1) total interest cost for a bond issued at a premium equals the total of the periodic

interest payments minus the premium.

2) it is unlikely that a company would want to bond its employees who handle cash or

inventory.

3) an auditor is an accounting professional who conducts an independent examination

of the accounting data presented by a company.

4) the present value of a bond is a function of two variables: (1) the payment amounts

and (2) the discount rate.

5) for a t account, an account balance is the difference in total dollars between total

debit amounts and total credit amounts.

6) bond interest paid by a corporation is an expense, whereas dividends paid are not an

expense of the corporation.

7) trade receivables occur when two companies trade or exchange notes receivables.

8) a business is usually involved in two types of activityfinancing and investing.

9) comparisons of company data with industry averages provide information about a

company’s relative position within the industry.

10) the two key parties to a note are the maker and the payee.

11) the cumulative effect of the declaration and payment of a cash dividend on a

companys financial statements is to

a.decrease total liabilities and stockholders equity

b.increase total expenses and total liabilities

c.increase total assets and stockholders equity

d.decrease total assets and stockholders equity

12) if the equity method is being used, the revenue from investment in stock account is

a.just another name for a dividend revenue account

b.credited when dividends are declared by the investee

c.credited when net income is reported by the investee

d.debited when dividends are declared by the investee

13) what causes the balance on the bank statement to differ from the cash balance in the

general ledger?

a.time lags

b.errors by the bank

c.errors by the company

d.all of the above

14) posting

a.transfers journal entries to ledger accounts.

b.transfers ledger transaction data to the journal.

c.involves transferring all debits and credits on a journal page to the trial balance.

d.provides a chronological record of transactions.

15) dominic’s salon has total receipts for the month of $20,140 including sales taxes. if

the sales tax rate is 6%, what are dominic’s sales for the month?

a.$18,932.20

b.$21,348.80

c.$19,000.00

d.it cannot be determined

16) when sales of merchandise are made for cash, the transaction may be recorded by

the following entry

a.debit sales revenue, credit cash

b.debit cash, credit sales

c.debit sales revenue, credit cash discounts

d.debit sales revenue, credit sales returns and allowances

17) danley corporation began business by issuing 100,000 shares of $5 par value

common stock for $24 per share. during its first year, the corporation sustained a net

loss of $20,000. the year-end balance sheet would show

a.common stock of $500,000

b.common stock of $2,400,000

c.total paid-in capital of $2,380,000

d.total paid-in capital of $1,900,000

18) jeremy snow invested $16,000 at 8% annual interest and left the money invested

without withdrawing any of the interest for 15 years. at the end of the 15 years, jeremy

withdrew the accumulated amount of money. what amount did jeremy withdraw,

assuming the investment earns simple interest?

a.$19,200

b.$35,200

c.$30,000

d.$17,600

19) grayson company purchased merchandise with an invoice price of $2,000 and credit

terms of 1/10, n/30. assuming a 360 day year, what is the implied annual interest rate

inherent in the credit terms?

a.1%

b.6%

c.12%

d18%

20) which of the following are the same under both gaap and ifrs?

a.the journal.

b.the ledger.

c.the chart of accounts.

d.all of these answer choices are correct.

21) a trial balance will not balance if

a.a correcting journal entry is posted twice.

b.a $50 cash dividend is debited to dividends for $500 and credit to cash for $50.

c.a $300 payment on accounts payable is debited to accounts payable for $30 and

credited to cash for $30.

d.a transaction is not posted at all.

22) all of the following statements regarding impairments are true except

a.an impairment is a permanent decline in an asset’s market value

b.after an impairment write-down, depreciation is generally lower in a subsequent

periods

c.immediate recognition of impairment write-downs is now required

d.impairments are generally recorded when the book value falls below the market value

23) ifrs allows companies to revalue plant assets to fair value. when an asset has

increased in value, where is the account “revaluation surplus” reported?

a.on the income statement as part of income from continuing operations (other revenues

and gains)

b.on the income statement as part of discontinued operations (discontinuing historical

cost)

c.on the statement of financial position as part of accumulated comprehensive income

(equity)

d.all of the choices are acceptable methods for the reporting of “revaluation surplus”

24) which one of the following would not be considered an advantage of the corporate

form of organization?

a.limited liability of stockholders

b.separate legal existence

c.continuous life

d.government regulation

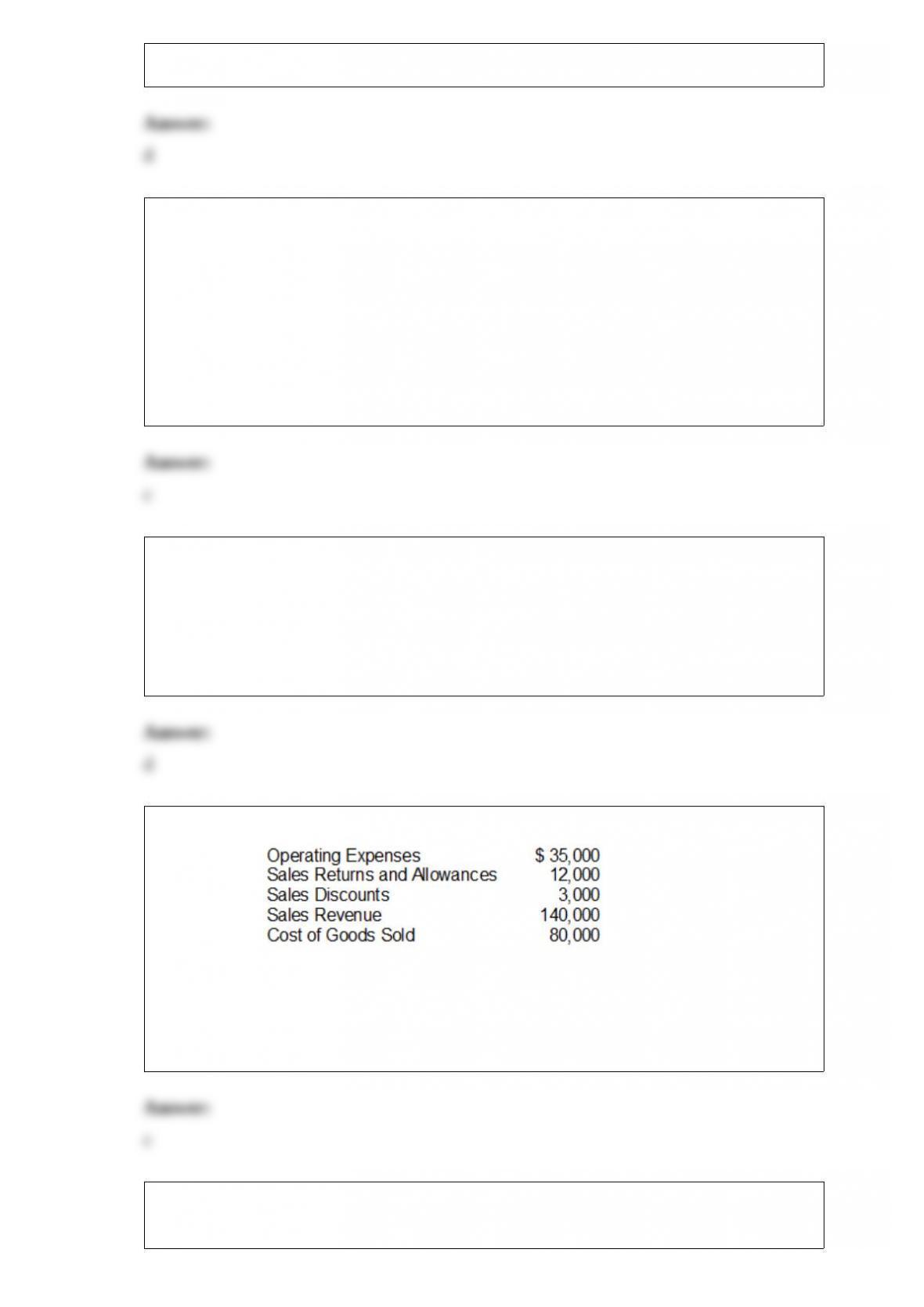

25) financial information is presented below:

the gross profit rate would be

a..64

b..43

c..36

d..32

26) weaver company purchased treasury stock with a cost of $15,000 during 2012.

during the year, the company paid dividends of $20,000 and issued bonds payable for

proceeds of $836,000. cash flows from financing activities for 2012 total

a.$816,000 net cash inflow

b.$831,000 net cash inflow

c.$5,000 net cash outflow

d.$801,000 net cash inflow

27) the interest on a $9,000, 6%, 60-day note receivable is

a.$45

b.$540

c.$270

d.$90

28) collins company borrowed $500,000 from banktwo on january 1, 2011 in order to

expand its mining capabilities. the five-year note required annual payments of $130,218

and carried an annual interest rate of 9.5%. what is the amount of expense collins must

recognize on its 2012 income statement?

a.$47,500

b.$39,642

c.$35,129

d.$31,037

29) mitchell corporation bought equipment on january 1, 2012 .the equipment cost

$120,000 and had an expected salvage value of $20,000. the life of the equipment was

estimated to be 6 years. the book value of the equipment at the beginning of the third

year would be

a.$120,000

b.$100,000

c.$86,667

d.$33,333

30) three important dates associated with dividends are the: (1)___________________,

(2)__________________, and (3)__________________.

31) for each of the following accounts indicate the effect of a debit or a credit on the

account and the normal balance. increase (+), decrease (-).

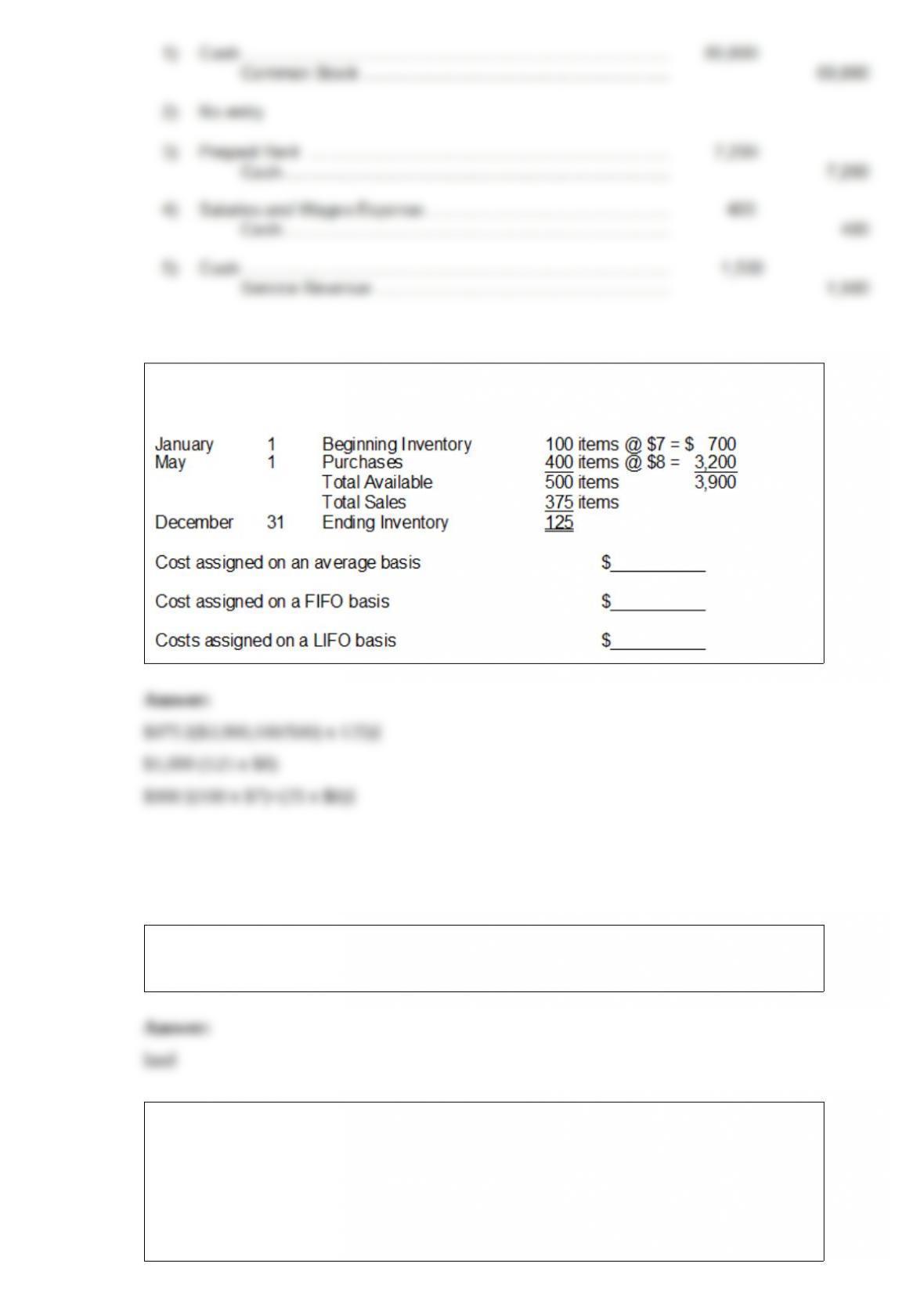

32) compute the cost to be assigned to ending inventory for each of the methods

indicated given the following information about purchases and sales during the year.

33) the cost of demolishing an old building on land that has been acquired so that a new

building can be constructed should be charged to the ______________ account.

34) dennis lee, an auditor with knapp cpas, is performing a review of dobson company’s

inventory account. dobson did not have a good year, and top management is under

pressure to boost reported income. according to its records, the inventory balance at

year-end was $640,000. however, the following information was not considered when

determining that amount.

1>included in the company’s count were goods with a cost of $200,000 that the

company is holding on consignment. the goods belong to agler corporation.

2>the physical count did not include goods purchased by dobson with a cost of $40,000

that were shipped fob shipping point on december 28 and did not arrive at dobson’s

warehouse until january 3.

3>included in the inventory account was $22,000 of office supplies that were stored in

the warehouse and were to be used by the company’s supervisors and managers during

the coming year.

4>the company received an order on december 29 that was boxed and was sitting on the

loading dock awaiting pick-up on december 31. the shipper picked up the goods on

january 1 and delivered them on january 6. the shipping terms were fob shipping point.

the goods had a selling price of $40,000 and a cost of $30,000. the goods were not

included in the count because they were sitting on the dock.

5>on december 29, dobson shipped goods with a selling price of $90,000 and a cost of

$60,000 to central sales corporation fob shipping point. the goods arrived on january 3.

central sales had only ordered goods with a selling price of $10,000 and a cost of

$7,000. however, a sales manager at dobson had authorized the shipment and said that if

central wanted to ship the goods back next week, it could.

6>included in the count was $50,000 of goods that were parts for a machine that the

company no longer made. given the high-tech nature of dobson’s products, it was

unlikely that these obsolete parts had any other use. however, management would prefer

to keep them on the books at cost, ‘since that is what we paid for them, after all.”

prepare a schedule to determine the correct inventory amount. provide explanations for

each item above, saying why you did or did not make an adjustment for each item.