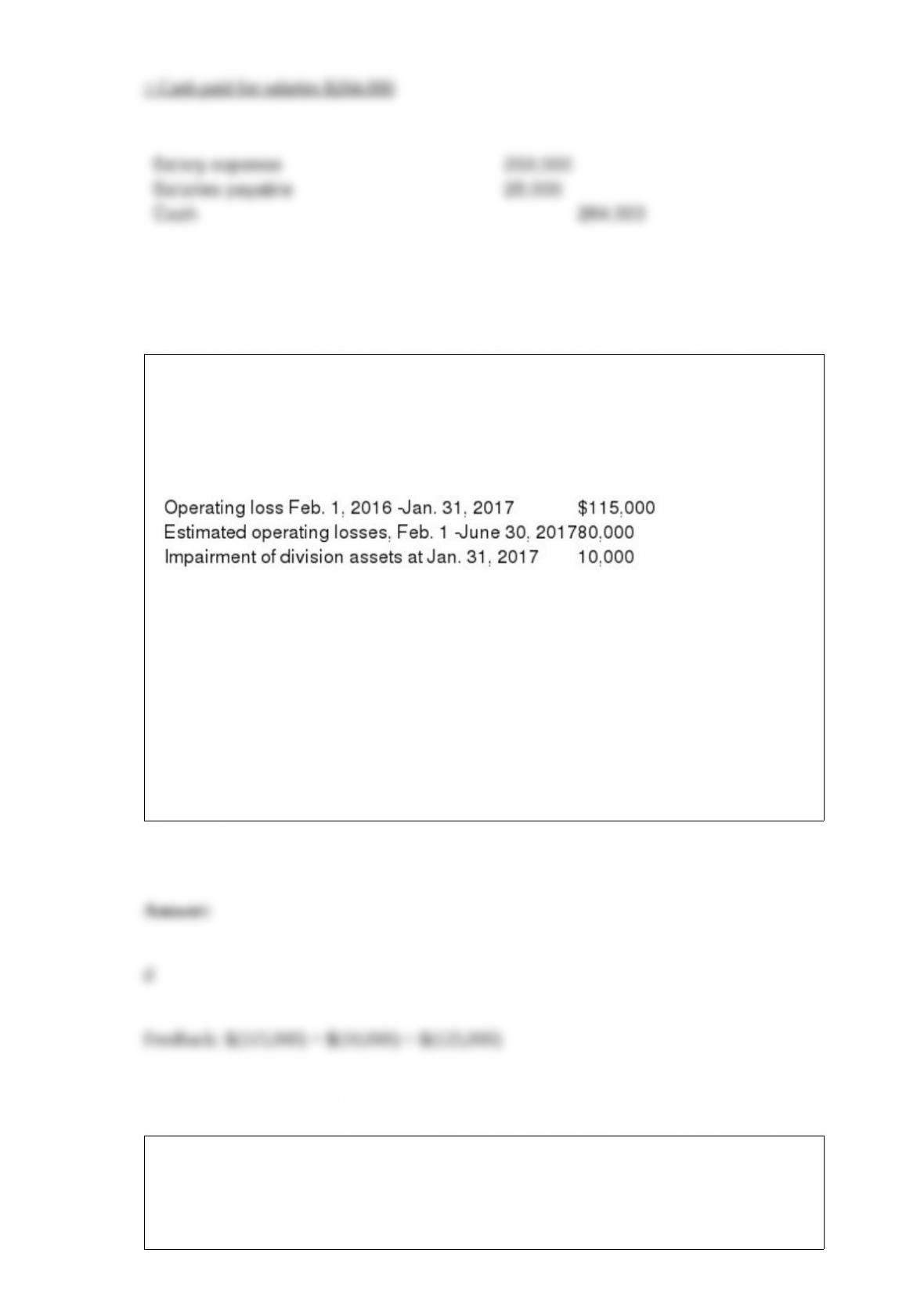

On August 1, 2016, Rocket Retailers adopted a plan to discontinue its catalog sales

division, which qualifies as a separate component of the business according to GAAP

regarding discontinued operations. The disposal of the division was expected to be

concluded by June 30, 2017. On January 31, 2017, Rocket’s fiscal year-end, the

following information relative to the discontinued division was accumulated:

In its income statement for the year ended January 31, 2017, Rocket would report a

before-tax loss on discontinued operations of:

a. $115,000.

b. $195,000.

c. $ 65,000.

d. $125,000.

When converting an income statement from a cash basis to an accrual basis, cash

received for services:

a. Exceed service revenue.

b. May exceed or be less than service revenue.

c. Is less than service revenue.

d. Equals service revenue.

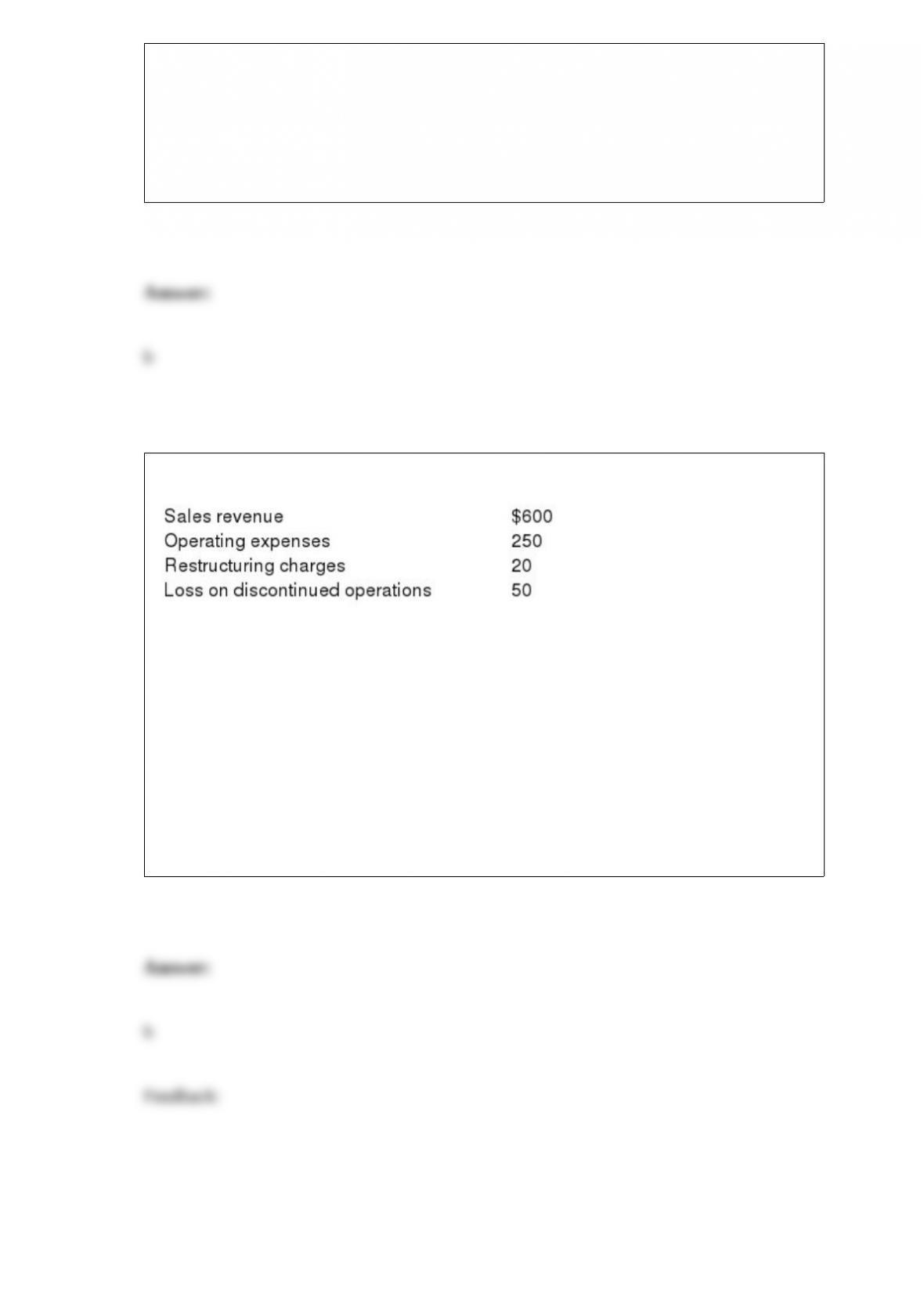

Misty Company reported the following before-tax items during the current year:

Misty’s effective tax rate is 40%.

What is Misty’s net income for the current year?

a. $148.

b. $168.

c. $112.

d. None of the amounts given are correct.

If no estimates are changed and there is no net loss or gain or prior service cost, which

of the following amounts related to an unfunded postretirement benefit plan will not

increase with each additional year of service before the full eligibility date?

a. Other comprehensive income.

b. Postretirement benefit expense.

c. APBO.

d. EPBO.

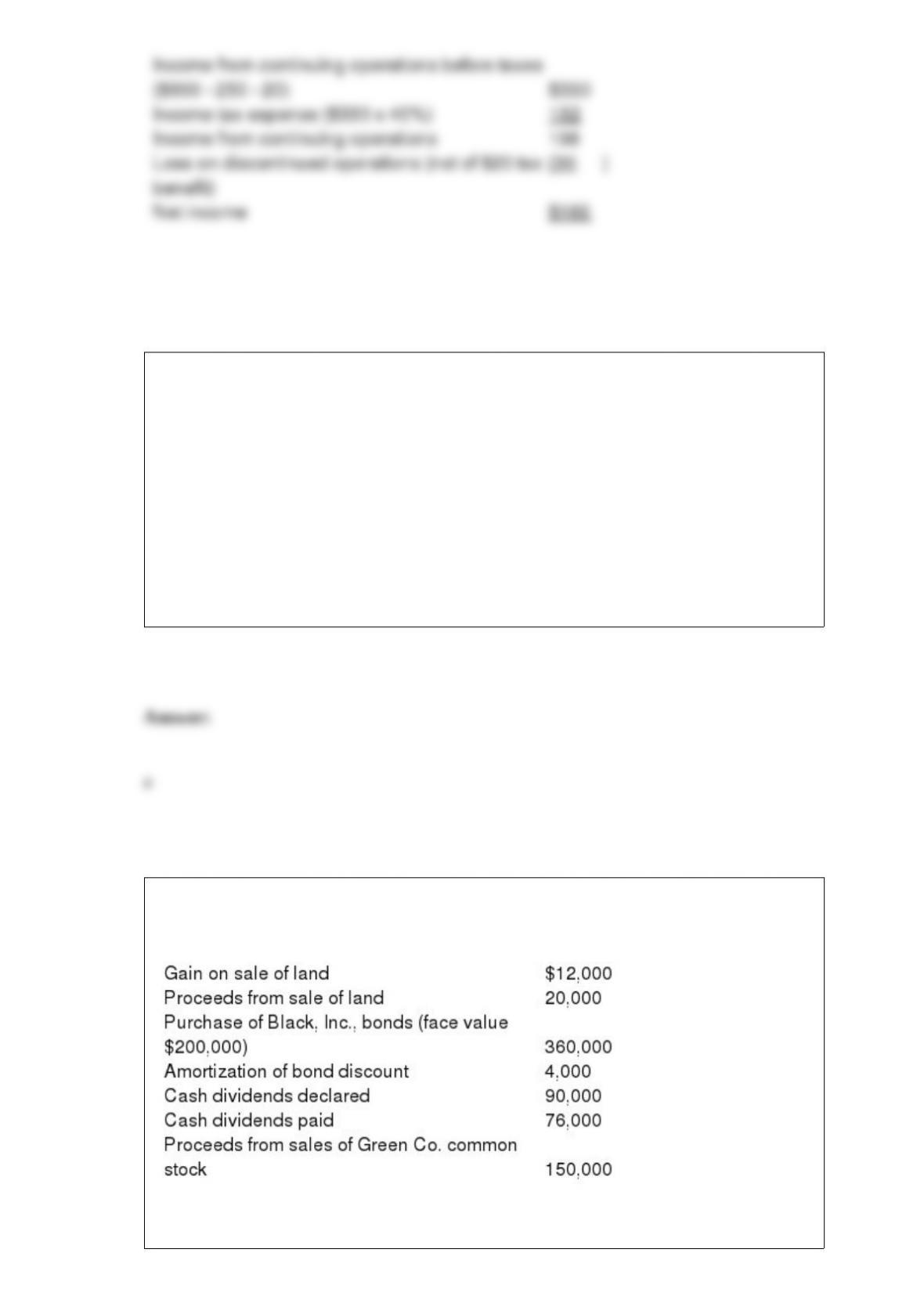

In preparing its cash flow statement for the year ended December 31, 2016, Green Co.

gathered the following data:

In its December 31, 2016, statement of cash flows, what amount should Green report as

net cash from financing activities?

a. $40,000.

b. $54,000.

c. $60,000.

d. $74,000.

Popson Inc. incurred a material loss that was unusual in character. This loss should be

reported as:

a. A discontinued operation.

b. A line item between income from continuing operations and income from

discontinued operations.

c. A line item within income from continuing operations.

d. A line item in the retained earnings statement.

Which of the following is not true about contract assets?

a. Contract assets are recorded when payment depends on something other than the

passage of time.

b. Contract assets are recognized when the seller has a conditional right to receive

payment.

c. Contract assets are recognized when the seller has been paid in advance for at least

partially fulfilling its performance obligations.

d. Contract assets are not the same as accounts receivable.

At December 31, 2015, Mallory, Inc., reported in its balance sheet a net loss of $12

million related to its postretirement benefit plan. The actuary for Mallory at the end of

2016 increased her estimate of future health care costs. Mallory’s entry to record the

effect of this change will include:

a. A debit to Loss-OCI and a credit to APBO.

b. A debit to APBO and a credit to Loss-OCI.

c. A debit to Postretirement benefit expense and a credit to APBO.

d. A debit to Postretirement benefit expense and a credit to Loss-OCI.

Fully vested incentive stock options for 60,000 shares of common stock at an exercise

price of $50 were outstanding at the beginning of 2016. The market price of the stock

averaged $56 during the year.

Required:

If these options are exercised on March 1 of the current year, by how many shares will

the options increase the weighted-average number of shares outstanding when

calculating diluted earnings per share?

McCombs Contractors received a contract to construct a mental health facility for

$2,500,000. Construction was begun in 2015 and completed in 2016. Cost and other

data are presented below:

Assume that McCombs recognizes revenue on this contract over time according to

percentage of completion.

Required: Compute the amount of gross profit recognized during 2015 and 2016.

On February 20, 2016, Genoa Mining Company incurred costs of $3,600,000 to acquire

and prepare to extract an estimated 4,000,000 tons of mineral deposits. In 2016,

450,000 tons of ore were mined. At the beginning of 2017, Genoa geologists estimated

that 3,900,000 tons of ore still remained. In 2017, 700,000 tons of ore were mined.

Required:

Compute depletion for 2016 and 2017.

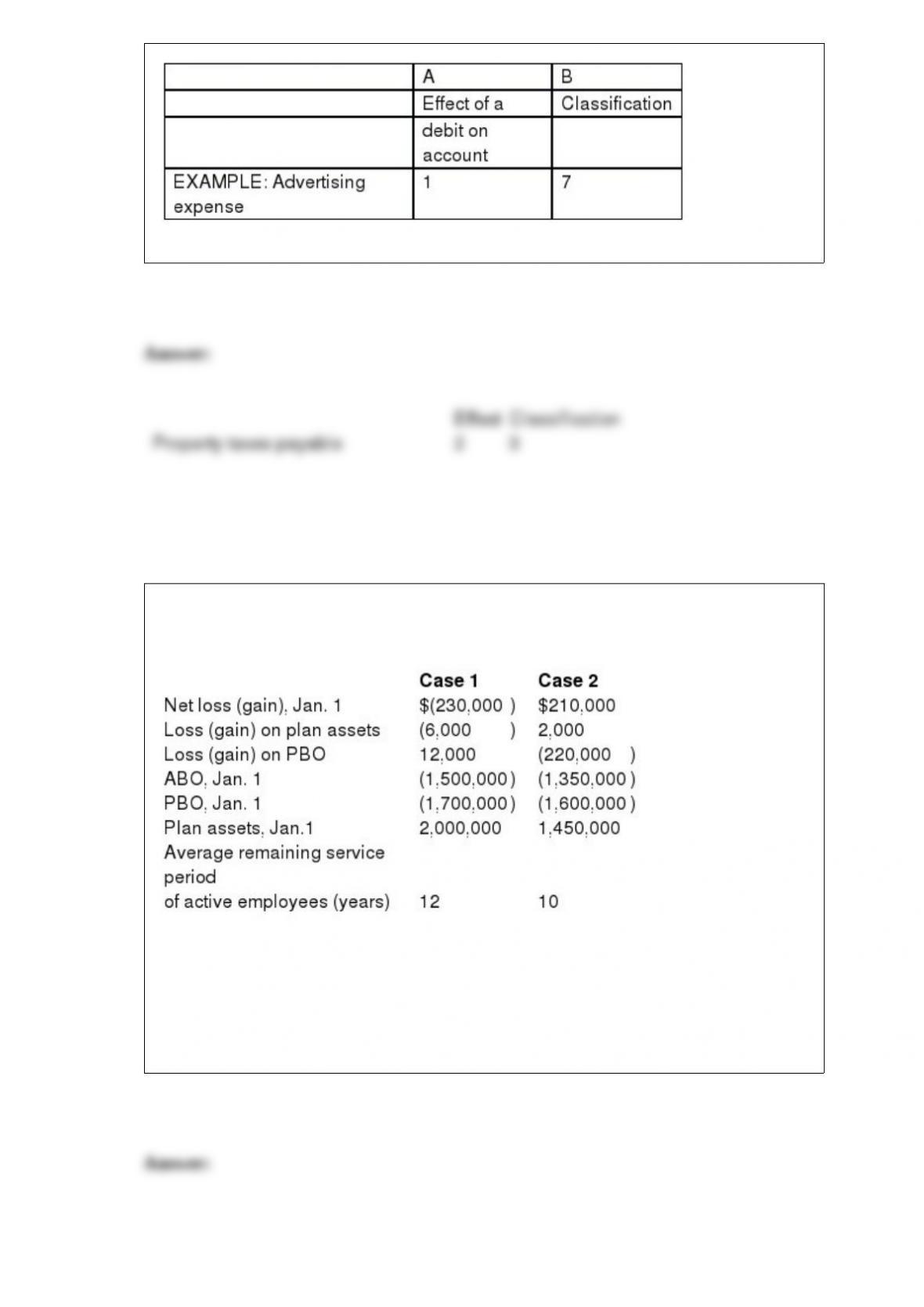

Below is a list of accounts in no particular order. Assume that all accounts have normal

balances. Required: In column A, indicate whether a debit will:

1> Increase the account balance, or

2> Decrease the account balance. In column B, classify each account according to the

following scheme. For contra accounts, indicate the classification of the account to

which it relates.

1>A current asset in the balance sheet.

2>A noncurrent asset in the balance sheet.

3>A current liability in the balance sheet.

4>A long-term liability in the balance sheet.

5>A permanent equity account in the balance sheet.

6>A revenue account in the income statement.

7>An expense account shown in the income statement.

8> Account does not appear in either the balance sheet or the income statement.

Property taxes payable

Hall of Fame Co. has a defined benefit pension plan. Two alternative possibilities for

pension-related data for the current calendar year are shown below:

Required:

1) For each independent case, calculate amortization of the net loss or gain that should

be included as a component of pension expense for the current year.

2) Determine the net loss or gain as of December 31 of the current year.