A small stock dividend is defined as one that is: A. Less than or equal to 40%.

B. Less than 40%.

C. Less than or equal to 10%.

D. Less than 25%.

Answer:

The following information relates to Franklin Freightways for its first year of

operations (data in millions of dollars):

The applicable tax rate is 40%. There are no other temporary or permanent differences.

Franklin Freightways experienced ($ in millions) a current: A. Tax liability of $66.

B. Tax liability of $36.

C. Tax liability of $70.6.

D. Tax benefit of $10 due to the NOL.

Answer:

When recognizing compensation under a stock option plan, unanticipated forfeitures are

treated as: A. A change in accounting principle.

B. A loss.

C. An income item.

D. A change in estimate.

Answer:

Lake Power Sports sells jet skis and other powered recreational equipment. Customers

pay one-third of the sales price of a jet ski when they initially purchase the ski, and then

pay another one-third each year for the next two years. Because Lake has little

information about the ability to collect these receivables, it uses the installment method

for revenue recognition. In 2012, Lake began operations and sold jet skis with a total

price of $900,000 that cost Lake $450,000. Lake collected $300,000 in 2012, $300,000

in 2013, and $300,000 in 2014 associated with those sales. In 2013, Lake sold jet skis

with a total price of $1,500,000 that cost Lake $900,000. Lake collected $500,000 in

2013, $400,000 in 2014, and $400,000 in 2015 associated with those sales. In 2015,

Lake also repossessed $200,000 of jet skis that were sold in 2013. Those jet skis had a

fair value of $75,000 at the time they were repossessed.

In 2012, Lake would recognize realized gross profit of: A. $150,000.

B. $0.

C. $300,000.

D. $450,000.

Answer:

The shareholders’ equity of Green Corporation includes $200,000 of $1 par common

stock and $400,000 par value of 6% cumulative preferred stock. The board of directors

of Green declared cash dividends of $50,000 in 2013 after paying $20,000 cash

dividends in each of 2012 and 2011. What is the amount of dividends common

shareholders will receive in 2013? A. $18,000.

B. $26,000.

C. $28,000.

D. $32,000.

Answer:

Interest payments and interest received must be reported as operating cash flows using:

A. U.S. GAAP.

B. IFRS.

C. Both U.S. GAAP and IFRS.

D. Neither U.S. GAAP nor IFRS.

Answer:

Cutter Enterprises purchased equipment for $72,000 on January 1, 2013. The equipment

is expected to have a five-year life and a residual value of $6,000.

Using the sum-of-the-years’-digits method, depreciation for 2014 and book value at

December 31, 2014, would be: A. $19,200 and $30,800.

B. $17,600 and $26,400.

C. $19,200 and $28,800.

D. $17,600 and $32,400.

Answer:

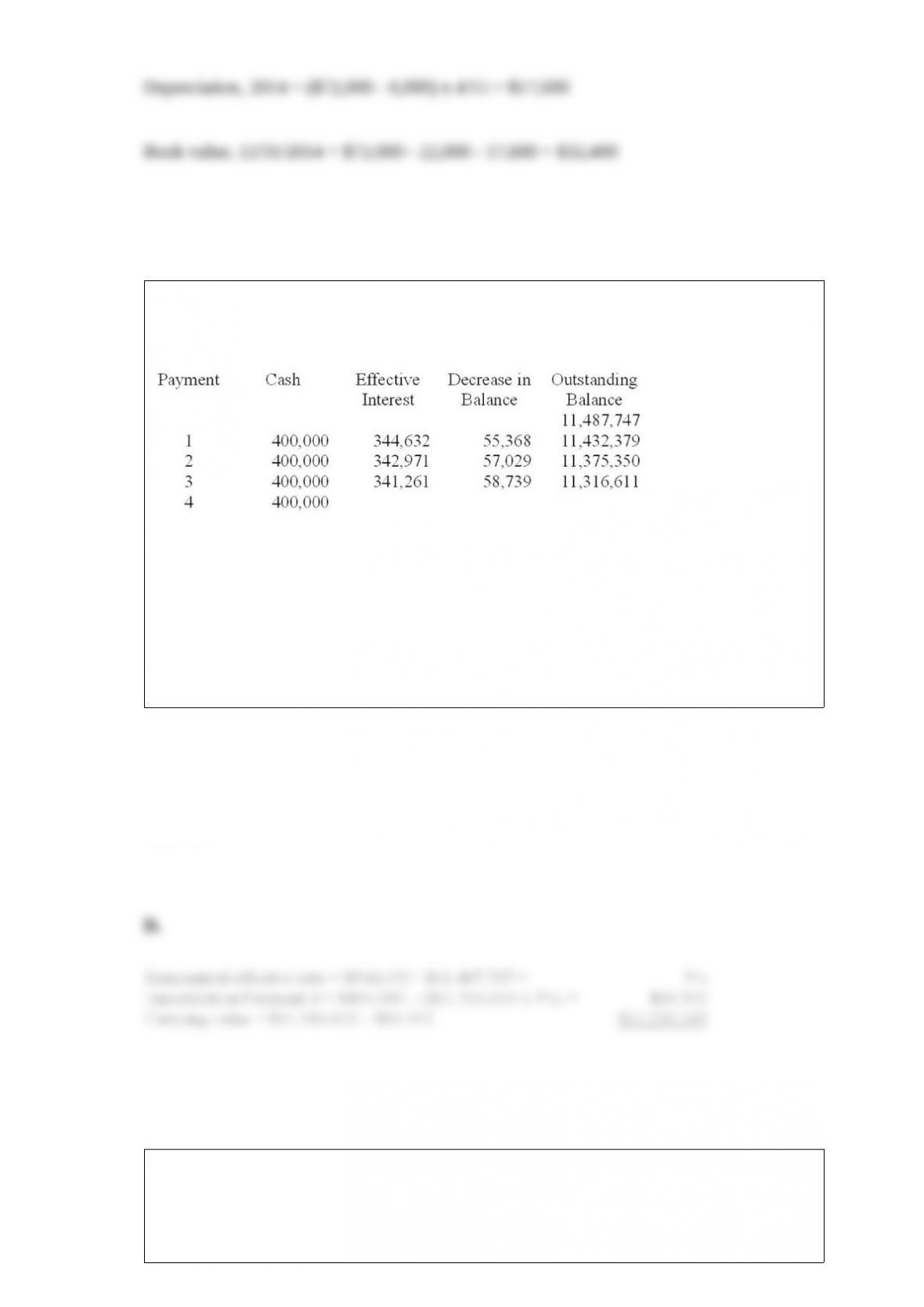

Prescott Corporation issued ten thousand $1,000 bonds on January 1, 2013. The bonds

have a 10-year term and pay interest semiannually. This is the partial bond amortization

schedule for the bonds.

What is the carrying value of the bonds as of December 31, 2014? A. $11,432,379.

B. $11,375,350.

C. $11,316,611.

D. $11,256,109.

Answer:

Which of the following is not true about the “fair value through other comprehensive

income” approach for accounting for investments under IFRS No. 9? A. Allowed for

debt investments.

B. Includes unrealized gains in other comprehensive income.

C. Does not require reclassification of realized gains from other comprehensive income.

D. Allowed for equity investments.

Answer:

On June 30, 2013, Prego Equipment purchased a precision laser-guided steel punch that

has an expected capacity of 300,000 units and no residual value. The cost of the

machine was $450,000 and is to be depreciated using the units-of-production method.

During the six months of 2013, 24,000 units of product were produced. At the

beginning of 2014, engineers estimated that the machine can realistically be used to

produce only another 230,000 units. During 2014, 70,000 units were produced.

Prego would report depreciation in 2014 of: A. $135,230.

B. $126,000.

C. $108,000.

D. $105,000.

Answer:

Donated assets are recorded at: A. Zero (memo entry only).

B. The donor’s book value.

C. The donee’s stated value.

D. Fair value.

Answer:

Bumble Bee Co. had taxable income of $7,000, MACRS depreciation of $5,000, book

depreciation of $2,000, and accrued warranty expense of $400 on the books although no

warranty work was performed. What is Bumble Bee’s pretax accounting income? A.

$4,400.

B. $3,600.

C. $9,600.

D. $2,600.

Answer:

Under IFRS, components of other comprehensive income: A. Can be reported as part of

a single statement of comprehensive income.

B. Are not permitted to be reported.

C. Must be reported in a separate statement of comprehensive income.

D. Can be reported as part of a statement of shareholders’ equity.

Answer:

Listed below are five terms followed by a list of phrases that describe or characterize

each of the terms. Match each phrase with the correct term. 1) Securities held to

maturity

2) Impairment of securities available for sale

3) Losses of investee

4) Amortization of a patent that was obtained in a business acquisition

5) Unrealized holding gains and losses

A. Requires positive intent and ability

B. Reported in the income statement for trading securities

C. Requires recognition in the income statement if judged to be other than temporary

D. Recognized only to the extent of carrying value under the equity method

E. Reduces investment account under the equity method if its fair value is higher than

its book value

Answer:

Prepayments occur when:A. Cash flow precedes expense recognition.

B. Sales are delayed pending credit approval.

C. Customers are unable to pay the full amount due when goods are delivered.

D. Manufactured goods await quality control inspections.

Answer:

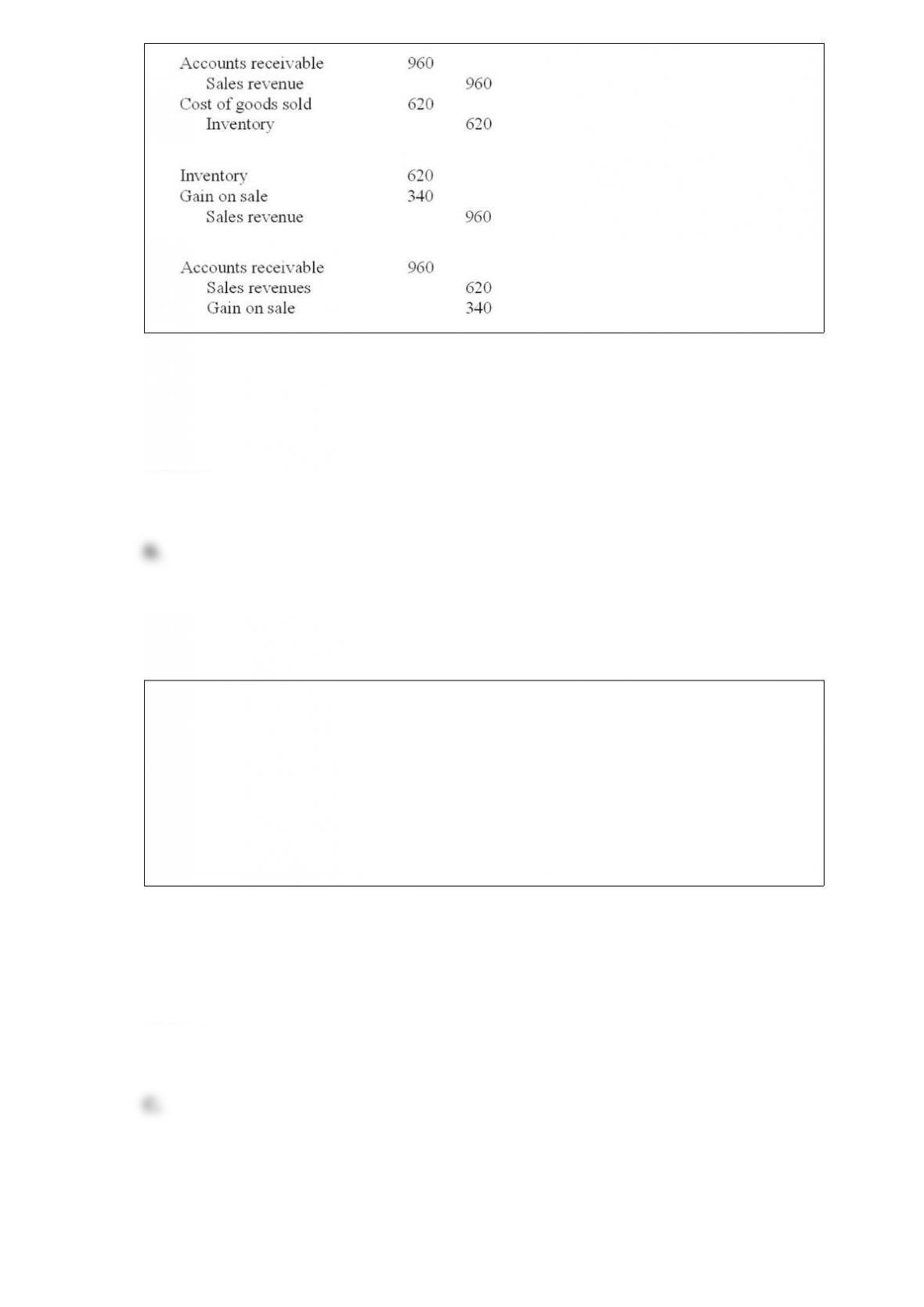

Davis Hardware Company uses a perpetual inventory system. How should Davis record

the sale of merchandise, costing $620 and sold for $960 on account? A.

B.

C.

D.

Answer:

Recognition of impairment for property, plant, and equipment is required if book value

exceeds: A. Fair value.

B. Present value of expected cash flows.

C. Undiscounted expected cash flows.

D. Accumulated depreciation.

Answer:

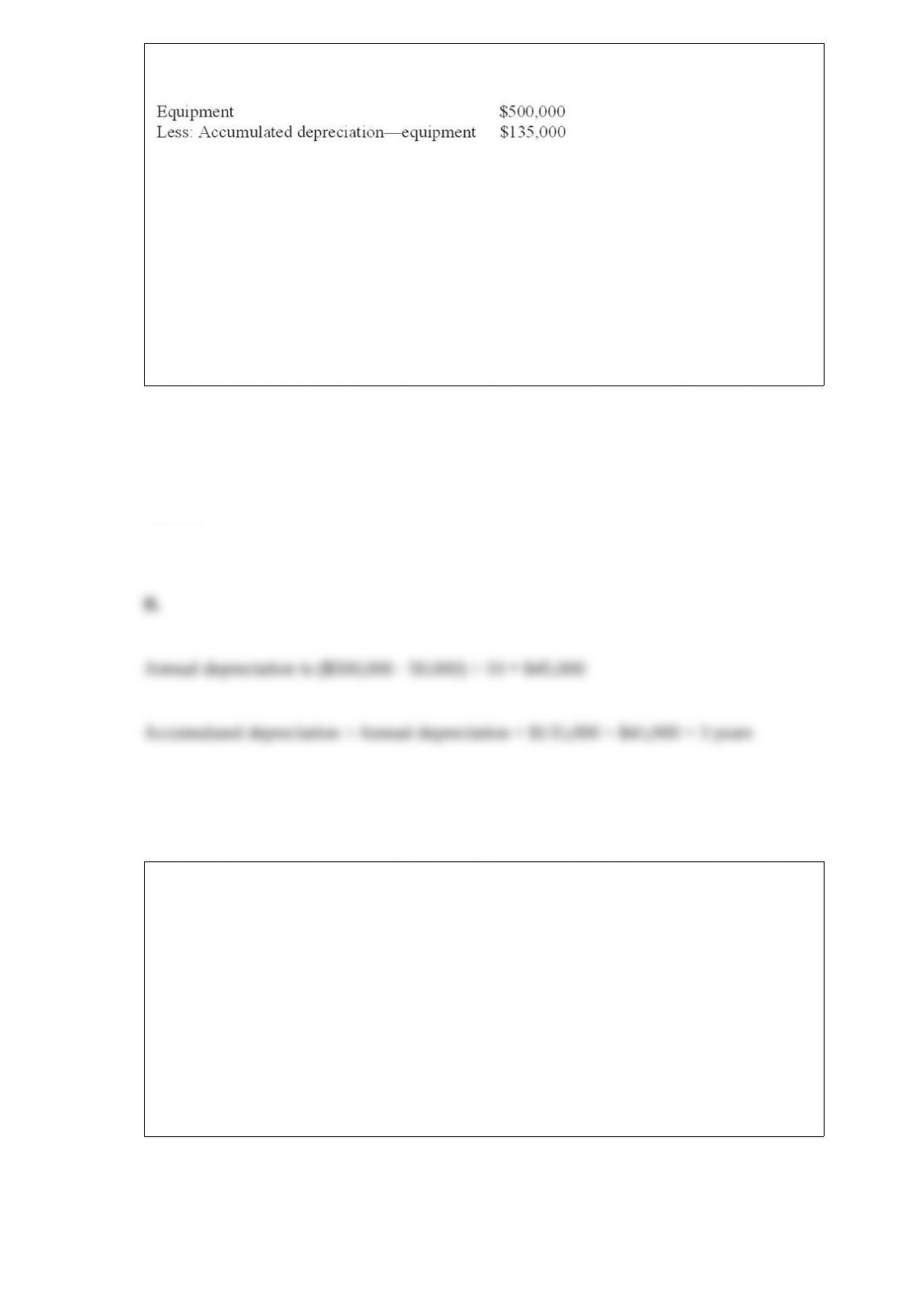

Jennings Advertising Inc. reported the following in its December 31, 2013, balance

sheet:

In a disclosure note, Jennings indicates that it uses straight-line depreciation over 10

years and estimates salvage value at 10% of cost. What is the average age of the

equipment owned by Jennings? A. 2.7 years.

B. 3 years.

C. 7 years.

D. 7.3 years.

Answer:

Beagle Corporation has 20,000 shares of $10 par common stock outstanding and 10,000

shares of $100 par, 6% cumulative, nonparticipating preferred stock outstanding.

Dividends have not been paid for the past two years. This year, a $300,000 dividend

will be paid. What are the dividends per share payable to preferred and common,

respectively? A. $6; $12.

B. $18; $6.

C. $6; $6.

D. None of the above is correct.

Answer:

Listed below are five terms followed by a list of phrases that describe or characterize

each of the terms with respect to accounting for investments under IFRS. Match each

phrase with the correct term by placing the letter designating the best term in the space

provided by the phrase. 1) Business model test

2) IFRS No. 9

3) Equity investments

4) Accounting mismatch

5) Fair value through other comprehensive income

A. One of the criteria that must be met under IFRS No. 9 to qualify for use of the

amortized cost method

B. Does not allow the “held-to-maturity” approach for debt investments

C. Can be accounted for as “fair value through profit and loss” or as “fair value through

other comprehensive income” under IFRS No. 9

D. Similar to available for sale investments, except realized gains and losses are not

reclassified into net income

E. One of the circumstances in which the fair-value option can be used under IFRS.

Answer:

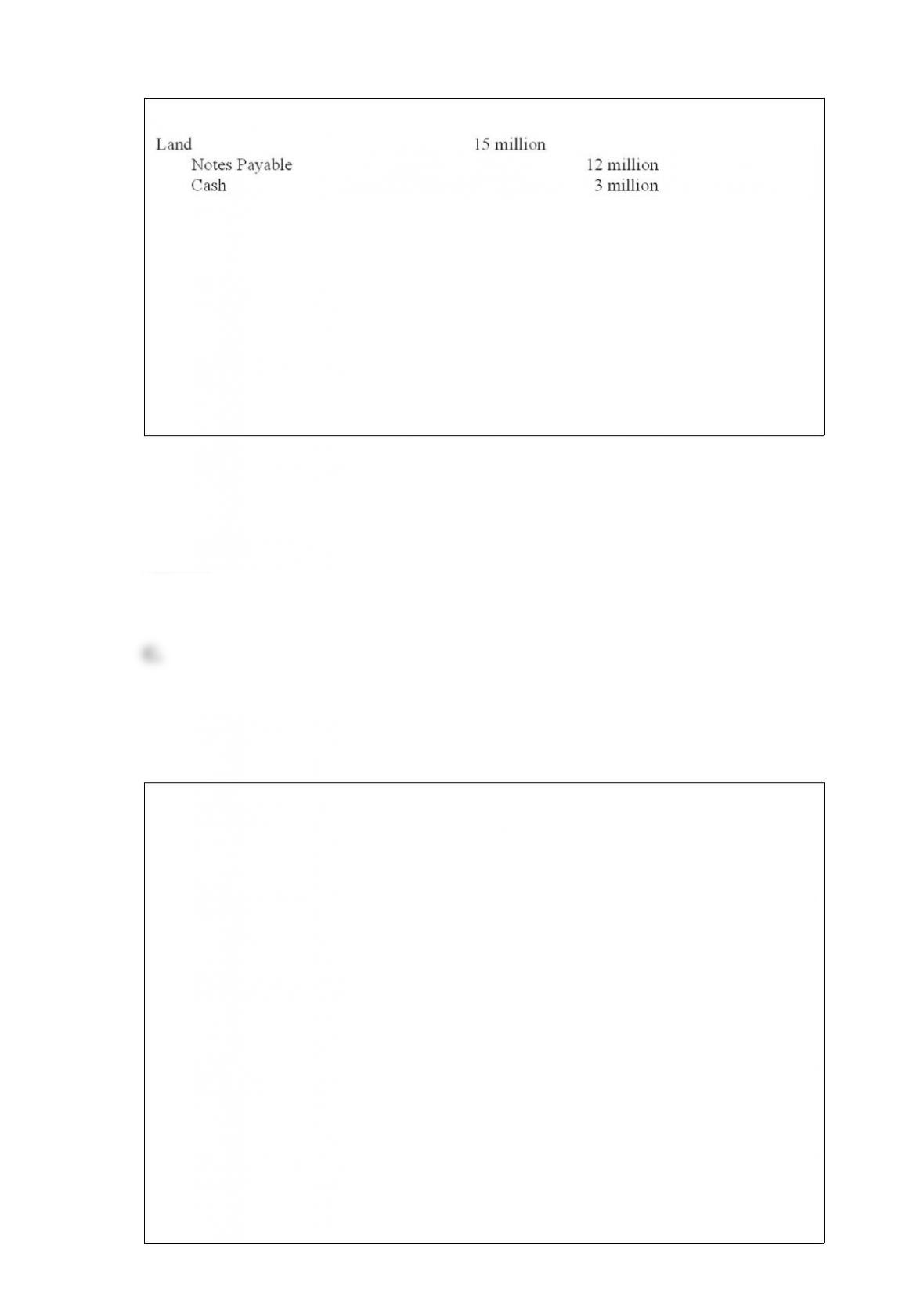

Rampart Inc. recorded the following transaction:

In the statement of cash flows, this would be reported as a: A. $3 million outflow from

investing activities.

B. $15 million outflow from investing activities.

C. $3 million outflow from investing activities and $12 million noncash investing and

financing activity.

D. None of the above is correct.

Answer:

Calstone, Inc., prepares a single, continuous statement of comprehensive income. The

following situations occurred during the company’s 2013 fiscal year:

1) An earthquake destroyed a manufacturing facility. The event is considered to be

unusual and infrequent in occurrence.

2) Land that had been held as an investment was sold and a gain was recognized.

3) Losses from foreign currency translation were recognized.

4) Interest revenue was recognized.

5) A division was sold that qualifies as a separate component according to GAAP

regarding discontinued operations.

6) Unrealized losses on investments.

7) Restructuring costs were incurred due to downsizing and reorganization of a

manufacturing facility.

Required:

For each situation, identify the appropriate reporting treatment from the list below

(consider each event to be material).

a) As a component of operating income.

b) As a nonoperating income item (other income or expense).

c) As a separately reported item.

d) As an item of other comprehensive income.

Answer:

Straight-line amortization of bond discount or premium: A. Can be used for

amortization of discount or premium in all cases and circumstances.

B. Provides the same amount of interest expense each period as does the effective

interest method.

C. Is appropriate for deep discount bonds.

D. Provides the same total amount of interest expense over the life of the bond issue as

does the effective interest method.

Answer:

On March 1, 2013, Doll Co. issued 10-year convertible bonds at 106. During 2016, the

bonds were converted into common stock when the market price of Doll’s common

stock was 500 percent above its par value. Doll prepares its financial statements

according to International Financial Reporting Standards (IFRS). On March 1, 2013,

cash proceeds from the issuance of the convertible bonds should be reported as: A. A

liability for the entire proceeds.

B. Paid-in capital for the entire proceeds.

C. Paid-in capital for the portion of the proceeds attributable to the conversion feature

and as a liability for the balance.

D. A liability for the face amount of the bonds and paid-in capital for the premium over

the par value.

Answer:

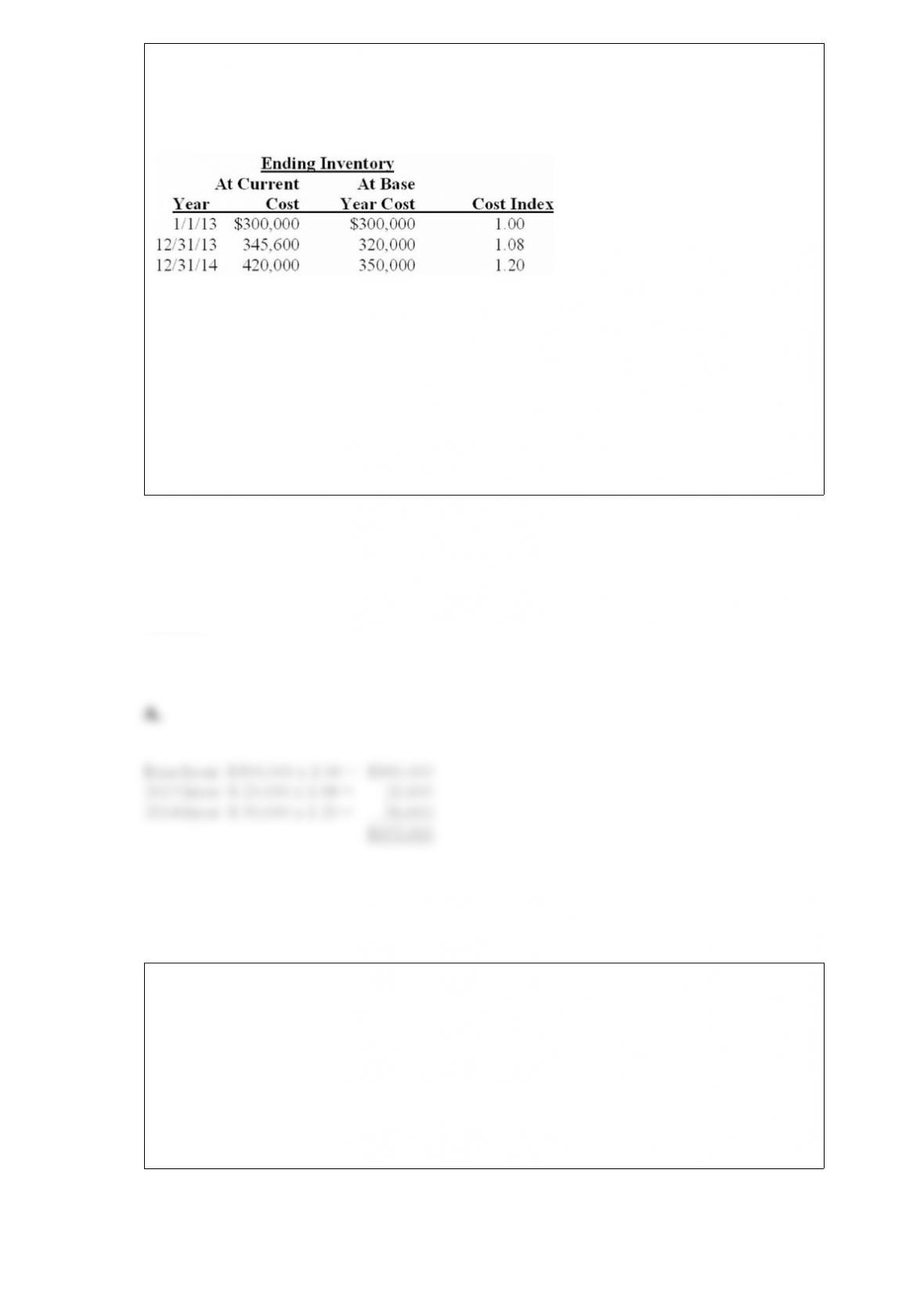

Bond Company adopted the dollar-value LIFO inventory method on January 1, 2013. In

applying the LIFO method, Bond uses internal cost indexes and the multiple-pools

approach. The following data were available for Inventory Pool No. 3 for the two years

following the adoption of LIFO:

Under the dollar-value LIFO method, the inventory at December 31, 2014, should be A.

$357,600.

B. $350,000.

C. $351,600.

D. None of the above.

Answer:

Which of the following causes a permanent difference between taxable income and

pretax accounting income? A. Advance collections of revenues.

B. MACRS depreciation method used for equipment.

C. The installment method used for sales of merchandise.

D. Interest earned on municipal securities.

Answer:

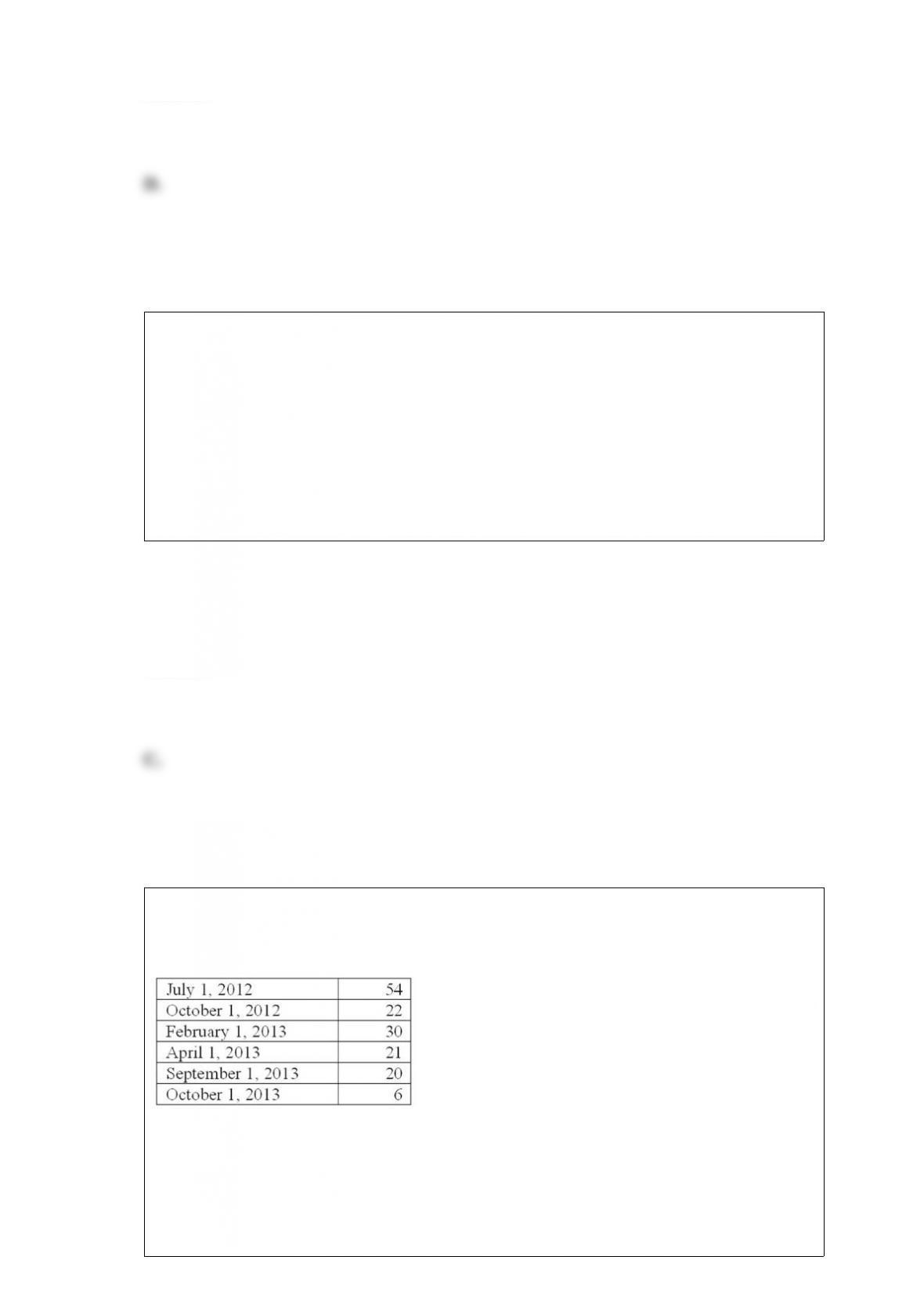

When the interest payment dates are March 1 and September 1, and notes are issued on

July 1, the amount of interest expense to be accrued at December 31 of the year of issue

would: A. Not be required.

B. Be for six months.

C. Be for four months.

D. Be for 10 months.

Answer:

On June 1, 2012, the Crocus Company began construction of a new manufacturing

plant. The plant was completed on October 31, 2013. Expenditures on the project were

as follows ($ in millions):

On July 1, 2012, Crocus obtained a $70 million construction loan with a 6% interest

rate. The loan was outstanding through the end of October, 2013. The company’s only

other interest-bearing debt was a long-term note for $100 million with an interest rate of

8%. This note was outstanding during all of 2012 and 2013. The company’s fiscal

year-end is December 31.

What is the amount of interest that Crocus should capitalize in 2013, using the specific

interest method (rounded to the nearest thousand dollars)? A. $7,248,000 (rounded).

B. $7,283,000 (rounded).

C. $8,740,000 (rounded).

D. None of the above is correct.

Answer:

The following partial information is taken from the comparative balance sheet of Levi

Corporation:

What was the amount of net income earned by Levi during 2013? A. $0.

B. $40 million.

C. $62 million.

D. Cannot be determined from the given information.

Answer:

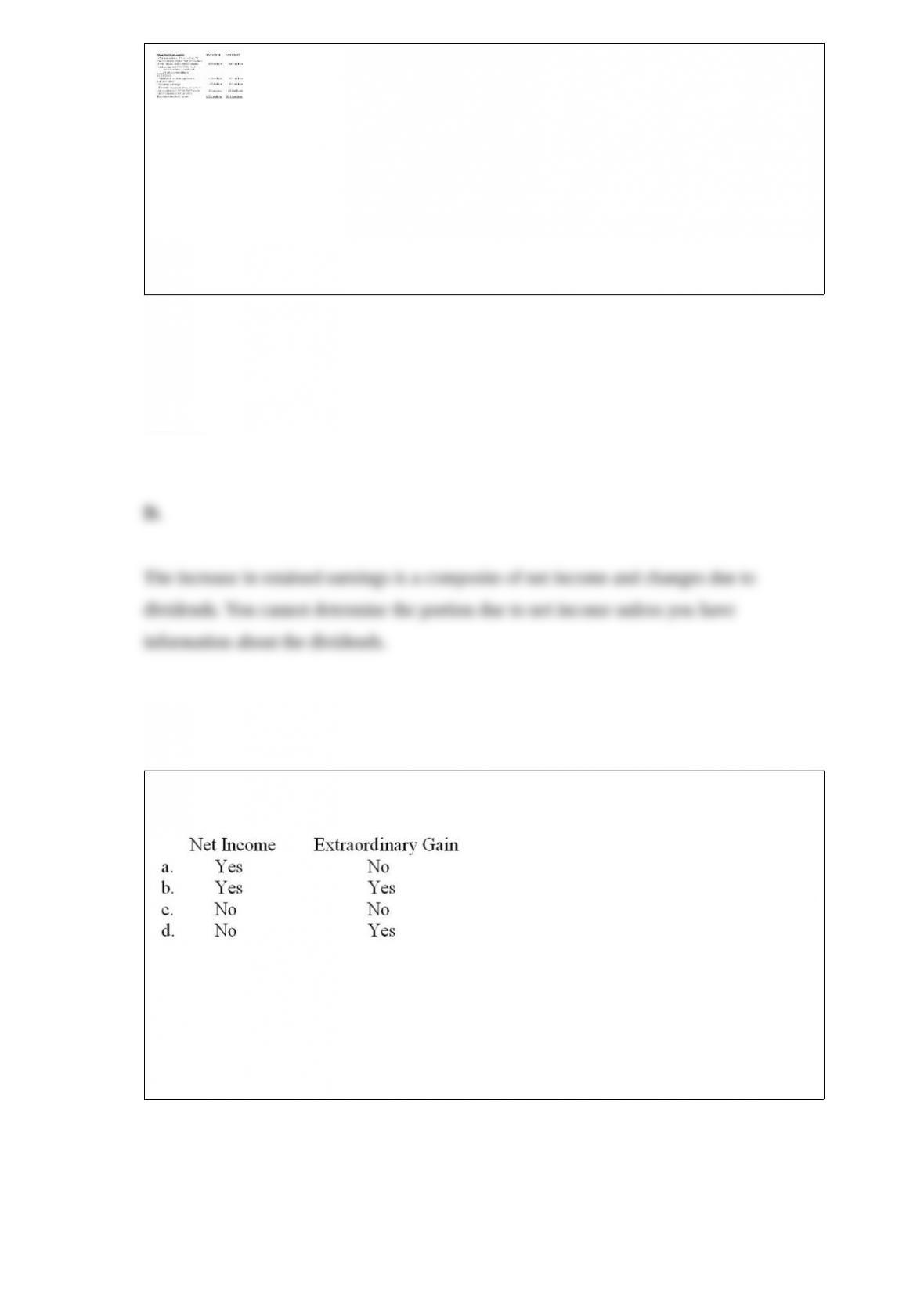

When a company’s income statement includes an extraordinary gain, the company

should report per share information on:

A. Option a

B. Option b

C. Option c

D. Option d

Answer:

On October 1, 2013, Chief Corporation declared and issued a 10% stock dividend.

Before this date, Chief had 80,000 shares of $5 par common stock outstanding. The

market value of Chief Corporation on the date of declaration was $10 per share. As a

result of this dividend, Chief’s retained earnings will: A. Decrease by $80,000.

B. Not change.

C. Decrease by $40,000.

D. Increase by $80,000.

Answer:

Which of the following is not reported as an adjustment to net income when using the

indirect method of computing net cash flows from operating activities? A. Cash

dividends paid.

B. A change in accounts receivable.

C. Depreciation.

D. A change in a prepaid expense.

Answer:

If the lessee and lessor use different interest rates to account for a capital lease, then: A.

Total expenses for the lessee will be different from the lessor’s total revenues.

B. Total expenses for the lessee will equal the lessor’s total revenues.

C. GAAP has been violated by at least one party.

D. The lessee will report more net income for the year.

Answer:

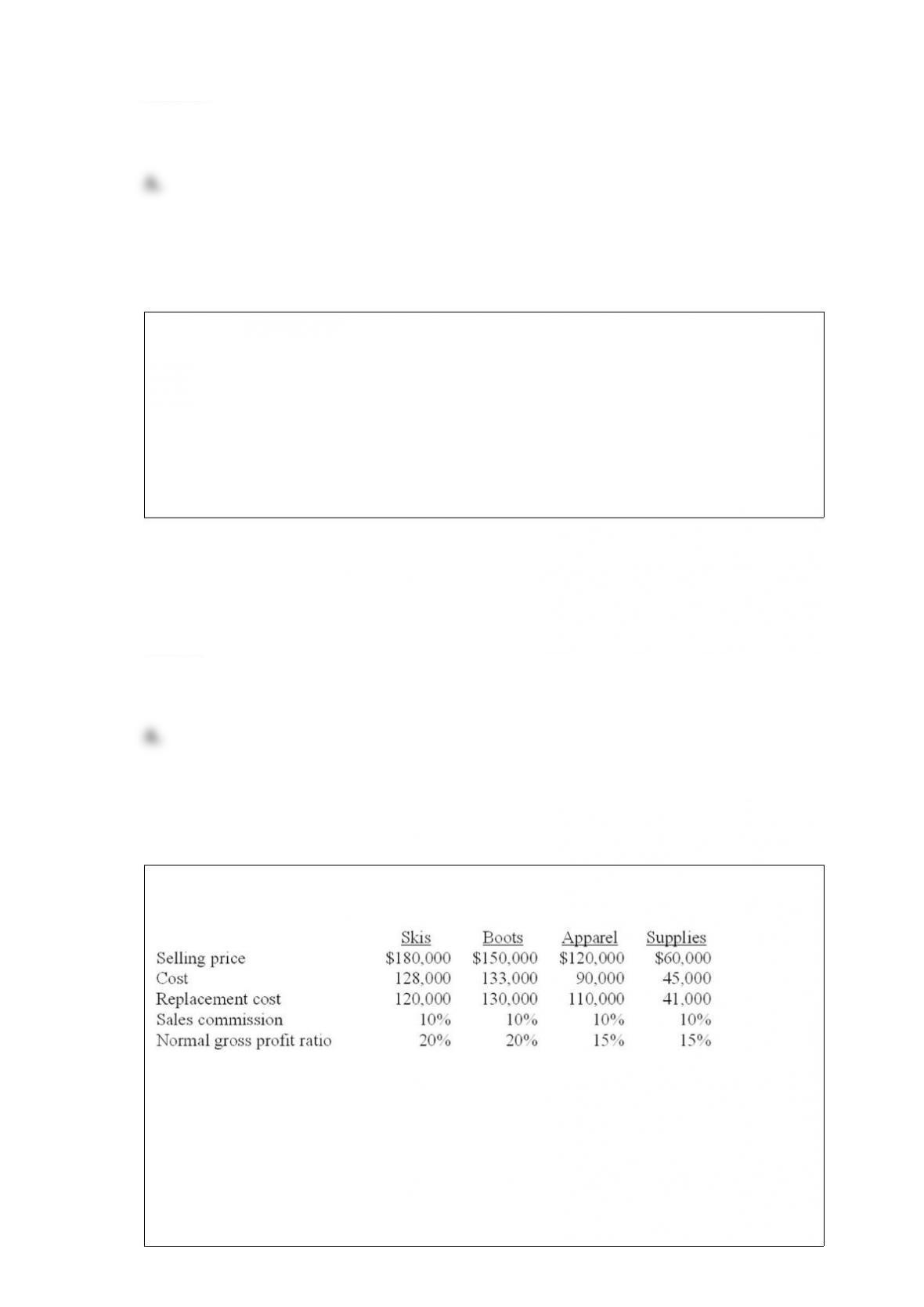

Data related to the inventories of Alpine Ski Equipment and Supplies is presented

below:

In applying the LCM rule, the inventory of boots would be valued at: A. $135,000.

B. $133,000.

C. $130,000.

D. $105,000.

Answer:

Red Corp. has a rate of return on assets of 10% and a debt/equity ratio of 2 to 1. Not

including any indirect effects on earnings, the immediate impact of retiring debt on

these ratios is a(n)

A. Option a

B. Option b

C. Option c

D. Option d

Answer:

Bank loans are often arranged in advance as lines of credit. What is a line of credit?

How do a committed and a noncommitted line of credit differ?

Answer:

Mozart Music Co. began operations in December of 2013. The company sold gift

certificates during December in various amounts totaling $1,600. The gift certificates

are redeemable for merchandise within three years of the purchase date. However,

experience within the industry predicts that 90% of gift certificates will be redeemed

within one year. Certificates totaling $500 were presented for redemption during 2013

as part of merchandise purchases having a total retail price of $750.

Required:

1) Determine the liability for gift certificates to be reported in the December 31, 2013,

balance sheet.

2) What is the appropriate classification (current or noncurrent) of the liabilities at

December 31, 2013? Show calculations.

Answer:

Why are earnings per share figures for prior years adjusted for stock splits and stock

dividends when data from prior years is presented in comparative financial statements?

Answer:

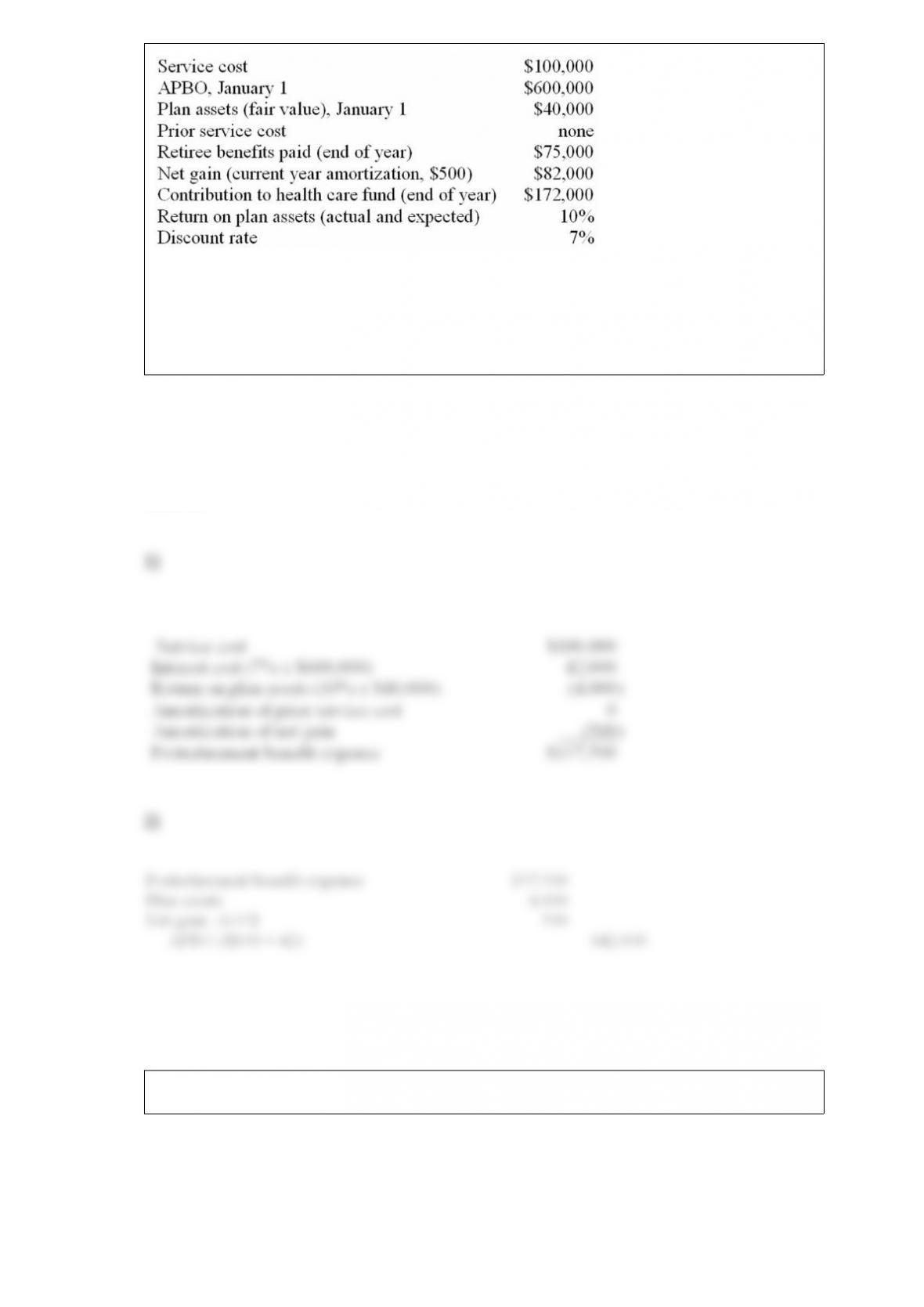

Data pertaining to the postretirement health care benefit plan of Amazing Delivery

Service include the following for the current calendar year:

Required:

1) Determine Amazing’s postretirement benefit expense for the current year.

2) Prepare the journal entry to record the benefit expense for the current year.

Answer:

How is a complex capital structure different from a simple capital structure?

Answer:

The following table presents a summary of ratio analysis for Uncle Joe’s Coffee, based

on the most recent 12 months and five-year comparisons of Uncle Joe’s with averages

in the restaurant industry and the services sector, respectively.

Using the information provided above, briefly summarize the operating performance of

Uncle Joe’s relative to its benchmark competitors.

Answer:

List the four financial statements most frequently provided to external users.

Answer:

XYZ Company had 200,000 shares of common stock outstanding on December 31,

2012. On July 1, 2013, XYZ issued an additional 50,000 shares for cash. On January 1,

2013, XYZ issued 20,000 shares of convertible preferred stock. The preferred stock had

a par value of $100 per share and paid a 5% dividend. Each share of preferred stock is

convertible into 8 shares of common. During 2013, XYZ paid the regular annual

dividend on the preferred and common stock. Net income for the year was $300,000.

Required:

Calculate XYZ’s basic and diluted earnings per share (rounded to 2 decimal places) for

2013.

Answer:

In 2013, KP Building Inc. began work on a four-year construction project (called Cincy

One). The contract price is $300 million. KP uses the percentage-of-completion method

of accounting. At the end of 2013, the following financial statement information

indicates the results to date for Cincy One:

Required: Compute the following, placing your answer in the spaces provided and

showing supporting computations below.

Answer:

The shareholders’ equity of Tru Corporation includes $600,000 of $1 par common stock

and $1,200,000 par value of 6% cumulative preferred stock. The board of directors of

Tru declared cash dividends of $150,000 in 2013 after paying $60,000 cash dividends

in each of 2012 and 2011.

Required:

What is the amount of dividends common shareholders will receive in 2013?

Answer:

Briefly discuss the factors that determine the service life of a depreciable asset.

Answer:

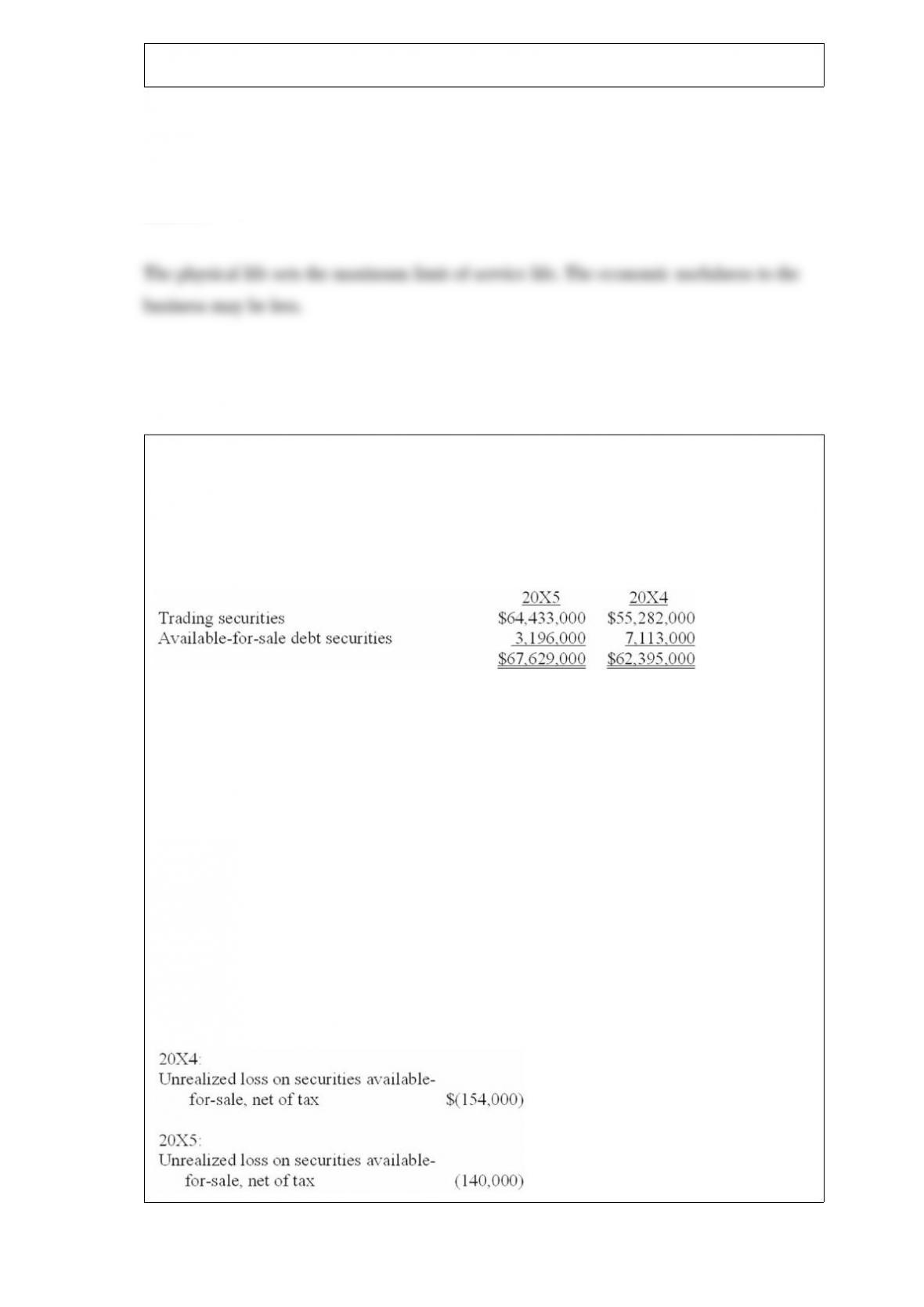

Arctic Cat Inc., the snowmobile manufacturer, reported the following in its 20X5

annual report to shareholders:

NOTE B – SHORT-TERM INVESTMENTS

Short-term investments consist primarily of a diversified portfolio of municipal bonds

and money market funds and are classified as follows at March 31:

Trading securities consist of $54,608,000 and $41,707,000 invested in various money

market funds at March 31, 20X5 and 20X4, respectively, while the remainder of trading

securities and available-for-sale securities consist primarily of A-rated or higher

municipal bond investments. The amortized cost and fair value of debt securities

classified as available-for-sale was $3,105,000 and $3,196,000, at March 31, 20X5. The

unrealized gain on available-for-sale debt securities is reported, net of tax, as a separate

component of shareholders’ equity.

Arctic Cat Inc.

CONSOLIDATED STATEMENTS OF SHAREHOLDERS’ EQUITY

Years Ended March 31,

Accumulated Other Comprehensive Income changed by the following amounts:

In its 20X4 annual report, Arctic Cat disclosed, “The contractual maturities of

available-for-sale debt securities at March 31, 20X4, are $3,573,000 within one year

and $3,340,000 from one year through five years.”

Assume Arctic Cat did not purchase any trading securities during 20X5. Write a journal

entry to record any unrealized holding gains or losses on trading securities during

20X5.

Answer:

How are customer advances and refundable deposits similar and yet different?

Answer:

On September 1, 2013, Jacob Furniture Mart enters into a tentative agreement to sell

the assets of its office equipment division. This division qualifies as a component of the

entity according to GAAP regarding discontinued operations. The division’s

contribution to Jacob’s operating income for 2013 was a $3 million loss before taxes.

Jacob has an average tax rate of 30%.

Required:

Consider independently the appropriate accounting by Jacob under the scenario below.

Scenario 3: Assume that Jacob had not yet sold the office furniture division by the end

of 2013. Further, assume that the fair value less costs to sell of the division’s assets at

December 31, 2013, was $12 million and was expected to remain the same when the

assets are sold in 2014. The book value of the division’s assets was $19 million at the

end of the year. Under these assumptions, what would Jacob report in its 2013 income

statement regarding the office equipment division? Explain where this information

would be presented.

Answer:

Briefly explain how a material adjustment to inventory due to application of the

lower-of-cost-or-market rule should be reported in the financial statements.

Answer:

In 2013, Chicago Construction began work on a three-year construction project to build

a new performing arts complex (the PAC). The PAC contract price is $150 million.

Chicago uses the percentage-of-completion method of accounting. At the end of 2013,

the following financial statement information indicates the results to date for the PAC:

Required: Compute the following, placing your answer in the spaces provided and

showing supporting computations below:

Answer:

On December 31, 2012, Jackson Company had 100,000 shares of common stock

outstanding and 30,000 shares of 7%, $50 par, cumulative preferred stock outstanding.

On February 28, 2013, Jackson purchased 24,000 shares of common stock on the open

market as treasury stock paying $45 per share. Jackson sold 6,000 of the treasury shares

on September 30, 2013, for $47 per share. Net income for 2013 was $180,905. Also

outstanding at December 31, 2012, were fully vested incentive stock options giving key

personnel the option to buy 50,000 common shares at $40. These stock options were

exercised on November 1, 2013. The market price of the common shares averaged $50

during

Required:

Compute Jackson’s basic and diluted earnings per share (rounded to 2 decimal places)

for 2013.

Answer:

On December 31, 2012, Brisbane Company had 100,000 shares of common stock

outstanding and 30,000 shares of 7%, $50 par, cumulative preferred stock outstanding.

On February 28, 2013, Brisbane purchased 24,000 shares of common stock on the open

market as treasury stock paying $40 per share. Brisbane sold 6,000 treasury shares on

September 30, 2013, for $45 per share. Net income for 2013 was $180,905. Also

outstanding during the year were fully vested incentive stock options giving key

personnel the option to buy 50,000 common shares at $40. The market price of the

common shares averaged $50 during 2013.

Required:

Compute Brisbane’s basic and diluted earnings per share (rounded to 2 decimal places)

for 2013.

Answer:

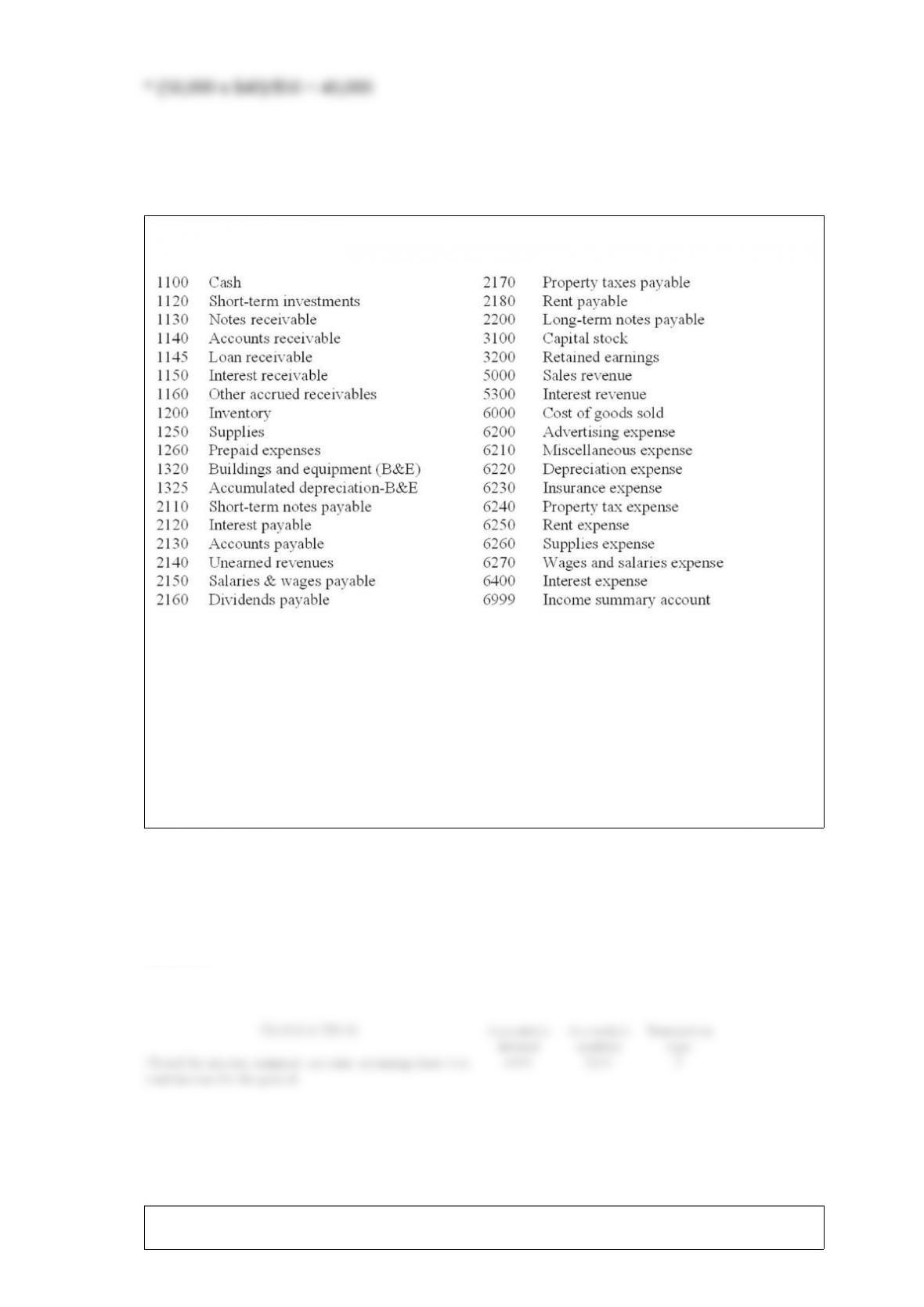

Using the chart of accounts provided, indicate by account number the account or

accounts that would be debited and credited in the following transactions and indicate

the type of transaction as: (1) an external transaction, (2) an internal transaction

recorded as an adjusting journal entry, or (3) a closing entry. The company uses a

perpetual inventory system. All prepayments are initially recorded in permanent

accounts.

Closed the income summary account, assuming there was a net income for the period.

Answer:

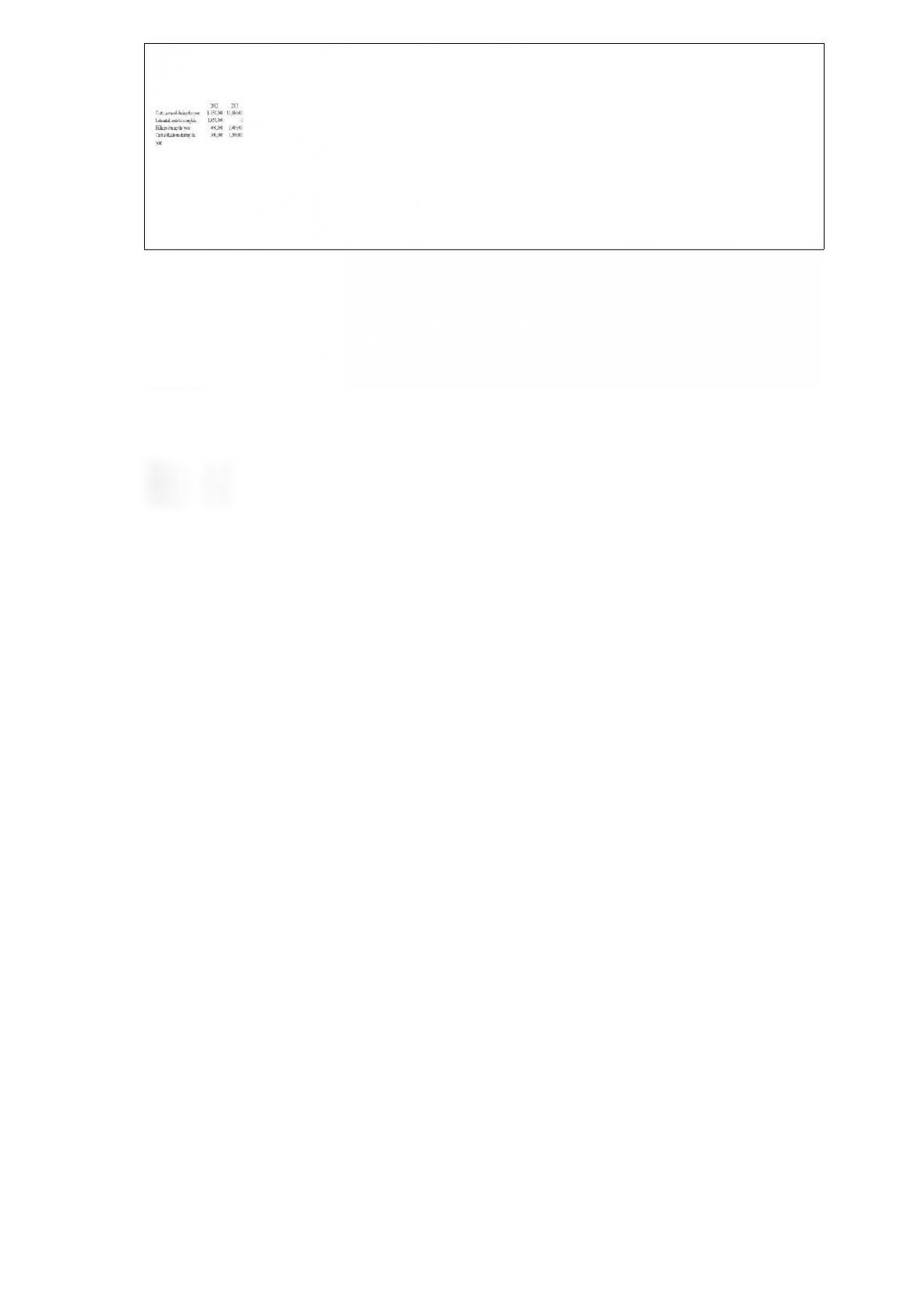

Beavis Construction Company was the low bidder on a construction project to build an

earthen dam for $1,800,000. The project was begun in 2012 and completed in 2013.

Cost and other data are presented below:

Assume that Beavis uses the percentage-of-completion method for revenue recognition.

Required: Prepare all journal entries to record costs, billings, collections, and profit

recognition.

Answer: