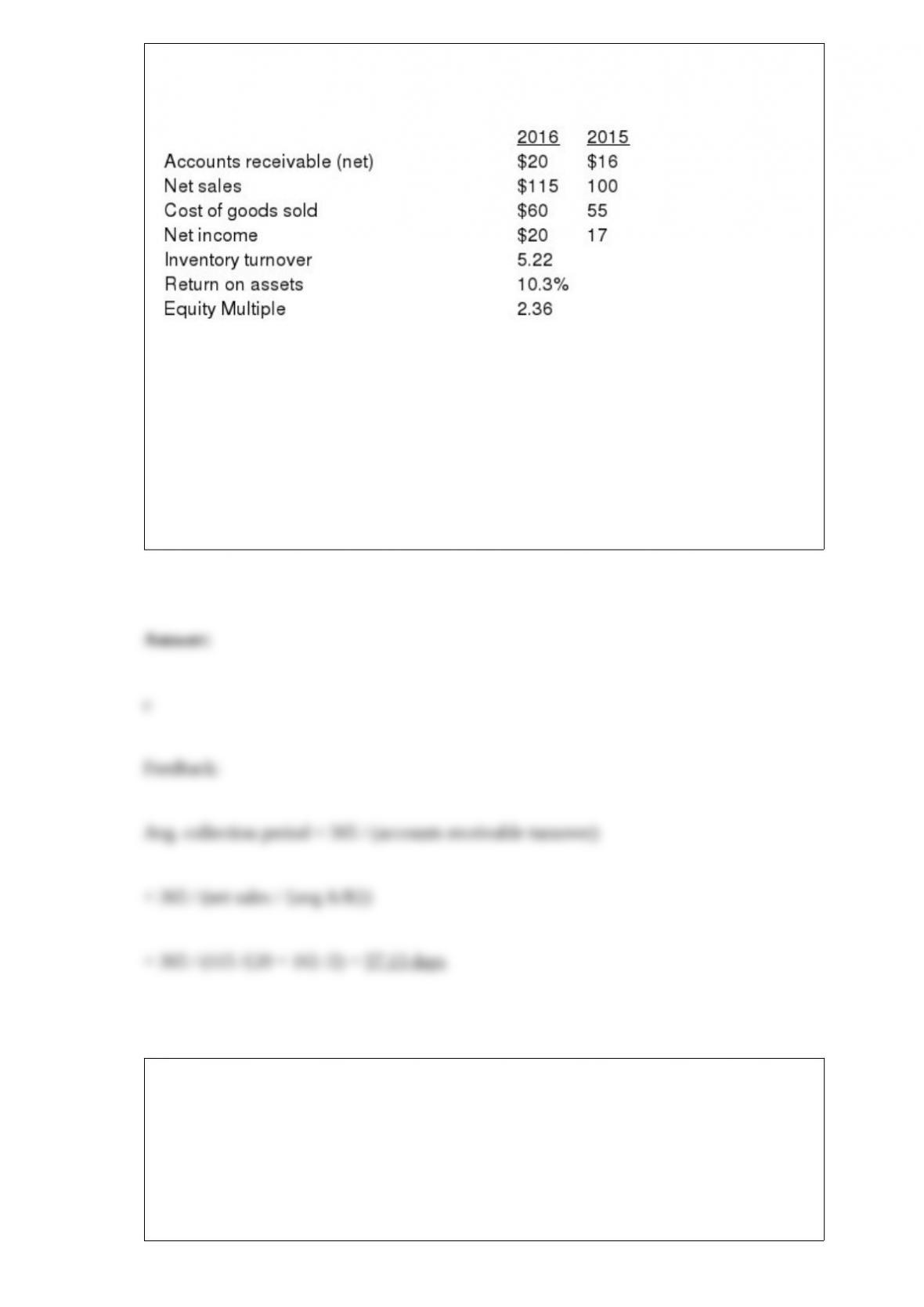

Excerpts from Dowling Company’s December 31, 2016 and 2015, financial statements

and key ratios are presented below (all numbers are in millions):

Dowling’s 2016 average collection period is (rounded):

a. 50 days.

b. 63 days.

c. 57 days.

d. 51 days.

Basic earnings per share is computed using:

a. The actual number of common shares outstanding at the end of the year.

b. A weighted-average of preferred and common shares.

c. The number of common shares outstanding plus potential common shares.

d. Weighted-average common shares outstanding for the year.

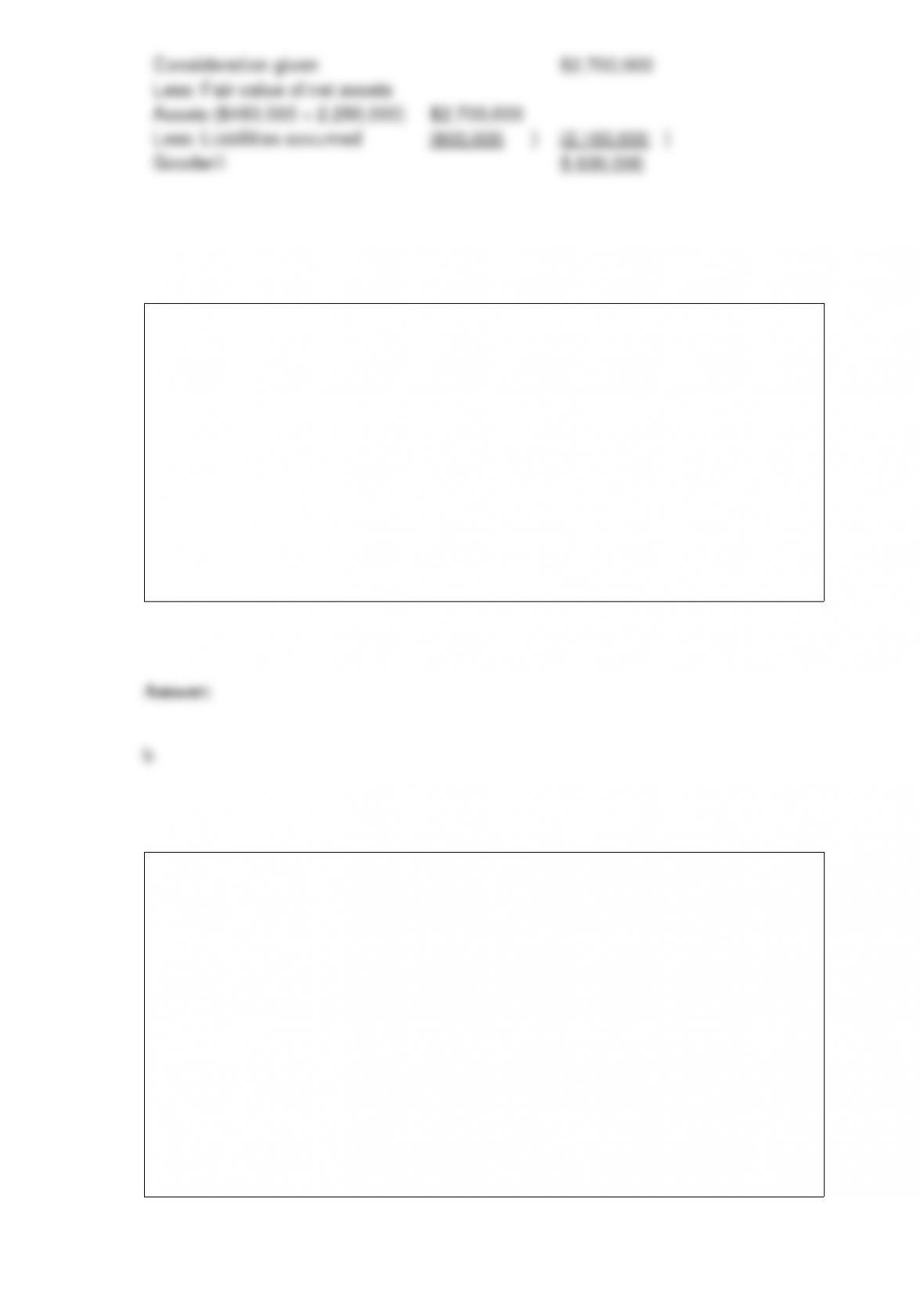

Juliana Corporation purchased all of the outstanding stock of Caldwell Inc., paying

$2,700,000 cash. Juliana assumed all of the liabilities of Caldwell. Book values and fair

values of acquired assets and liabilities were:

Juliana would record goodwill of:

a. $1,180,000.

b. $ 600,000.

c. $ 880,000.

d. $ 100,000.

In a recent annual report, Apple Computer reported the following in one of its

disclosure notes: “Warranty Expense: The Company provides currently for the

estimated cost for product warranties at the time the related revenue is recognized.'”

This note exemplifies Apple’s use of:

a. Conservatism.

b. The matching principle.

c. Realization principle.

d. Economic entity.

If a company uses the balance sheet approach to estimate bad debt expense, bad debt

expense for a period can be determined by:

a. Multiplying net credit sales by the bad debt experience ratio.

b. Adding the beginning balance in the allowance for uncollectible accounts to the

provision for uncollectible accounts and deducting the desired ending balance in the

allowance for uncollectible accounts.

c. Multiplying ending accounts receivable in each age category by the expected loss

ratio for each age category.

d. Taking the difference between the unadjusted balance in the allowance account and

the desired balance.

A long-term liability should be reported as a current liability in a classified balance

sheet if the long-term debt:

a. Is callable by the creditor.

b. Is secured by adequate collateral.

c. Will be refinanced with stock.

d. Will be refinanced with debt.

Under IFRS, components of other comprehensive income:

a. Can be reported as part of a single statement of comprehensive income.

b. Are not permitted to be reported.

c. Must be reported in a separate statement of comprehensive income.

d. Can be reported as part of a statement of shareholders’ ‘equity.

The attribution approach required by GAAP for postretirement health care plans is to

assign:

a. An equal fraction of the EPBO to each year the employee is on the company payroll.

b. An equal fraction of the APBO to each year the employee is on the company payroll.

c. An equal fraction of the APBO to each year of service from the employee’s hire date

to the employee’s full eligibility date.

d. An equal fraction of the EPBO to each year of service from the employee’s hire date

to the employee’s full eligibility date.

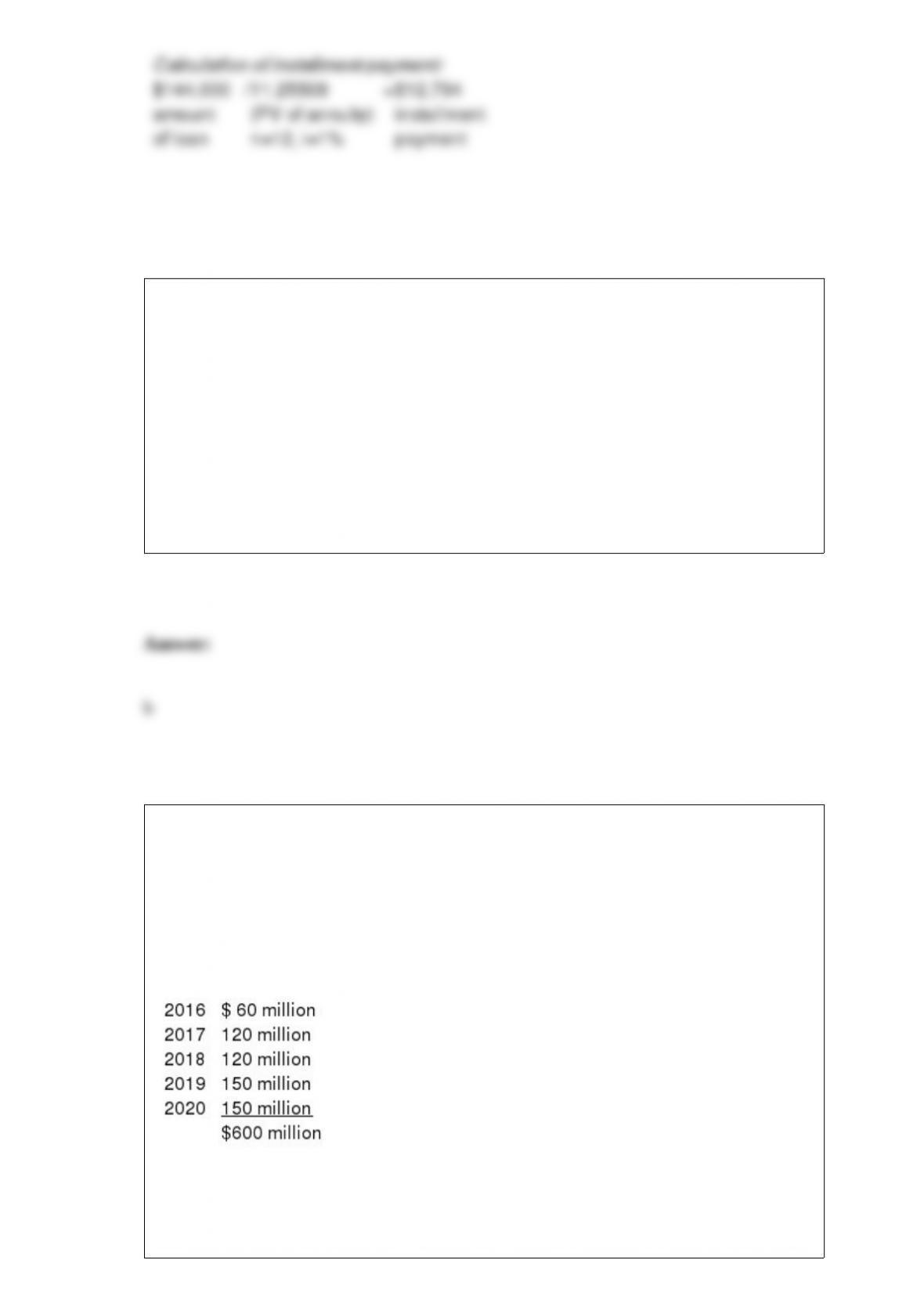

Green Industries purchased a machine from Cyan Corporation on October 1, 2016. In

payment for the $144,000 purchase, Green issued a one-year installment note to be paid

in equal monthly payments at the end of each month. The payments include interest at

the rate of 12%. Monthly installment payments are closest to:

a. $12,000.

b. $12,445.

c. $12,668.

d. $12,794.

Which of the accounting changes listed below is more associated with financial

statements prepared in accordance with U.S. GAAP than with International Financial

Reporting Standards (IFRS)?

a. Change in estimated useful life of depreciable assets.

b. Change from the FIFO method of costing inventories to the LIFO method.

c. Change in depreciation method.

d. Change in reporting entity.

Isaac Inc. began operations in January 2016. For certain of its property sales, Isaac

recognizes income in the period of sale for financial reporting purposes. However, for

income tax purposes, Isaac recognizes income when it collects cash from the buyer’s

installment payments.

In 2016, Isaac had $600 million in sales of this type. Scheduled collections for these

sales are as follows:

Assume that Isaac has a 30% income tax rate and that there were no other differences in

income for financial statement and tax purposes.

Ignoring operating expenses, what deferred tax liability would Isaac report in its

year-end 2016 balance sheet?

a. $18 million

b. $162 million

c. $180 million

d. $540 million

On December 31, 2015, Coolwear, Inc. had a balance in its prepaid insurance account

of $48,400. During 2016, $86,000 was paid for insurance. At the end of 2016, after

adjusting entries were recorded, the balance in the prepaid insurance account was

42,000. Insurance expense for 2016 would be:

a. $ 6,400.

b. $134,400.

c. $ 86,000.

d. $ 92,400.

On February 1st, H&B Bank originated a loan for $50,000 at an interest rate of 7.2%.

On March 15th, an interest payment of $300 was received. Which of the following best

describes when interest revenue should be recognized?

a. At a point in time (February 1st)

b. At a point in time (March 15th)

c. At a point in time (March 31st)

d. Over time

Use I = Increase, D = Decrease, or N = No effect, to indicate the effect on retained

earnings for each of the listed transactions.

____ A net loss for the year.

____ A stock split effected in the form of a stock dividend.

____ A stock split in which the par per share is reduced (but not effected in the form of

a stock

dividend).

____ Declaration of a 5% stock dividend.

____ Declaration of a cash dividend.

____ Issue stock for noncash assets.

____ Payment of previously declared cash dividend.

____ Retirement of common stock at a cost greater than the original issue price.

____ Retirement of common stock at a cost less than the original issue price.

____ Resale of treasury stock for less than book value assuming no previous

treasury stock sales.

We record and report most changes in accounting principle retrospectively, but

sometimes report the changes prospectively. Explain when it is appropriate to report the

changes prospectively. Provide examples.

Cash is the most liquid of all assets but is not always reported under current assets.

Explain this statement.

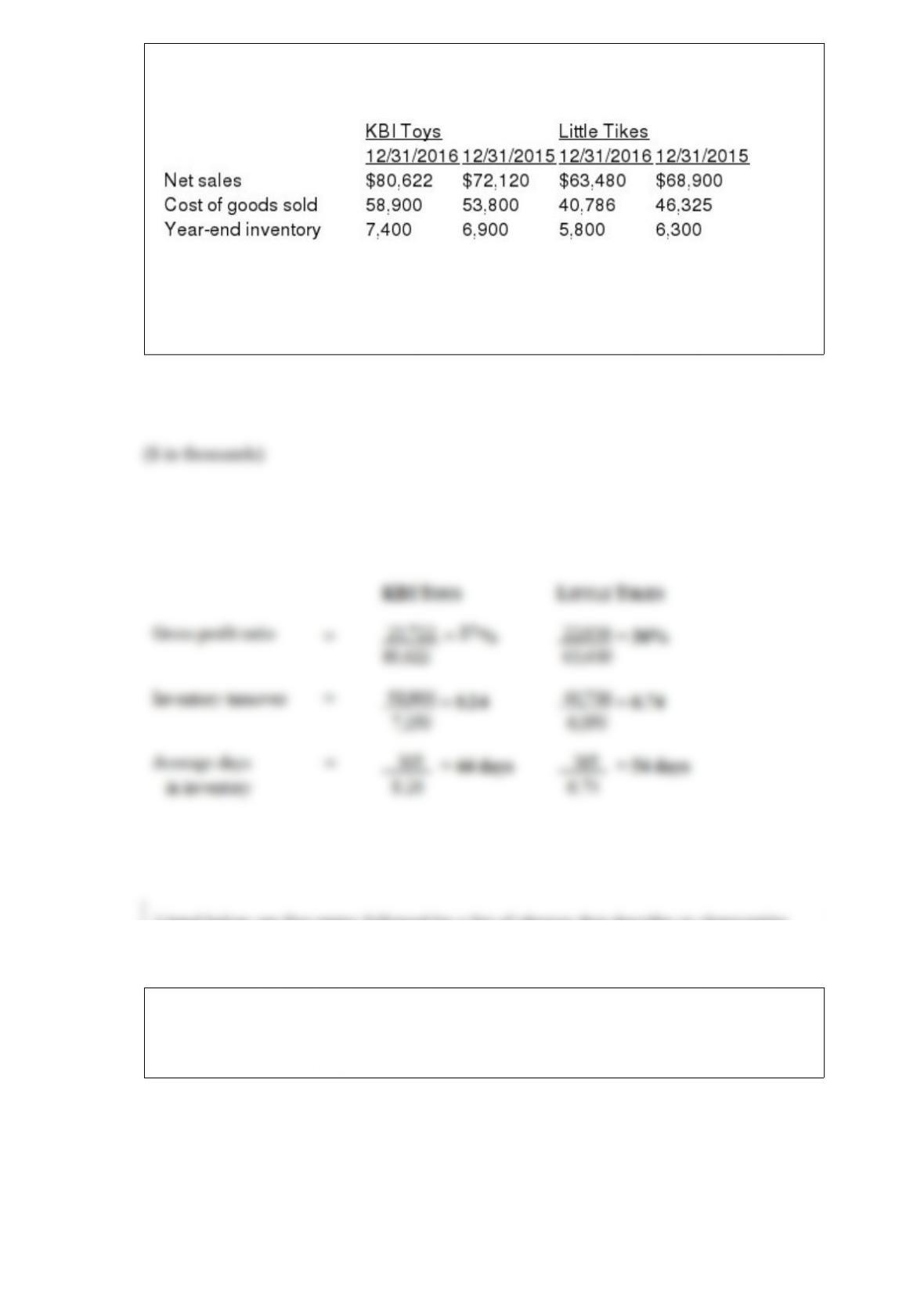

The table below contains selected financial information from recent financial

statements of KBI Toys and Little Tikes Adventure Toys, Inc., two toy manufacturing

companies ($ in thousands):

Required:

Calculate the 2016 gross profit ratio, inventory turnover ratio, and the average days in

inventory for the two companies (rounded).

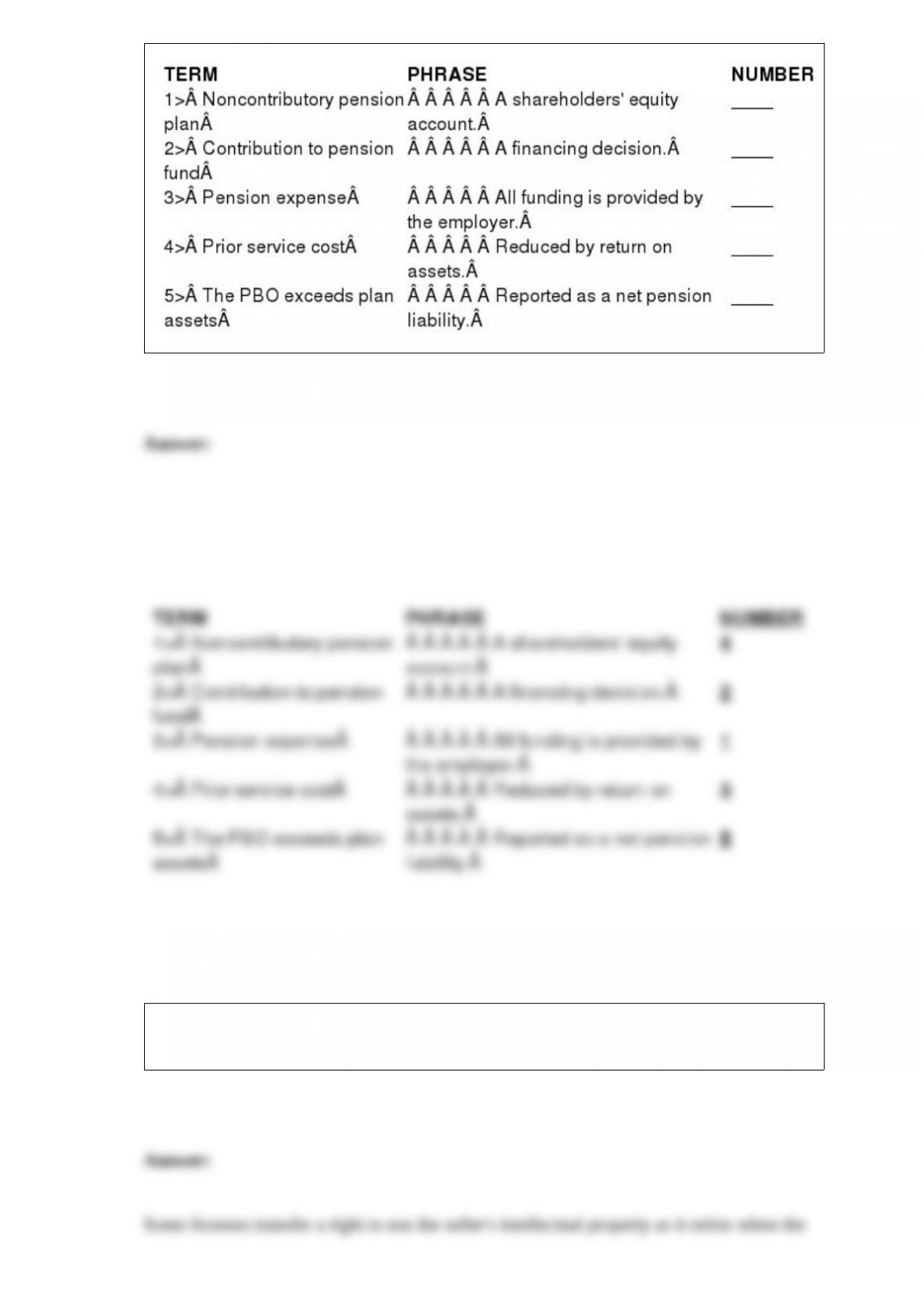

Listed below are five terms followed by a list of phrases that describe or characterize

each of the terms. Match each phrase with the most correct term by placing the number

designating that term in the space provided.

Briefly explain the circumstances in which license revenue is recognized over time

versus at a point in time. Provide an example of each.

Briefly describe how materiality is featured in the conceptual framework.

Cool Globe Inc. entered into two transactions, as follows: 1> Purchased equipment

paying $20,000 down and signed a noninterest-bearing note requiring the balance to be

paid in four annual installments of $20,000 on the anniversary date of the contract.

Based on Cool Globe’s 12% borrowing rate for such transactions, the implicit interest

cost is $19,253.

2> Purchased a tract of land in exchange for $10,000 cash down payment and a

noninterest-bearing note requiring five $10,000 annual payments, with the first annual

payment in one year. The fair value of the land is $46,000.

Required:

Prepare the journal entries for these transactions.

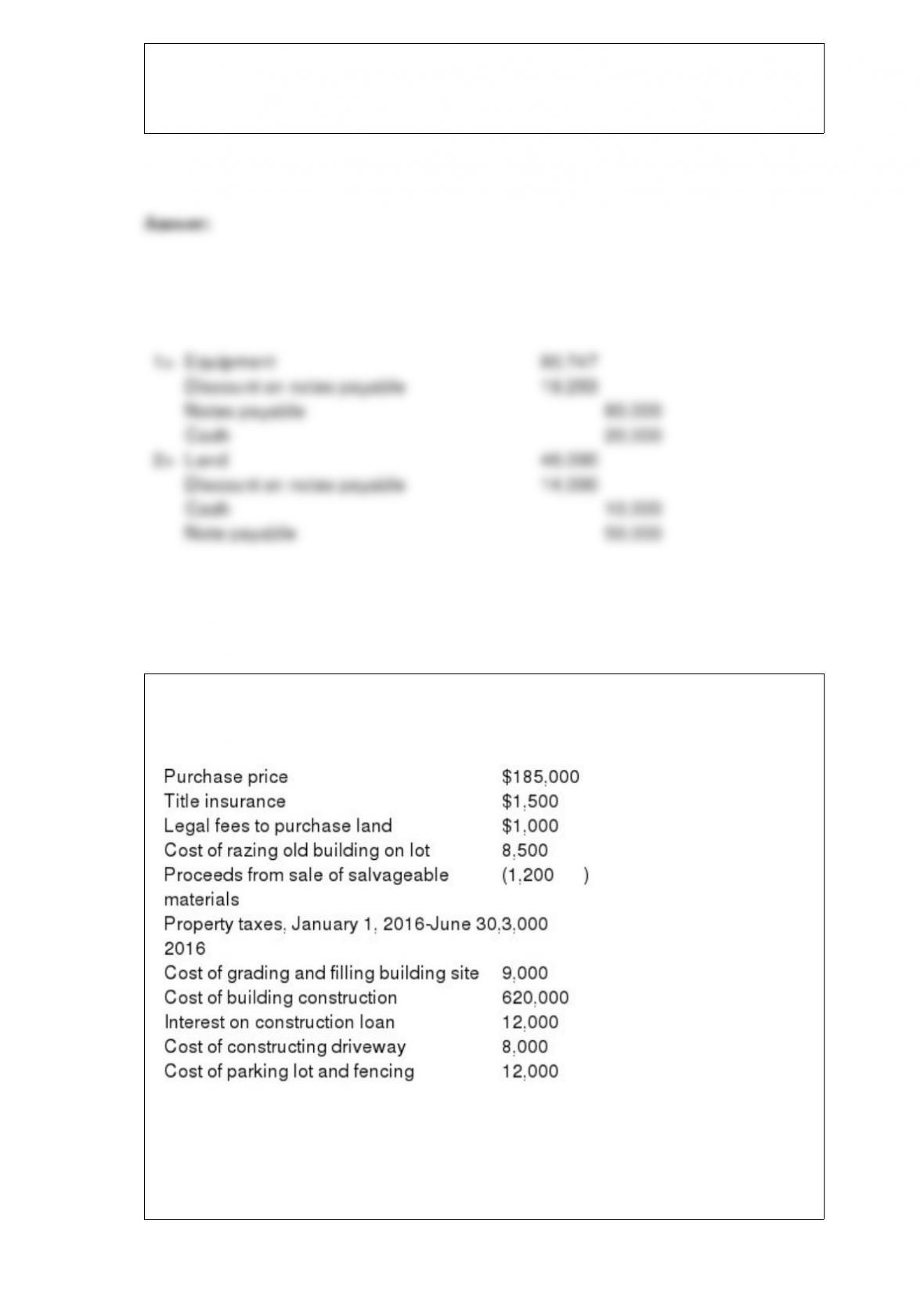

On July 1, 2016, Jekel & Hyde Inc. purchased land and incurred other costs relative to

the construction of a new warehouse. A summary of economic activities is listed below:

Required:

Indicate the accounts that would be affected by the above transactions and the resulting

balance in each account. Apply the interest on the construction loan to the cost of the

building only.