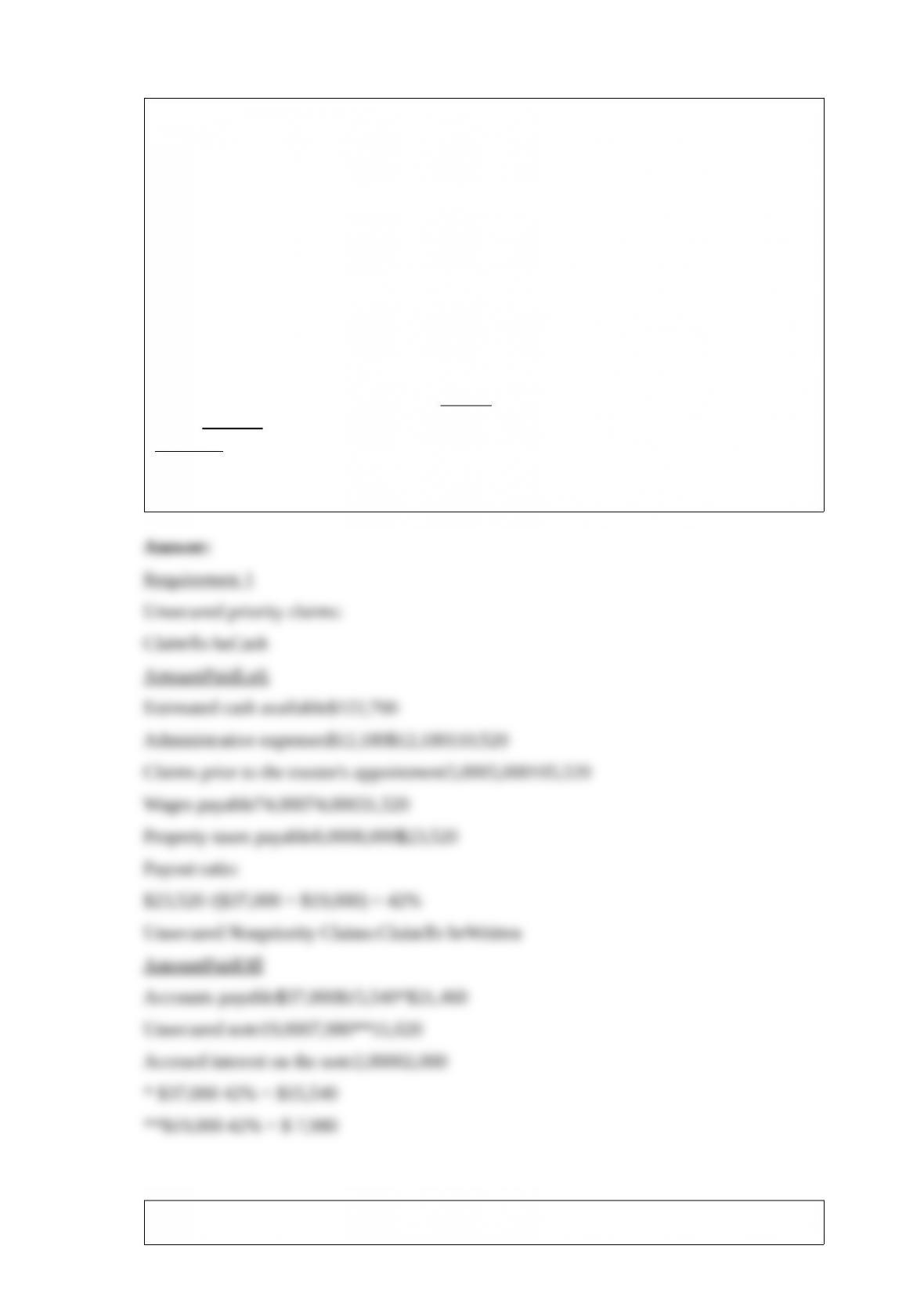

1) Kline Corporation incurred major losses in 2011 and entered into voluntary Chapter

7 bankruptcy in the early part of 2012 . By July 1, all assets were converted into cash,

the secured creditors were paid, and $122,700 in cash was left to pay the remaining

claims as follows:

Accounts payable$37,000

Claims incurred between the date of filing an involuntary5,000

petition and the date an interim trustee is appointed

Property taxes payable8,000

Wages payable (all under $10,000 per employee; 74,000

earned within 90 days of filing bankruptcy petition)

Unsecured note payable19,000

Accrued interest on the note payable2,000

Administrative expenses of the trustee12,180

Total$157,180

Required:

Classify the claims by their Chapter 7 priority ranking, and analyze which amounts will

be paid and which amounts will be written off.

2) Prepare journal entries in an Internal Service Fund of Union County to record each of

the following transactions.

1>Purchased equipment on September 1, 2011 by paying $25,000 down and borrowing

$100,000 on a 6%, 2-year note.

2>In 2011, billed General Fund $620,000 for services provided. Billings to the

Enterprise Fund totaled $165,000. All billings were collected by December 31, 2011

except for $100,000 charged to the General Fund.

3>Accrued year-end adjustments at December 31, 2011 for interest expense and

depreciation. The useful life of the equipment is 5 years with no salvage value.

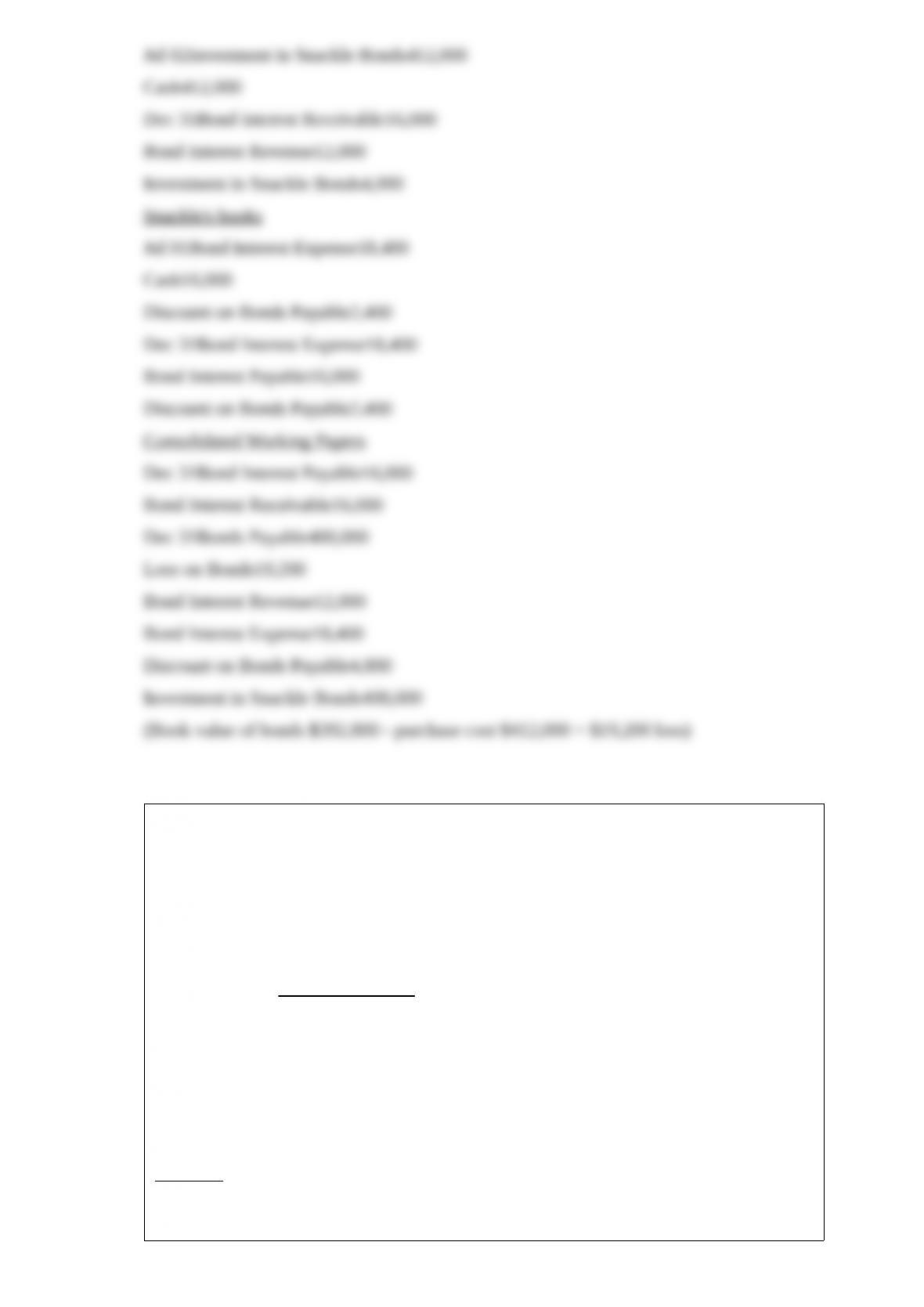

3) Snackle Inc. is a 90%-owned subsidiary of Pasha Corp. On January 1, 2010, Snackle

issued $400,000 of $1,000 face amount 8% bonds at $964 per bond. Interest is paid on

January 1 and July 1 of each year and covers the preceding six months. On July 2, 2011,

Pasha purchased all 400 bonds on the open market for $1,030 per bond. The bonds

mature on December 31, 2012 . Both companies use straight-line amortization.

Required:

With respect to the bonds, use General Journal format to:

1>Record the 2011 journal entries from July 1 to December 31 on Pasha’s books.

2>Record the 2011 journal entries from July 1 to December 31 on Snackle’s books.

3>Record the elimination entries for the consolidation working papers for the year

ending December 31, 2011 .

4) Daniel, Ethan, and Frank have a retail partnership business selling personal

computers. The partners are allowed an interest allocation of 8% on their average

capital. Capital account balances on the first day of each month are used in determining

weighted average capital, regardless of additional partner investment or withdrawal

transactions during any given month. Withdrawals of capital that are debited to the

capital account are used in the average calculation. Partner capital activity for the year

was:

Capital accountsDanielEthanFrank

Jan 1 balance$ 200,000$ 300,000$ 250,000

Feb 2 investment50,000

Mar 6 investment10,00020,000

Apr 20 withdrawal(10,000)

Jul 3 withdrawal and investment(7,000)10,000

Sep 29 investment5,0004,0005,000

Nov 5 investment5,000

Required:

Calculate weighted average capital for each partner, and determine the amount of

interest that each partner will be allocated. Round all calculations to the nearest whole

dollar.

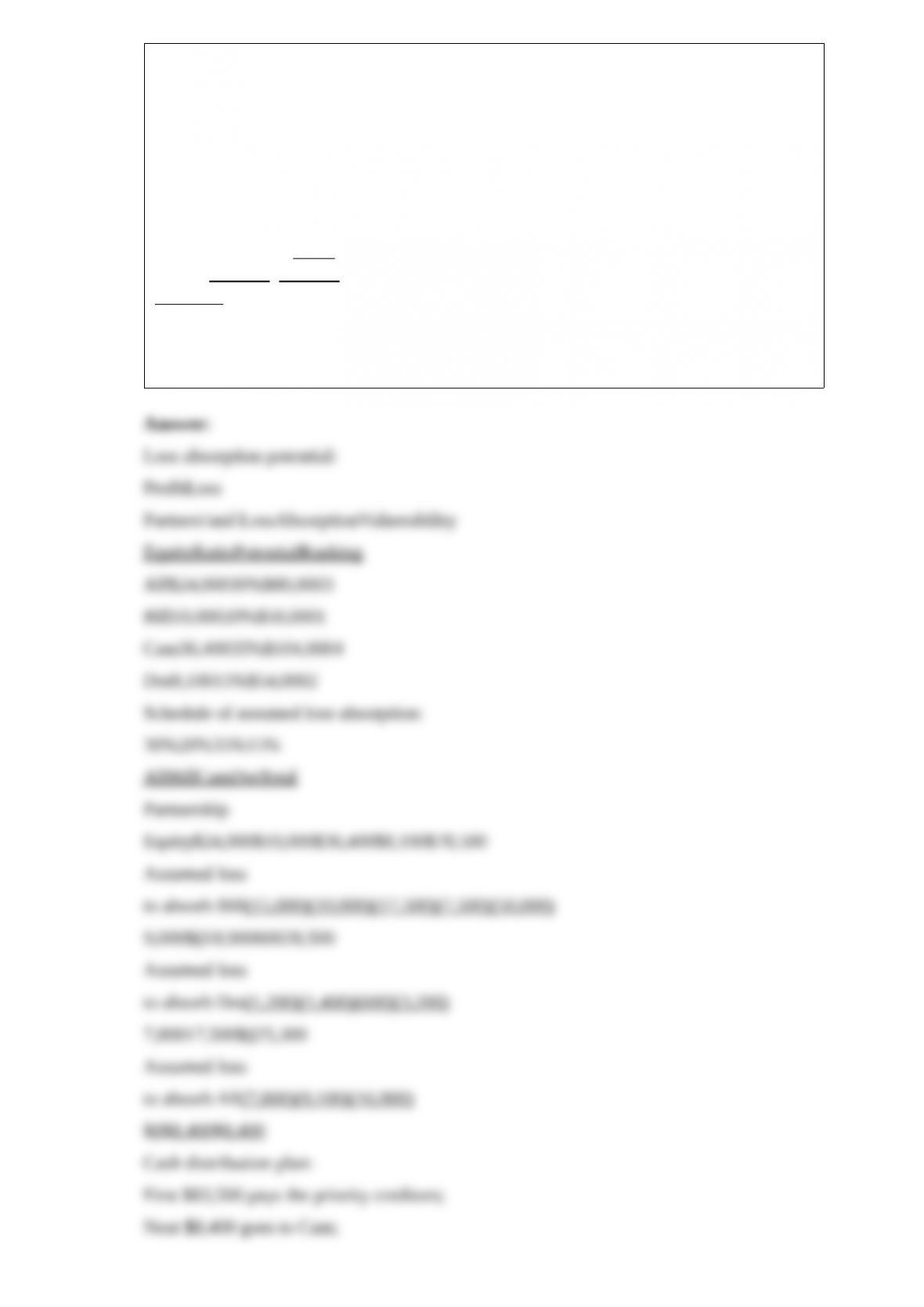

5) Alf, Bill, Cam, and Dot are partners who share profits and losses 30%, 20%, 35%,

and 15%, respectively. The partnership will be liquidated gradually over several months

beginning January 1, 2011 . The partnership trial balance at December 31, 2010 is as

follows:

DebitsCredits

Cash$6,000

Accounts receivable20,000

Inventory50,000

Loan to Bill8,000

Furniture30,000

Equipment36,000

Goodwill20,000

Accounts payable$23,500

Note payable60,000

Loan from Cam12,400

Alf, capital (30%)24,000

Bill, capital (20%)18,000

Cam, capital (35%)24,000

Dot, capital (15%)8,100

Totals$170,000$170,000

Required:

Prepare a cash distribution plan for January 1, 2011, showing how cash installments

will be distributed among the partners as it becomes available. Prepare vulnerability

rankings for the partners and a schedule of assumed loss absorption.