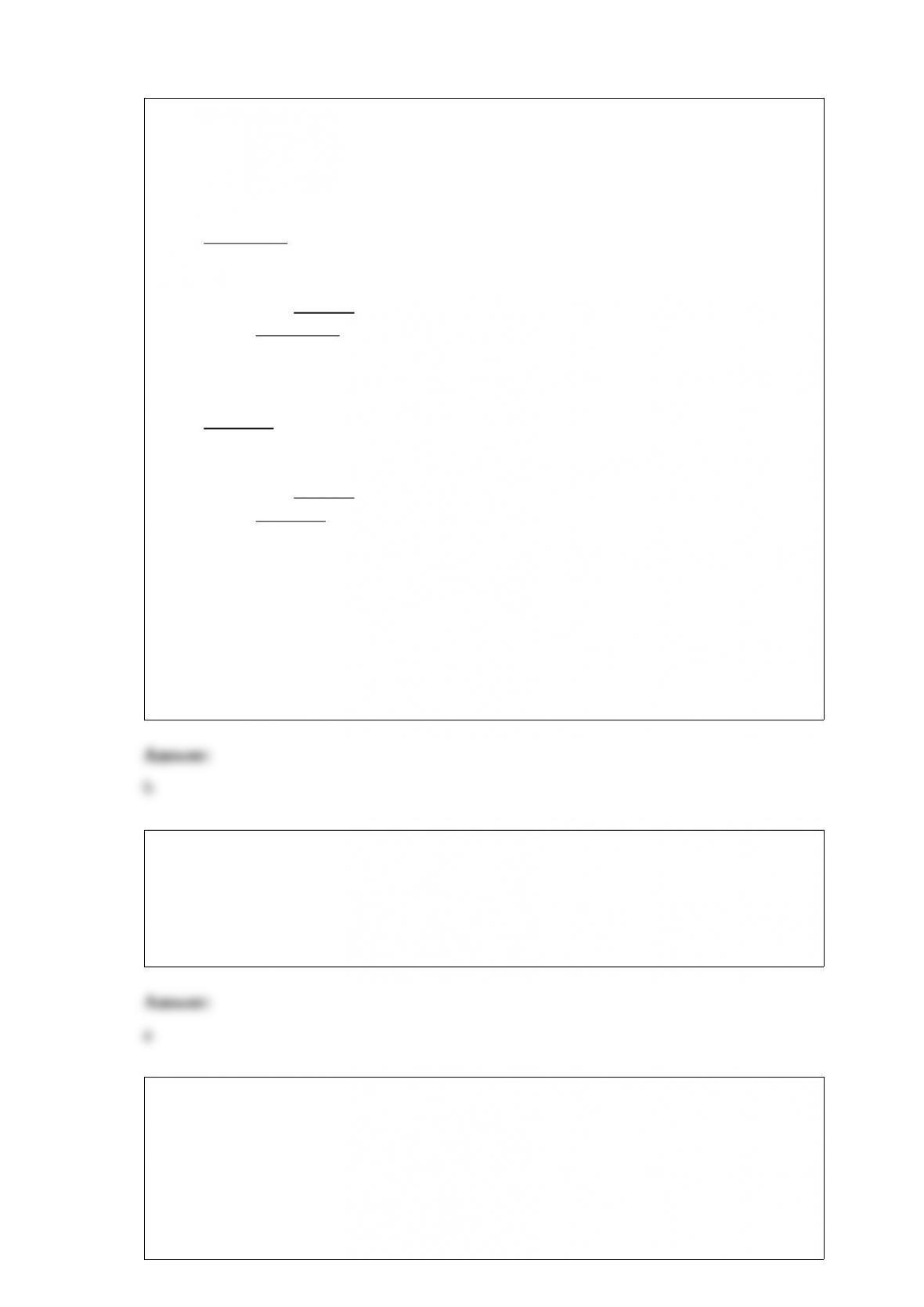

1) The summarized balance sheets of Goebel Company and Dobbs Company as of

December 31, 2014 are as follows:

Goebel Company

Balance Sheet

December 31, 2014

Assets$1,200,000

Liabilities$ 150,000

Capital stock600,000

Retained earnings 450,000

Total equities$1,200,000

Dobbs Company

Balance Sheet

December 31, 2014

Assets$900,000

Liabilities$205,000

Capital stock575,000

Retained earnings 120,000

Total equities$900,000

If Goebel Company acquired a 30% interest in Dobbs Company on December 31, 2014

for $220,000 and during 2015 Dobbs Company had net income of $75,000 and paid a

cash dividend of $30,000, applying the equity method would give a debit balance in the

Equity Investments (Dobbs) account at the end of 2015 of

a.$220,000

b.$233,500

c.$242,500

d.$211,000

2) Gains” on sales of treasury stock (using the cost method) should be credited to

a.paid-in capital from treasury stock

b.capital stock

c.retained earnings

d.other income

3) Glen Inc. and Armstrong Co. have an exchange with no commercial substance. The

asset given up by Glen Inc. has a book value of $36,000 and a fair value of $45,000.

The asset given up by Armstrong Co. has a book value of $60,000 and a fair value of

$57,000. Boot of $12,000 is received by Armstrong Co.

What amount should Armstrong Co. record for the asset received?

a.$45,000

b.$48,000

c.$57,000

d.$60,000

4) When $5,000,000 in convertible bonds are issued at par with $800,000 in value of

the equity option embedded in the bond, the IFRS journal entry will include a debit of

a.$800,000 to Paid-in Capital Convertible Bonds and a credit to Bonds Payable

b.$800,000 to Premium on Bonds Payable and a credit to Paid-in Capital Convertible

Bonds

c.$800,000 to Bonds Payable and a credit to Paid-in Capital Convertible Bonds

d.$4,200,000 to Cash along with a debit of $800,000 to Discount on Bonds Payable and

a credit to Bonds Payable and a credit to Paid-in Capital Convertible Bonds

5) If an industrial firm uses the units-of-production method for computing depreciation

on its only plant asset, factory machinery, the credit to accumulated depreciation from

period to period during the life of the firm will

a.be constant

b.vary with unit sales

c.vary with sales revenue

d.vary with production

6) Betty wants to know how much she should begin saving each month to fund her

retirement. What kind of problem is this?

a.Present value of one

b.Future value of an ordinary annuity

c.Present value of an ordinary

d.Future value of one

7) Wheeler Company issued 5,000 shares of its $5 par value common stock having a

fair value of $25 per share and 7,500 shares of its $15 par value preferred stock having

a fair value of $20 per share for a lump sum of $264,000. The proceeds allocated to the

preferred stock is

a.$158,400

b.$150,000

c.$144,000

d.$120,000

8) Which of the following sets of conditions would give rise to the accrual of a

contingency under current generally accepted accounting principles?

a.Amount of loss is reasonably estimable and event occurs infrequently

b.Amount of loss is reasonably estimable and occurrence of event is probable

c.Event is unusual in nature and occurrence of event is probable

d.Event is unusual in nature and event occurs infrequently

9) On March 1, Felt Co. began construction of a small building. Payments of $320,000

were made monthly for three months beginning March 1 . The building was completed

and ready for occupancy on June 1 . In determining the amount of interest cost to be

capitalized, the weighted-average accumulated expenditures are

a.$80,000

b.$160,000

c.$320,000

d.$640,000

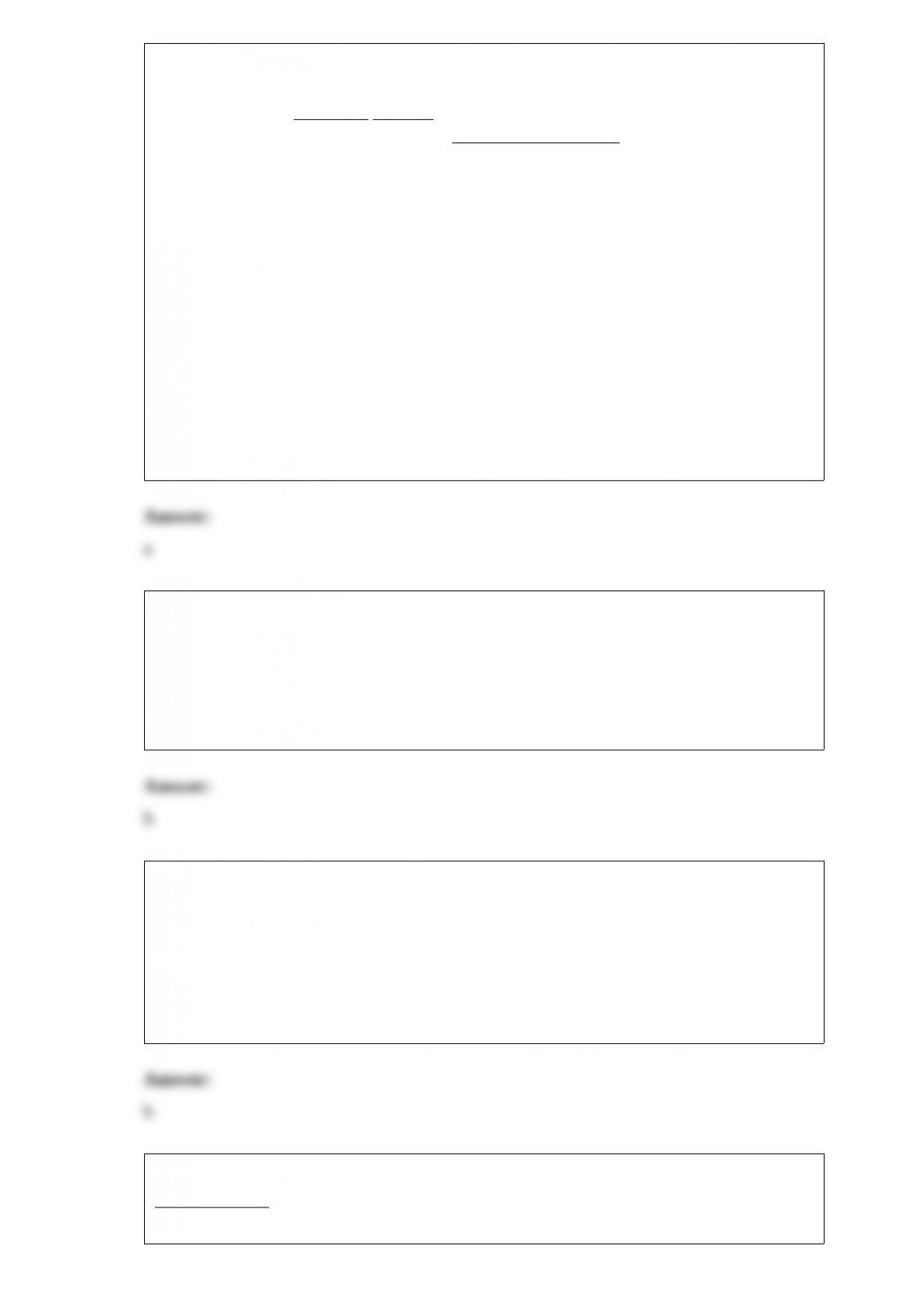

10) December 31,

2015 2014

Assets

Cash$ 440,000$ 200,000

Short-term investments600,000

Accounts receivable (net)1,020,0001,020,000

Inventory1,380,0001,200,000

Long-term investments400,000600,000

Plant assets3,400,0002,000,000

Accumulated depreciation(900,000)(900,000)

Patent 180,000 200,000

Total assets$6,520,000$4,320,000

Liabilities and Stockholders’ Equity

Accounts payable and accrued liabilities$1,660,000$1,440,000

Notes payable (nontrade)580,000

Common stock, $10 par1,600,0001,400,000

Additional paid-in capital800,000500,000

Retained earnings 1,880,000 980,000

Total liabilities and stockholders’ equity$6,520,000$4,320,000

Information relating to 2015 activities:

Net income for 2015 was $1,300,000.

Cash dividends of $400,000 were declared and paid in 2015 .

Equipment costing $1,000,000 and having a carrying amount of $320,000 was sold in

2015 for $360,000.

A long-term investment was sold in 2015 for $320,000. There were no other

transactions affecting long-term investments in 2015 .

20,000 shares of common stock were issued in 2015 for $25 a share.

Short-term investments consist of treasury bills maturing on 6/30/16.

Net cash provided by Jamisons 2015 financing activities was

a.$680,000

b.$320,000

c.$1,080,000

d.$1,480,000

11) The accounting for treasury stock retirements under IFRS requires

a.a charge for the entire amount to paid-in capital

b.a charge for the excess to paid-in capital, depending on the original transaction related

to the issuance of the stock

c.a charge for the excess of the cost of treasury stock over par value to retained earnings

d.an allocation for the difference between paid-in capital and retained earnings

12) Land was purchased to be used as the site for the construction of a plant. A building

on the property was sold and removed by the buyer so that construction on the plant

could begin. The proceeds from the sale of the building should be

a.classified as other income

b.deducted from the cost of the land

c.netted against the costs to clear the land and expensed as incurred

d.netted against the costs to clear the land and amortized over the life of the plant

13) Transactions for the month of June were:

PurchasesSales

June 1(balance) 1,600 @ $3.20June 21,200 @ $5.50

34,400 @ 3.1063,200 @ 5.50

72,400 @ 3.3092,000 @ 5.50

153,600 @ 3.4010800 @ 6.00

221,000 @ 3.50182,800 @ 6.00

25400 @ 6.00

Assuming that perpetual inventory records are kept in units only, the ending inventory

on a LIFO basis is

a.$8,220

b.$8,320

c.$8,580

d.$8,940

14) For the year ended December 31, 2014, Transformers Inc. reported the following:

Net income$180,000

Preferred dividends declared30,000

Common dividend declared6,000

Unrealized holding loss, net of tax3,000

Retained earnings, beginning balance240,000

Common stock120,000

Accumulated Other Comprehensive Income,

Beginning Balance15,000

What would Transformers report as total stockholders’ equity?

a.$516,000

b.$504,000

c.$384,000

d.$360,000

15) An example of a correction of an error in previously issued financial statements is a

change

a.from the FIFO method of inventory valuation to the LIFO method

b.in the service life of plant assets, based on changes in the economic environment

c.from the cash basis of accounting to the accrual basis of accounting

d.in the tax assessment related to a prior period

16) Of the following costs related to the development of natural resources, which one is

not a part of depletion cost?

a.Acquisition cost of the natural resource deposit

b.Exploration costs

c.Tangible equipment costs associated with machinery used to extract the natural

resource

d.Intangible development costs such as drilling costs, tunnels, and shafts

17) When a customer purchases merchandise inventory from a business organization,

she may be given a discount which is designed to induce prompt payment. Such a

discount is called a(n)

a.trade discount

b.nominal discount

c.enhancement discount

d.cash discount

18) The following data are provided:

December 31,

2015 2014

5% Cumulative preferred stock, $50 par$100,000$100,000

Common stock, $10 par140,00090,000

Additional paid-in capital80,00070,000

Retained earnings (includes current year net income)240,000215,000

Net income60,000

Additional information:

On May 1, 2015, 5,000 shares of common stock were issued. The preferred dividends

were not declared during 2015 . The market price of the common stock was $50 at

December 31, 2015 .

The rate of return on common stock equity for 2015 is calculated as

a.60 / 415

b.60 / 460

c.55 / 415

d.55 / 460