Which of the following misstatements in the payroll cycle could be detected during the

audit of payroll transactions (but would not be discovered as part of the audit of the

bank reconciliation)?

A) failure to include outstanding payroll cheques on the outstanding cheque list

B) overpayment of Receiver General payments received after the year end but recorded

as cash receipts in the current year

C) unclaimed payroll cheques recorded as a deposit near the end of the year, but

reconciled as deposits in transit

D) payment to fictitious employees that had been set up by the payroll supervisor

Which of the following control procedures may prevent the failure to bill customers for

some shipments?

A) Each shipment should be supported by a prenumbered sales invoice that is

accounted for.

B) Each sales order should be approved by authorized personnel.

C) Sales journal entries should be reconciled to daily sales summaries.

D) Each sales invoice should be supported by a shipping document.

The auditor would like to test the existence and accuracy of the transfer of goods from

the raw materials storeroom to the manufacturing assembly lines. Which of the

following audit procedures should be used?

A) conduct a variance analysis of the costs associated with manufacturing, looking for

gross profit fluctuations

B) account for a sequence of raw material requisitions, examining details and looking

for proper approvals

C) look at overtime records to determine the amount and timing of overtime hours used

in the manufacturing process

D) inquire of the inventory custodian with respect to procedures used to transfer raw

materials to the production line

You have just recently become a member of your local non-profit housing co-op by

moving into the largest unit. The Board of Directors has asked that you handle the

review engagement, but you are concerned about independence. What is a practical way

for you to stay in the co-op but also perform the review engagement?

A) Request a bylaw stating that the accountant cannot vote for Board members.

B) Do a compilation rather than a review engagement.

C) Have all the preparation work for the review engagement completed by a Board

member.

D) Include a paragraph in the review engagement report stating that you are not

independent.

A) Describe each of the major types of cash accounts maintained by business entities.

B) Discuss the advantages of using an imprest bank account for payroll transactions.

To help improve the cash balance on the financial statements, the controller recorded

several deposits from early January in the month of December. The general

balance-related audit objective affected by this activity is

A) allocation timing.

B) accuracy.

C) classification.

D) existence.

The point at which most companies first recognize the acquisition and related liability

on their records is when the

A) purchase requisition is completed.

B) purchase order is completed.

C) receiving report is completed.

D) vendor’s invoice is paid.

Which of the following internal control tests would help to assess whether payroll

transactions were recorded on the correct dates?

A) Compare cancelled cheques with payroll journal for name, amount, and date

B) Compare date on cheque with date the cheque cleared the bank

C) Compare cancelled cheques with personnel records

D) Recompute hours worked from pay records

The sample exception rate equals the number of

A) exceptions in the population divided by the sample size.

B) items in the population multiplied by the number of exceptions in the sample.

C) exceptions in the sample divided by the sample size.

D) exceptions in the population divided by the population size.

Which of the following is a typical consequence to a PA or PA firm if practice

inspectors find any files or quality control procedures to be unsatisfactory? The PA

A) will lose the right immediately to conduct audit engagements.

B) will no longer be allowed to sign audit reports for a period of time (such as a year).

C) may be required to revise processes or attend training courses.

D) will be required to rewrite the professional qualification examinations.

The most common fraud in the acquisitions area is for the perpetrator to

A) alter the cheque payment file before it is printed so that the payee name is changed.

B) issue payments to fictitious vendors and deposit the cheques to a fictitious account.

C) change the optical characters at the bottom of a cheque to alter the account to be

credited.

D) issue duplicate payments for invoices and then pocket the second cheque.

Blader Ng. Inc. has recently placed into production new air-cleaning systems in their

smoke-stacks to meet clean-air quality regulations. PA has been engaged to assess air

quality and compare results to legislated requirements. What type of audit or

engagement is PA conducting?

A) financial statement

B) compliance

C) operational

D) review

To ensure that goods and services acquired are for authorized company purposes, and

help acquire only needed items

A) receiving reports should be independently signed and reconciled to the purchase

order.

B) proper authorization for acquisitions and changes to the master file should take

place.

C) purchase requisitions should be approved and matched to purchase orders.

D) account allocations of vendor invoices should be carefully checked.

Tests of details of balances relate to which part of the Audit Risk Model?

A) control risk

B) inherent risk

C) substantive risk

D) planned detection risk

A) Describe each of the six key control activities for sales.

B) When assessing planned control risk for sales, the auditor is concerned about proper

authorization at three key points. Discuss each of these three points.

C) When testing the existence objective for sales, the auditor is concerned with the

possibility of three types of misstatements. One type is sales being including in the

journal for which no shipment was made. Discuss the other two types of misstatements.

When processing and recording cash disbursements, it is important to have a method of

cancelling the supporting documents to prevent their reuse as support for another

cheque at a later time. A common method is to

A) shred the documents so they can’t be reused.

B) transfer possession of the documents to a bank vault such as a safety deposit box.

C) move the documents to a permanent off-site facility such as a warehouse.

D) write the cheque number and payment date on the supporting documents.

The internal control which requires “purchase orders be prenumbered and accounted

for” satisfies the objective of

A) occurrence.

B) completeness.

C) accuracy.

D) posting and summarization.

Lauralye Leasing Limited (LLL) provides lease financing to companies and individuals

for equipment other than automobiles. Leases on commercial signs make up 50% of

total leases, computer and telecommunications equipment are 30% and restaurant

equipment makes up most of the remainder. LLL’s customers arrange to buy new

equipment from equipment dealers, then contact LLL to arrange lease financing.

LLL was founded over thirty years ago by Laura and Al Ye. It is now run by Mr. and

Mrs. Ye’s daughter, Betsy, who is the President of LLL. LLL owns a small building

downtown, where the offices of the business are located. Unused office space is rented

out to other commercial tenants.

Betsy was a classmate of yours at York University, and you have kept loosely in touch

over the years. This year, she moved the audit to your firm (a local firm with five

partners), deciding that the firm her parents had hired many years ago did not really

understand her business’ needs.

LLL has a small loan that is used to cover blips in working capital. The company has

two salespeople. Most loans are received from stores throughout the city, with whom

LLL has standing agreements. If customers require financing, they fill in an application

at the store, which is faxed to LLL for approval. LLL will reply within two business

days.

The company has been profitable for many years. There are no extraordinary items in

the current year’s financial statements.

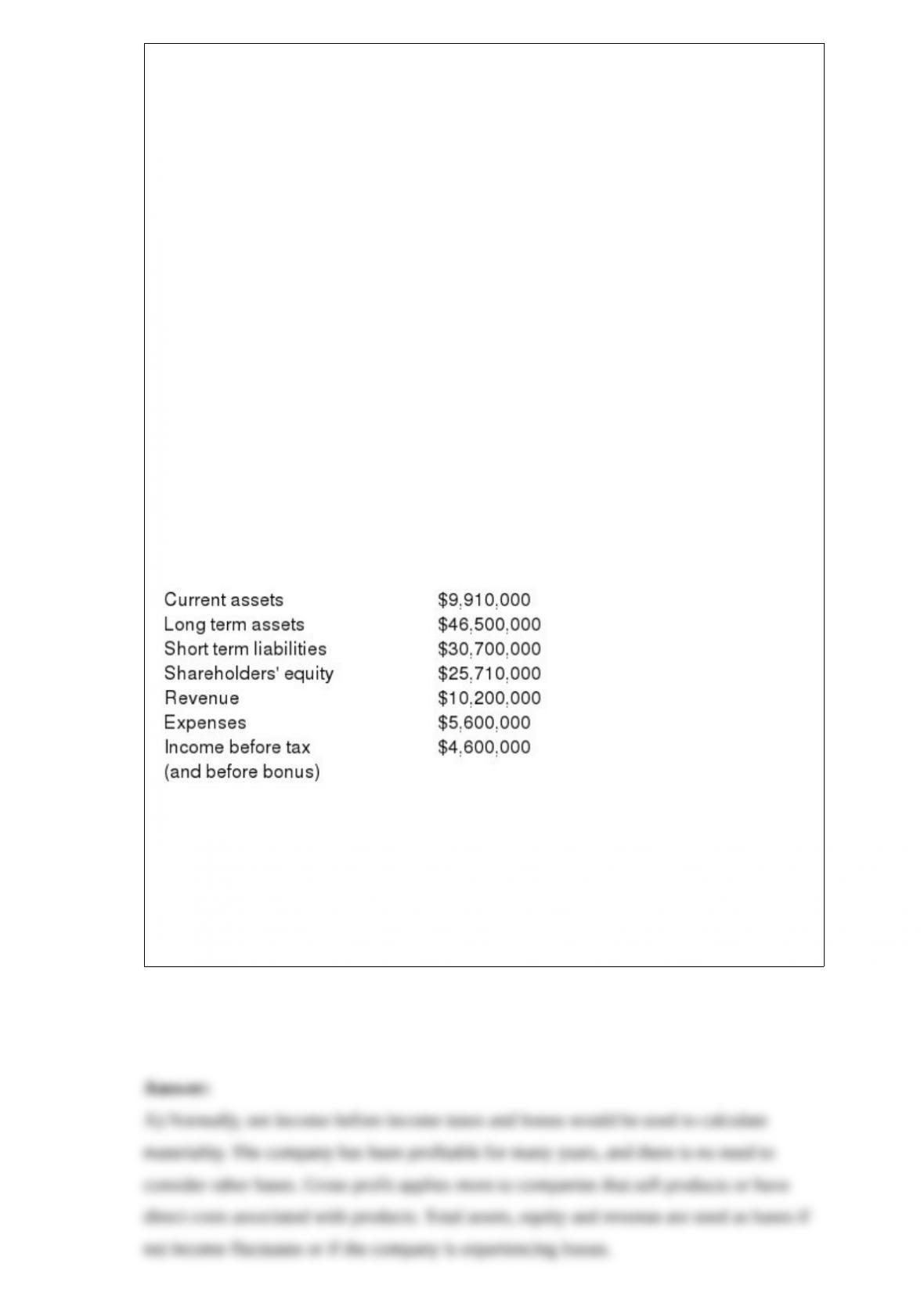

Selected financial information is as follows:

Required:

A) Which base would you use to calculate materiality? Why?

B) Calculate materiality. Choose a specific number, and explain why you chose that

amount.

The use of the term “reasonable assurance” is intended to indicate that an audit cannot

be expected to

A) completely eliminate the possibility that a material error or fraud exists.

B) consider or search for minor errors.

C) be compliant with the generally accepted accounting principles for every account.

D) provide assurance of no material errors or irregularities to investors who are using

the financial statements for investment decisions.

Radio Supplies Limited sells parts and components to organizations that repair radios

and other forms of audio equipment. It has many parts on its inventory listing at cost

that were purchased up to fifteen years ago. Some of these parts have not seen any

movement in the last ten years. The general balance-related audit objective affected by

this activity is

A) completeness.

B) accuracy.

C) valuation.

D) existence.

After completing tests of key controls, the auditor should review the results and

consider whether

A) the planned degree of reliance on internal controls is justified.

B) the audit evidence obtained from the study of internal controls can provide a

reasonable basis for an opinion.

C) further study of internal controls is likely to justify any restriction of tests of details

of balances.

D) sufficient knowledge has been obtained about the entity’s entire internal control

structure.

As a result of management’s refusal to permit the auditor to physically examine

inventory, the auditor has not accumulated sufficient evidence to conclude whether

financial statements are stated in accordance with ASPE (Accounting Standards for

Private Enterprises). The auditor must depart from the unqualified audit report because

A) the financial statements have not been prepared in accordance with GAAP.

B) the scope of the audit has been restricted by circumstances beyond either the client’s

or auditor’s control.

C) the auditor has lost independence.

D) the scope of the audit has been restricted by the client.

Receipt of ordered materials by the receiving department will generate the completion

of a form called the

A) receiving report.

B) materials requisition.

C) bill of lading.

D) inventory acquisition summary.

There are three main types of revenue manipulations. Which of the following revenue

manipulations affects the valuation objective?

A) recording subsequent period sales as current period sales

B) the use of “bill and holds” (goods are invoiced but not shipped)

C) understatement of bad debts

D) creation of fictitious sales that are misclassified as revenue

A procedure that would most likely be used by an auditor in performing tests of control

procedures that involve segregation of functions and that leave no transaction trail is

A) inspection.

B) observation.

C) reperformance.

D) reconciliation.

XYZ Company uses standard costs for allocating costs to work-in-process and finished

goods inventory. What internal control is required with respect to these costs to ensure

proper valuation of inventory?

A) procedures must be designed to keep the standards updated for changes in

production processes and costs

B) computer software should be used to make sure that the standard costs are properly

updated into the inventory item master file

C) input edit routines should be used to help detect input data entry errors for the entry

of the standard costs

D) standard costs should be used to provide a value for inventory every month by

calculating cost times quantity on hand

Sarbanes-Oxley in the U.S. and regulatory reporting requirements in Canada provide

the clout to make management directly responsible for the financial statements. What is

one of the ways that this is implemented in the CASs (Canadian Auditing Standards)?

A) all listed company management must certify the accuracy of the evidence provided

B) management must implement and carry out development of high quality internal

controls

C) management must acknowledge and understand its responsibilities

D) companies must use internal auditors to assess the quality of the financial statements

The auditor of ABC Ltd. has concluded that there are significant risks of misstatement

of revenue at the company, with potential overstatement of revenue. Which of the

following audit tests should the auditor conduct to address this significant risk?

A) control tests of authorization, to ensure that credit limits for sales are all approved by

the sales manager

B) analytical review of sales, comparing sales trends over the last five years by division

and to the industry

C) examination of sales after the year end to quantify potential cut-off errors (income

from the subsequent period included in the current year)

D) risk assessment procedures, looking carefully at inherent risks associated with the

handling of cash in the sales cycle

The main focus taken by the auditor in verifying liability balances is on the discovery of

A) liabilities posted to the wrong account.

B) overstated liabilities.

C) understated or omitted liabilities.

D) overstated or extraneous liabilities.

One of the ways to prevent the use of fictitious suppliers to steal company funds is by

A) having adequate network access controls to prevent unauthorized access to

transaction files.

B) ensuring that accounts payable programs are available only in source code.

C) having software automatically check for duplicate invoice numbers before payment.

D) having authorized personnel carefully scrutinize documentation supporting

payments.

Confirmations from outside organizations such as banks and law firms are

A) a highly regarded and often-used type of evidence.

B) expensive and rarely used during the audit.

C) difficult to obtain and infrequently required.

D) internal documents that provide low quality evidence.