1) If the company bases its predetermined overhead rate on the estimated amount of the

allocation base for the upcoming year, by how much was manufacturing overhead

underapplied or overapplied?

The management of Richbourg Corporation would like to investigate the possibility of

basing its predetermined overhead rate on activity at capacity. The company’s controller

has provided an example to illustrate how this new system would work. In this

example, the allocation base is machine-hours and the estimated amount of the

allocation base for the upcoming year is 63,000 machine-hours. In addition, capacity is

70,000 machine-hours and the actual level of activity for the year is 66,200

machine-hours. All of the manufacturing overhead is fixed and is $2,866,500 per year.

For simplicity, it is assumed that this is the estimated manufacturing overhead for the

year as well as the manufacturing overhead at capacity. It is further assumed that this is

also the actual amount of manufacturing overhead for the year.

A.$87,232 Underapplied

B.$27,648 Underapplied

C.$27,648 Overapplied

D.$87,232 Overapplied

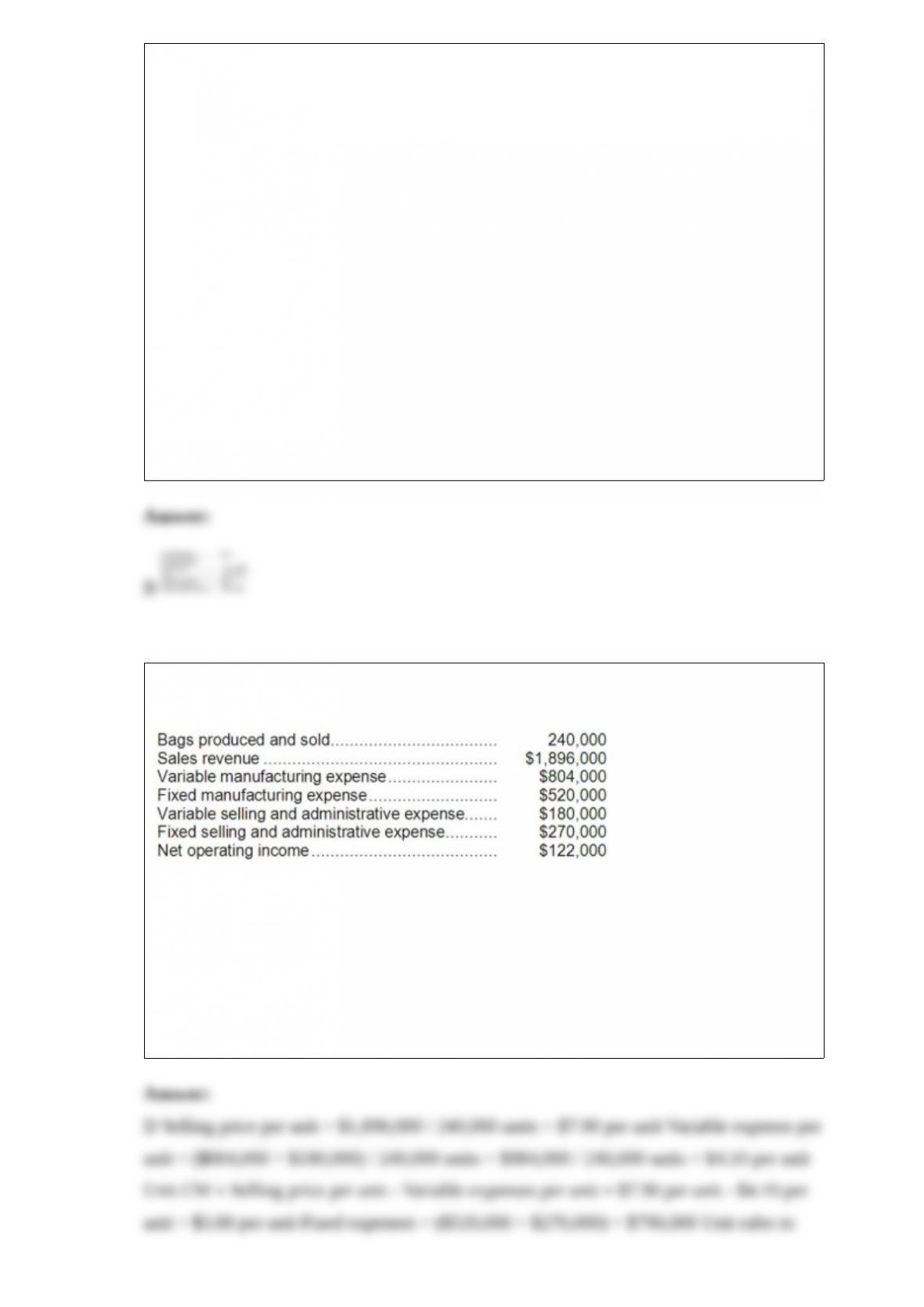

2) A company that makes organic fertilizer has supplied the following data:

The company’s margin of safety in units is closest to:

A.140,000 units

B.202,238 units

C.125,714 units

D.32,105 units

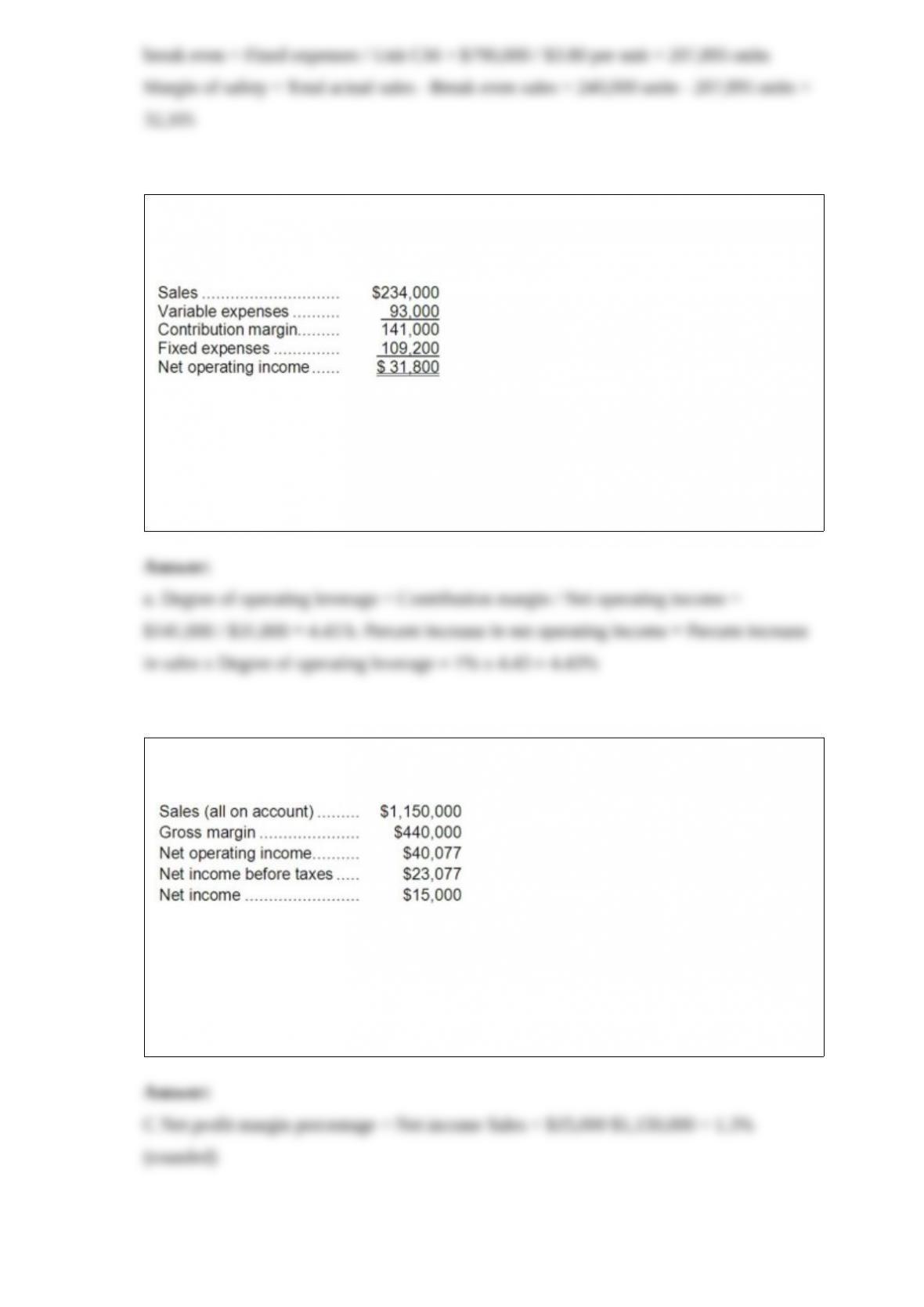

3) Eickhoff Corporation’s contribution format income statement for the most recent

month follows:

Required:

a. Compute the degree of operating leverage to two decimal places.

b. Using the degree of operating leverage, estimate the percentage change in net

operating income that should result from a 1% increase in sales.

4) Valdovinos Corporation has provided the following data:

The company’s net profit margin percentage is closest to:

A.38.3%

B.3.5%

C.1.3%

D.2.0%

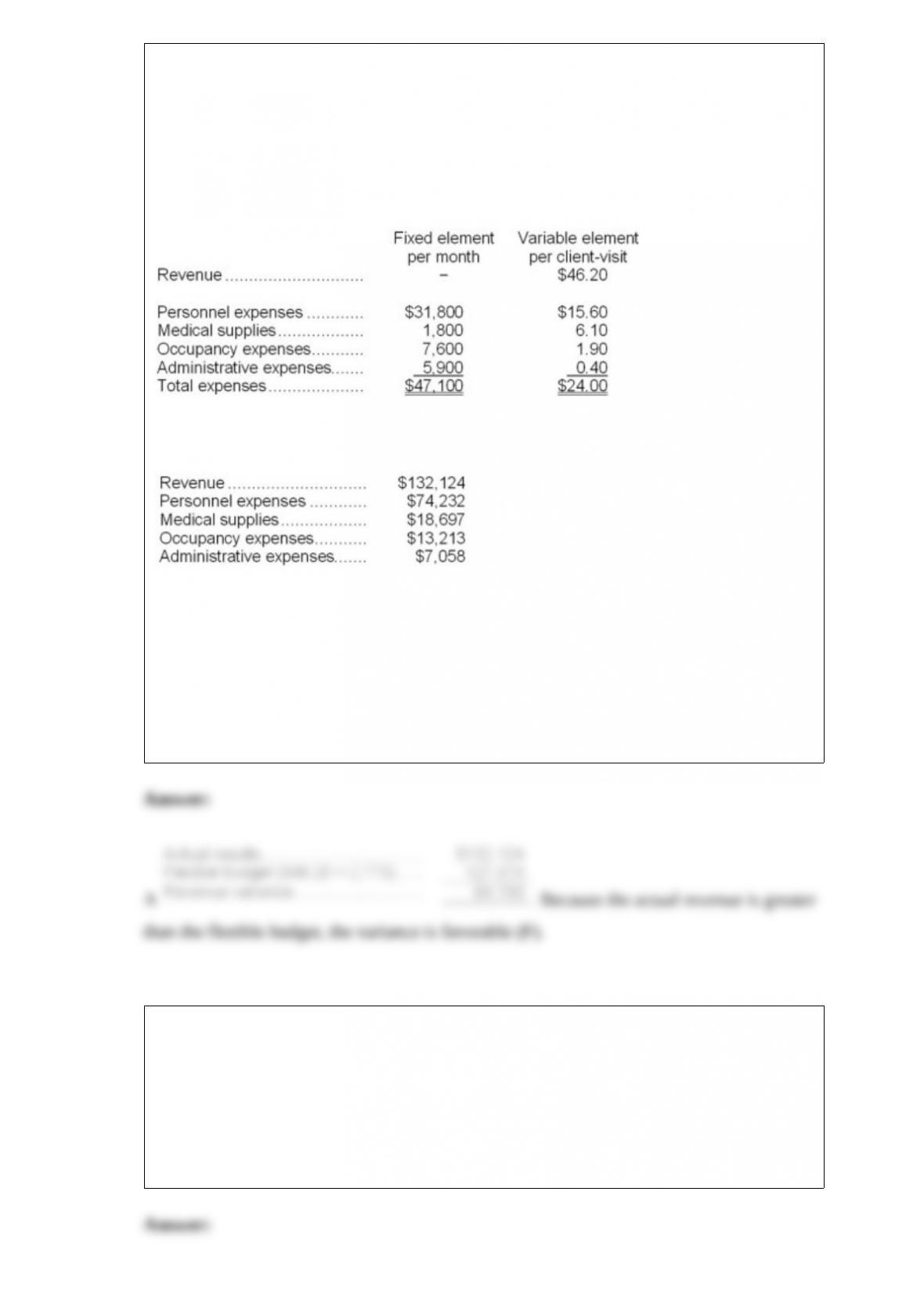

5) Buonocore Clinic uses client-visits as its measure of activity. During August, the

clinic budgeted for 2,800 client-visits, but its actual level of activity was 2,770

client-visits. The clinic has provided the following data concerning the formulas used in

its budgeting and its actual results for August:

Data used in budgeting:

Actual results for August:

The revenue variance for August would be closest to:

A.$4,150 F

B.$2,764 F

C.$2,764 U

D.$4,150 U

6) Management is considering a one-time-only special order. There is sufficient idle

capacity to fill the order without affecting any normal sales. Which one of the following

is NOT relevant in making the decision?

A.absorption costing unit product costs

B.variable costs

C.incremental costs

D.differential costs

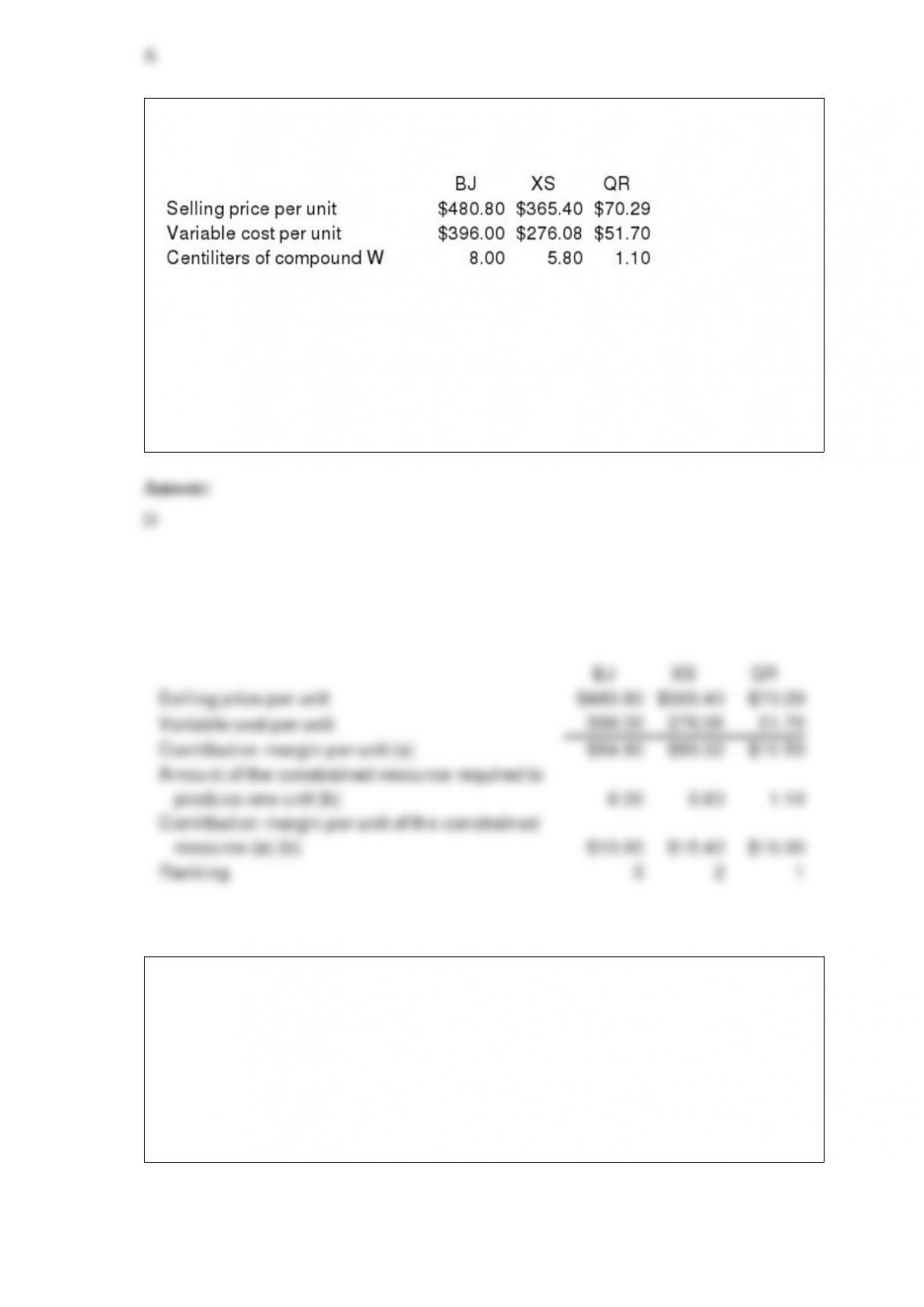

7) Fahringer Corporation makes three products that use compound W, the current

constrained resource. Data concerning those products appear below:

Rank the products in order of their current profitability from most profitable to least

profitable. In other words, rank the products in the order in which they should be

emphasized.

A) XS,BJ,QR

B) QR,BJ,XS

C) BJ,QR,XS

D) QR,XS,BJ

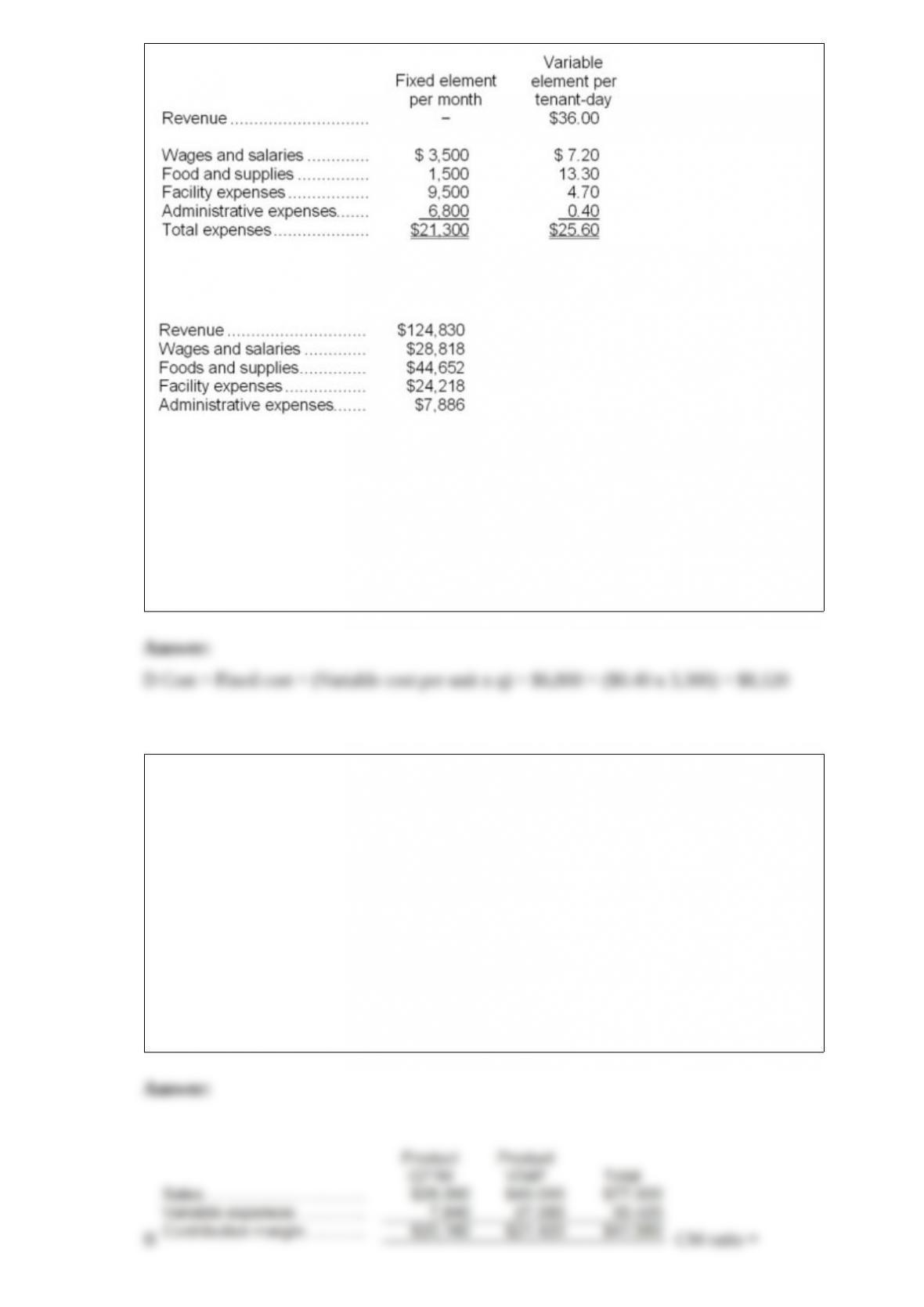

8) Vanderhyde Kennel uses tenant-days as its measure of activity; an animal housed in

the kennel for one day is counted as one tenant-day. During May, the kennel budgeted

for 3,300 tenant-days, but its actual level of activity was 3,340 tenant-days. The kennel

has provided the following data concerning the formulas used in its budgeting and its

actual results for May:

Data used in budgeting:

Actual results for May:

The administrative expenses in the planning budget for May would be closest to:

A.$7,792

B.$7,886

C.$8,136

D.$8,120

9) Gilpatric Corporation produces and sells two products. In the most recent month,

Product Q71M had sales of $28,000 and variable expenses of $7,840. Product V04P

had sales of $49,000 and variable expenses of $27,580. The fixed expenses of the entire

company were $34,630.

The break-even point for the entire company is closest to:

A.$70,050

B.$64,130

C.$34,630

D.$42,370

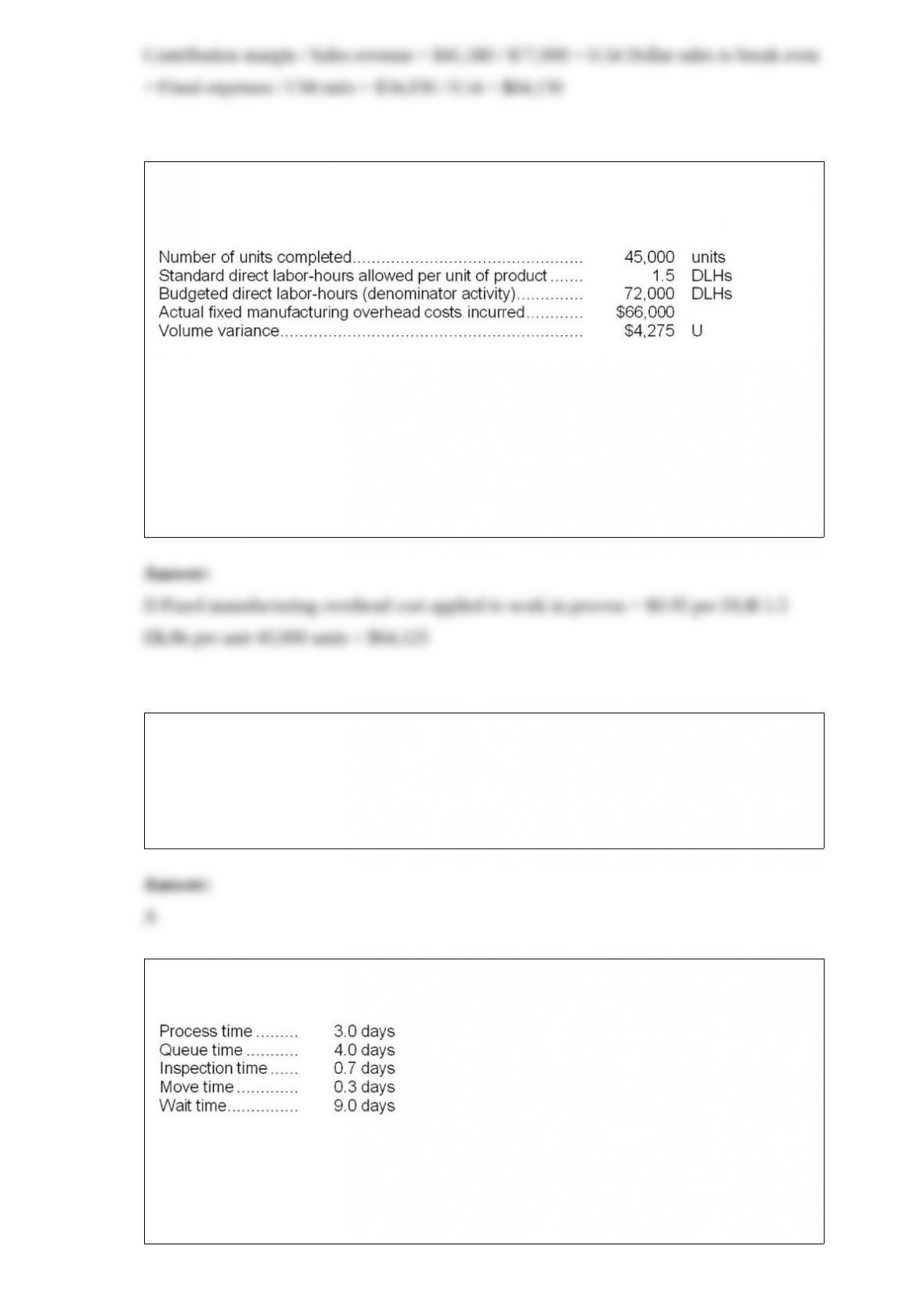

10) The Murray Corporation makes and sells a single product. The company recorded

the following activity and cost data for May:

The fixed component of the predetermined overhead rate is $0.95 per direct labor-hour.

The amount of fixed manufacturing overhead cost applied to work in process during

May was:

A.$61,725

B.$62,700

C.$42,750

D.$64,125

11) Assembling a product is an example of a:

A.Unit-level activity.

B.Batch-level activity.

C.Product-level activity.

D.Organization-sustaining.

12) Ricric Corporation has provided the following data for one of its products:

The delivery cycle time for this operation is:

A.8 days

B.17 days

C.9.3 days

D.7.7 days

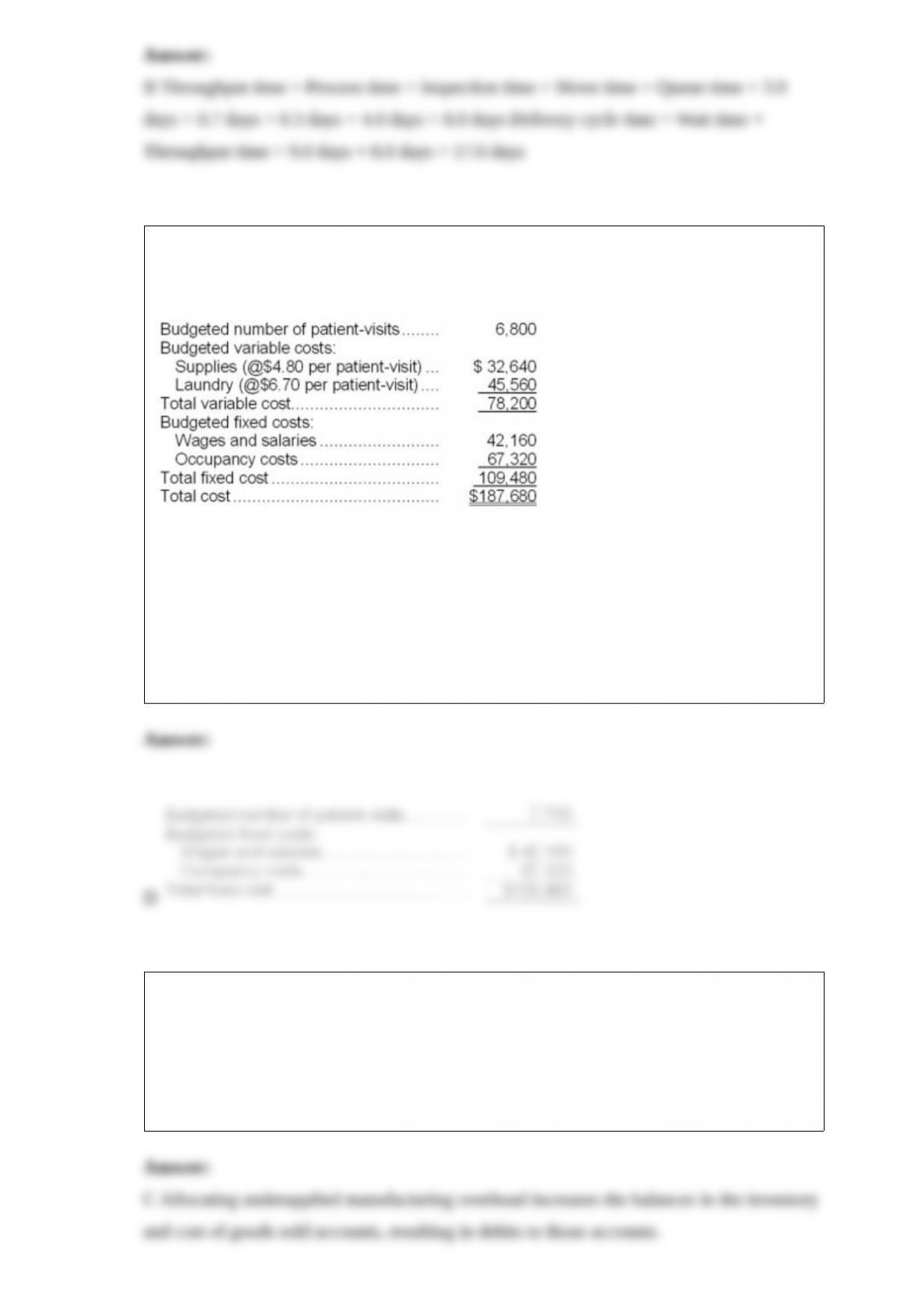

13) Hettinger Hospital bases its budgets on patient-visits. The hospital’s static budget

for March appears below:

The total fixed cost at the activity level of 7,700 patient-visits per month should be:

A.$123,970

B.$187,680

C.$212,520

D.$109,480

14) The journal entry to record the allocation of any underapplied or overapplied

manufacturing overhead for November would include the following:

A.debit to Work in Process of $16,240

B.credit to Work in Process of $16,240

C.debit to Work in Process of $180

D.credit to Work in Process of $180

15) Bruley Corporation applies manufacturing overhead to products on the basis of

standard machine-hours. The company’s predetermined overhead rate for fixed

manufacturing overhead is $3.30 per machine-hour and the denominator level of

activity is 3,500 machine-hours. In the most recent month, the total actual fixed

manufacturing overhead was $11,570 and the company actually worked 3,430

machine-hours during the month. The standard hours allowed for the actual output of

the month totaled 3,450 machine-hours. What was the overall fixed manufacturing

overhead volume variance for the month?

A.$66 Favorable

B.$231 Favorable

C.$231 Unfavorable

D.$165 Unfavorable

16) The company’s average collection period (age of receivables) for Year 2 is closest

to:

A.1.1 days

B.28.2 days

C.1.0 days

D.27.9 days

17) What would be the average fixed maintenance cost per unit at an activity level of

8,600 machine-hours in a month? Assume that this level of activity is within the

relevant range.

A) $93.64

B) $67.08

C) $64.74

D) $75.15

18) ( Betterway Pharmacy has purchased a small auto for delivery of prescriptions. The

auto cost $30,000 and will be usable for five years. Delivery of prescriptions (which the

pharmacy has never done before) should increase revenues by at least $29,000 per year.

The cost of these prescriptions will be about $21,000 per year. The pharmacy

depreciates all assets by the straight-line method.

Required:

a. Compute the payback period on the new auto.

b. Compute the simple rate of return of the new auto.